Key Insights

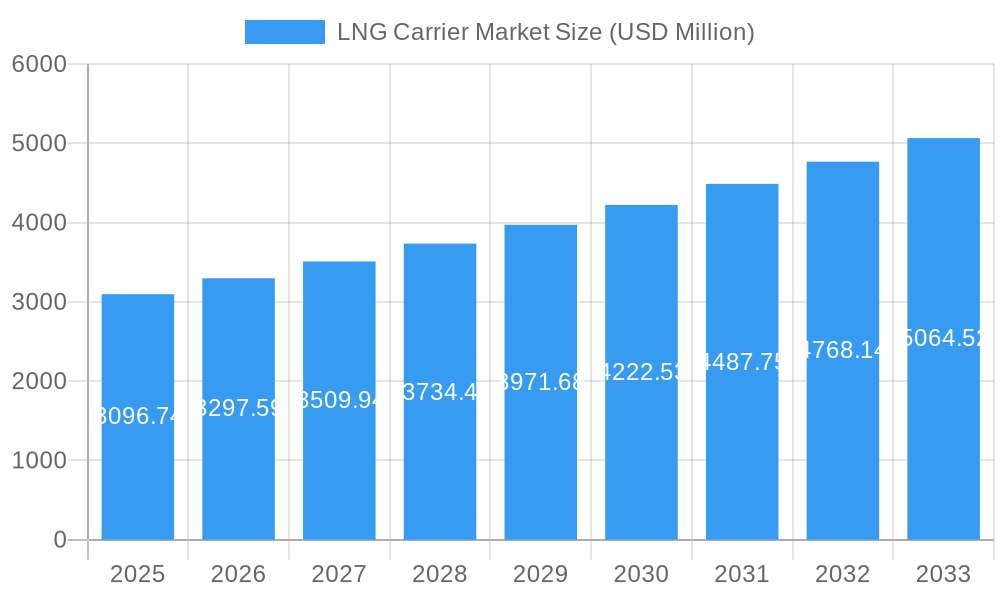

The global LNG carrier market is poised for substantial growth, projected to reach $3096.74 million in 2025, with a robust CAGR of 6.56% anticipated to sustain this upward trajectory through 2033. This expansion is primarily fueled by the increasing global demand for liquefied natural gas (LNG) as a cleaner and more sustainable energy alternative to traditional fossil fuels. The rising energy needs in developing economies, coupled with stringent environmental regulations pushing for reduced emissions, are significant drivers behind this demand. Furthermore, the ongoing energy transition and the strategic importance of energy security for many nations are bolstering investments in LNG infrastructure, including a growing fleet of specialized LNG carriers. The market's growth is further supported by advancements in vessel technology, leading to more efficient and environmentally friendly propulsion systems, which are increasingly being adopted by shipbuilders and operators.

LNG Carrier Market Market Size (In Billion)

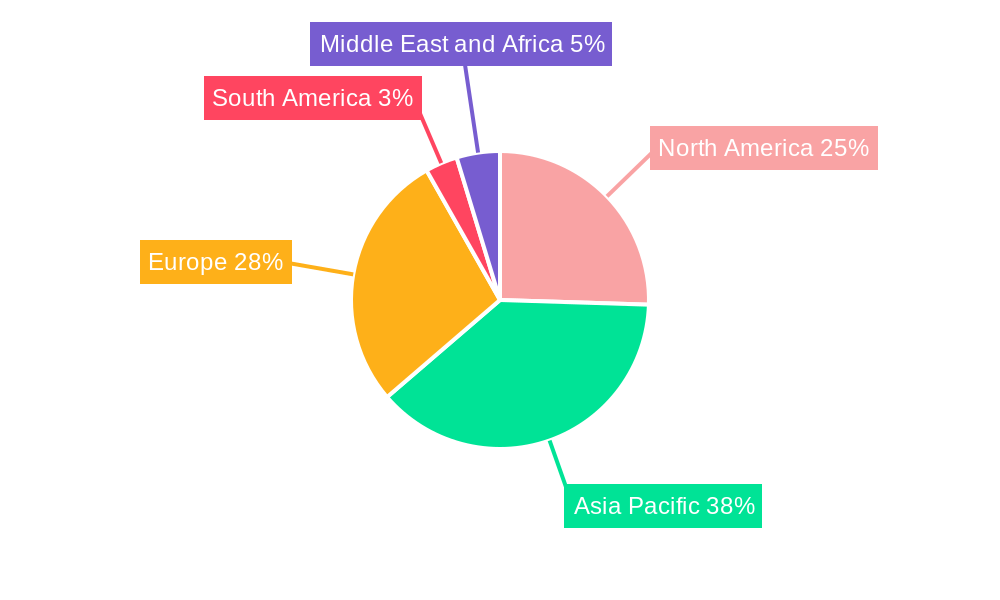

Key segments within the LNG carrier market include containment types like Moss and Membrane, offering different advantages for LNG storage and transportation. The propulsion type segment is characterized by a shift towards more fuel-efficient and lower-emission technologies, with Steam Turbines, Dual Fuel, Slow-Speed Diesel (SSD), XDF Two-stroke Engines, and Steam Re-heat and Stage technologies gaining prominence. Major players such as Samsung Heavy Industries, Hyundai Samho Heavy Industries, and Mitsui OSK Lines are actively investing in expanding their fleets and developing innovative carrier designs to meet the evolving market demands. Geographically, the Asia Pacific region, particularly China and South Korea, is expected to lead in both shipbuilding capacity and demand for LNG carriers, driven by their substantial energy consumption and ongoing infrastructure development. North America and Europe also represent significant markets, with a focus on upgrading existing fleets and incorporating advanced technologies to comply with stricter environmental standards.

LNG Carrier Market Company Market Share

This comprehensive report offers an in-depth analysis of the global LNG carrier market, providing critical insights into market dynamics, growth trends, regional dominance, product landscape, key drivers, barriers, challenges, emerging opportunities, and growth accelerators. Covering the historical period from 2019-2024 and a forecast period from 2025-2033, with a base year of 2025, this study is an essential resource for industry professionals seeking to understand the evolving LNG shipping sector. The report presents all values in million units and integrates high-traffic keywords to maximize search engine visibility.

LNG Carrier Market Market Dynamics & Structure

The global LNG carrier market is characterized by a moderate level of concentration, with key players actively engaged in strategic alliances and mergers to enhance their operational capabilities and market reach. Technological innovation is a significant driver, with continuous advancements in propulsion systems, containment technologies, and vessel design aiming to improve efficiency, safety, and environmental compliance. Regulatory frameworks, driven by increasing global environmental awareness and the push for decarbonization, are shaping the future of LNG transportation. For instance, the International Maritime Organization's (IMO) stricter emissions regulations are compelling shipbuilders and operators to invest in cleaner technologies. Competitive product substitutes, such as alternative fuel carriers and pipeline transportation, pose a challenge, but the unique energy density and logistical advantages of LNG maintain its dominance in specific markets. End-user demographics are shifting, with growing demand from developing economies and a greater emphasis on energy security.

- Market Concentration: Moderate, with key players dominating newbuild orders and charter agreements.

- Technological Innovation: Focus on dual-fuel engines, advanced membrane containment systems, and digitalization for optimized operations.

- Regulatory Frameworks: Stringent emissions standards and safety regulations are driving investment in advanced vessel technologies.

- Competitive Product Substitutes: Ethane carriers, hydrogen carriers, and advancements in pipeline infrastructure.

- End-User Demographics: Growing demand from Asia-Pacific and emerging markets; increasing focus on energy security.

- M&A Trends: Strategic partnerships and acquisitions to consolidate market share and gain access to new technologies and routes. For example, recent agreements highlight a trend of time chartering new builds and acquiring stakes in existing vessels.

LNG Carrier Market Growth Trends & Insights

The LNG carrier market is poised for significant expansion, driven by the escalating global demand for liquefied natural gas as a cleaner alternative to traditional fossil fuels. This growth is underpinned by increasing energy consumption in developing economies, the need for enhanced energy security, and the ongoing transition towards lower-carbon energy sources. The market size is projected to witness a robust compound annual growth rate (CAGR) from 2025 to 2033. Adoption rates for advanced LNG carrier technologies, such as dual-fuel propulsion and highly efficient containment systems, are accelerating as operators strive to meet stricter environmental regulations and improve operational economics. Technological disruptions, including the development of innovative cargo containment solutions that reduce construction costs and enhance safety, are reshaping the shipbuilding landscape. Consumer behavior shifts, characterized by a greater preference for flexible and reliable energy supply chains, further bolster the demand for a modern and efficient LNG carrier fleet. For instance, the adoption of new designs that simplify construction and reduce capital expenditure is a key indicator of this trend. The increasing reliance on LNG for power generation and industrial processes worldwide will continue to fuel demand for specialized shipping capacity.

Dominant Regions, Countries, or Segments in LNG Carrier Market

The global LNG carrier market's growth is significantly influenced by a confluence of factors across dominant regions, countries, and specific market segments. Among the containment types, Membrane technology is increasingly favored due to its space efficiency and suitability for larger vessel capacities, directly impacting market share and growth potential. This segment's dominance is amplified by its compatibility with newer, larger vessel designs that are crucial for economies of scale in global LNG trade. In terms of propulsion, Dual Fuel engines, particularly the XDF Two-stroke Engine variants, are emerging as the leading choice, driven by stringent environmental regulations and the pursuit of reduced emissions. This propulsion type is critical for operators looking to comply with global sulfur caps and other environmental mandates, thereby capturing a substantial market share.

Containment Type Dominance:

- Membrane: Preferred for its cargo capacity and structural integrity, leading the market in new vessel orders. Significant investments in R&D for improved membrane designs contribute to its leading position.

- Moss: While historically significant, it is now facing increased competition from more efficient membrane systems for new builds.

Propulsion Type Dominance:

- Dual Fuel (specifically XDF Two-stroke Engine): This segment is experiencing rapid growth due to its ability to run on both LNG and conventional marine fuels, offering flexibility and significant emissions reductions. It is the key driver for new vessel specifications.

- Steam Turbines: Traditional but being phased out in favor of more fuel-efficient and environmentally compliant options.

- Slow-Speed Diesel (SSD): Remains a viable option for certain vessel types but faces competition from dual-fuel technologies.

- Steam Re-heat and Stage: Advanced steam turbine technology offering improved efficiency over older systems.

Key drivers for this dominance include robust economic policies supporting energy infrastructure development, particularly in regions with substantial LNG import and export capabilities. Countries in the Asia-Pacific region, such as China, Japan, and South Korea, are at the forefront of LNG carrier demand, driven by their growing energy needs and substantial shipbuilding capacities. Infrastructure development, including the expansion of LNG terminals and regasification facilities, directly correlates with the demand for efficient LNG transportation. Furthermore, government initiatives promoting cleaner energy adoption and supporting the maritime industry's transition to greener technologies are pivotal. Market share analysis indicates a clear trend towards vessels equipped with membrane containment and dual-fuel propulsion, reflecting industry-wide investment and preference.

LNG Carrier Market Product Landscape

The LNG carrier market's product landscape is defined by continuous innovation aimed at enhancing efficiency, safety, and environmental sustainability. Leading shipyards are focusing on developing vessels with increased cargo capacities and advanced containment systems, such as the Membrane type, which offers superior volumetric efficiency and structural integrity. Propulsion technologies are also a focal point, with the widespread adoption of Dual Fuel engines, particularly the XDF Two-stroke Engine, enabling vessels to run on both LNG and conventional fuels, thereby significantly reducing emissions. The M-type E and Steam Re-heat and Stage technologies represent further advancements in optimizing fuel consumption and operational performance. Unique selling propositions for new builds include improved hull designs for reduced drag, advanced ballast water treatment systems, and sophisticated cargo management systems.

Key Drivers, Barriers & Challenges in LNG Carrier Market

The LNG carrier market is propelled by several key drivers. The global shift towards cleaner energy sources, driven by environmental concerns and regulatory mandates, is a primary catalyst, increasing the demand for LNG as a transitional fuel. Growing energy consumption, particularly in emerging economies, necessitates robust and flexible transportation solutions that LNG carriers provide. Technological advancements in shipbuilding, such as the development of more fuel-efficient engines and advanced containment systems, are also driving market growth. Strategic partnerships and the expansion of LNG liquefaction and regasification capacities worldwide create a favorable ecosystem for LNG shipping.

However, the market faces significant barriers and challenges. High capital costs associated with building LNG carriers, coupled with the long lead times for construction, pose a considerable hurdle. Volatility in global energy prices and geopolitical factors can impact LNG demand and charter rates, creating uncertainty. Stringent environmental regulations, while a driver, also require substantial investment in compliant technologies. Furthermore, competition from alternative energy sources and the development of new transportation infrastructure can pose threats. Supply chain disruptions and the availability of skilled labor in the shipbuilding industry can also present challenges to timely project execution.

Emerging Opportunities in LNG Carrier Market

Emerging opportunities in the LNG carrier market are diverse and promising, driven by the evolving global energy landscape. The increasing focus on decarbonization is creating a demand for next-generation LNG carriers, including those equipped with advanced propulsion systems that can run on lower-carbon fuels or be retrofitted for future fuel types. Untapped markets, particularly in regions undergoing rapid industrialization and seeking to diversify their energy mix, present significant growth potential. Innovative applications, such as the use of smaller, specialized LNG carriers for coastal and regional trade, are also gaining traction. Evolving consumer preferences for more sustainable and reliable energy supplies will further bolster the demand for efficient and environmentally responsible LNG transportation solutions, including the development of floating storage and regasification units (FSRUs).

Growth Accelerators in the LNG Carrier Market Industry

Several catalysts are accelerating growth within the LNG carrier market. Technological breakthroughs in dual-fuel engine efficiency and the development of advanced, cost-effective membrane containment systems are making LNG transportation more economically viable and environmentally compliant. Strategic partnerships between shipowners, charterers, and shipbuilders are streamlining the development and deployment of new vessels. Furthermore, the expansion of LNG liquefaction and export capacity globally, particularly in North America and the Middle East, directly fuels the demand for carrier capacity. Government policies promoting LNG as a cleaner alternative and supporting the maritime industry's green transition are also significant growth accelerators, encouraging investment and fleet modernization.

Key Players Shaping the LNG Carrier Market Market

- Ship Builders

- 4 MISC Berhad

- 8 Japan Marine United Corporation

- 9 GasLog Ltd

- 3 Mitsui OSK Lines Ltd

- 8 BW LPG

- Ship Operators

- 4 STX Offshore and Shipbuilding CO LTD

- 3 Daewoo Shipbuilding and Marine Engineering Co Ltd

- 6 Kawasaki Heavy Industries Ltd

- 1 Royal Dutch Shell PLC

- 2 Nippon Yusen Kabushiki Kaisha

- 6 Maran Gas Maritime Inc

- 5 Seapeak

- 1 Samsung Heavy Industries Co Ltd

- 7 China Shipbuilding Trading Co Ltd

- 5 Mitsubishi Heavy Industries Ltd

- 7 Golar LNG

- 10 Kawasaki Kisen Kaisha Ltd List Not Exhaustive

- 2 Hyundai Samho Heavy Industries Co Ltd

- 9 HJ Shipbuilding & Construction Company Ltd

Notable Milestones in LNG Carrier Market Sector

- December 2022: GAIL (India) Ltd agreed to time charter a new liquefied natural gas (LNG) carrier with Japan's Mitsui O. S. K. Lines Ltd (MOL) and acquired a stake in an existing LNG carrier. The new LNG carrier, built by South Korea's Daewoo Shipbuilding & Marine Engineering Co Ltd, will be the second MOL Group LNG ship to serve GAIL and will commence time chartering in 2023. This event underscores the growing demand for new builds and the strategic importance of chartering agreements in the market.

- October 2022: GTT announced that it earned two Approvals in Principle (AiP) from DNV and Bureau Veritas for its revolutionary three-tank LNG tanker design. The three-tank LNG carrier concept reduces construction costs by eliminating one cofferdam, one pump tower, and all related cryogenic equipment. This innovation signifies a significant advancement in shipbuilding efficiency and cost reduction, potentially impacting future vessel designs.

In-Depth LNG Carrier Market Market Outlook

The future outlook for the LNG carrier market is exceptionally strong, fueled by the ongoing global energy transition and the increasing reliance on LNG as a cleaner, more versatile fuel. Growth accelerators such as advancements in propulsion technology, including the widespread adoption of dual-fuel XDF engines, and the development of more efficient membrane containment systems are paving the way for a more sustainable and cost-effective shipping industry. Strategic partnerships among key market players, coupled with substantial investments in new liquefaction and regasification facilities worldwide, will continue to drive demand for a modern and expanded LNG carrier fleet. Emerging opportunities in untapped markets and the potential for innovative applications of LNG transport will further solidify the market's upward trajectory, making it a critical component of global energy security and supply chains for the foreseeable future.

LNG Carrier Market Segmentation

-

1. Containment Type

- 1.1. Moss

- 1.2. Membrane

-

2. Propulsion Type

- 2.1. Steam Turbines

- 2.2. Dual Fue

- 2.3. Slow-Speed Diesel (SSD)

- 2.4. M-type E

- 2.5. XDF Two-stroke Engine

- 2.6. Steam Re-heat and Stage

LNG Carrier Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of the North America

-

2. Asia Pacific

- 2.1. China

- 2.2. India

- 2.3. Japan

- 2.4. South Korea

- 2.5. Rest of the Asia Pacific

-

3. Europe

- 3.1. Germany

- 3.2. France

- 3.3. Spain

- 3.4. United Kingdom

- 3.5. Rest of the Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of the South America

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Nigeria

- 5.3. Saudi Arabia

- 5.4. Rest of the Middle East and Africa

LNG Carrier Market Regional Market Share

Geographic Coverage of LNG Carrier Market

LNG Carrier Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Containment Type

- 5.1.1. Moss

- 5.1.2. Membrane

- 5.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 5.2.1. Steam Turbines

- 5.2.2. Dual Fue

- 5.2.3. Slow-Speed Diesel (SSD)

- 5.2.4. M-type E

- 5.2.5. XDF Two-stroke Engine

- 5.2.6. Steam Re-heat and Stage

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Asia Pacific

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Containment Type

- 6. Global LNG Carrier Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Containment Type

- 6.1.1. Moss

- 6.1.2. Membrane

- 6.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 6.2.1. Steam Turbines

- 6.2.2. Dual Fue

- 6.2.3. Slow-Speed Diesel (SSD)

- 6.2.4. M-type E

- 6.2.5. XDF Two-stroke Engine

- 6.2.6. Steam Re-heat and Stage

- 6.1. Market Analysis, Insights and Forecast - by Containment Type

- 7. North America LNG Carrier Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Containment Type

- 7.1.1. Moss

- 7.1.2. Membrane

- 7.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 7.2.1. Steam Turbines

- 7.2.2. Dual Fue

- 7.2.3. Slow-Speed Diesel (SSD)

- 7.2.4. M-type E

- 7.2.5. XDF Two-stroke Engine

- 7.2.6. Steam Re-heat and Stage

- 7.1. Market Analysis, Insights and Forecast - by Containment Type

- 8. Asia Pacific LNG Carrier Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Containment Type

- 8.1.1. Moss

- 8.1.2. Membrane

- 8.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 8.2.1. Steam Turbines

- 8.2.2. Dual Fue

- 8.2.3. Slow-Speed Diesel (SSD)

- 8.2.4. M-type E

- 8.2.5. XDF Two-stroke Engine

- 8.2.6. Steam Re-heat and Stage

- 8.1. Market Analysis, Insights and Forecast - by Containment Type

- 9. Europe LNG Carrier Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Containment Type

- 9.1.1. Moss

- 9.1.2. Membrane

- 9.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 9.2.1. Steam Turbines

- 9.2.2. Dual Fue

- 9.2.3. Slow-Speed Diesel (SSD)

- 9.2.4. M-type E

- 9.2.5. XDF Two-stroke Engine

- 9.2.6. Steam Re-heat and Stage

- 9.1. Market Analysis, Insights and Forecast - by Containment Type

- 10. South America LNG Carrier Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Containment Type

- 10.1.1. Moss

- 10.1.2. Membrane

- 10.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 10.2.1. Steam Turbines

- 10.2.2. Dual Fue

- 10.2.3. Slow-Speed Diesel (SSD)

- 10.2.4. M-type E

- 10.2.5. XDF Two-stroke Engine

- 10.2.6. Steam Re-heat and Stage

- 10.1. Market Analysis, Insights and Forecast - by Containment Type

- 11. Middle East and Africa LNG Carrier Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Containment Type

- 11.1.1. Moss

- 11.1.2. Membrane

- 11.2. Market Analysis, Insights and Forecast - by Propulsion Type

- 11.2.1. Steam Turbines

- 11.2.2. Dual Fue

- 11.2.3. Slow-Speed Diesel (SSD)

- 11.2.4. M-type E

- 11.2.5. XDF Two-stroke Engine

- 11.2.6. Steam Re-heat and Stage

- 11.1. Market Analysis, Insights and Forecast - by Containment Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ship Builders

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 4 MISC Berhad

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 8 Japan Marine United Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 9 GasLog Ltd

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 3 Mitsui OSK Lines Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 8 BW LPG

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Ship Operators

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 4 STX Offshore and Shipbuilding CO LTD

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 3 Daewoo Shipbuilding and Marine Engineering Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 6 Kawasaki Heavy Industries Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 1 Royal Dutch Shell PLC

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 2 Nippon Yusen Kabushiki Kaisha

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 6 Maran Gas Maritime Inc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 5 Seapeak

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 1 Samsung Heavy Industries Co Ltd

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 7 China Shipbuilding Trading Co Ltd

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 5 Mitsubishi Heavy Industries Ltd

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 7 Golar LNG

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 10 Kawasaki Kisen Kaisha Ltd *List Not Exhaustive

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 2 Hyundai Samho Heavy Industries Co Ltd

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 9 HJ Shipbuilding & Construction Company Ltd

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.1 Ship Builders

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global LNG Carrier Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America LNG Carrier Market Revenue (billion), by Containment Type 2025 & 2033

- Figure 3: North America LNG Carrier Market Revenue Share (%), by Containment Type 2025 & 2033

- Figure 4: North America LNG Carrier Market Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 5: North America LNG Carrier Market Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 6: North America LNG Carrier Market Revenue (billion), by Country 2025 & 2033

- Figure 7: North America LNG Carrier Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: Asia Pacific LNG Carrier Market Revenue (billion), by Containment Type 2025 & 2033

- Figure 9: Asia Pacific LNG Carrier Market Revenue Share (%), by Containment Type 2025 & 2033

- Figure 10: Asia Pacific LNG Carrier Market Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 11: Asia Pacific LNG Carrier Market Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 12: Asia Pacific LNG Carrier Market Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific LNG Carrier Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe LNG Carrier Market Revenue (billion), by Containment Type 2025 & 2033

- Figure 15: Europe LNG Carrier Market Revenue Share (%), by Containment Type 2025 & 2033

- Figure 16: Europe LNG Carrier Market Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 17: Europe LNG Carrier Market Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 18: Europe LNG Carrier Market Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe LNG Carrier Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: South America LNG Carrier Market Revenue (billion), by Containment Type 2025 & 2033

- Figure 21: South America LNG Carrier Market Revenue Share (%), by Containment Type 2025 & 2033

- Figure 22: South America LNG Carrier Market Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 23: South America LNG Carrier Market Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 24: South America LNG Carrier Market Revenue (billion), by Country 2025 & 2033

- Figure 25: South America LNG Carrier Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa LNG Carrier Market Revenue (billion), by Containment Type 2025 & 2033

- Figure 27: Middle East and Africa LNG Carrier Market Revenue Share (%), by Containment Type 2025 & 2033

- Figure 28: Middle East and Africa LNG Carrier Market Revenue (billion), by Propulsion Type 2025 & 2033

- Figure 29: Middle East and Africa LNG Carrier Market Revenue Share (%), by Propulsion Type 2025 & 2033

- Figure 30: Middle East and Africa LNG Carrier Market Revenue (billion), by Country 2025 & 2033

- Figure 31: Middle East and Africa LNG Carrier Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global LNG Carrier Market Revenue billion Forecast, by Containment Type 2020 & 2033

- Table 2: Global LNG Carrier Market Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 3: Global LNG Carrier Market Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global LNG Carrier Market Revenue billion Forecast, by Containment Type 2020 & 2033

- Table 5: Global LNG Carrier Market Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 6: Global LNG Carrier Market Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Rest of the North America LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global LNG Carrier Market Revenue billion Forecast, by Containment Type 2020 & 2033

- Table 11: Global LNG Carrier Market Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 12: Global LNG Carrier Market Revenue billion Forecast, by Country 2020 & 2033

- Table 13: China LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: India LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Japan LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: South Korea LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Rest of the Asia Pacific LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global LNG Carrier Market Revenue billion Forecast, by Containment Type 2020 & 2033

- Table 19: Global LNG Carrier Market Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 20: Global LNG Carrier Market Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Germany LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: France LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: United Kingdom LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of the Europe LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global LNG Carrier Market Revenue billion Forecast, by Containment Type 2020 & 2033

- Table 27: Global LNG Carrier Market Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 28: Global LNG Carrier Market Revenue billion Forecast, by Country 2020 & 2033

- Table 29: Brazil LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Argentina LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of the South America LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global LNG Carrier Market Revenue billion Forecast, by Containment Type 2020 & 2033

- Table 33: Global LNG Carrier Market Revenue billion Forecast, by Propulsion Type 2020 & 2033

- Table 34: Global LNG Carrier Market Revenue billion Forecast, by Country 2020 & 2033

- Table 35: United Arab Emirates LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Nigeria LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Saudi Arabia LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Rest of the Middle East and Africa LNG Carrier Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the LNG Carrier Market?

The projected CAGR is approximately 6.2%.

2. Which companies are prominent players in the LNG Carrier Market?

Key companies in the market include Ship Builders, 4 MISC Berhad, 8 Japan Marine United Corporation, 9 GasLog Ltd, 3 Mitsui OSK Lines Ltd, 8 BW LPG, Ship Operators, 4 STX Offshore and Shipbuilding CO LTD, 3 Daewoo Shipbuilding and Marine Engineering Co Ltd, 6 Kawasaki Heavy Industries Ltd, 1 Royal Dutch Shell PLC, 2 Nippon Yusen Kabushiki Kaisha, 6 Maran Gas Maritime Inc, 5 Seapeak, 1 Samsung Heavy Industries Co Ltd, 7 China Shipbuilding Trading Co Ltd, 5 Mitsubishi Heavy Industries Ltd, 7 Golar LNG, 10 Kawasaki Kisen Kaisha Ltd *List Not Exhaustive, 2 Hyundai Samho Heavy Industries Co Ltd, 9 HJ Shipbuilding & Construction Company Ltd.

3. What are the main segments of the LNG Carrier Market?

The market segments include Containment Type, Propulsion Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 135.1 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Natural Gas Demand4.; Rising Pipeline Network and Associated Infrastructure Development.

6. What are the notable trends driving market growth?

Membrane-Type Containment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Rising Shift toward Renewable Energy.

8. Can you provide examples of recent developments in the market?

December 2022: GAIL (India) Ltd agreed to time charter a new liquefied natural gas (LNG) carrier with Japan's Mitsui O. S. K. Lines Ltd (MOL) and acquired a stake in an existing LNG carrier. The new LNG carrier, built by South Korea's Daewoo Shipbuilding & Marine Engineering Co Ltd, will be the second MOL Group LNG ship to serve GAIL and will commence time chartering in 2023.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "LNG Carrier Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the LNG Carrier Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the LNG Carrier Market?

To stay informed about further developments, trends, and reports in the LNG Carrier Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence