Key Insights

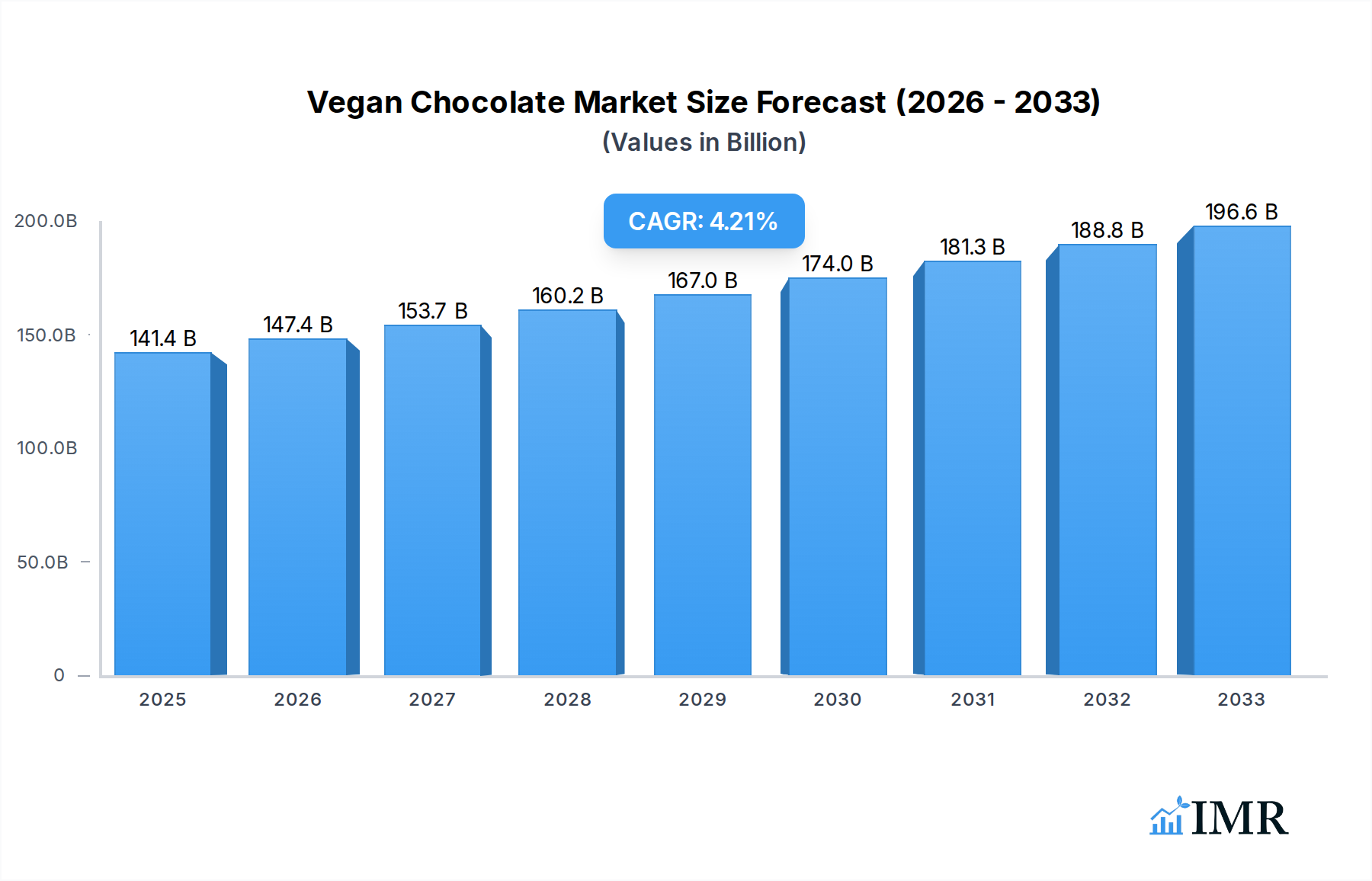

The global vegan chocolate market is poised for significant expansion, with a projected market size of $141.42 billion in 2025 and an impressive CAGR of 4.2%. This robust growth is fueled by a confluence of powerful drivers, including the escalating consumer demand for plant-based and ethically sourced products, a growing awareness of the health benefits associated with dark chocolate, and the increasing availability of innovative and diverse vegan chocolate offerings across various retail channels. Supermarkets and convenience stores are witnessing a surge in vegan chocolate sales, while online platforms are proving instrumental in reaching a wider, digitally-savvy consumer base. The burgeoning trend towards mindful consumption and the desire to reduce environmental impact are further propelling the adoption of vegan chocolate. Manufacturers are responding by diversifying their product portfolios, introducing an array of flavors and formats, from classic chocolate bars to sophisticated flavoring ingredients for culinary applications, catering to a sophisticated palate.

Vegan Chocolate Market Size (In Billion)

Despite the optimistic outlook, certain restraints could temper the market's trajectory. The comparatively higher cost of raw materials, such as cocoa beans and alternative dairy ingredients, can translate to higher retail prices, potentially limiting accessibility for some consumer segments. Fluctuations in the price of these key ingredients also pose a challenge for consistent pricing strategies. Furthermore, while consumer awareness is growing, widespread misconceptions about the taste and texture of vegan chocolate persist in some markets, requiring sustained marketing efforts to educate and engage consumers. However, leading companies like Lindt, Alter Eco, and Hu Kitchen are actively investing in research and development, aiming to overcome these challenges through enhanced production efficiencies and innovative product formulations, ensuring the continued vibrancy and growth of the vegan chocolate industry.

Vegan Chocolate Company Market Share

Here's a SEO-optimized report description for Vegan Chocolate, designed to attract industry professionals and maximize search engine visibility:

This in-depth market research report provides an unparalleled analysis of the global Vegan Chocolate market, covering the historical period from 2019 to 2024, with a base year of 2025 and a forecast period extending to 2033. Delve into the burgeoning demand for plant-based confections and gain strategic insights into market dynamics, growth trajectories, competitive landscapes, and emerging opportunities. This report is an essential resource for manufacturers, ingredient suppliers, retailers, investors, and market strategists seeking to capitalize on the rapid expansion of the vegan chocolate industry.

Vegan Chocolate Market Dynamics & Structure

The global vegan chocolate market is characterized by increasing fragmentation and dynamic shifts driven by technological advancements and evolving consumer preferences. The market concentration is moderate, with a growing number of specialized vegan brands alongside established confectionery giants introducing plant-based lines. Technological innovation is a key driver, particularly in developing superior dairy-free alternatives and sustainable sourcing practices for cocoa. Regulatory frameworks are becoming more defined, focusing on clear labeling and ethical sourcing. Competitive product substitutes, including other vegan confectioneries and traditional dairy-based chocolates, present ongoing challenges. End-user demographics are broadening beyond strict vegans to include flexitarians, health-conscious consumers, and individuals with dairy intolerances, driving mainstream adoption. Mergers and acquisitions (M&A) are on the rise as larger players seek to capture market share and integrate innovative vegan brands into their portfolios.

- Market Concentration: Moderate, with increasing competition from niche and mainstream players.

- Technological Innovation: Focus on dairy-free formulation, ethical sourcing, and improved taste profiles.

- Regulatory Frameworks: Evolving standards for labeling, sustainability, and ingredient transparency.

- Competitive Product Substitutes: Dairy chocolate, other vegan snacks, and plant-based desserts.

- End-User Demographics: Expanding to include flexitarians, health-conscious individuals, and those with dietary restrictions.

- M&A Trends: Increasing consolidation as larger companies acquire or partner with established vegan chocolate brands.

Vegan Chocolate Growth Trends & Insights

The global vegan chocolate market is poised for remarkable growth, driven by a confluence of factors including rising health consciousness, ethical consumerism, and innovative product development. The market size is projected to witness a significant expansion, fueled by increasing consumer adoption of plant-based diets and a growing awareness of the environmental impact associated with dairy production. Technological disruptions in ingredient sourcing and processing are enabling the creation of vegan chocolates that rival their dairy counterparts in taste and texture, thus accelerating market penetration. Consumer behavior shifts are paramount, with a discernible move towards premium, ethically sourced, and transparently produced vegan chocolate products. This evolving consumer landscape presents a substantial opportunity for brands that can effectively communicate their value proposition.

The compound annual growth rate (CAGR) for the vegan chocolate market is anticipated to be robust, reflecting sustained consumer interest and ongoing innovation. Market penetration is steadily increasing across developed and emerging economies, as distribution channels expand to include mainstream supermarkets and online platforms. The demand for specific vegan chocolate types, such as those made with oat milk, almond milk, and coconut milk, is surging, as consumers seek diverse flavor experiences. Furthermore, the growing preference for dark chocolate, often naturally vegan and perceived as healthier, is contributing to the market's upward trajectory. This dynamic growth is not merely a niche trend but a fundamental shift in consumer preferences, signaling a long-term expansion for the vegan chocolate industry.

Dominant Regions, Countries, or Segments in Vegan Chocolate

The Application segment of Supermarkets is currently the dominant force driving global vegan chocolate market growth. This prominence is attributed to their extensive reach, ability to cater to a broad consumer base, and the increasing allocation of shelf space to plant-based alternatives. Supermarkets provide convenient access for a wide array of consumers, from dedicated vegans to those experimenting with plant-based options, thus maximizing market penetration. Furthermore, the increasing commitment of major supermarket chains to promoting sustainable and healthy food options directly correlates with the amplified sales of vegan chocolates.

- Dominant Application Segment: Supermarkets, leveraging wide distribution and accessibility.

- Key Drivers:

- Economic Policies: Government support for plant-based initiatives and sustainable agriculture.

- Infrastructure: Well-established retail distribution networks facilitating product availability.

- Consumer Income: Rising disposable incomes allowing for premium product purchases.

- Awareness Campaigns: Public health and environmental awareness driving demand for vegan options.

- Dominant Type Segment: Chocolate Bars hold a significant market share within the vegan chocolate landscape. Their convenience, portability, and wide variety of flavors make them a go-to choice for consumers seeking indulgent yet plant-based treats. The innovation in vegan chocolate bar formulations, including the incorporation of diverse inclusions like nuts, fruits, and seeds, further solidifies their leading position.

The Online Sales application segment is experiencing the fastest growth and is a critical emerging driver. E-commerce platforms offer unparalleled convenience, wider product selection, and direct-to-consumer models, appealing to tech-savvy consumers and those seeking specialized vegan products not readily available in local stores. The increasing digital penetration and comfort with online shopping further accelerate this trend, making online sales a crucial frontier for future market expansion.

Vegan Chocolate Product Landscape

The vegan chocolate product landscape is characterized by a surge in innovative formulations and appealing applications. Leading companies are focusing on developing premium, ethically sourced chocolates that offer sophisticated flavor profiles and superior textures, moving beyond basic dark chocolate offerings. Innovations include the use of alternative milk bases such as oat, almond, coconut, and cashew, alongside novel inclusions like adaptogens, superfoods, and artisanal flavorings. Unique selling propositions often revolve around transparency in sourcing, commitment to sustainability, and allergen-free formulations, appealing to a health-conscious and ethically driven consumer base. Technological advancements in processing are crucial for achieving creamy textures and rich flavors without traditional dairy ingredients, ensuring competitive parity with conventional chocolates.

Key Drivers, Barriers & Challenges in Vegan Chocolate

Key Drivers:

- Growing Health Consciousness: Consumers are increasingly seeking healthier alternatives to traditional confectionery, with vegan chocolate often perceived as a healthier option due to the absence of dairy and potentially lower saturated fat content.

- Ethical and Environmental Concerns: A rising global awareness of animal welfare and the environmental impact of dairy farming is propelling demand for plant-based products, including vegan chocolate.

- Lactose Intolerance and Allergies: The increasing prevalence of dairy allergies and lactose intolerance creates a significant market for dairy-free alternatives.

- Product Innovation and Availability: The continuous development of diverse, high-quality vegan chocolate products and their expanding availability across various retail channels are crucial growth catalysts.

Barriers & Challenges:

- Perceived Taste and Texture Differences: Some consumers still associate vegan chocolate with inferior taste and texture compared to dairy chocolate, a perception that brands are actively working to overcome.

- Price Sensitivity: Premium vegan ingredients and ethical sourcing can lead to higher production costs, resulting in higher retail prices, which can be a barrier for some price-sensitive consumers.

- Supply Chain Volatility: Global cocoa bean prices and the availability of specific plant-based ingredients can be subject to volatility due to climate, geopolitical factors, and demand fluctuations.

- Competition from Traditional Chocolate: The established market presence and brand loyalty of traditional dairy chocolate manufacturers pose a significant competitive challenge.

Emerging Opportunities in Vegan Chocolate

Emerging opportunities in the vegan chocolate market lie in the expansion of premiumization, the development of functional chocolates, and the penetration of untapped emerging markets. The demand for single-origin, artisanal vegan chocolates with unique flavor profiles is on the rise, offering premium pricing opportunities. Furthermore, incorporating functional ingredients like adaptogens, probiotics, and vitamins into vegan chocolate formulations presents a significant avenue for growth, catering to consumers seeking added health benefits. Untapped emerging markets in Asia and Latin America, where plant-based diets are gaining traction, offer substantial long-term growth potential.

Growth Accelerators in the Vegan Chocolate Industry

Technological breakthroughs in plant-based dairy alternatives are pivotal growth accelerators for the vegan chocolate industry. Innovations in oat milk, almond milk, and coconut milk processing are enabling the creation of exceptionally creamy and flavorful vegan chocolates that are indistinguishable from their dairy counterparts. Strategic partnerships between established confectionery brands and niche vegan chocolate manufacturers are also playing a crucial role, leveraging combined expertise and distribution networks to reach a wider consumer base. Furthermore, aggressive market expansion strategies, including targeted marketing campaigns and the development of innovative product formats, are accelerating adoption rates globally.

Key Players Shaping the Vegan Chocolate Market

- Alter Eco

- Chocolove

- Eating Evolved

- Endangered Species

- Equal Exchange

- Goodio

- Hu Kitchen

- Taza Chocolate

- Theo Chocolate

- Chocolate Inspirations

- Lindt

Notable Milestones in Vegan Chocolate Sector

- 2019: Increased investment in oat milk technology for dairy-free chocolate formulations.

- 2020: Launch of several premium vegan chocolate bars with exotic flavor combinations, increasing consumer interest.

- 2021: Major confectionery brands begin launching dedicated vegan chocolate lines, signaling mainstream acceptance.

- 2022: Growing consumer demand for transparent sourcing and ethical production practices highlighted in product marketing.

- 2023: Advancements in plant-based emulsifiers and stabilizers improve the texture and melt of vegan chocolates.

- 2024: Expansion of vegan chocolate offerings in convenience stores and online marketplaces.

In-Depth Vegan Chocolate Market Outlook

The future outlook for the vegan chocolate market is exceptionally bright, propelled by sustained consumer demand for healthier, ethical, and environmentally conscious food choices. Growth accelerators, including continued technological innovation in plant-based ingredients and strategic market expansions, will ensure a robust CAGR. Emerging opportunities in functional chocolates and the untapped potential of developing economies present significant avenues for future revenue streams. Strategic partnerships and increasing investment in sustainable cocoa sourcing will further fortify the market's growth trajectory, solidifying vegan chocolate's position as a dominant force in the global confectionery landscape.

Vegan Chocolate Segmentation

-

1. Application

- 1.1. Supermarket

- 1.2. Convenience Store

- 1.3. Online Sales

- 1.4. Others

-

2. Type

- 2.1. Chocolate Bars

- 2.2. Flavoring Ingredient

Vegan Chocolate Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

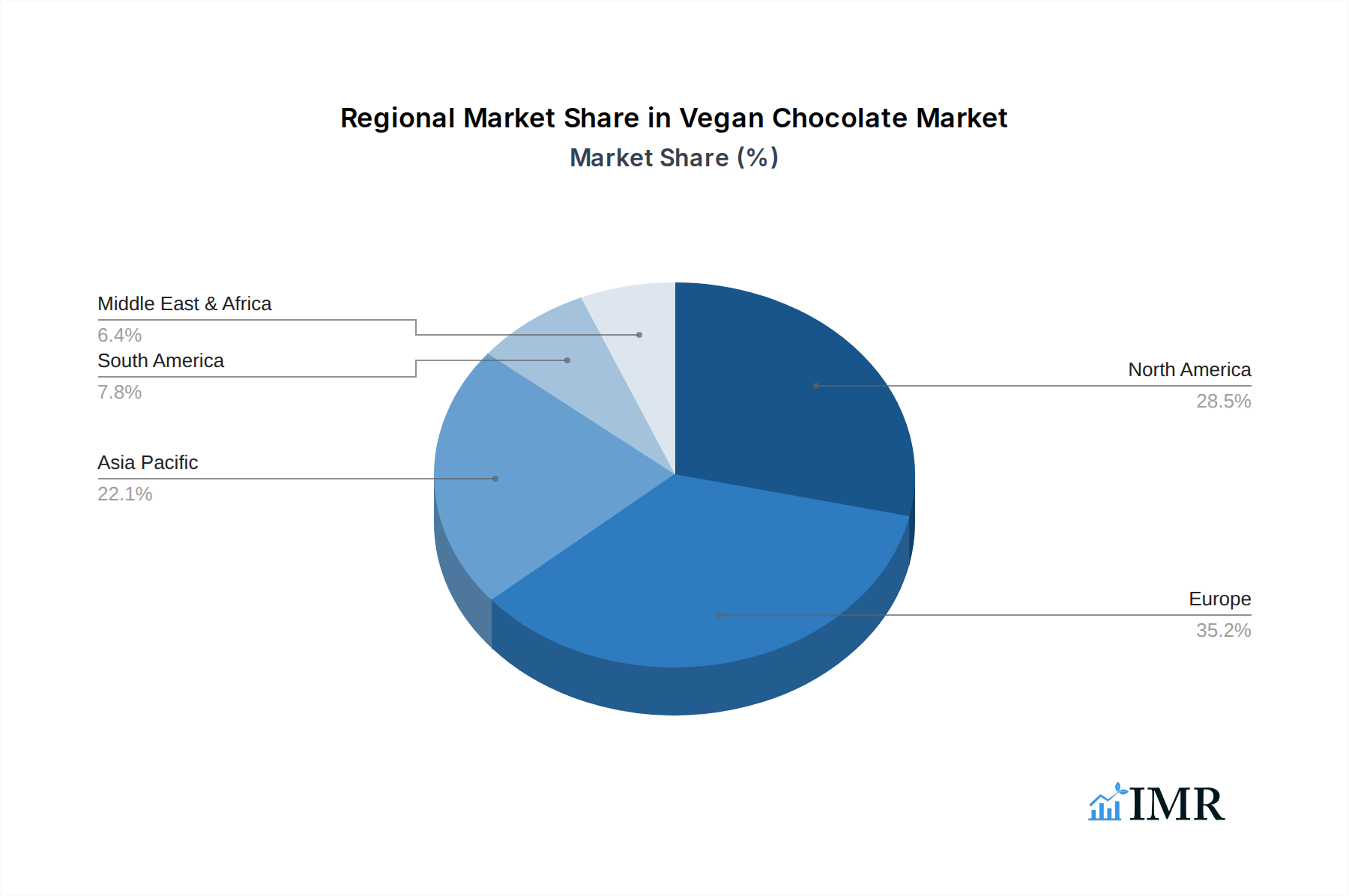

Vegan Chocolate Regional Market Share

Geographic Coverage of Vegan Chocolate

Vegan Chocolate REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.75% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Vegan Chocolate Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Supermarket

- 5.1.2. Convenience Store

- 5.1.3. Online Sales

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Chocolate Bars

- 5.2.2. Flavoring Ingredient

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Vegan Chocolate Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Supermarket

- 6.1.2. Convenience Store

- 6.1.3. Online Sales

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Chocolate Bars

- 6.2.2. Flavoring Ingredient

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Vegan Chocolate Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Supermarket

- 7.1.2. Convenience Store

- 7.1.3. Online Sales

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Chocolate Bars

- 7.2.2. Flavoring Ingredient

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Vegan Chocolate Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Supermarket

- 8.1.2. Convenience Store

- 8.1.3. Online Sales

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Chocolate Bars

- 8.2.2. Flavoring Ingredient

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Vegan Chocolate Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Supermarket

- 9.1.2. Convenience Store

- 9.1.3. Online Sales

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Chocolate Bars

- 9.2.2. Flavoring Ingredient

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Vegan Chocolate Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Supermarket

- 10.1.2. Convenience Store

- 10.1.3. Online Sales

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Chocolate Bars

- 10.2.2. Flavoring Ingredient

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Alter Eco

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Chocolove

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Eating Evolved

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Endangered Species

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Equal Exchange

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Goodio

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Hu Kitchen

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Taza Chocolate

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Theo Chocolate

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Chocolate Inspirations

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Lindt

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Alter Eco

List of Figures

- Figure 1: Global Vegan Chocolate Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Vegan Chocolate Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Vegan Chocolate Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Vegan Chocolate Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Vegan Chocolate Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Vegan Chocolate Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Vegan Chocolate Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Vegan Chocolate Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Vegan Chocolate Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Vegan Chocolate Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Vegan Chocolate Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Vegan Chocolate Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Vegan Chocolate Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Vegan Chocolate Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Vegan Chocolate Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Vegan Chocolate Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Vegan Chocolate Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Vegan Chocolate Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Vegan Chocolate Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Vegan Chocolate Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Vegan Chocolate Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Vegan Chocolate Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Vegan Chocolate Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Vegan Chocolate Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Vegan Chocolate Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Vegan Chocolate Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Vegan Chocolate Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Vegan Chocolate Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Vegan Chocolate Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Vegan Chocolate Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Vegan Chocolate Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Vegan Chocolate Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Vegan Chocolate Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Vegan Chocolate Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Vegan Chocolate Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Vegan Chocolate Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Vegan Chocolate Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Vegan Chocolate Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Vegan Chocolate Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Vegan Chocolate Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Vegan Chocolate Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Vegan Chocolate Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Vegan Chocolate Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Vegan Chocolate Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Vegan Chocolate Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Vegan Chocolate Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Vegan Chocolate Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Vegan Chocolate Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Vegan Chocolate Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Vegan Chocolate Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Vegan Chocolate?

The projected CAGR is approximately 9.75%.

2. Which companies are prominent players in the Vegan Chocolate?

Key companies in the market include Alter Eco, Chocolove, Eating Evolved, Endangered Species, Equal Exchange, Goodio, Hu Kitchen, Taza Chocolate, Theo Chocolate, Chocolate Inspirations, Lindt.

3. What are the main segments of the Vegan Chocolate?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Vegan Chocolate," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Vegan Chocolate report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Vegan Chocolate?

To stay informed about further developments, trends, and reports in the Vegan Chocolate, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence