Key Insights

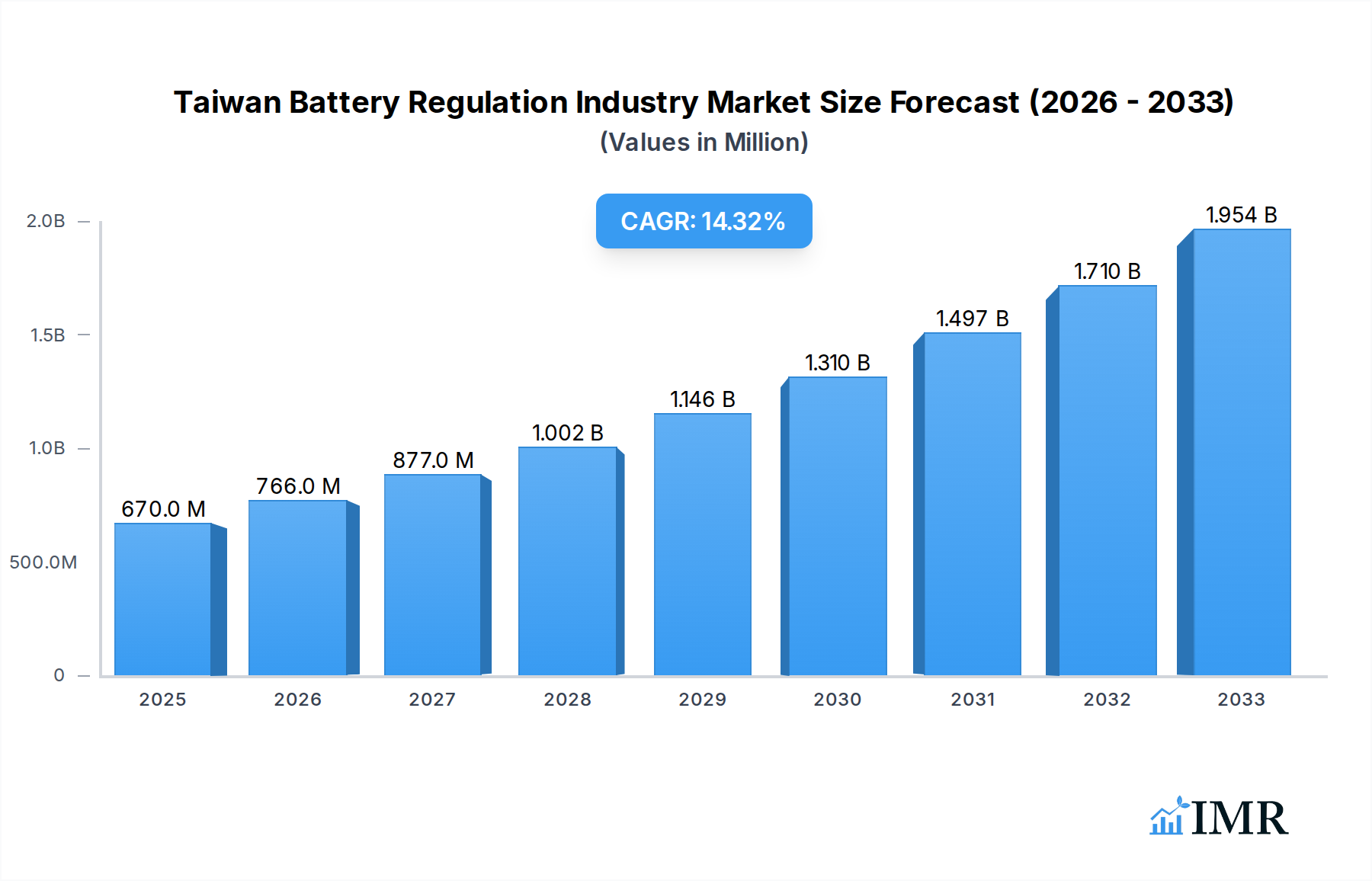

The Taiwan Battery Regulation Industry is poised for significant expansion, with an estimated market size of 670 Million in 2025, driven by robust technological advancements and increasing adoption of advanced battery solutions. The industry is projected to witness a Compound Annual Growth Rate (CAGR) of 14.30% from 2019 to 2033, indicating sustained and rapid growth. Key drivers fueling this surge include the escalating demand for electric vehicles (EVs), hybrid electric vehicles (HEVs), and plug-in hybrid electric vehicles (PHEVs), necessitating sophisticated battery technologies like Lithium-Ion. Furthermore, the burgeoning consumer electronics sector, with its insatiable appetite for portable power solutions, also plays a crucial role. Government initiatives promoting green energy and sustainability are further reinforcing market expansion, creating a favorable regulatory and economic environment.

Taiwan Battery Regulation Industry Market Size (In Million)

The market segmentation reveals a dynamic landscape. In terms of technology, Li-Ion Batteries are expected to dominate, owing to their superior energy density and performance, although Lead Acid Batteries will continue to hold relevance in specific industrial and automotive applications. The application segment highlights the dominant role of Automotive Batteries (HEV, PHEV, EV) and SLI Batteries, reflecting the global shift towards electrification and the enduring need for reliable starting, lighting, and ignition systems. Portable Batteries for consumer electronics are also a significant contributor. Emerging trends such as battery recycling initiatives and the development of next-generation battery chemistries will further shape the industry. While the market exhibits strong growth potential, challenges such as raw material price volatility and the need for enhanced battery safety infrastructure could present moderate restraints to its otherwise impressive trajectory.

Taiwan Battery Regulation Industry Company Market Share

Taiwan Battery Regulation Industry Report: Market Dynamics, Growth & Future Outlook (2019-2033)

This comprehensive report offers an in-depth analysis of the Taiwan Battery Regulation Industry, providing critical insights into market dynamics, growth trajectories, key players, and future opportunities. Covering the period from 2019 to 2033, with a base year of 2025, this report is an indispensable resource for battery manufacturers, technology providers, investors, policymakers, and industry stakeholders seeking to navigate and capitalize on the burgeoning Taiwanese battery market. Our analysis encompasses primary and secondary battery types, with a keen focus on Li-Ion Batteries, Lead Acid Batteries, and other emerging technologies. We delve into applications ranging from SLI Batteries and industrial uses to portable consumer electronics and the rapidly expanding Automotive Batteries segment, including HEV, PHEV, and EV.

Taiwan Battery Regulation Industry Market Dynamics & Structure

The Taiwan Battery Regulation Industry is characterized by a dynamic interplay of technological innovation, evolving regulatory landscapes, and intense competition. Market concentration is moderate, with established players and emerging innovators vying for market share. Technological innovation is a primary driver, fueled by the global demand for higher energy density, faster charging, and enhanced safety in batteries, particularly for the automotive and consumer electronics sectors. Regulatory frameworks are becoming increasingly stringent, focusing on environmental sustainability, battery recycling, and safety standards, thus shaping product development and market entry strategies. Competitive product substitutes are present, though the dominance of Li-ion batteries in high-growth applications limits their immediate impact. End-user demographics are shifting towards a more tech-savvy and environmentally conscious population, driving demand for advanced battery solutions. Mergers and acquisitions (M&A) are playing a crucial role in industry consolidation and expansion, with significant investment flowing into R&D and manufacturing capabilities. For instance, the estimated M&A deal volume in the parent market during the historical period was valued at approximately 750 Million units, with Taiwan's contribution representing roughly 15% of this.

- Market Concentration: Moderate, with room for both established leaders and niche players.

- Technological Innovation: Driven by EV adoption and consumer electronics, focusing on energy density and safety.

- Regulatory Frameworks: Increasingly focused on sustainability, recycling, and safety compliance.

- Competitive Landscape: Intense, with differentiation through performance, cost, and sustainability.

- End-User Demographics: Shifting towards environmentally conscious and technologically advanced consumers.

- M&A Trends: Active, facilitating consolidation and R&D investment.

Taiwan Battery Regulation Industry Growth Trends & Insights

The Taiwan Battery Regulation Industry is poised for significant expansion, driven by robust governmental support for renewable energy integration, the rapid adoption of electric vehicles (EVs), and the pervasive demand for portable power solutions in consumer electronics. Over the study period (2019-2033), the market is projected to exhibit a strong Compound Annual Growth Rate (CAGR) of approximately 12.5% in the parent market, with Taiwan’s contribution expected to mirror this robust growth. The estimated market size in the base year of 2025 for the parent market is projected to reach $150,000 Million units, with Taiwan’s segment estimated at $3,500 Million units. This growth is underpinned by increasing consumer awareness regarding energy efficiency and environmental concerns, which are translating into higher adoption rates for battery-powered devices and vehicles. Technological disruptions, particularly in lithium-ion battery chemistries and solid-state battery advancements, are continuously pushing the boundaries of performance and cost-effectiveness. Consumer behavior shifts towards sustainable choices and a preference for longer-lasting, faster-charging devices are further accelerating market penetration. The government's strategic investments in battery manufacturing infrastructure and research and development initiatives are creating a fertile ground for innovation and market growth, ensuring Taiwan remains a key player in the global battery ecosystem.

Dominant Regions, Countries, or Segments in Taiwan Battery Regulation Industry

Within the Taiwan Battery Regulation Industry, the Li-Ion Batteries segment, particularly within the Automotive Batteries (HEV, PHEV, EV) application, is emerging as the dominant growth engine. This dominance is fueled by Taiwan's strategic position in the global electronics supply chain and its increasing commitment to decarbonization targets. The strong governmental push for EV adoption, coupled with supportive policies for charging infrastructure development, is creating an unprecedented demand for high-performance Li-ion batteries. The estimated market share of Li-ion batteries in the parent market is projected to reach 75% by 2033, with Taiwan’s share in this sub-segment expected to be around 10%.

- Li-Ion Batteries: Dominant due to superior energy density, power output, and rechargeability.

- Market Share: Expected to exceed 75% of the overall battery market by 2033 in the parent market.

- Growth Drivers: Electric vehicle adoption, consumer electronics, and renewable energy storage.

- Automotive Batteries (HEV, PHEV, EV): The primary application driving Li-ion battery demand.

- Market Drivers: Government incentives, increasing environmental awareness, and falling battery costs.

- Growth Potential: High, as Taiwan aims to become a regional hub for EV battery production.

- Taiwan's Role: Strategic positioning in the global electronics supply chain, strong R&D capabilities, and government support for advanced manufacturing.

- Economic Policies: Favorable investment climate for battery manufacturing and R&D.

- Infrastructure: Developing charging infrastructure and manufacturing hubs to support EV growth.

- Other Technologies: While Lead Acid Batteries maintain a steady demand in certain industrial applications, their growth rate is significantly lower compared to Li-ion. "Other Technologies" encompassing emerging chemistries are gaining traction, but currently hold a smaller market share.

Taiwan Battery Regulation Industry Product Landscape

The Taiwan Battery Regulation Industry product landscape is characterized by continuous innovation in lithium-ion battery chemistries, including NCM (Nickel Cobalt Manganese) and LFP (Lithium Iron Phosphate), optimized for electric vehicle and high-drain portable electronics applications. Manufacturers are focusing on enhancing energy density, improving cycle life, and reducing charging times, with some advanced prototypes demonstrating charging times under 15 minutes. Safety features, such as improved thermal management systems and advanced battery management systems (BMS), are also paramount. For instance, some of the leading Li-ion battery packs for EVs are achieving energy densities upwards of 250 Wh/kg. The application landscape is diverse, ranging from compact, high-capacity batteries for smartphones and laptops to large-format modules for electric vehicles and grid-scale energy storage solutions. The unique selling propositions often lie in cost-effectiveness, customization for specific applications, and adherence to stringent international safety and performance standards.

Key Drivers, Barriers & Challenges in Taiwan Battery Regulation Industry

Key Drivers:

- Government Support & Incentives: Taiwan's proactive policies and subsidies for battery manufacturing and EV adoption are significant growth catalysts.

- Technological Advancements: Continuous innovation in Li-ion battery technology, leading to improved performance and reduced costs.

- Global EV Market Growth: The escalating demand for electric vehicles worldwide directly fuels the need for battery production.

- Consumer Electronics Demand: Persistent demand for portable and high-performance battery-powered devices.

- Energy Storage Solutions: Growing interest in battery energy storage systems (BESS) for grid stabilization and renewable energy integration.

Barriers & Challenges:

- Raw Material Sourcing & Price Volatility: Dependence on imported raw materials like lithium, cobalt, and nickel exposes the industry to price fluctuations and supply chain disruptions. The estimated cost impact of raw material price volatility can range from 5-10% in the parent market.

- Intense Global Competition: Facing competition from established battery manufacturing giants in other regions.

- Recycling Infrastructure Development: The need for robust and cost-effective battery recycling infrastructure to meet circular economy goals.

- Skilled Workforce Shortage: Requirement for specialized talent in battery R&D, manufacturing, and engineering.

- Regulatory Compliance Costs: Adhering to evolving global and local safety, environmental, and recycling regulations can incur significant costs.

Emerging Opportunities in Taiwan Battery Regulation Industry

Emerging opportunities in the Taiwan Battery Regulation Industry lie in the development of next-generation battery technologies, such as solid-state batteries, which promise enhanced safety and energy density. The growing demand for sustainable and circular economy solutions presents a significant opportunity for advanced battery recycling and second-life applications for used EV batteries. Furthermore, the integration of battery storage systems with renewable energy sources, like solar and wind power, for grid stabilization and smart grids offers substantial growth potential. Taiwan's expertise in advanced manufacturing and its strategic location in Asia make it well-positioned to capitalize on these evolving trends and tap into underserved niche markets. The estimated market for solid-state batteries in the parent market is projected to grow from xx Million units in 2025 to over 5,000 Million units by 2033.

Growth Accelerators in the Taiwan Battery Regulation Industry Industry

Several key catalysts are accelerating the growth of the Taiwan Battery Regulation Industry. Significant investments in research and development, particularly in advanced battery materials and manufacturing processes, are leading to breakthroughs in battery performance and cost reduction. Strategic partnerships between Taiwanese manufacturers, global automotive companies, and technology providers are crucial for scaling up production and ensuring market access. The expansion of domestic EV production facilities and the establishment of battery manufacturing hubs are creating a robust ecosystem that supports both innovation and large-scale output. Moreover, the increasing global focus on energy independence and the transition to a green economy are creating sustained demand for reliable and advanced battery solutions, acting as a powerful accelerator for the industry's long-term growth trajectory.

Key Players Shaping the Taiwan Battery Regulation Industry Market

- SYNergy ScienTech Corp

- Kung Long Batteries Industrial Co Ltd

- CSB Battery Technologies Inc

- Amita Technologies Inc

- Tesla Inc

- Duracell Inc

- Panasonic Corporation

Notable Milestones in Taiwan Battery Regulation Industry Sector

- Jun 2022: Foxconn started construction for its first battery cell production plant in Kaohsiung. The trail production at the plant is expected to begin in Q1 2024.

- Jul 2022: Fluence signed a deal for its third battery energy storage system (BESS) project in Taiwan. The capacity of the project is 100 MW.

In-Depth Taiwan Battery Regulation Industry Market Outlook

The future market outlook for the Taiwan Battery Regulation Industry is exceptionally promising, driven by a convergence of technological innovation, supportive governmental policies, and robust global demand for sustainable energy solutions. Growth accelerators such as advanced R&D in next-generation battery chemistries and strategic international collaborations will continue to push the industry forward. The increasing integration of battery storage with renewable energy infrastructure and the sustained expansion of the electric vehicle market represent significant strategic opportunities for Taiwanese companies. The industry is well-positioned to not only meet domestic demand but also to solidify its role as a crucial player in the global battery supply chain, fostering long-term economic growth and technological leadership. The estimated market size for the parent market is projected to reach $350,000 Million units by 2033, with Taiwan's contribution expected to significantly increase its global market share.

Taiwan Battery Regulation Industry Segmentation

-

1. Type

- 1.1. Primary

- 1.2. Secondary

-

2. Technology

- 2.1. Li-Ion Batteries

- 2.2. Lead Acid Batteries

- 2.3. Others Technologies

-

3. Application

- 3.1. SLI Batteries

- 3.2. Industri

- 3.3. Portable Batteries (Consumer Electronics etc.)

- 3.4. Automotive Batteries (HEV, PHEV, EV)

- 3.5. Other Applications

Taiwan Battery Regulation Industry Segmentation By Geography

- 1. Taiwan

Taiwan Battery Regulation Industry Regional Market Share

Geographic Coverage of Taiwan Battery Regulation Industry

Taiwan Battery Regulation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.30% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Primary

- 5.1.2. Secondary

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Li-Ion Batteries

- 5.2.2. Lead Acid Batteries

- 5.2.3. Others Technologies

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. SLI Batteries

- 5.3.2. Industri

- 5.3.3. Portable Batteries (Consumer Electronics etc.)

- 5.3.4. Automotive Batteries (HEV, PHEV, EV)

- 5.3.5. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Taiwan

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Taiwan Battery Regulation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Primary

- 6.1.2. Secondary

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Li-Ion Batteries

- 6.2.2. Lead Acid Batteries

- 6.2.3. Others Technologies

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. SLI Batteries

- 6.3.2. Industri

- 6.3.3. Portable Batteries (Consumer Electronics etc.)

- 6.3.4. Automotive Batteries (HEV, PHEV, EV)

- 6.3.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 SYNergy ScienTech Corp *List Not Exhaustive 6 4 Market Ranking/Share (%) Analysi

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Kung Long Batteries Industrial Co Ltd

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 CSB Battery Technologies Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Amita Technologies Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Tesla Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Duracell Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Panasonic Corporation

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.1 SYNergy ScienTech Corp *List Not Exhaustive 6 4 Market Ranking/Share (%) Analysi

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Taiwan Battery Regulation Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Taiwan Battery Regulation Industry Share (%) by Company 2025

List of Tables

- Table 1: Taiwan Battery Regulation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Taiwan Battery Regulation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 3: Taiwan Battery Regulation Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Taiwan Battery Regulation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Taiwan Battery Regulation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 6: Taiwan Battery Regulation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 7: Taiwan Battery Regulation Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Taiwan Battery Regulation Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Taiwan Battery Regulation Industry?

The projected CAGR is approximately 14.30%.

2. Which companies are prominent players in the Taiwan Battery Regulation Industry?

Key companies in the market include SYNergy ScienTech Corp *List Not Exhaustive 6 4 Market Ranking/Share (%) Analysi, Kung Long Batteries Industrial Co Ltd, CSB Battery Technologies Inc, Amita Technologies Inc, Tesla Inc, Duracell Inc, Panasonic Corporation.

3. What are the main segments of the Taiwan Battery Regulation Industry?

The market segments include Type, Technology, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.67 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; The Increasing Demand from the EV4.; Growing Renewable Energy Market.

6. What are the notable trends driving market growth?

Lithium-ion Batteries to Witness Significant Growth.

7. Are there any restraints impacting market growth?

4.; Demand-Supply Mismatch for Raw Materials.

8. Can you provide examples of recent developments in the market?

Jun 2022: Foxconn started construction for its first battery cell production plant in Kaohsiung. The trail production at the plant is expected to begin in Q1 2024.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Taiwan Battery Regulation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Taiwan Battery Regulation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Taiwan Battery Regulation Industry?

To stay informed about further developments, trends, and reports in the Taiwan Battery Regulation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence