Key Insights

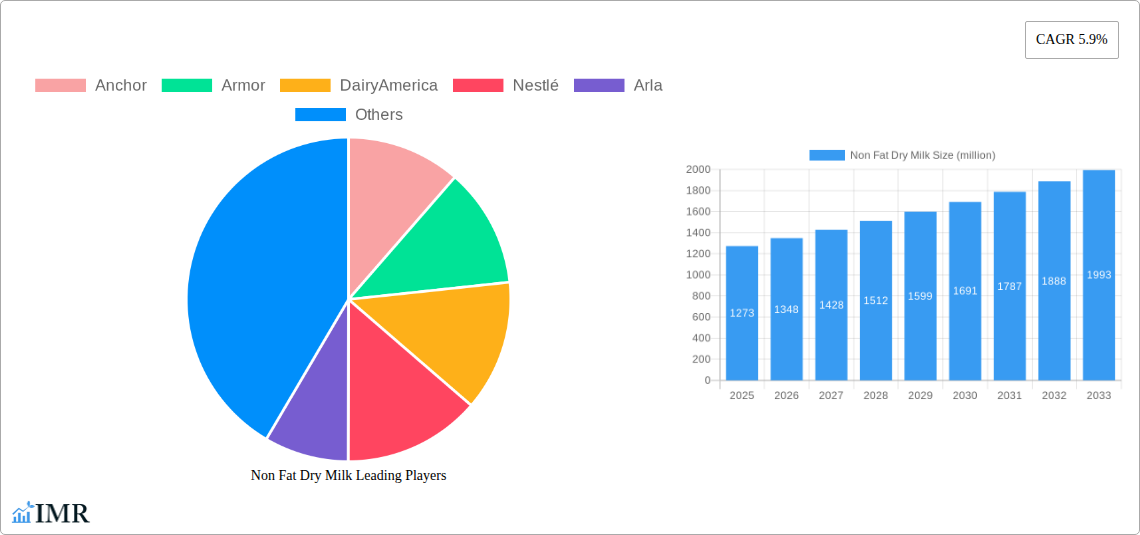

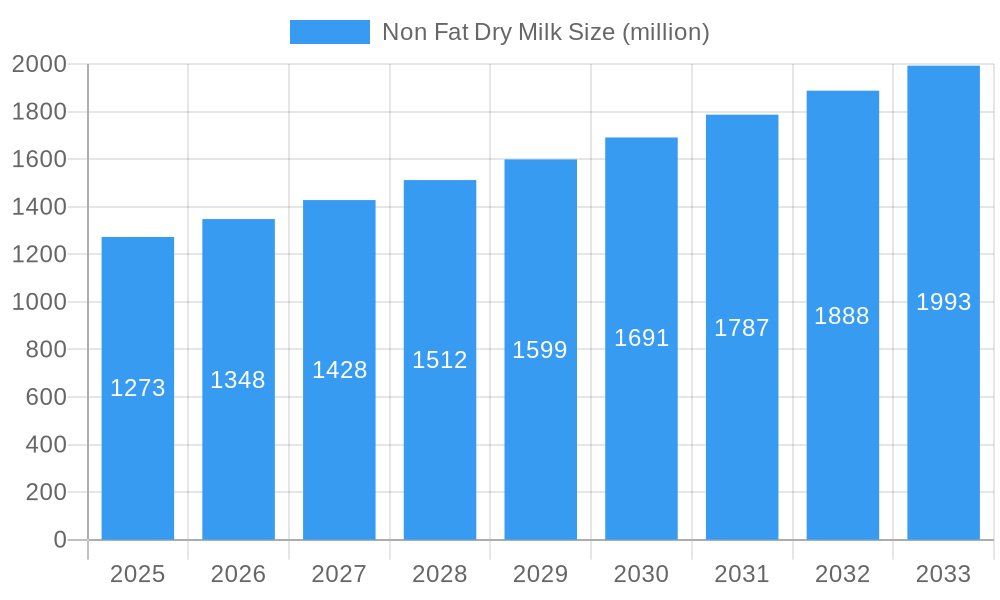

The global Non-Fat Dry Milk (NFDM) market is poised for substantial growth, with a current market size estimated at USD 1273 million and projected to expand at a Compound Annual Growth Rate (CAGR) of 5.9% from 2025 to 2033. This robust expansion is fueled by a confluence of favorable factors, primarily driven by the escalating demand for dairy-based ingredients across diverse food and beverage applications. The bakery and confectionery sector, a significant consumer of NFDM for its functional properties like emulsification, browning, and texture enhancement, continues to be a primary growth engine. Furthermore, the burgeoning popularity of convenient and healthy dessert options, coupled with the consistent demand from the ice cream and dairy blends industries, further underpins the market's upward trajectory. NFDM's versatility, cost-effectiveness, and extended shelf life compared to liquid milk make it an indispensable ingredient for manufacturers seeking to optimize production processes and product quality.

Non Fat Dry Milk Market Size (In Billion)

Emerging trends and evolving consumer preferences are also playing a crucial role in shaping the NFDM market landscape. A growing emphasis on healthier food choices, characterized by reduced fat content, directly benefits NFDM, a naturally low-fat dairy product. This aligns with global health and wellness trends, pushing consumers and food manufacturers towards ingredients that offer nutritional benefits without compromising on taste or functionality. While the market enjoys strong growth drivers, potential challenges such as fluctuating raw milk prices and increasing competition from alternative protein sources necessitate strategic navigation by market players. However, the inherent nutritional profile, extensive applications, and ongoing innovation in product development within the NFDM sector are expected to outweigh these restraints, ensuring sustained market vitality and expansion in the coming years.

Non Fat Dry Milk Company Market Share

Here is the SEO-optimized report description for Non Fat Dry Milk, adhering to all your specifications.

Non Fat Dry Milk Market Dynamics & Structure

The global Non Fat Dry Milk (NFDM) market exhibits a moderately concentrated structure, with a few key players commanding significant market share. Technological innovation is primarily driven by advancements in drying processes that enhance product shelf-life, solubility, and nutritional content, meeting stringent food ingredient and dairy powder industry standards. Regulatory frameworks, particularly concerning food safety, labeling, and import/export of dairy products, play a crucial role in shaping market entry and operational strategies. Competitive product substitutes, such as whey protein concentrate and soy-based milk powders, present ongoing challenges, albeit NFDM's unique functionalities in bakery ingredients and dairy blends maintain its distinct market position. End-user demographics are increasingly influenced by a growing demand for convenient, shelf-stable food products and fortified nutritional supplements. Mergers and acquisitions (M&A) trends are observed as companies seek to expand their product portfolios, gain access to new geographical markets, and achieve economies of scale.

- Market Concentration: Dominated by a mix of large dairy cooperatives and multinational food corporations.

- Technological Innovation Drivers: Improved spray drying techniques, agglomeration for better reconstitution, and enhanced nutritional fortification.

- Regulatory Frameworks: Stringent food safety regulations (e.g., FDA, EFSA) and international trade agreements impact market access.

- Competitive Product Substitutes: Whey protein, plant-based milk powders, and other functional dairy ingredients.

- End-User Demographics: Rising demand from developing economies, health-conscious consumers, and the food processing industry.

- M&A Trends: Strategic acquisitions to consolidate market presence and diversify product offerings.

Non Fat Dry Milk Growth Trends & Insights

The Non Fat Dry Milk (NFDM) market is poised for robust growth, driven by an escalating demand for versatile and nutritious dairy ingredients across various food applications. The global dairy market is experiencing a significant uplift, with NFDM at its forefront due to its cost-effectiveness and functional properties. Market size evolution indicates a steady upward trajectory, projected to reach approximately $XX billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of XX% from the base year of 2025. Adoption rates of NFDM are particularly high in emerging economies, where it serves as an affordable and accessible source of essential nutrients, contributing to food security initiatives. Technological disruptions are focused on optimizing production efficiency and enhancing product quality, such as developing NFDM with improved heat stability for processed foods. Consumer behavior shifts are a key influencer, with an increasing preference for convenience foods, ready-to-drink beverages, and fortified nutritional products, all of which widely utilize NFDM. The food and beverage industry's growing reliance on shelf-stable ingredients further fuels this trend. Penetration of NFDM in the infant formula and sports nutrition segments is also on the rise, signaling a diversification of its application base beyond traditional uses. The dairy ingredients sector is experiencing transformative growth, with NFDM playing a pivotal role in meeting evolving dietary needs and industrial demands. The expanding food processing industry is a primary driver, leveraging NFDM for its emulsifying, binding, and browning properties in confectionery ingredients and bakery products. The overall food supply chain benefits from the stability and extended shelf-life offered by NFDM, reducing waste and ensuring consistent product quality. This sustained demand, coupled with ongoing innovation, solidifies NFDM's position as a cornerstone in the modern food landscape. The report anticipates a significant increase in the utilization of NFDM within the dairy alternatives sector as well, as manufacturers seek to enhance texture and nutritional profiles.

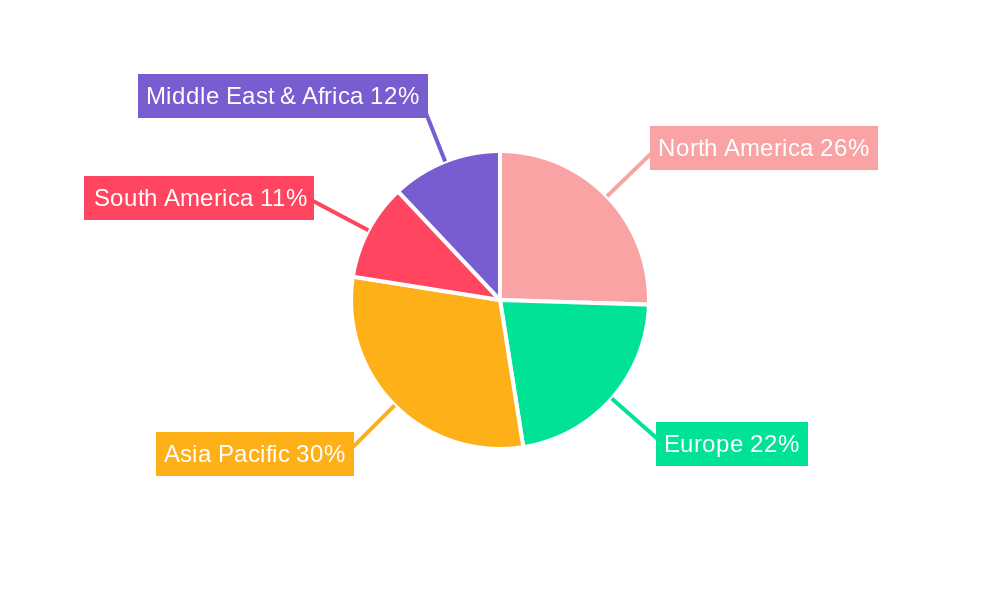

Dominant Regions, Countries, or Segments in Non Fat Dry Milk

The North America region, particularly the United States, is a dominant force in the global Non Fat Dry Milk (NFDM) market, driven by a well-established dairy infrastructure and a strong demand from its expansive food processing industry. The application segment of Bakery and Confectionery stands out as a primary growth engine, accounting for a substantial market share. This dominance is fueled by the extensive use of NFDM in bread, cakes, cookies, and various sweet treats, where its properties contribute to texture, browning, and shelf-life.

Dominant Region: North America (USA and Canada)

- Key Drivers: Advanced dairy processing technology, high consumer spending on processed foods, strong export capabilities, and supportive agricultural policies.

- Market Share: North America is estimated to hold XX% of the global NFDM market share in the base year.

- Growth Potential: Moderate but stable growth, driven by product innovation and consistent demand from the food industry.

Dominant Country: United States

- Economic Policies: Government subsidies and trade agreements favor dairy production and export.

- Infrastructure: Highly developed supply chains and logistics networks ensure efficient distribution.

- Consumer Demand: High per capita consumption of dairy products and processed foods.

Dominant Application Segment: Bakery and Confectionery

- Market Share: This segment is projected to account for approximately XX% of the total NFDM market by 2025.

- Key Drivers: Its crucial role in enhancing the flavor, texture, and shelf-life of a wide range of baked goods and confectionery items. The versatility of NFDM allows for its use in both industrial and artisanal production.

- Growth Potential: Continuous growth is expected due to the ongoing popularity of convenience foods and the global expansion of the bakery and confectionery industries.

Dominant Type: Medium-Heat NFDM

- Rationale: Offers a balance of functionality and cost-effectiveness, making it suitable for a broad spectrum of applications, especially in baking ingredients where heat stability is important but not to the extreme levels required for certain dairy blends.

- Growth Potential: Steady demand, with potential for growth in newer product formulations.

The dominance of North America and the Bakery and Confectionery segment highlights the mature yet consistently growing nature of NFDM demand in these areas. Future growth will likely see increased contributions from other regions and segments as global food consumption patterns evolve.

Non Fat Dry Milk Product Landscape

The Non Fat Dry Milk (NFDM) product landscape is characterized by continuous innovation aimed at enhancing functional properties and expanding application possibilities. Manufacturers are increasingly focusing on producing NFDM with improved solubility, heat stability, and emulsifying capabilities, catering to sophisticated food ingredient demands. Developments in spray drying and agglomeration technologies have led to variants with superior reconstitution properties, reducing processing time and improving end-product homogeneity for dairy blends and desserts. Unique selling propositions often lie in the granular form, instant dissolving characteristics, and specific protein denaturation levels tailored for applications like ice-cream and infant nutrition. Technological advancements are also driving the development of specialized NFDM products for niche markets, such as fortified variants with added vitamins and minerals, or those with reduced lactose content.

Key Drivers, Barriers & Challenges in Non Fat Dry Milk

Key Drivers:

- Growing Demand for Convenience Foods: NFDM's shelf-stability and ease of incorporation into a wide array of processed foods are major drivers.

- Nutritional Benefits: Its role as a source of protein, calcium, and other essential nutrients appeals to health-conscious consumers and fortified food manufacturers.

- Cost-Effectiveness: Compared to liquid milk, NFDM offers significant cost savings in transportation and storage for the food processing industry.

- Versatile Functionality: Its emulsifying, binding, and browning properties make it indispensable in bakery and confectionery, ice-cream, and dairy blends.

Barriers & Challenges:

- Volatile Raw Material Prices: Fluctuations in global milk production and commodity prices can impact NFDM profitability.

- Competition from Alternatives: Plant-based milk powders and other protein sources pose competitive threats.

- Regulatory Compliance: Adhering to diverse international food safety standards and labeling requirements can be complex.

- Supply Chain Disruptions: Geopolitical events, climate change, and logistical issues can impact raw milk availability and distribution.

- Consumer Perception: Negative perceptions regarding the processing of dairy products can sometimes hinder demand.

- Energy Costs: The drying process is energy-intensive, making manufacturers vulnerable to rising energy prices.

Emerging Opportunities in Non Fat Dry Milk

Emerging opportunities in the Non Fat Dry Milk (NFDM) market lie in tapping into burgeoning markets for fortified foods and beverages, particularly in developing economies where nutritional deficiencies are prevalent. The demand for clean-label and natural ingredients also presents an avenue for innovation, with opportunities to develop organic or minimally processed NFDM variants. Furthermore, the expanding market for sports nutrition and functional foods offers a substantial growth area, as NFDM can be incorporated into protein bars, shakes, and meal replacements. Exploring new applications in pet food and specialized animal feed formulations also represents an untapped potential.

Growth Accelerators in the Non Fat Dry Milk Industry

Technological breakthroughs in drying and processing methods are significant growth accelerators for the NFDM industry, leading to enhanced product quality, improved functionality, and reduced production costs. Strategic partnerships between NFDM producers and food manufacturers are crucial for co-developing innovative products and expanding market reach. Market expansion strategies, particularly targeting the growing middle class in Asia and Africa, will drive volume growth. Investments in sustainable production practices and traceability systems will further enhance brand value and consumer trust, accelerating long-term market expansion.

Key Players Shaping the Non Fat Dry Milk Market

- Anchor

- Armor

- DairyAmerica

- Nestlé

- Arla

- Premier Foods

- Darigold

- Amul

- Devondale

- Sterling Agro Industries

- Karivita

- Glanbia plc

- Alpen Dairies

- Lakeland Dairies

- TATURA

- Senel BV

Notable Milestones in Non Fat Dry Milk Sector

- 2019: Increased focus on sustainability in dairy processing, leading to investments in energy-efficient drying technologies.

- 2020: Supply chain disruptions due to global events highlighted the importance of localized sourcing and robust inventory management for NFDM.

- 2021: Growing consumer interest in plant-based alternatives spurred innovation in dairy-based ingredients for enhanced functionality.

- 2022: Advancements in spray drying technology enabled the production of NFDM with superior reconstitution properties for instant food applications.

- 2023: Heightened demand for protein-rich foods and beverages drove increased utilization of NFDM in sports nutrition and health supplements.

- 2024: Emergence of specialized NFDM grades tailored for specific applications, such as infant formula and confectionery, with precise nutritional profiles.

In-Depth Non Fat Dry Milk Market Outlook

The Non Fat Dry Milk market outlook is exceptionally positive, driven by sustained global demand for affordable, nutritious, and versatile dairy ingredients. Growth accelerators, including technological advancements in processing, strategic market expansions into emerging economies, and the increasing demand for functional foods, are poised to significantly boost market expansion. Future opportunities lie in the continued innovation of specialized NFDM products, catering to evolving consumer preferences for health and convenience, further solidifying its indispensable role in the global food supply chain.

Non Fat Dry Milk Segmentation

-

1. Application

- 1.1. Bakery and Confectionery

- 1.2. Desserts

- 1.3. Ice-cream

- 1.4. Dairy Blends

- 1.5. Others

-

2. Type

- 2.1. Low-Heat

- 2.2. Medium-Heat

- 2.3. High-Heat

Non Fat Dry Milk Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Non Fat Dry Milk Regional Market Share

Geographic Coverage of Non Fat Dry Milk

Non Fat Dry Milk REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Bakery and Confectionery

- 5.1.2. Desserts

- 5.1.3. Ice-cream

- 5.1.4. Dairy Blends

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Low-Heat

- 5.2.2. Medium-Heat

- 5.2.3. High-Heat

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Non Fat Dry Milk Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Bakery and Confectionery

- 6.1.2. Desserts

- 6.1.3. Ice-cream

- 6.1.4. Dairy Blends

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Low-Heat

- 6.2.2. Medium-Heat

- 6.2.3. High-Heat

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Non Fat Dry Milk Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Bakery and Confectionery

- 7.1.2. Desserts

- 7.1.3. Ice-cream

- 7.1.4. Dairy Blends

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Low-Heat

- 7.2.2. Medium-Heat

- 7.2.3. High-Heat

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Non Fat Dry Milk Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Bakery and Confectionery

- 8.1.2. Desserts

- 8.1.3. Ice-cream

- 8.1.4. Dairy Blends

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Low-Heat

- 8.2.2. Medium-Heat

- 8.2.3. High-Heat

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Non Fat Dry Milk Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Bakery and Confectionery

- 9.1.2. Desserts

- 9.1.3. Ice-cream

- 9.1.4. Dairy Blends

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Low-Heat

- 9.2.2. Medium-Heat

- 9.2.3. High-Heat

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Non Fat Dry Milk Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Bakery and Confectionery

- 10.1.2. Desserts

- 10.1.3. Ice-cream

- 10.1.4. Dairy Blends

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Low-Heat

- 10.2.2. Medium-Heat

- 10.2.3. High-Heat

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Non Fat Dry Milk Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Bakery and Confectionery

- 11.1.2. Desserts

- 11.1.3. Ice-cream

- 11.1.4. Dairy Blends

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Low-Heat

- 11.2.2. Medium-Heat

- 11.2.3. High-Heat

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Anchor

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Armor

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 DairyAmerica

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Nestlé

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Arla

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Premier Foods

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Darigold

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Amul

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Devondale

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Sterling Agro Industries

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Karivita

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Glanbia plc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Alpen Dairies

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Lakeland Dairies

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 TATURA

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Senel BV

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 Anchor

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Non Fat Dry Milk Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Non Fat Dry Milk Revenue (million), by Application 2025 & 2033

- Figure 3: North America Non Fat Dry Milk Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Non Fat Dry Milk Revenue (million), by Type 2025 & 2033

- Figure 5: North America Non Fat Dry Milk Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Non Fat Dry Milk Revenue (million), by Country 2025 & 2033

- Figure 7: North America Non Fat Dry Milk Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Non Fat Dry Milk Revenue (million), by Application 2025 & 2033

- Figure 9: South America Non Fat Dry Milk Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Non Fat Dry Milk Revenue (million), by Type 2025 & 2033

- Figure 11: South America Non Fat Dry Milk Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Non Fat Dry Milk Revenue (million), by Country 2025 & 2033

- Figure 13: South America Non Fat Dry Milk Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Non Fat Dry Milk Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Non Fat Dry Milk Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Non Fat Dry Milk Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Non Fat Dry Milk Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Non Fat Dry Milk Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Non Fat Dry Milk Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Non Fat Dry Milk Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Non Fat Dry Milk Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Non Fat Dry Milk Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Non Fat Dry Milk Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Non Fat Dry Milk Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Non Fat Dry Milk Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Non Fat Dry Milk Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Non Fat Dry Milk Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Non Fat Dry Milk Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Non Fat Dry Milk Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Non Fat Dry Milk Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Non Fat Dry Milk Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Non Fat Dry Milk Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Non Fat Dry Milk Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Non Fat Dry Milk Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Non Fat Dry Milk Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Non Fat Dry Milk Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Non Fat Dry Milk Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Non Fat Dry Milk Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Non Fat Dry Milk Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Non Fat Dry Milk Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Non Fat Dry Milk Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Non Fat Dry Milk Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Non Fat Dry Milk Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Non Fat Dry Milk Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Non Fat Dry Milk Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Non Fat Dry Milk Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Non Fat Dry Milk Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Non Fat Dry Milk Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Non Fat Dry Milk Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Non Fat Dry Milk Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Non Fat Dry Milk?

The projected CAGR is approximately 5.9%.

2. Which companies are prominent players in the Non Fat Dry Milk?

Key companies in the market include Anchor, Armor, DairyAmerica, Nestlé, Arla, Premier Foods, Darigold, Amul, Devondale, Sterling Agro Industries, Karivita, Glanbia plc, Alpen Dairies, Lakeland Dairies, TATURA, Senel BV.

3. What are the main segments of the Non Fat Dry Milk?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1273 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Non Fat Dry Milk," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Non Fat Dry Milk report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Non Fat Dry Milk?

To stay informed about further developments, trends, and reports in the Non Fat Dry Milk, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence