Key Insights

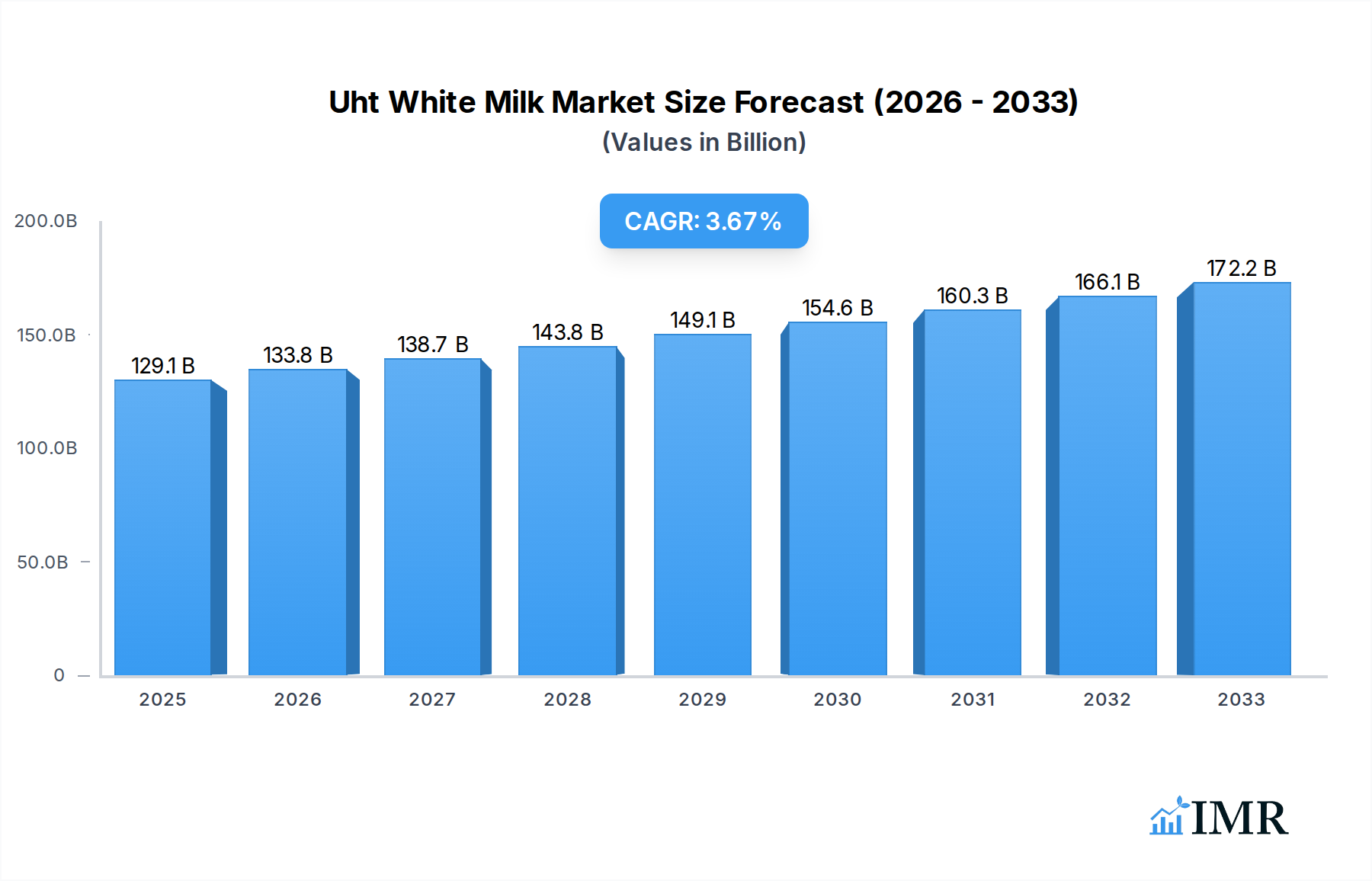

The global UHT White Milk market is poised for substantial growth, projected to reach approximately USD 129,050 million by 2025. This expansion is fueled by a projected Compound Annual Growth Rate (CAGR) of 3.7% over the forecast period of 2025-2033. Key drivers contributing to this robust growth include the increasing consumer demand for convenient and long-shelf-life dairy products, especially in emerging economies. The enhanced safety and extended freshness offered by UHT processing make it an attractive option for consumers globally, aligning with busy lifestyles and improving access to nutritious dairy in regions with less developed cold chain infrastructure. Furthermore, the growing awareness of milk's health benefits, coupled with innovative product development, such as fortified UHT milk and plant-based alternatives within the white milk category, are expected to further stimulate market penetration and value.

Uht White Milk Market Size (In Billion)

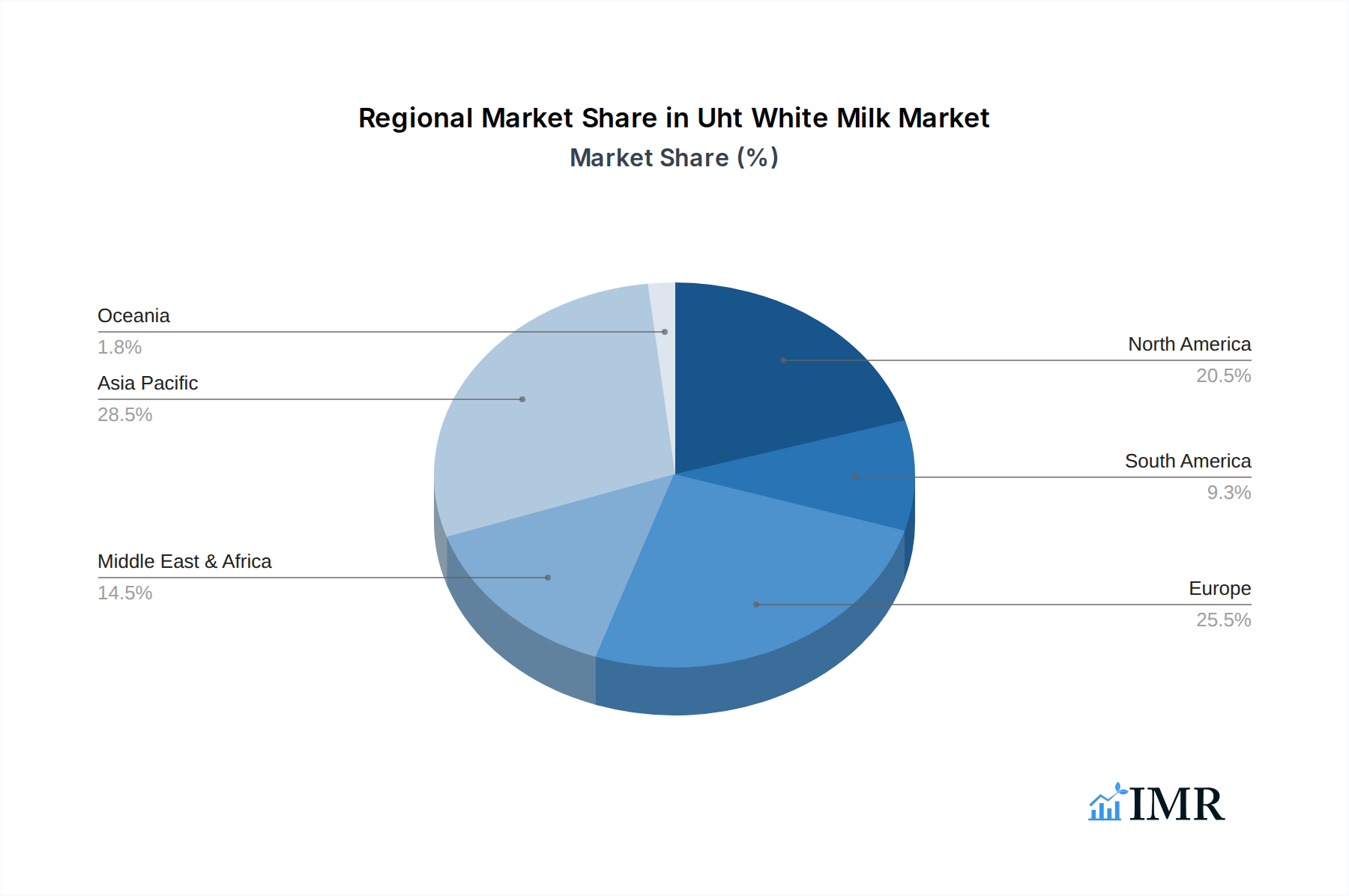

The market segmentation reveals a dynamic landscape. In terms of application, online sales are experiencing rapid growth, mirroring broader e-commerce trends, while offline sales, though dominant, are adapting to evolving retail environments. The type segmentation indicates a balanced demand across Whole Milk, Low-fat Milk, and Skimmed Milk, reflecting diverse dietary preferences and health consciousness. Geographically, the Asia Pacific region, particularly China and India, is anticipated to be a significant growth engine due to its large population, rising disposable incomes, and increasing urbanization. Europe and North America remain mature but substantial markets, driven by product innovation and a focus on premium and specialized UHT milk offerings. Major players like Nestle, Danone, Yili Group, and Mengniu Dairy are actively investing in expanding their production capacities and distribution networks to capitalize on these burgeoning opportunities.

Uht White Milk Company Market Share

UHT White Milk Market Dynamics & Structure

The global UHT white milk market exhibits a moderately consolidated structure, with key players like Nestle, Danone, Yili Group, Mengniu Dairy, and Lactalis Group holding significant market shares, estimated to be around 45% of the total market value. Technological innovation is primarily driven by advancements in aseptic processing, packaging materials, and fortification technologies, enhancing shelf-life and nutritional value. Regulatory frameworks, particularly food safety standards and labeling requirements in major consumption hubs like North America and Europe, play a crucial role in market entry and product development. Competitive product substitutes, including plant-based milk alternatives and fresh milk, exert continuous pressure, necessitating strategic product differentiation. End-user demographics are shifting towards health-conscious consumers, driving demand for low-fat and skimmed milk variants. Mergers and acquisitions (M&A) are a notable trend, with recent activity indicating a focus on expanding geographical reach and product portfolios. For instance, in the historical period (2019-2024), an estimated 5 significant M&A deals occurred, involving acquisitions of smaller regional players by larger multinational corporations.

- Market Concentration: Moderately consolidated, with top 5 players holding approximately 45% market share.

- Technological Drivers: Aseptic processing, advanced packaging, and nutritional fortification.

- Regulatory Influence: Food safety standards and labeling compliance in key markets.

- Competitive Landscape: Pressure from plant-based alternatives and fresh milk.

- End-User Trends: Growing demand for healthier, low-fat, and skimmed milk options.

- M&A Activity: Strategic acquisitions to enhance market presence and product offerings.

UHT White Milk Growth Trends & Insights

The UHT white milk market is poised for robust growth over the forecast period (2025–2033), driven by an increasing global population, rising disposable incomes in emerging economies, and a growing awareness of dairy's nutritional benefits. The market size is projected to expand from an estimated 98,500 million units in the base year 2025 to over 115,000 million units by 2033, reflecting a Compound Annual Growth Rate (CAGR) of approximately 2.5%. Adoption rates are steadily increasing, particularly in regions with developing cold chain infrastructure, where UHT milk offers a significant advantage over fresh milk due to its extended shelf life and ambient storage capabilities. Technological disruptions, such as improved processing efficiencies and sustainable packaging solutions, are further enhancing market appeal. Consumer behavior shifts are evident, with a rising preference for convenience, leading to the growth of online sales channels for UHT milk. Furthermore, a heightened focus on health and wellness is boosting demand for fortified UHT milk products, enriched with vitamins and minerals, catering to specific dietary needs and preferences. The penetration of UHT white milk is expected to rise from an estimated 65% in 2025 to over 70% by 2033 in the parent market, signifying its increasing dominance over traditional milk consumption methods.

The parent market for UHT white milk, encompassing global consumption, is experiencing a sustained upward trajectory. This growth is underpinned by fundamental demographic shifts and evolving lifestyle choices across diverse economies. In the historical period (2019-2024), the market demonstrated resilience, navigating through supply chain fluctuations and changing consumer habits. The estimated market size in 2024 was approximately 96,200 million units, with a preceding CAGR of 2.3%. The base year 2025 is estimated to see a market size of 98,500 million units. Looking ahead to the forecast period (2025–2033), the market is anticipated to grow at a CAGR of around 2.5%. This expansion is largely attributable to the increasing urbanization in developing nations, where access to reliable refrigeration is often limited, making UHT milk an indispensable staple. The nutritional benefits associated with milk consumption, including calcium and protein content, are also being actively promoted by health organizations, further solidifying its position in consumer diets. Technological advancements in UHT processing, such as ultra-high temperature treatments and improved aseptic packaging, have significantly enhanced product quality and shelf-life, reducing spoilage and waste. This innovation is a key factor in boosting consumer confidence and adoption rates.

The child market, or the segmentation within UHT white milk, also reflects these overarching trends. The shift towards healthier options is particularly evident in the growing preference for low-fat and skimmed milk types. While whole milk remains a significant segment, its growth is being outpaced by the demand for reduced-fat alternatives, driven by health-conscious consumers seeking to manage their calorie intake. Online sales channels are experiencing exponential growth, mirroring the broader e-commerce boom. This trend is particularly pronounced in developed markets, but its adoption is rapidly expanding in emerging economies as digital infrastructure improves. Offline sales, while still dominant, are witnessing a diversification in retail formats, with convenience stores and hypermarkets playing crucial roles in product accessibility. The market penetration of UHT white milk is not uniform across all segments; for instance, while its penetration in urban areas is already high, rural adoption is still gaining momentum. The increasing availability of UHT milk in smaller, single-serve packaging formats further caters to the on-the-go consumption patterns of modern consumers, acting as a significant growth accelerator.

Dominant Regions, Countries, or Segments in UHT White Milk

The dominance in the UHT white milk market is largely attributed to a confluence of economic, demographic, and infrastructural factors. Asia Pacific, particularly China, stands out as the leading region, driven by its massive population, rapidly growing middle class, and a strong cultural inclination towards dairy consumption. In the historical period (2019-2024), Asia Pacific accounted for an estimated 35% of the global UHT white milk market share, with China alone contributing approximately 20% of this. The base year 2025 is projected to see Asia Pacific maintaining its lead with an estimated market share of 36%.

Within the application segments, Offline Sales continue to be the dominant channel, accounting for an estimated 78% of the market in 2025. This dominance is fueled by the widespread presence of traditional retail outlets, supermarkets, and hypermarkets, especially in developing economies where e-commerce penetration is still evolving. Key drivers for offline sales include immediate availability, the ability to physically inspect products, and established purchasing habits. However, Online Sales are exhibiting a significantly higher growth rate, projected to expand at a CAGR of 5.2% from 2025 to 2033, indicating a gradual shift in consumer preferences towards convenience and digital purchasing platforms. By 2033, the online sales share is expected to increase to approximately 25%.

Regarding product types, Whole Milk remains the largest segment by volume, holding an estimated 55% market share in 2025. Its widespread acceptance, perceived nutritional richness, and affordability contribute to its sustained dominance. However, the Low-fat Milk segment is experiencing robust growth, driven by increasing health consciousness and a desire to manage calorie intake. This segment is projected to grow at a CAGR of 3.1% from 2025 to 2033. Skimmed Milk, while a smaller segment, is also witnessing steady demand, particularly among consumers focused on very low-fat diets. The growth potential for low-fat and skimmed milk is substantial as health trends continue to influence purchasing decisions.

- Leading Region: Asia Pacific, with China as a primary contributor, driven by population size and economic growth.

- Dominant Application: Offline Sales continue to lead due to extensive retail networks and established consumer habits.

- Key Drivers: Immediate availability, physical product inspection, traditional purchasing patterns.

- Growing Application: Online Sales exhibit a higher growth rate, fueled by convenience and digital adoption.

- Market Share Projection: Expected to increase significantly by 2033.

- Dominant Type: Whole Milk holds the largest market share due to broad appeal and affordability.

- Growth Factors: Widespread acceptance, perceived nutritional value.

- High Growth Type: Low-fat Milk is rapidly gaining traction due to increasing health consciousness and dietary awareness.

- CAGR: Projected to outpace overall market growth.

UHT White Milk Product Landscape

The UHT white milk product landscape is characterized by continuous innovation focused on enhancing nutritional value and consumer convenience. Companies are increasingly introducing fortified UHT milk variants, enriched with essential vitamins (like Vitamin D and B12) and minerals (such as calcium and iron), catering to specific dietary needs and health trends. Advancements in aseptic packaging technology have led to more sustainable and durable options, reducing environmental impact and improving product integrity. Unique selling propositions often revolve around specific health benefits, such as improved bone health or enhanced immunity. The market also sees a rise in lactose-free UHT milk options, addressing the needs of lactose-intolerant consumers.

Key Drivers, Barriers & Challenges in UHT White Milk

Key Drivers: The UHT white milk market is propelled by several key drivers. Growing global population and increasing disposable incomes, especially in emerging economies, expand the consumer base. Rising health consciousness fuels demand for nutrient-rich and fortified milk options. The extended shelf-life and ambient storage capabilities of UHT milk make it an ideal choice in regions with developing cold chain infrastructure. Technological advancements in processing and packaging also contribute significantly by improving quality and reducing costs.

Barriers & Challenges: Despite the positive outlook, the market faces several challenges. Intense competition from plant-based milk alternatives poses a significant restraint, with consumers increasingly exploring vegan and dairy-free options. Volatility in raw milk prices can impact production costs and profitability. Stringent regulatory requirements and food safety standards in various countries can create barriers to entry. Furthermore, consumer perception regarding the taste and nutritional profile of UHT milk compared to fresh milk remains a challenge in some mature markets. Supply chain disruptions, as witnessed historically, can also impact availability and pricing.

Emerging Opportunities in UHT White Milk

Emerging opportunities in the UHT white milk sector lie in leveraging the growing demand for functional beverages and personalized nutrition. Untapped markets in Sub-Saharan Africa and parts of Southeast Asia present significant growth potential due to improving economic conditions and increasing awareness of dairy's health benefits. Innovative applications, such as UHT milk as an ingredient in ready-to-drink beverages and dairy-based snacks, offer new revenue streams. Evolving consumer preferences for sustainable and eco-friendly packaging present an opportunity for companies to innovate and differentiate. The development of specialized UHT milk formulations for specific age groups or health conditions (e.g., elder nutrition, sports nutrition) also represents a promising avenue.

Growth Accelerators in the UHT White Milk Industry

Several catalysts are accelerating the growth of the UHT white milk industry. Technological breakthroughs in ultra-clean filling and advanced packaging materials are enhancing product safety, extending shelf life even further, and reducing waste. Strategic partnerships between dairy producers and e-commerce platforms are vital for expanding market reach and tapping into the digital consumer base. Market expansion strategies targeting rural and semi-urban areas in developing countries, coupled with localized marketing campaigns highlighting nutritional benefits and affordability, are crucial. Furthermore, government initiatives promoting dairy consumption for public health can significantly boost market penetration.

Key Players Shaping the UHT White Milk Market

- Nestle

- Danone

- Yili Group

- Mengniu Dairy

- Lactalis Group

- DFA

- Arla Foods

- FrieslandCampina

- Fonterra

- DMK

- Saputo

- Vinamilk

- Sodiaal

- Schreiber Foods

- Amul

- KMF

- Meiji Group

Notable Milestones in UHT White Milk Sector

- 2019: Introduction of plant-based milk alternatives gain significant market traction, posing a new competitive challenge.

- 2020: COVID-19 pandemic leads to a surge in demand for shelf-stable products, boosting UHT milk sales and highlighting its logistical advantages.

- 2021: Increased focus on sustainable packaging solutions by major manufacturers, with a move towards recyclable materials.

- 2022: Launch of fortified UHT milk variants with enhanced vitamins and minerals to cater to growing health and wellness trends.

- 2023: Significant investment in e-commerce infrastructure and digital marketing strategies by key players to capitalize on growing online sales.

In-Depth UHT White Milk Market Outlook

The future of the UHT white milk market is characterized by sustained growth, driven by its inherent advantages in shelf-life and logistics, particularly in emerging economies. Key strategic opportunities lie in further penetrating rural and semi-urban markets through accessible distribution networks and affordable product offerings. Continued innovation in fortification and specialized formulations to meet diverse health needs will be paramount. The integration of smart packaging technologies offering enhanced traceability and consumer engagement presents another promising avenue. Strategic collaborations with food service providers and the development of unique product formats will also be critical for capturing a larger market share and ensuring long-term growth in this dynamic sector.

Uht White Milk Segmentation

-

1. Application

- 1.1. Online Sales

- 1.2. Offline Sales

-

2. Type

- 2.1. Whole Milk

- 2.2. Low-fat Milk

- 2.3. Skimmed Milk

Uht White Milk Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Uht White Milk Regional Market Share

Geographic Coverage of Uht White Milk

Uht White Milk REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Uht White Milk Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Online Sales

- 5.1.2. Offline Sales

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Whole Milk

- 5.2.2. Low-fat Milk

- 5.2.3. Skimmed Milk

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Uht White Milk Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Online Sales

- 6.1.2. Offline Sales

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Whole Milk

- 6.2.2. Low-fat Milk

- 6.2.3. Skimmed Milk

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Uht White Milk Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Online Sales

- 7.1.2. Offline Sales

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Whole Milk

- 7.2.2. Low-fat Milk

- 7.2.3. Skimmed Milk

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Uht White Milk Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Online Sales

- 8.1.2. Offline Sales

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Whole Milk

- 8.2.2. Low-fat Milk

- 8.2.3. Skimmed Milk

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Uht White Milk Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Online Sales

- 9.1.2. Offline Sales

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Whole Milk

- 9.2.2. Low-fat Milk

- 9.2.3. Skimmed Milk

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Uht White Milk Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Online Sales

- 10.1.2. Offline Sales

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Whole Milk

- 10.2.2. Low-fat Milk

- 10.2.3. Skimmed Milk

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Nestle

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Danone

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Yili Group

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Mengniu Dairy

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Lactalis Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 DFA

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Arla Foods

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 FrieslandCampina

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Fonterra

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 DMK

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Saputo

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Vinamilk

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Sodiaal

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Schreiber Foods

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Amul

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 KMF

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Meiji Group

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Nestle

List of Figures

- Figure 1: Global Uht White Milk Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Uht White Milk Revenue (million), by Application 2025 & 2033

- Figure 3: North America Uht White Milk Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Uht White Milk Revenue (million), by Type 2025 & 2033

- Figure 5: North America Uht White Milk Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Uht White Milk Revenue (million), by Country 2025 & 2033

- Figure 7: North America Uht White Milk Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Uht White Milk Revenue (million), by Application 2025 & 2033

- Figure 9: South America Uht White Milk Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Uht White Milk Revenue (million), by Type 2025 & 2033

- Figure 11: South America Uht White Milk Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Uht White Milk Revenue (million), by Country 2025 & 2033

- Figure 13: South America Uht White Milk Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Uht White Milk Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Uht White Milk Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Uht White Milk Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Uht White Milk Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Uht White Milk Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Uht White Milk Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Uht White Milk Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Uht White Milk Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Uht White Milk Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Uht White Milk Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Uht White Milk Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Uht White Milk Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Uht White Milk Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Uht White Milk Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Uht White Milk Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Uht White Milk Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Uht White Milk Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Uht White Milk Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Uht White Milk Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Uht White Milk Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Uht White Milk Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Uht White Milk Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Uht White Milk Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Uht White Milk Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Uht White Milk Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Uht White Milk Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Uht White Milk Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Uht White Milk Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Uht White Milk Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Uht White Milk Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Uht White Milk Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Uht White Milk Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Uht White Milk Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Uht White Milk Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Uht White Milk Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Uht White Milk Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Uht White Milk Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Uht White Milk?

The projected CAGR is approximately 3.7%.

2. Which companies are prominent players in the Uht White Milk?

Key companies in the market include Nestle, Danone, Yili Group, Mengniu Dairy, Lactalis Group, DFA, Arla Foods, FrieslandCampina, Fonterra, DMK, Saputo, Vinamilk, Sodiaal, Schreiber Foods, Amul, KMF, Meiji Group.

3. What are the main segments of the Uht White Milk?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 129050 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Uht White Milk," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Uht White Milk report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Uht White Milk?

To stay informed about further developments, trends, and reports in the Uht White Milk, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence