Key Insights

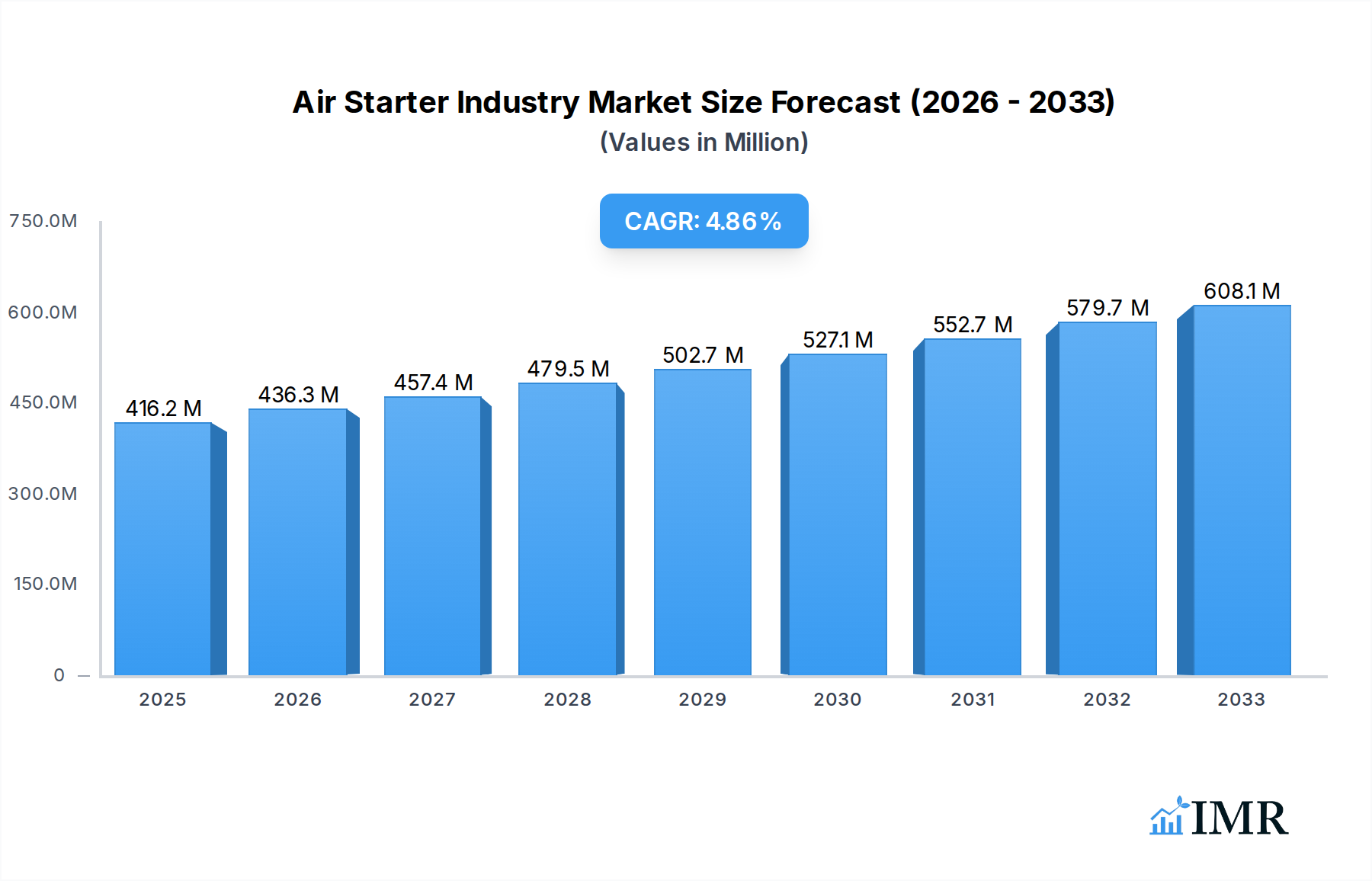

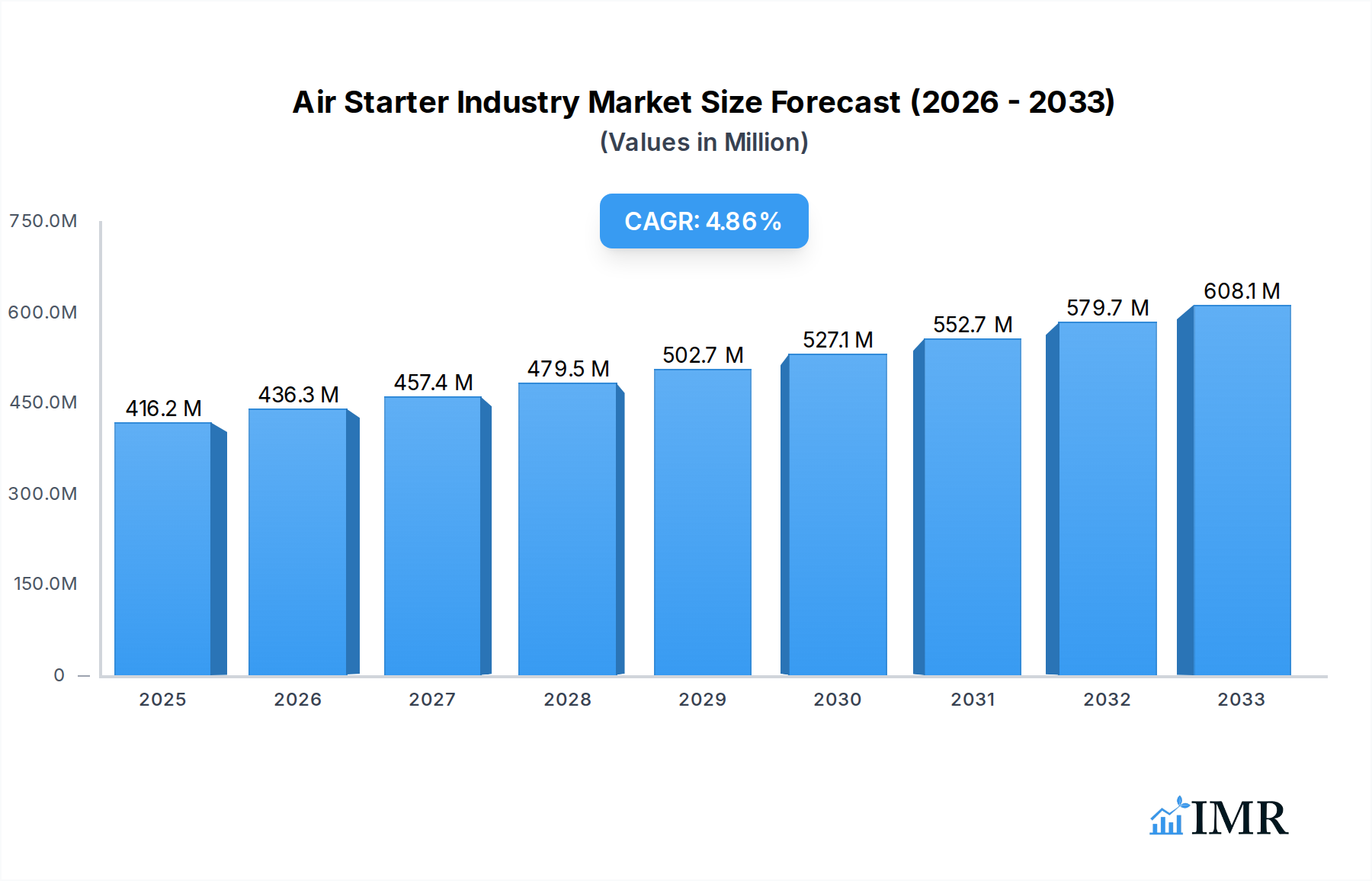

The global Air Starter Industry is poised for robust growth, projected to reach $416.18 million by 2025, with a Compound Annual Growth Rate (CAGR) of 4.75% from 2019 to 2033. This expansion is primarily fueled by the increasing demand from critical sectors such as Oil & Gas, Power Generation, and Mining. The inherent reliability, durability, and low maintenance requirements of air starters, especially in harsh and hazardous environments where electrical starters pose a significant risk, make them the preferred choice. Furthermore, advancements in turbine air starter technology are enhancing efficiency and performance, catering to the evolving needs of these industries. The ongoing industrialization and infrastructure development across emerging economies, particularly in the Asia Pacific region, are creating substantial opportunities for market players.

Air Starter Industry Market Size (In Million)

Despite the positive trajectory, the industry faces certain challenges. The initial cost of installation for air starter systems can be higher compared to some electric alternatives, acting as a potential restraint. Moreover, the availability and cost of compressed air infrastructure in certain remote mining or exploration sites could pose logistical hurdles. However, the long-term operational cost savings and enhanced safety features often outweigh these initial concerns. Key market segments include Vane Air Starters and Turbine Air Starters, with the former being a prevalent choice for smaller engines and the latter gaining traction for larger industrial applications. Leading companies like Ingersoll-Rand Plc, Maradyne Corp, and Austart Air Starters are actively innovating and expanding their product portfolios to capture market share and address diverse customer needs.

Air Starter Industry Company Market Share

Air Starter Industry Market Dynamics & Structure

The global Air Starter Industry, projected to reach USD 1.5 billion in 2025 and grow to USD 1.9 billion by 2033, exhibits a moderately concentrated market. Key players like Maradyne Corp, Austart Air Starters, Ingersoll-Rand Plc, and Miller Air Starter Co Inc hold significant market share, though smaller, specialized manufacturers contribute to the competitive landscape. Technological innovation is a primary driver, with advancements focusing on increased efficiency, reduced emissions, and enhanced durability of both Vane Air Starter and Turbine Air Starter types. Regulatory frameworks, particularly concerning emissions and safety standards in industries like Oil & Gas and Mining, also influence product development and market adoption. Competitive product substitutes, such as electric starters, present a challenge, particularly in applications where energy availability and infrastructure are less of a constraint.

- Market Concentration: Moderate, with a few dominant players and a significant number of niche manufacturers.

- Technological Innovation: Driven by efficiency gains, emissions reduction, and improved lifespan.

- Regulatory Frameworks: Influencing product design and adoption in critical sectors.

- Competitive Substitutes: Electric starters emerging as an alternative in certain segments.

- End-User Demographics: Dominated by Oil & Gas, Power Generation, and Mining industries, with increasing adoption in other heavy industrial applications.

- M&A Trends: Steady consolidation to gain market share and expand technological portfolios. While specific M&A deal volumes are not publicly detailed, the trend indicates a strategic move towards integrated solutions.

Air Starter Industry Growth Trends & Insights

The Air Starter Industry is poised for robust expansion, driven by escalating demand from foundational sectors and continuous technological advancements. The market size, estimated at USD 1.5 billion in the base year of 2025, is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 3.1% during the forecast period of 2025–2033. This steady growth trajectory is underpinned by the inherent reliability and robust performance of air starters, especially in challenging operational environments where electric starters may falter. Adoption rates are particularly high in remote or hazardous locations prevalent in the Oil & Gas and Mining sectors.

Technological disruptions, while not entirely replacing air starters, are focusing on enhancing their performance and sustainability. Innovations in turbine air starter technology, for instance, are leading to higher power-to-weight ratios and improved fuel efficiency. Vane air starters, a more established technology, are witnessing improvements in materials and sealing mechanisms, leading to extended service life and reduced maintenance requirements. Consumer behavior shifts are also playing a role, with a growing emphasis on operational uptime and reduced total cost of ownership, areas where air starters excel due to their simplicity and ruggedness. The mining industry, with its increasing reliance on heavy machinery in remote and often explosive atmospheres, represents a significant market penetration opportunity. Similarly, the power generation sector, requiring reliable engine starting for backup generators and critical infrastructure, continues to be a strong demand driver. The historical period from 2019–2024 saw a steady increase in demand, influenced by industrial expansion and infrastructure projects globally, setting a strong foundation for the projected growth. The estimated market size for 2025 reflects this sustained demand and the ongoing need for dependable starting solutions in critical industrial applications.

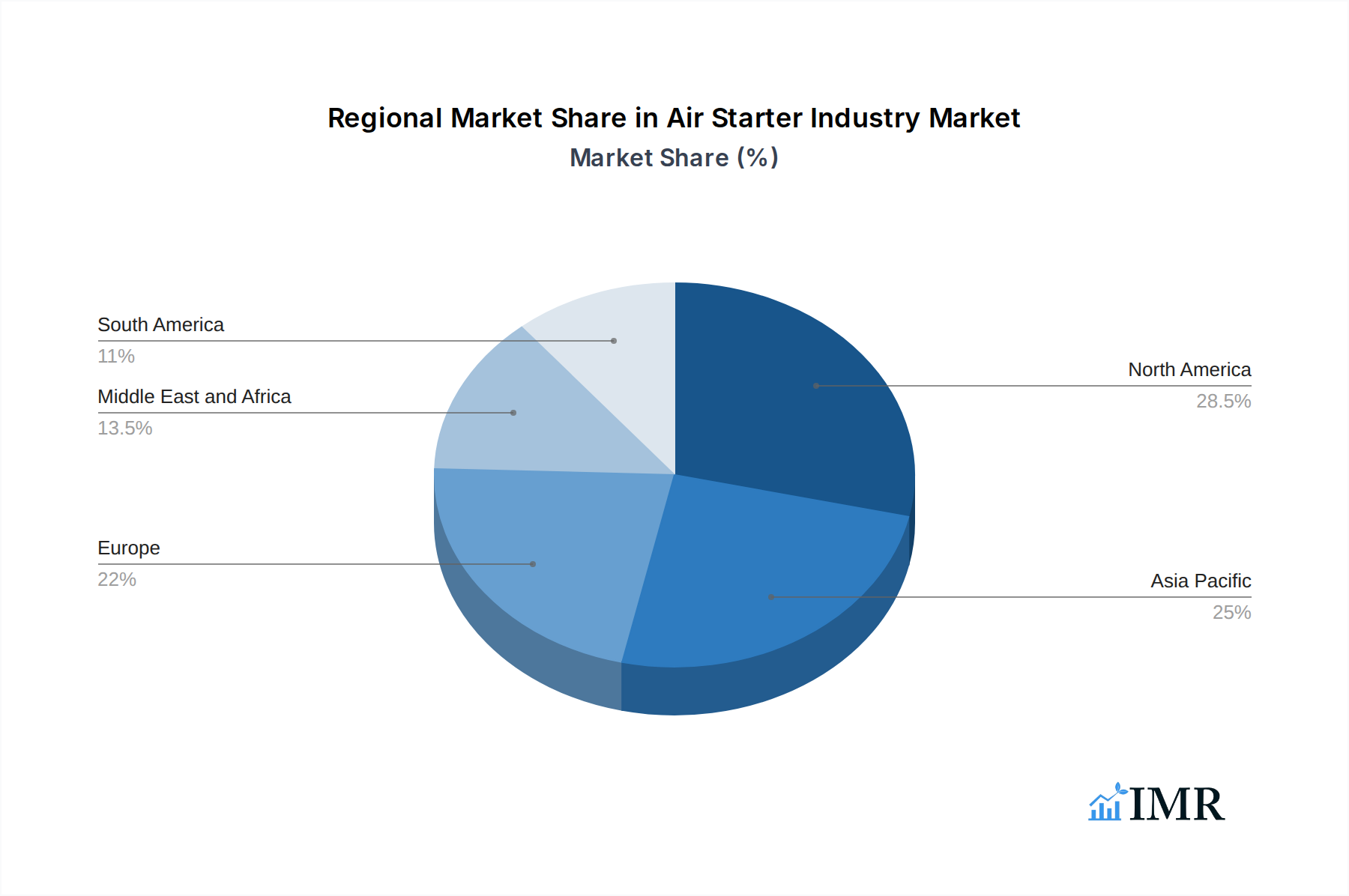

Dominant Regions, Countries, or Segments in Air Starter Industry

The global Air Starter Industry is significantly influenced by regional industrial activity and the specific needs of its dominant end-user segments. The Oil & Gas sector emerges as a primary growth engine, driving demand for both Vane Air Starter and Turbine Air Starter technologies across various operational stages, from exploration and extraction to refining and transportation. This dominance is particularly pronounced in regions with extensive offshore drilling activities and remote onshore operations, where the reliability and inherent safety of air starters are paramount.

Key Drivers for Dominance in Oil & Gas:

- Hazardous Environments: Air starters operate on compressed air, eliminating spark risks inherent in electrical systems, crucial for explosive atmospheres in upstream and downstream oil and gas operations.

- Remote Locations: The availability of compressed air infrastructure in many oil and gas facilities, coupled with the air starter's ability to function without reliance on electrical grids, makes them ideal for remote sites.

- Large Engine Requirements: The need to start large diesel and natural gas engines in drilling rigs, pumps, and compressors necessitates the high torque and reliable starting power provided by air starters.

- Regulatory Compliance: Stringent safety regulations in the Oil & Gas industry often favor air-starting systems due to their intrinsically safe nature.

Geographically, North America and the Middle East are identified as dominant regions for air starter consumption within the Oil & Gas sector. North America, with its significant shale gas and oil production, and the Middle East, a global hub for oil exports, exhibit high market penetration. The country-specific analysis reveals the United States and Saudi Arabia as key markets, driven by extensive investments in exploration and production. The Mining sector, particularly for large-scale mining operations in countries like Australia, Canada, and South Africa, also contributes substantially to the market. Here, the need to start heavy-duty diesel engines in remote and often challenging conditions solidifies the importance of air starters.

- Vane Air Starters represent the larger market share within the Type segment due to their established reliability and cost-effectiveness for a wide range of applications.

- Turbine Air Starters, while historically a smaller segment, are experiencing significant growth due to their higher power density and efficiency, making them increasingly attractive for larger engines and more demanding applications.

The Power Generation sector, especially for emergency backup diesel generators, further bolsters the demand for air starters, particularly in regions experiencing grid instability or requiring critical power continuity. The "Others" segment, encompassing applications like marine propulsion, construction equipment, and industrial compressors, collectively forms a significant and growing portion of the market, indicating a broad applicability of air starting technology.

Air Starter Industry Product Landscape

The Air Starter Industry is characterized by continuous product innovation aimed at enhancing efficiency, durability, and user-friendliness. Manufacturers are actively developing Vane Air Starter and Turbine Air Starter models that offer increased power output with reduced air consumption, leading to lower operational costs. Innovations include advanced sealing technologies to prevent leaks, more robust internal components for extended service life, and improved exhaust systems for quieter operation. Applications span across the Oil & Gas, Power Generation, and Mining sectors, where reliable engine starting is critical for operational continuity. Unique selling propositions often revolve around the inherent safety of air starters in hazardous environments, their ability to perform in extreme temperatures, and their low maintenance requirements compared to electrical alternatives. Technological advancements are also focusing on integrating smart features for diagnostics and predictive maintenance.

Key Drivers, Barriers & Challenges in Air Starter Industry

Key Drivers:

- Demand from Core Industries: Sustained growth and operational needs in the Oil & Gas, Power Generation, and Mining sectors, which rely heavily on reliable engine starting.

- Harsh Environment Suitability: Air starters' inherent safety and reliability in explosive, remote, and extreme temperature conditions where electric starters are less viable.

- Technological Advancements: Improvements in efficiency, power density, and durability of both Vane and Turbine air starters.

- Cost-Effectiveness: Lower total cost of ownership over the lifespan of the equipment compared to some electrical starting systems.

Key Barriers & Challenges:

- Competition from Electric Starters: The increasing availability and efficiency of electric starters in less demanding applications.

- Compressed Air Infrastructure Dependency: The requirement for a compressed air supply, which can be a limitation in some new or retrofitted installations.

- Supply Chain Disruptions: Global supply chain volatility can impact the availability of raw materials and components.

- Initial Investment Costs: For certain high-performance turbine air starters, the upfront cost can be a barrier for smaller enterprises.

- Environmental Regulations: Evolving environmental regulations might indirectly impact industries that are major consumers of air starters, leading to potential shifts in operational needs. For instance, a significant portion of the USD 1.5 billion market in 2025 is linked to these core industries.

Emerging Opportunities in Air Starter Industry

Emerging opportunities within the Air Starter Industry lie in the expanding applications of Turbine Air Starters for larger and more complex engines. The growing global emphasis on renewable energy infrastructure, particularly in areas that may lack stable grid power, presents a niche but expanding market for backup power solutions. Furthermore, the mining sector's increasing adoption of automation and remote operation technologies necessitates highly reliable and fault-tolerant starting systems. Untapped markets in developing economies with expanding industrial bases also offer significant growth potential. Innovative applications in specialized heavy-duty vehicles and industrial equipment not traditionally associated with air starters could unlock new revenue streams.

Growth Accelerators in the Air Starter Industry Industry

Several catalysts are accelerating the growth of the Air Starter Industry. Technological breakthroughs in materials science are leading to more durable and lighter components, enhancing the performance and reducing the maintenance of both vane and turbine air starters. Strategic partnerships between air starter manufacturers and original equipment manufacturers (OEMs) are ensuring integrated solutions and wider market penetration from the design phase onwards. Market expansion strategies targeting emerging economies with developing industrial infrastructure are also key growth accelerators. The increasing demand for robust and reliable solutions in the Oil & Gas and Mining sectors, estimated to contribute over 60% of the market value in 2025, continues to be a primary driver.

Key Players Shaping the Air Starter Industry Market

Notable Milestones in Air Starter Industry Sector

- 2021: Introduction of enhanced efficiency Turbine Air Starters by several key players, offering improved power-to-weight ratios.

- 2022: Increased focus on digitalization and IoT integration for remote diagnostics and predictive maintenance of air starter systems.

- 2023: Significant R&D investment in developing more compact and powerful Vane Air Starter models for niche applications.

- 2024: Consolidation within the industry through strategic acquisitions aimed at expanding product portfolios and market reach.

- 2025 (Projected): Launch of next-generation air starter technologies with a focus on reduced environmental impact and extended service intervals.

In-Depth Air Starter Industry Market Outlook

The Air Starter Industry is set for sustained and robust growth, with a promising market outlook. The intrinsic advantages of air starters in critical industrial applications, particularly in the Oil & Gas, Power Generation, and Mining sectors, will continue to drive demand. Technological advancements in turbine air starter efficiency and vane air starter durability will further solidify their market position. Emerging markets and innovative applications represent significant untapped potential. Strategic partnerships and a focus on providing integrated, reliable starting solutions are expected to be key growth accelerators, ensuring the industry's continued expansion and relevance in the global industrial landscape. The estimated market value of USD 1.5 billion in 2025 is projected to experience a healthy upward trend.

Air Starter Industry Segmentation

-

1. Type

- 1.1. Vane Air Starter

- 1.2. Turbine Air Starter

-

2. End-User

- 2.1. Oil & Gas

- 2.2. Power Generation

- 2.3. Mining

- 2.4. Others

Air Starter Industry Segmentation By Geography

- 1. North America

- 2. Asia Pacific

- 3. Europe

- 4. South America

- 5. Middle East and Africa

Air Starter Industry Regional Market Share

Geographic Coverage of Air Starter Industry

Air Starter Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.75% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Vane Air Starter

- 5.1.2. Turbine Air Starter

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Oil & Gas

- 5.2.2. Power Generation

- 5.2.3. Mining

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Asia Pacific

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Air Starter Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Vane Air Starter

- 6.1.2. Turbine Air Starter

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Oil & Gas

- 6.2.2. Power Generation

- 6.2.3. Mining

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Air Starter Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Vane Air Starter

- 7.1.2. Turbine Air Starter

- 7.2. Market Analysis, Insights and Forecast - by End-User

- 7.2.1. Oil & Gas

- 7.2.2. Power Generation

- 7.2.3. Mining

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Asia Pacific Air Starter Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Vane Air Starter

- 8.1.2. Turbine Air Starter

- 8.2. Market Analysis, Insights and Forecast - by End-User

- 8.2.1. Oil & Gas

- 8.2.2. Power Generation

- 8.2.3. Mining

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Air Starter Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Vane Air Starter

- 9.1.2. Turbine Air Starter

- 9.2. Market Analysis, Insights and Forecast - by End-User

- 9.2.1. Oil & Gas

- 9.2.2. Power Generation

- 9.2.3. Mining

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. South America Air Starter Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Vane Air Starter

- 10.1.2. Turbine Air Starter

- 10.2. Market Analysis, Insights and Forecast - by End-User

- 10.2.1. Oil & Gas

- 10.2.2. Power Generation

- 10.2.3. Mining

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Air Starter Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Vane Air Starter

- 11.1.2. Turbine Air Starter

- 11.2. Market Analysis, Insights and Forecast - by End-User

- 11.2.1. Oil & Gas

- 11.2.2. Power Generation

- 11.2.3. Mining

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Maradyne Corp

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Austart Air Starters

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Ingersoll-Rand Plc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Miller Air Starter Co Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 IPU Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Multi Torque Industries Pty Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 The Rowland Company

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 KH Equipment Pty Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Air Starter Components

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Gali Group

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Maradyne Corp

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Air Starter Industry Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Air Starter Industry Volume Breakdown (K Units, %) by Region 2025 & 2033

- Figure 3: North America Air Starter Industry Revenue (million), by Type 2025 & 2033

- Figure 4: North America Air Starter Industry Volume (K Units), by Type 2025 & 2033

- Figure 5: North America Air Starter Industry Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Air Starter Industry Volume Share (%), by Type 2025 & 2033

- Figure 7: North America Air Starter Industry Revenue (million), by End-User 2025 & 2033

- Figure 8: North America Air Starter Industry Volume (K Units), by End-User 2025 & 2033

- Figure 9: North America Air Starter Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 10: North America Air Starter Industry Volume Share (%), by End-User 2025 & 2033

- Figure 11: North America Air Starter Industry Revenue (million), by Country 2025 & 2033

- Figure 12: North America Air Starter Industry Volume (K Units), by Country 2025 & 2033

- Figure 13: North America Air Starter Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Air Starter Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Asia Pacific Air Starter Industry Revenue (million), by Type 2025 & 2033

- Figure 16: Asia Pacific Air Starter Industry Volume (K Units), by Type 2025 & 2033

- Figure 17: Asia Pacific Air Starter Industry Revenue Share (%), by Type 2025 & 2033

- Figure 18: Asia Pacific Air Starter Industry Volume Share (%), by Type 2025 & 2033

- Figure 19: Asia Pacific Air Starter Industry Revenue (million), by End-User 2025 & 2033

- Figure 20: Asia Pacific Air Starter Industry Volume (K Units), by End-User 2025 & 2033

- Figure 21: Asia Pacific Air Starter Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 22: Asia Pacific Air Starter Industry Volume Share (%), by End-User 2025 & 2033

- Figure 23: Asia Pacific Air Starter Industry Revenue (million), by Country 2025 & 2033

- Figure 24: Asia Pacific Air Starter Industry Volume (K Units), by Country 2025 & 2033

- Figure 25: Asia Pacific Air Starter Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Air Starter Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Air Starter Industry Revenue (million), by Type 2025 & 2033

- Figure 28: Europe Air Starter Industry Volume (K Units), by Type 2025 & 2033

- Figure 29: Europe Air Starter Industry Revenue Share (%), by Type 2025 & 2033

- Figure 30: Europe Air Starter Industry Volume Share (%), by Type 2025 & 2033

- Figure 31: Europe Air Starter Industry Revenue (million), by End-User 2025 & 2033

- Figure 32: Europe Air Starter Industry Volume (K Units), by End-User 2025 & 2033

- Figure 33: Europe Air Starter Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 34: Europe Air Starter Industry Volume Share (%), by End-User 2025 & 2033

- Figure 35: Europe Air Starter Industry Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Air Starter Industry Volume (K Units), by Country 2025 & 2033

- Figure 37: Europe Air Starter Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Air Starter Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: South America Air Starter Industry Revenue (million), by Type 2025 & 2033

- Figure 40: South America Air Starter Industry Volume (K Units), by Type 2025 & 2033

- Figure 41: South America Air Starter Industry Revenue Share (%), by Type 2025 & 2033

- Figure 42: South America Air Starter Industry Volume Share (%), by Type 2025 & 2033

- Figure 43: South America Air Starter Industry Revenue (million), by End-User 2025 & 2033

- Figure 44: South America Air Starter Industry Volume (K Units), by End-User 2025 & 2033

- Figure 45: South America Air Starter Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 46: South America Air Starter Industry Volume Share (%), by End-User 2025 & 2033

- Figure 47: South America Air Starter Industry Revenue (million), by Country 2025 & 2033

- Figure 48: South America Air Starter Industry Volume (K Units), by Country 2025 & 2033

- Figure 49: South America Air Starter Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: South America Air Starter Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Air Starter Industry Revenue (million), by Type 2025 & 2033

- Figure 52: Middle East and Africa Air Starter Industry Volume (K Units), by Type 2025 & 2033

- Figure 53: Middle East and Africa Air Starter Industry Revenue Share (%), by Type 2025 & 2033

- Figure 54: Middle East and Africa Air Starter Industry Volume Share (%), by Type 2025 & 2033

- Figure 55: Middle East and Africa Air Starter Industry Revenue (million), by End-User 2025 & 2033

- Figure 56: Middle East and Africa Air Starter Industry Volume (K Units), by End-User 2025 & 2033

- Figure 57: Middle East and Africa Air Starter Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 58: Middle East and Africa Air Starter Industry Volume Share (%), by End-User 2025 & 2033

- Figure 59: Middle East and Africa Air Starter Industry Revenue (million), by Country 2025 & 2033

- Figure 60: Middle East and Africa Air Starter Industry Volume (K Units), by Country 2025 & 2033

- Figure 61: Middle East and Africa Air Starter Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Middle East and Africa Air Starter Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Air Starter Industry Revenue million Forecast, by Type 2020 & 2033

- Table 2: Global Air Starter Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 3: Global Air Starter Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 4: Global Air Starter Industry Volume K Units Forecast, by End-User 2020 & 2033

- Table 5: Global Air Starter Industry Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Air Starter Industry Volume K Units Forecast, by Region 2020 & 2033

- Table 7: Global Air Starter Industry Revenue million Forecast, by Type 2020 & 2033

- Table 8: Global Air Starter Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 9: Global Air Starter Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 10: Global Air Starter Industry Volume K Units Forecast, by End-User 2020 & 2033

- Table 11: Global Air Starter Industry Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Air Starter Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 13: Global Air Starter Industry Revenue million Forecast, by Type 2020 & 2033

- Table 14: Global Air Starter Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 15: Global Air Starter Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 16: Global Air Starter Industry Volume K Units Forecast, by End-User 2020 & 2033

- Table 17: Global Air Starter Industry Revenue million Forecast, by Country 2020 & 2033

- Table 18: Global Air Starter Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 19: Global Air Starter Industry Revenue million Forecast, by Type 2020 & 2033

- Table 20: Global Air Starter Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 21: Global Air Starter Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 22: Global Air Starter Industry Volume K Units Forecast, by End-User 2020 & 2033

- Table 23: Global Air Starter Industry Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Air Starter Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 25: Global Air Starter Industry Revenue million Forecast, by Type 2020 & 2033

- Table 26: Global Air Starter Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 27: Global Air Starter Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 28: Global Air Starter Industry Volume K Units Forecast, by End-User 2020 & 2033

- Table 29: Global Air Starter Industry Revenue million Forecast, by Country 2020 & 2033

- Table 30: Global Air Starter Industry Volume K Units Forecast, by Country 2020 & 2033

- Table 31: Global Air Starter Industry Revenue million Forecast, by Type 2020 & 2033

- Table 32: Global Air Starter Industry Volume K Units Forecast, by Type 2020 & 2033

- Table 33: Global Air Starter Industry Revenue million Forecast, by End-User 2020 & 2033

- Table 34: Global Air Starter Industry Volume K Units Forecast, by End-User 2020 & 2033

- Table 35: Global Air Starter Industry Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Air Starter Industry Volume K Units Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Air Starter Industry?

The projected CAGR is approximately 4.75%.

2. Which companies are prominent players in the Air Starter Industry?

Key companies in the market include Maradyne Corp, Austart Air Starters, Ingersoll-Rand Plc, Miller Air Starter Co Inc, IPU Group, Multi Torque Industries Pty Ltd, The Rowland Company, KH Equipment Pty Ltd, Air Starter Components, Gali Group.

3. What are the main segments of the Air Starter Industry?

The market segments include Type, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 416.18 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Growing Vehicle Ownership4.; Government Initiatives.

6. What are the notable trends driving market growth?

Oil & Gas Sector to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Volatile Crude Oil Prices.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Air Starter Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Air Starter Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Air Starter Industry?

To stay informed about further developments, trends, and reports in the Air Starter Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence