Key Insights

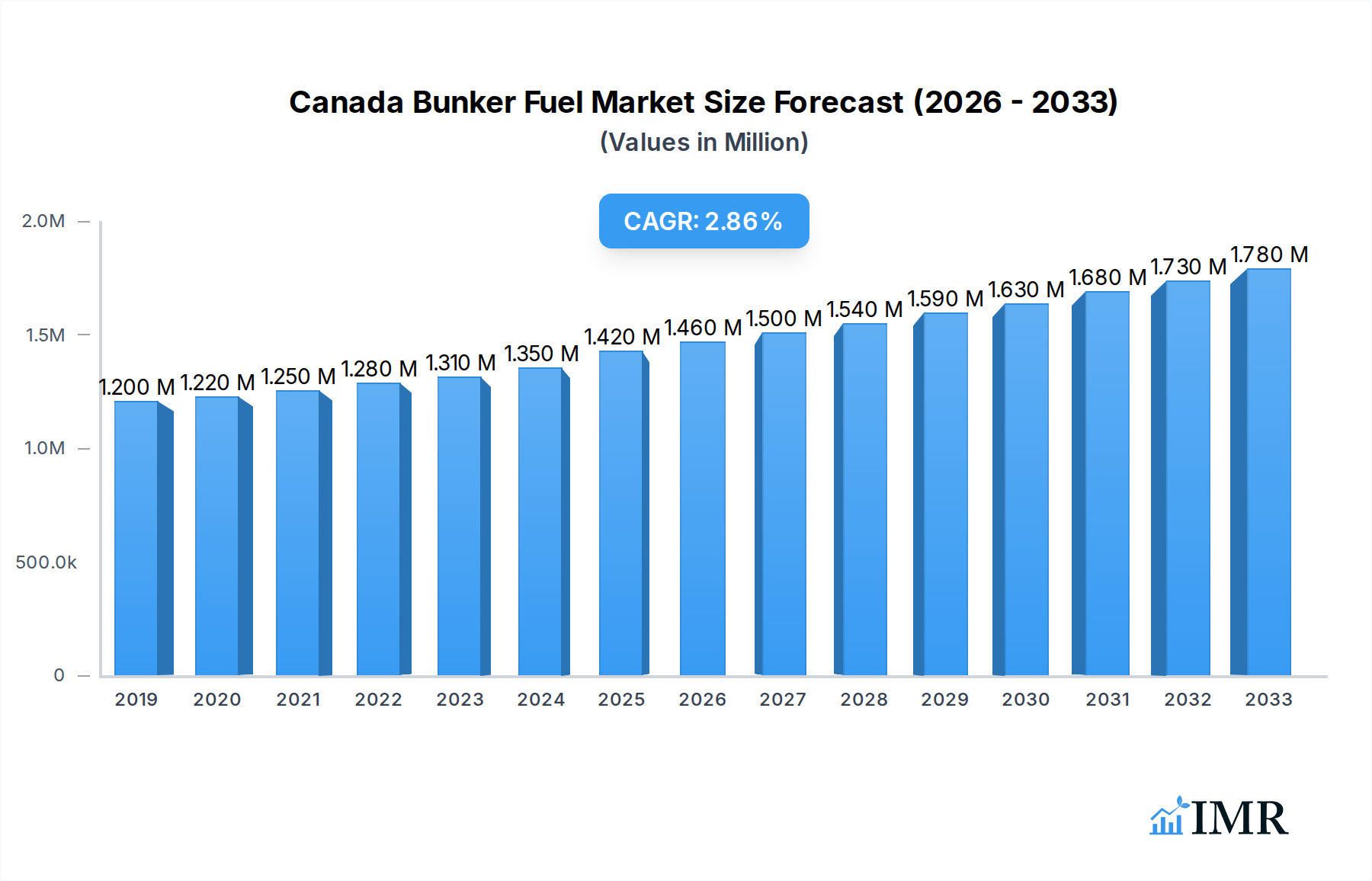

The Canadian bunker fuel market is poised for steady growth, projected to reach $1.42 million by 2025 and expand at a Compound Annual Growth Rate (CAGR) exceeding 2.93% through 2033. This expansion is driven by an increasing volume of maritime trade along Canada's extensive coastlines, necessitating a robust supply of marine fuels for a diverse range of vessels. Key growth catalysts include the continuous demand for container ships and tankers, which are essential for the import and export of goods and commodities. Furthermore, evolving environmental regulations are pushing for the adoption of cleaner fuel alternatives, presenting significant opportunities for Very-low Sulfur Fuel Oil (VLSFO) and Liquefied Natural Gas (LNG). The Canadian government's commitment to sustainable shipping practices and the development of port infrastructure further underpins this market's upward trajectory.

Canada Bunker Fuel Market Market Size (In Million)

Despite the positive outlook, the market faces certain restraints. The volatile nature of global oil prices can significantly impact bunker fuel costs, creating uncertainty for both suppliers and ship owners. Additionally, the substantial investment required for transitioning to newer, greener fuel technologies, such as LNG bunkering infrastructure, presents a financial hurdle. However, the long-term trend favors the adoption of low-sulfur and alternative fuels, driven by international maritime conventions and a growing emphasis on environmental stewardship. The market segmentation reveals a significant presence of High Sulfur Fuel Oil (HSFO) and VLSFO, with LNG emerging as a key growth segment, aligning with global decarbonization efforts. Major players in the fuel supply and shipping industries, including PetroChina, TotalEnergies, Maersk, and Cosco Shipping Lines, are actively shaping the competitive landscape through strategic partnerships and infrastructure investments.

Canada Bunker Fuel Market Company Market Share

Canada Bunker Fuel Market: Comprehensive Insights & Forecasts (2019-2033)

Unlock the future of Canada's maritime energy with this in-depth report on the Canada Bunker Fuel Market. Covering historical trends from 2019-2024 and offering projections through 2033, this analysis delves into market dynamics, growth drivers, key players, and emerging opportunities. Essential for fuel suppliers, ship owners, and industry stakeholders seeking to navigate the evolving landscape of marine fuels in Canada.

Canada Bunker Fuel Market Market Dynamics & Structure

The Canada Bunker Fuel Market is characterized by a dynamic interplay of factors shaping its structure and competitive landscape. Market concentration is influenced by the presence of major international and domestic fuel suppliers alongside large shipping conglomerates that directly or indirectly impact fuel demand. Technological innovation is a significant driver, particularly in the pursuit of lower sulfur content fuels and alternative maritime energy sources like Liquefied Natural Gas (LNG). Regulatory frameworks, including International Maritime Organization (IMO) 2020 sulfur cap regulations and Canada's own environmental policies, are paramount in dictating fuel choices and compliance strategies. Competitive product substitutes are emerging rapidly, with a growing emphasis on cleaner fuels such as Very-low Sulfur Fuel Oil (VLSFO), Marine Gas Oil (MGO), and increasingly, LNG. End-user demographics are primarily driven by the vessel types operating within Canadian waters, including Containers, Tankers, General Cargo, and Bulk Carriers. Mergers and acquisitions (M&A) trends, while perhaps less prevalent than in some other energy sectors, can significantly alter market shares and operational capabilities. For instance, the recent merger of Cryopeak LNG Solutions and Ferus Natural Gas Fuels indicates consolidation in the LNG bunkering infrastructure space. Innovation barriers include the high capital investment required for new bunkering infrastructure, especially for alternative fuels, and the need for standardized safety protocols.

- Market Concentration: Dominated by a few large fuel suppliers and influenced by major ship owners.

- Technological Innovation Drivers: Focus on sulfur reduction, emissions control, and alternative fuels like LNG and biofuels.

- Regulatory Frameworks: IMO 2020 sulfur cap, Canadian environmental regulations, and emissions reduction targets.

- Competitive Product Substitutes: VLSFO, MGO, LNG, and emerging biofuels gaining traction.

- End-User Demographics: Driven by demand from Container ships, Tankers, Bulk Carriers, and General Cargo vessels.

- M&A Trends: Indications of consolidation in the LNG bunkering sector.

- Innovation Barriers: High infrastructure costs, safety standardization challenges.

Canada Bunker Fuel Market Growth Trends & Insights

The Canada Bunker Fuel Market is poised for significant evolution, driven by a confluence of environmental regulations, technological advancements, and shifting consumer behavior within the shipping industry. The market size has witnessed a steady growth trajectory, with its evolution closely tied to global maritime trade volumes and Canada's position as a key facilitator of international and coastal shipping. Adoption rates of cleaner fuels have been accelerating, directly influenced by the stringent sulfur emission limits mandated by international and domestic regulations. This has led to a discernible shift away from High Sulfur Fuel Oil (HSFO) towards Very-low Sulfur Fuel Oil (VLSFO) and Marine Gas Oil (MGO). Technological disruptions are at the forefront, with Liquefied Natural Gas (LNG) emerging as a prominent alternative fuel, offering substantial reductions in sulfur dioxide, nitrogen oxides, and particulate matter emissions. The development of LNG bunkering infrastructure and the increasing availability of LNG-powered vessels are key indicators of this disruption. Consumer behavior shifts are also evident, with ship owners and operators prioritizing vessels and fuel choices that ensure long-term compliance, operational efficiency, and enhanced corporate sustainability credentials. The forecast period from 2025 to 2033 is expected to witness a considerable CAGR driven by these factors. Market penetration of alternative fuels, particularly LNG, is projected to expand significantly as economies of scale are achieved and infrastructure networks mature. The historical period from 2019 to 2024 laid the groundwork for this transition, with initial adaptations to stricter sulfur regulations. The estimated market size in 2025 is projected to be in the billions of Canadian dollars, reflecting the substantial volume of bunker fuel consumed.

Dominant Regions, Countries, or Segments in Canada Bunker Fuel Market

The Canada Bunker Fuel Market's dominance is a multi-faceted phenomenon, influenced by key segments within fuel types and vessel operations, underpinned by regional infrastructure and economic activity. Liquefied Natural Gas (LNG) has emerged as a particularly dominant and growth-driving fuel type. Its ability to significantly reduce emissions compared to traditional heavy fuel oils aligns perfectly with Canada's commitment to environmental stewardship and international maritime decarbonization goals. The increasing investment in LNG production and distribution networks across the country, exemplified by the planned merger of Cryopeak LNG Solutions and Ferus Natural Gas Fuels, directly fuels its market dominance.

Within Vessel Type, Containers and Tankers represent the most significant demand segments. Container ships, vital for global trade and Canada's import/export activities, have a substantial and consistent need for bunker fuel. Similarly, Tankers, crucial for transporting oil and gas, represent a large and steady market. However, the increasing adoption of LNG as a cleaner fuel is also influencing these segments, with new builds and retrofits focusing on LNG capabilities.

Geographically, while the entire Canadian coastline is relevant, regions with major port infrastructure and high shipping traffic, such as those along the Pacific Coast (e.g., Vancouver) and the Atlantic Coast (e.g., Halifax, Montreal via the St. Lawrence Seaway), are the primary hubs for bunker fuel consumption and distribution. The development of LNG bunkering facilities in these key ports will further solidify their dominance.

- Dominant Fuel Type: Liquefied Natural Gas (LNG) due to its environmental advantages and growing infrastructure.

- Key Drivers for LNG Dominance:

- Strict emissions regulations and decarbonization targets.

- Government support and investment in LNG infrastructure.

- Increasing availability of LNG-powered vessels.

- Reduction in sulfur, NOx, and particulate matter emissions.

- Dominant Vessel Types:

- Containers: High volume of trade necessitates consistent fuel supply.

- Tankers: Essential for energy transportation, with significant fuel requirements.

- Key Drivers for Vessel Type Dominance:

- Canada's role in international and coastal trade.

- Specific fuel needs for long-haul and bulk transport.

- Dominant Geographic Regions:

- Pacific Coast (e.g., Vancouver): Major gateway for Asian trade.

- Atlantic Coast (e.g., Halifax, Montreal): Hub for transatlantic trade and domestic shipping.

- Key Drivers for Regional Dominance:

- Presence of major deep-water ports and logistics hubs.

- Proximity to key shipping lanes.

- Development of specialized bunkering facilities.

- Market Share Analysis: LNG's market share is projected to grow substantially, potentially reaching XX% by 2033, impacting the shares of VLSFO and MGO. Container vessels are estimated to account for over XX% of bunker fuel demand.

Canada Bunker Fuel Market Product Landscape

The product landscape of the Canada Bunker Fuel Market is undergoing a significant transformation driven by environmental regulations and the pursuit of sustainable maritime operations. High Sulfur Fuel Oil (HSFO) is gradually being phased out in many applications due to its high sulfur content, while Very-low Sulfur Fuel Oil (VLSFO) and Marine Gas Oil (MGO) have become the prevalent compliant fuels, offering significantly reduced sulfur emissions. The most disruptive innovation is the increasing adoption of Liquefied Natural Gas (LNG), a cryogenic fuel that offers substantial reductions in sulfur, nitrogen oxides, and particulate matter. Other emerging fuel types, such as advanced biofuels (e.g., B100 biodiesel initiatives by CSL Group), are also carving out niche applications, demonstrating a commitment to diverse decarbonization pathways. The performance metrics of these fuels are evaluated based on their environmental impact, energy density, compatibility with existing and new engine technologies, and cost-effectiveness. The unique selling proposition for LNG lies in its significant emission reduction capabilities, while biofuels highlight a circular economy approach and the utilization of waste materials. Technological advancements in engine design and fuel processing are crucial for optimizing the performance and efficiency of these diverse fuel types in the Canadian context.

Key Drivers, Barriers & Challenges in Canada Bunker Fuel Market

The Canada Bunker Fuel Market is propelled by several key drivers, primarily the stringent global and national environmental regulations like IMO 2020, pushing for cleaner fuels and reduced emissions. Technological advancements in engine efficiency and the development of alternative fuel sources, such as LNG and biofuels, are crucial catalysts. Furthermore, Canada's commitment to decarbonization targets and increasing global awareness of climate change are significant policy-driven factors. The growing demand for energy transportation and trade, both domestically and internationally, also underpins market growth.

However, the market faces significant barriers and challenges. The high capital investment required for developing new bunkering infrastructure, especially for LNG, presents a major hurdle. The availability and logistical complexities of new fuel types, coupled with the need for specialized training for personnel, also pose challenges. Regulatory uncertainty and the harmonization of international standards can create implementation complexities. Supply chain disruptions, geopolitical factors affecting fuel prices, and the competitive pressure from established fuel suppliers are additional restraints impacting market expansion. The cost-competitiveness of alternative fuels compared to traditional bunker fuels remains a critical factor for widespread adoption.

Emerging Opportunities in Canada Bunker Fuel Market

Emerging opportunities in the Canada Bunker Fuel Market are predominantly centered around the expansion of cleaner energy solutions for maritime transport. The growing global mandate for decarbonization presents a significant opening for the widespread adoption of Liquefied Natural Gas (LNG) as a primary bunker fuel. Investments in LNG bunkering infrastructure across Canada's key ports, from the West Coast to the East Coast, represent a substantial growth avenue. Furthermore, the development and scaling of biofuels, such as B100 biodiesel initiatives, offer a promising pathway for reducing the carbon footprint of existing vessel fleets. Untapped markets lie in providing comprehensive bunkering solutions for these alternative fuels in regions with currently limited infrastructure. Evolving consumer preferences, driven by corporate sustainability goals and investor pressure, are creating demand for ships powered by or capable of using low-carbon fuels, opening avenues for specialized fuel suppliers and technology providers. The demand for greener shipping corridors and emission reduction services also presents a significant opportunity for innovation and market leadership.

Growth Accelerators in the Canada Bunker Fuel Market Industry

Several catalysts are poised to accelerate long-term growth in the Canada Bunker Fuel Market. Technological breakthroughs in fuel cell technology for maritime applications, while still nascent, hold immense potential for zero-emission shipping. Strategic partnerships between fuel producers, shipping companies, and port authorities are crucial for building robust supply chains and investing in necessary infrastructure. The expansion of LNG liquefaction and regasification terminals, coupled with the development of dedicated LNG bunkering vessels, will significantly boost its availability and competitiveness. Government incentives, such as tax credits for adopting cleaner fuels and investing in green maritime technologies, are vital for de-risking investments and encouraging wider adoption. The increasing number of new-build vessels designed for alternative fuels will create sustained demand, while retrofitting existing fleets will further expand the market for compliant fuels. The drive towards digitalization in bunkering operations, optimizing logistics and transaction processes, will also contribute to efficiency and growth.

Key Players Shaping the Canada Bunker Fuel Market Market

- PetroChina Company Limited

- TotalEnergies SE

- Peninsula Petroleum Ltd

- A P Møller – Mærsk AS

- World Fuel Services Corporation

- Cosco Shipping Lines Co Ltd

- Orient Overseas Container Line (OOCL)

- Mediterranean Shipping Company

- Ocean Network Express

- CMA CGM Group

- CSL Group

- Canada Clean Fuels Inc.

- Cryopeak LNG Solutions

- Ferus Natural Gas Fuels

Notable Milestones in Canada Bunker Fuel Market Sector

- May 2024: CSL Group announced that its gearless bulk carrier, CSL Welland, will operate on B100 biodiesel for the upcoming season, revitalizing its biofuel initiative. In collaboration with Canada Clean Fuels Inc., eight of its vessels will be fueled with B100 biodiesel sourced from North America and produced from waste plant materials.

- February 2024: Cryopeak LNG Solutions signed an agreement to merge operations with Ferus Natural Gas Fuels, aiming to establish a comprehensive LNG production and distribution organization across Canada. This expansion includes managing three LNG production facilities in Western Canada and operating the country's largest LNG transportation network.

In-Depth Canada Bunker Fuel Market Market Outlook

The Canada Bunker Fuel Market outlook is exceptionally positive, driven by an accelerating global and domestic push towards sustainable maritime energy. The forecast period is characterized by a pronounced shift towards Liquefied Natural Gas (LNG), with substantial investments in production, distribution, and bunkering infrastructure set to solidify its market position. Emerging biofuel initiatives, demonstrating innovative uses of waste materials, offer a complementary pathway for decarbonization, particularly for existing fleets. The demand for cleaner fuels will continue to grow, creating strategic opportunities for companies that can reliably supply compliant and cost-effective bunker fuel solutions. Collaboration between industry stakeholders, government support for green maritime technologies, and the development of specialized port facilities will be crucial growth accelerators. The market is poised for significant expansion as Canada solidifies its role as a responsible provider of future-proof maritime energy.

Canada Bunker Fuel Market Segmentation

-

1. Fuel Type

- 1.1. High Sulfur Fuel Oil (HSFO)

- 1.2. Very-low Sulfur Fuel Oil (VLSFO)

- 1.3. Marine Gas Oil (MGO)

- 1.4. Liquefied Natural Gas (LNG)

- 1.5. Other Fuel Types

-

2. Vessel Type

- 2.1. Containers

- 2.2. Tankers

- 2.3. General Cargo

- 2.4. Bulk Carrier

- 2.5. Other Vessel Types

Canada Bunker Fuel Market Segmentation By Geography

- 1. Canada

Canada Bunker Fuel Market Regional Market Share

Geographic Coverage of Canada Bunker Fuel Market

Canada Bunker Fuel Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 2.93% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 5.1.1. High Sulfur Fuel Oil (HSFO)

- 5.1.2. Very-low Sulfur Fuel Oil (VLSFO)

- 5.1.3. Marine Gas Oil (MGO)

- 5.1.4. Liquefied Natural Gas (LNG)

- 5.1.5. Other Fuel Types

- 5.2. Market Analysis, Insights and Forecast - by Vessel Type

- 5.2.1. Containers

- 5.2.2. Tankers

- 5.2.3. General Cargo

- 5.2.4. Bulk Carrier

- 5.2.5. Other Vessel Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6. Canada Bunker Fuel Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6.1.1. High Sulfur Fuel Oil (HSFO)

- 6.1.2. Very-low Sulfur Fuel Oil (VLSFO)

- 6.1.3. Marine Gas Oil (MGO)

- 6.1.4. Liquefied Natural Gas (LNG)

- 6.1.5. Other Fuel Types

- 6.2. Market Analysis, Insights and Forecast - by Vessel Type

- 6.2.1. Containers

- 6.2.2. Tankers

- 6.2.3. General Cargo

- 6.2.4. Bulk Carrier

- 6.2.5. Other Vessel Types

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Fuel Suppliers

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 1 PetroChina Company Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 2 TotalEnergies SE

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 3 Peninsula Petroleum Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 4 A P Møller – Mærsk AS

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 5 World Fuel Services Corporation

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Ship Owners

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 1 Cosco Shipping Lines Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 2 Orient Overseas Container Line (OOCL)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 3 Mediterranean Shipping Company

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 4 Ocean Network Express

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 5 CMA CGM Group*List Not Exhaustive 6 4 List of Other Prominent Companies6 5 Market Ranking/ Share Analysi

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Fuel Suppliers

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Canada Bunker Fuel Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Canada Bunker Fuel Market Share (%) by Company 2025

List of Tables

- Table 1: Canada Bunker Fuel Market Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 2: Canada Bunker Fuel Market Volume Billion Forecast, by Fuel Type 2020 & 2033

- Table 3: Canada Bunker Fuel Market Revenue Million Forecast, by Vessel Type 2020 & 2033

- Table 4: Canada Bunker Fuel Market Volume Billion Forecast, by Vessel Type 2020 & 2033

- Table 5: Canada Bunker Fuel Market Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Canada Bunker Fuel Market Volume Billion Forecast, by Region 2020 & 2033

- Table 7: Canada Bunker Fuel Market Revenue Million Forecast, by Fuel Type 2020 & 2033

- Table 8: Canada Bunker Fuel Market Volume Billion Forecast, by Fuel Type 2020 & 2033

- Table 9: Canada Bunker Fuel Market Revenue Million Forecast, by Vessel Type 2020 & 2033

- Table 10: Canada Bunker Fuel Market Volume Billion Forecast, by Vessel Type 2020 & 2033

- Table 11: Canada Bunker Fuel Market Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Canada Bunker Fuel Market Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Bunker Fuel Market?

The projected CAGR is approximately > 2.93%.

2. Which companies are prominent players in the Canada Bunker Fuel Market?

Key companies in the market include Fuel Suppliers, 1 PetroChina Company Limited, 2 TotalEnergies SE, 3 Peninsula Petroleum Ltd, 4 A P Møller – Mærsk AS, 5 World Fuel Services Corporation, Ship Owners, 1 Cosco Shipping Lines Co Ltd, 2 Orient Overseas Container Line (OOCL), 3 Mediterranean Shipping Company, 4 Ocean Network Express, 5 CMA CGM Group*List Not Exhaustive 6 4 List of Other Prominent Companies6 5 Market Ranking/ Share Analysi.

3. What are the main segments of the Canada Bunker Fuel Market?

The market segments include Fuel Type, Vessel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.42 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Rising LNG Trade4.; Surge in Marine Transportation.

6. What are the notable trends driving market growth?

The Very Low Sulphur Fuel Oil (VLSFO) Segment is to Witness Significant Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

4.; Rising LNG Trade4.; Surge in Marine Transportation.

8. Can you provide examples of recent developments in the market?

May 2024: CSL Group, a Canadian company, announced that its gearless bulk carrier, CSL Welland, will once again operate on B100 biodiesel for the upcoming season, signaling the revival of its biofuel initiative. In collaboration with Canada Clean Fuels Inc., the company is fueling eight of its vessels with B100 biodiesel sourced from North America and produced from waste plant materials.February 2024: Cryopeak LNG Solutions signed an agreement to merge operations with Ferus Natural Gas Fuels to develop a new liquefied natural gas (LNG) production and distribution organization across Canada. The company also manages three LNG production facilities through this expansion in Western Canada and operates the country's most significant LNG transportation.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Bunker Fuel Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Bunker Fuel Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Bunker Fuel Market?

To stay informed about further developments, trends, and reports in the Canada Bunker Fuel Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence