Key Insights

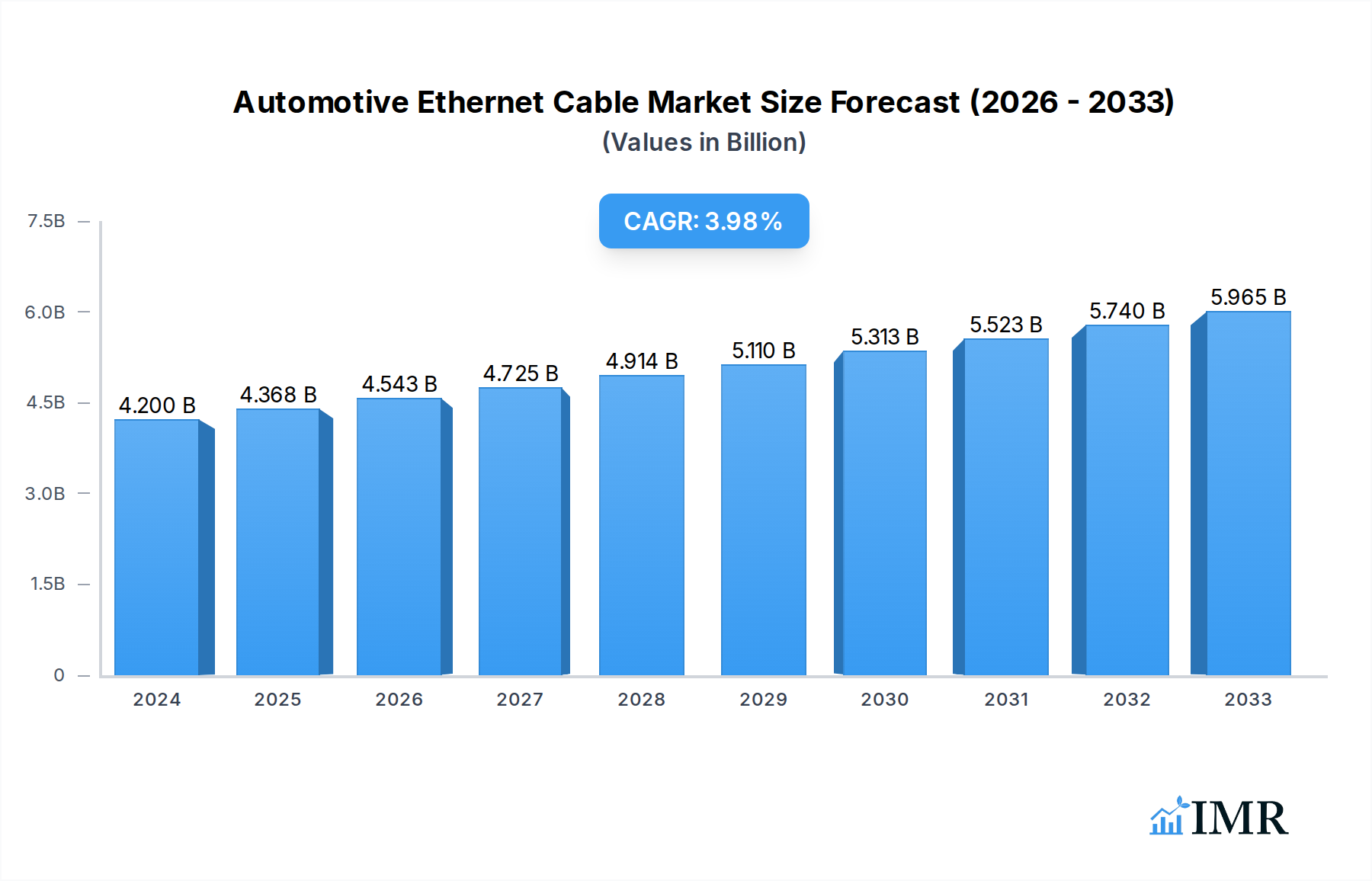

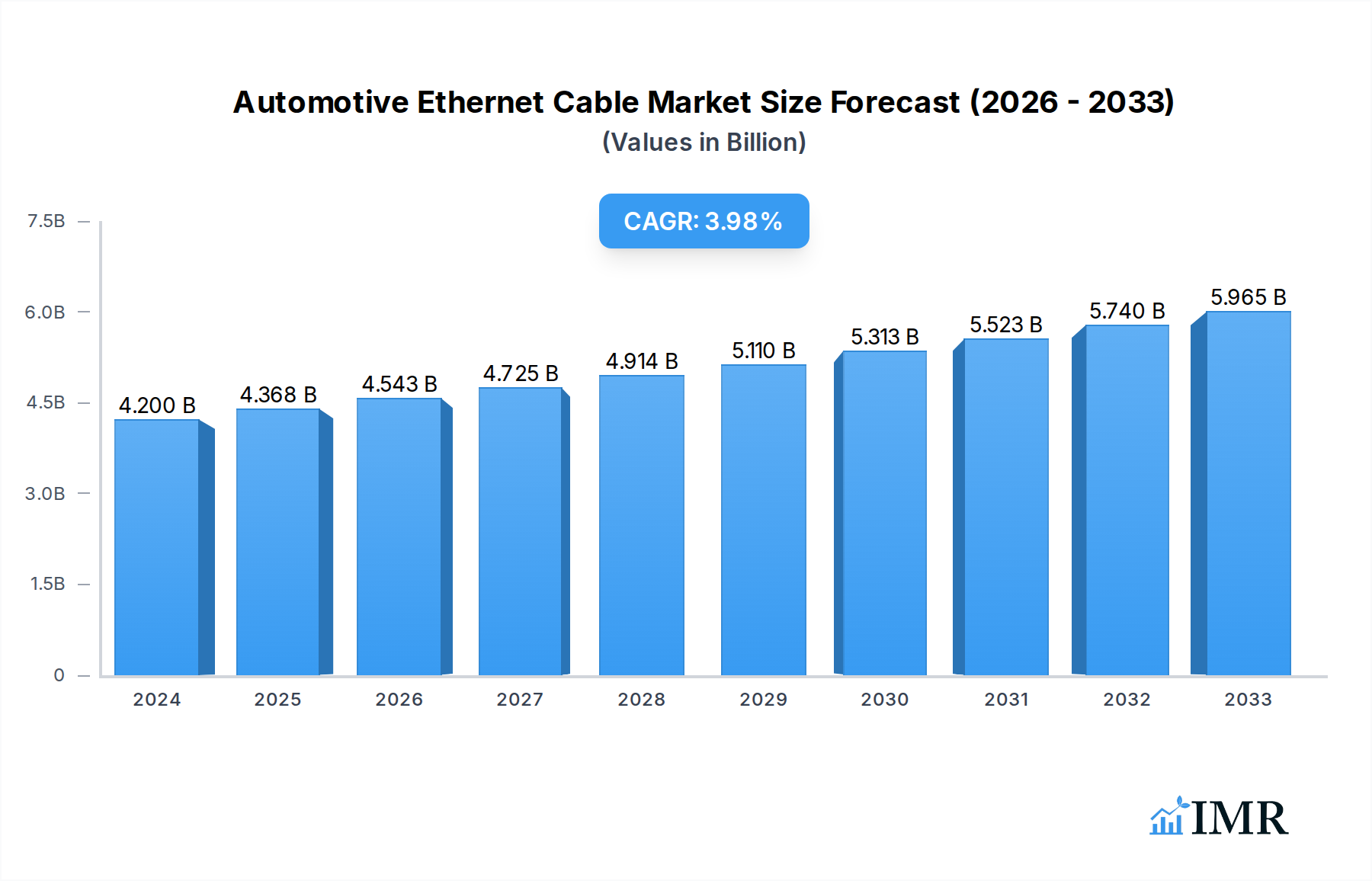

The global Automotive Ethernet Cable market is poised for robust expansion, projected to reach USD 4.2 billion in 2024 with a steady Compound Annual Growth Rate (CAGR) of 4% over the forecast period from 2025 to 2033. This growth is primarily fueled by the escalating demand for advanced in-vehicle connectivity solutions, driven by the increasing adoption of sophisticated features such as advanced driver-assistance systems (ADAS), autonomous driving technologies, and in-car infotainment systems. The transition from traditional CAN bus architectures to higher bandwidth Ethernet is a critical enabler, offering superior data transmission capabilities necessary for the complex sensor networks and real-time processing required by these evolving automotive applications. Emerging markets are also contributing significantly as automotive production continues to surge, creating a substantial demand for reliable and high-performance Ethernet cabling.

Automotive Ethernet Cable Market Size (In Billion)

The market landscape is characterized by several key trends that will shape its trajectory. The increasing complexity of vehicle electronics necessitates cables capable of handling higher data rates and offering enhanced electromagnetic interference (EMI) shielding, thus driving demand for shielded Ethernet cables. Furthermore, the growing focus on vehicle safety and cybersecurity is pushing manufacturers to adopt more robust and secure connectivity solutions. While the market presents significant opportunities, certain challenges persist. The stringent regulatory environment and the need for extensive testing and validation of automotive-grade components can introduce complexities and longer development cycles. Additionally, the price sensitivity in the automotive sector, coupled with the need for continuous innovation to meet evolving technological demands, presents a competitive challenge for cable manufacturers. Strategic collaborations and investments in research and development are crucial for companies to maintain a competitive edge and capitalize on the burgeoning opportunities within this dynamic market.

Automotive Ethernet Cable Company Market Share

Report Overview: This in-depth report provides a definitive analysis of the global Automotive Ethernet Cable market, exploring its intricate dynamics, growth trajectories, and future potential from 2019 to 2033. Delving into parent and child markets, this study equips industry stakeholders with actionable insights into market concentration, technological advancements, regulatory landscapes, competitive strategies, and burgeoning opportunities. The report leverages extensive historical data, current market conditions, and precise forecasts, with a base year of 2025 and a forecast period extending to 2033.

Automotive Ethernet Cable Market Dynamics & Structure

The Automotive Ethernet Cable market is characterized by a moderately concentrated structure, with a few key players holding significant market share. Technological innovation is the primary driver, fueled by the escalating demand for advanced in-car connectivity, high-speed data transmission for autonomous driving systems, and sophisticated infotainment features. Regulatory frameworks, particularly those related to vehicle safety standards and data security, are increasingly shaping product development and market entry strategies. Competitive product substitutes, such as traditional CAN buses and LIN buses, are gradually being displaced by the superior bandwidth and latency offered by automotive Ethernet. End-user demographics, predominantly automotive OEMs and Tier-1 suppliers, are keenly focused on integrating reliable and scalable networking solutions. Mergers and Acquisitions (M&A) trends are observed as companies seek to consolidate their market position, acquire cutting-edge technologies, and expand their product portfolios. For instance, recent M&A activities in the automotive connectivity sector have seen a combined deal volume of approximately $1.5 billion, reflecting the strategic importance of this segment. Innovation barriers include the rigorous validation processes for automotive-grade components and the need for robust electromagnetic compatibility (EMC) performance.

- Market Concentration: Moderately concentrated, with key players investing heavily in R&D and strategic partnerships.

- Technological Innovation Drivers: Increasing complexity of automotive electronics, demand for higher data rates, and the evolution of ADAS and autonomous driving.

- Regulatory Frameworks: Growing emphasis on functional safety (ISO 26262) and cybersecurity standards for automotive networks.

- Competitive Product Substitutes: Gradual phasing out of older bus systems in favor of Ethernet for bandwidth-intensive applications.

- End-User Demographics: Dominated by automotive OEMs and Tier-1 suppliers seeking advanced connectivity solutions.

- M&A Trends: Ongoing consolidation and strategic acquisitions to gain technological edge and market share.

- Innovation Barriers: Stringent automotive qualification processes and the need for high-performance, reliable solutions.

Automotive Ethernet Cable Growth Trends & Insights

The global Automotive Ethernet Cable market is poised for substantial growth, driven by the transformative shift towards connected and autonomous vehicles. The market size is projected to expand from approximately $3.2 billion in 2025 to an estimated $7.8 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of around 11.5%. Adoption rates for automotive Ethernet are rapidly increasing as OEMs recognize its critical role in enabling next-generation automotive architectures. The widespread integration of advanced driver-assistance systems (ADAS), high-resolution cameras, lidar, radar, and other sensor devices necessitates high-bandwidth, low-latency communication, which automotive Ethernet cables provide. Consumer behavior shifts are also playing a crucial role, with drivers and passengers demanding seamless in-car connectivity, advanced infotainment systems, and over-the-air (OTA) updates – all powered by robust networking. Technological disruptions, such as the development of multi-gigabit Ethernet standards and Power over Ethernet (PoE) for automotive applications, are further accelerating market penetration. The market penetration of automotive Ethernet cables, which stood at roughly 35% in 2024, is expected to surpass 65% by 2033. This evolution is not merely about connectivity but about creating a sophisticated, software-defined vehicle ecosystem.

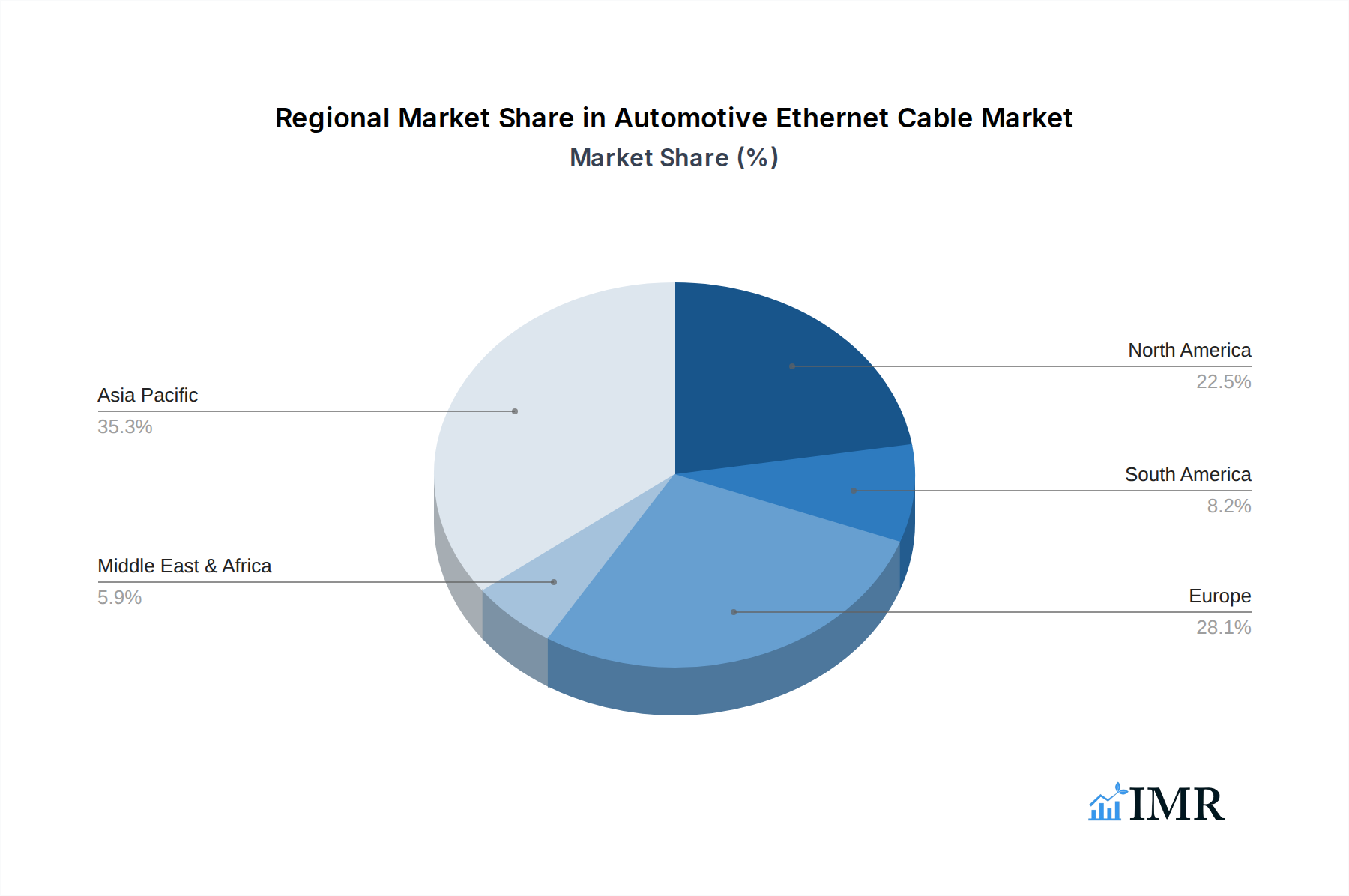

Dominant Regions, Countries, or Segments in Automotive Ethernet Cable

North America is emerging as a dominant region in the Automotive Ethernet Cable market, driven by its advanced automotive manufacturing base, significant investments in autonomous driving research and development, and strong consumer adoption of connected car technologies. Within North America, the United States, with its leading automotive OEMs and technology giants pushing the boundaries of self-driving capabilities, is a key country propelling market growth. The Application segment of Cameras is a primary growth driver, with an estimated market share of 25% in 2025. The increasing number of cameras for surround-view systems, rearview, driver monitoring, and advanced ADAS features directly translates into a higher demand for high-bandwidth Ethernet cables. Following closely is the Self-driving application, projected to capture approximately 20% of the market in 2025, as the development and deployment of autonomous vehicles rely heavily on extensive sensor data processing and inter-component communication. The Sensor Device application also holds significant sway, representing about 18% of the market. The evolution of lidar, radar, and ultrasonic sensors, all requiring high-speed data transfer, is critical. The GPS segment, while important for navigation and location-based services, currently accounts for a smaller but growing portion of around 12%. The Type segment of Shielded automotive Ethernet cables is dominant, holding approximately 60% of the market in 2025 due to the stringent requirement for noise immunity and electromagnetic compatibility in the automotive environment. Unshielded variants, while growing, represent the remaining 40%. Economic policies encouraging automotive innovation and substantial government funding for research in autonomous technologies further bolster North America's leadership. The robust infrastructure for research and development, coupled with a forward-thinking regulatory environment for advanced automotive technologies, ensures North America's continued dominance.

Automotive Ethernet Cable Product Landscape

The product landscape of Automotive Ethernet Cables is characterized by continuous innovation focused on enhancing data rates, miniaturization, and robustness. Key product developments include multi-gigabit Ethernet cables (e.g., 10BASE-T1L, 100BASE-T1, 1000BASE-T1, and multi-gigabit variants like 2.5GBASE-T1, 5GBASE-T1, and 10GBASE-T1) designed to meet the escalating bandwidth demands of advanced automotive applications. These cables are engineered for high-performance, offering superior signal integrity, minimal EMI/RFI interference, and exceptional durability in harsh automotive environments. Unique selling propositions include specialized shielding technologies, compact connector designs, and the integration of power delivery capabilities (PoE) to reduce cabling complexity. Technological advancements are also focused on improving flexibility, thermal management, and resistance to vibration and moisture, ensuring reliable operation throughout the vehicle's lifecycle.

Key Drivers, Barriers & Challenges in Automotive Ethernet Cable

Key Drivers:

- Growing adoption of ADAS and autonomous driving technologies: Requires high-speed data transfer for sensors and control systems.

- Increasing demand for in-car infotainment and connectivity: Drives the need for higher bandwidth for streaming and advanced features.

- Vehicle electrification: Offers opportunities for integrated power and data transmission solutions.

- Advancements in network architectures: Simplifies wiring harnesses and reduces vehicle weight.

Barriers & Challenges:

- Cost of implementation: Compared to traditional automotive networking solutions, Ethernet can be more expensive initially.

- Standardization and interoperability: Ensuring seamless communication between different vendors' components.

- Ruggedization and reliability: Meeting stringent automotive environmental and durability standards.

- Cybersecurity concerns: Protecting sensitive data transmitted over the network.

- Supply chain disruptions: Potential for material shortages and manufacturing delays impacting availability and pricing. The global automotive Ethernet cable market is expected to face supply chain disruptions impacting an estimated 15-20% of projected production capacity in the short term, leading to potential price increases of 5-10%.

Emerging Opportunities in Automotive Ethernet Cable

Emerging opportunities lie in the development of specialized Ethernet cables for niche applications such as high-resolution imaging for advanced driver monitoring systems and robust connectivity for next-generation LiDAR and radar sensors. The growing trend of software-defined vehicles opens avenues for enhanced diagnostic capabilities and remote updates over Ethernet networks. Untapped markets in emerging economies with rapidly expanding automotive sectors also present significant growth potential. Furthermore, the integration of AI and machine learning in vehicle systems will necessitate even more sophisticated and high-capacity data networking, creating demand for cutting-edge automotive Ethernet solutions. The expansion of in-vehicle networking to support 5G connectivity and V2X (Vehicle-to-Everything) communication is another significant emerging opportunity.

Growth Accelerators in the Automotive Ethernet Cable Industry

Technological breakthroughs in multi-gigabit Ethernet standards, such as 10GBASE-T1, are significant growth accelerators, enabling unprecedented data transfer speeds essential for complex autonomous driving systems. Strategic partnerships between cable manufacturers, semiconductor companies, and automotive OEMs are crucial for driving innovation and accelerating product adoption. Market expansion strategies, including targeting new vehicle platforms and segments like commercial vehicles, will also contribute to long-term growth. The increasing focus on vehicle cybersecurity and data management will further propel the demand for secure and reliable automotive Ethernet solutions.

Key Players Shaping the Automotive Ethernet Cable Market

- LEONI

- TE Connectivity

- Champlain Cable

- Molex

- Vector

- NI

- Bizlinktech

- FibreCode GmbH

- Rosenberger

Notable Milestones in Automotive Ethernet Cable Sector

- 2019: Standardization efforts for 100BASE-T1 and 1000BASE-T1 gain significant traction, paving the way for wider adoption.

- 2020: Major OEMs begin pilot programs and integrate automotive Ethernet into select premium vehicle models.

- 2021: Development of multi-gigabit Ethernet standards (2.5G, 5G, 10G) for automotive applications intensifies.

- 2022: Increased focus on cybersecurity and functional safety certifications for automotive Ethernet components.

- 2023: First commercial vehicle models featuring widespread adoption of automotive Ethernet for ADAS and infotainment systems are launched.

- 2024: Growing demand for miniaturized and high-performance connectors and cables to support complex vehicle architectures.

In-Depth Automotive Ethernet Cable Market Outlook

The automotive Ethernet cable market is set for sustained and robust growth, driven by the inexorable march towards autonomous driving, advanced connectivity, and sophisticated in-car experiences. The integration of multi-gigabit Ethernet and the ongoing development of specialized cabling solutions will be pivotal in meeting the ever-increasing data demands of future vehicles. Strategic collaborations and continuous innovation in product design and manufacturing processes will be key differentiators. The market's future is characterized by a strong outlook for technological advancements, expanded applications across diverse vehicle segments, and a growing demand for high-bandwidth, low-latency, and secure networking solutions, solidifying its position as a critical enabler of automotive evolution.

Automotive Ethernet Cable Segmentation

-

1. Application

- 1.1. Cameras

- 1.2. GPS

- 1.3. Self-driving

- 1.4. Sensor Device

- 1.5. Other

-

2. Type

- 2.1. Shielded

- 2.2. Unshielded

Automotive Ethernet Cable Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Ethernet Cable Regional Market Share

Geographic Coverage of Automotive Ethernet Cable

Automotive Ethernet Cable REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Ethernet Cable Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Cameras

- 5.1.2. GPS

- 5.1.3. Self-driving

- 5.1.4. Sensor Device

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Shielded

- 5.2.2. Unshielded

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Automotive Ethernet Cable Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Cameras

- 6.1.2. GPS

- 6.1.3. Self-driving

- 6.1.4. Sensor Device

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Shielded

- 6.2.2. Unshielded

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Automotive Ethernet Cable Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Cameras

- 7.1.2. GPS

- 7.1.3. Self-driving

- 7.1.4. Sensor Device

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Shielded

- 7.2.2. Unshielded

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Automotive Ethernet Cable Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Cameras

- 8.1.2. GPS

- 8.1.3. Self-driving

- 8.1.4. Sensor Device

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Shielded

- 8.2.2. Unshielded

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Automotive Ethernet Cable Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Cameras

- 9.1.2. GPS

- 9.1.3. Self-driving

- 9.1.4. Sensor Device

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Shielded

- 9.2.2. Unshielded

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Automotive Ethernet Cable Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Cameras

- 10.1.2. GPS

- 10.1.3. Self-driving

- 10.1.4. Sensor Device

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Shielded

- 10.2.2. Unshielded

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 LEONI

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 TE Connectivity

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Champlain Cable

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Molex

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Vector

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 NI

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Bizlinktech

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 FibreCode GmbH

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Rosenberger

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 LEONI

List of Figures

- Figure 1: Global Automotive Ethernet Cable Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Automotive Ethernet Cable Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Automotive Ethernet Cable Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Ethernet Cable Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Automotive Ethernet Cable Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Automotive Ethernet Cable Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Automotive Ethernet Cable Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Ethernet Cable Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Automotive Ethernet Cable Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Ethernet Cable Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Automotive Ethernet Cable Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Automotive Ethernet Cable Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Automotive Ethernet Cable Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Ethernet Cable Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Automotive Ethernet Cable Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Ethernet Cable Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Automotive Ethernet Cable Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Automotive Ethernet Cable Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Automotive Ethernet Cable Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Ethernet Cable Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Ethernet Cable Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Ethernet Cable Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Automotive Ethernet Cable Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Automotive Ethernet Cable Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Ethernet Cable Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Ethernet Cable Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Ethernet Cable Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Ethernet Cable Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Automotive Ethernet Cable Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Automotive Ethernet Cable Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Ethernet Cable Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Ethernet Cable Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Ethernet Cable Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Automotive Ethernet Cable Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Ethernet Cable Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Ethernet Cable Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Automotive Ethernet Cable Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Ethernet Cable Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Ethernet Cable Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Automotive Ethernet Cable Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Ethernet Cable Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Ethernet Cable Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Automotive Ethernet Cable Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Ethernet Cable Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Ethernet Cable Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Automotive Ethernet Cable Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Ethernet Cable Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Ethernet Cable Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Automotive Ethernet Cable Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Ethernet Cable Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Ethernet Cable?

The projected CAGR is approximately 4%.

2. Which companies are prominent players in the Automotive Ethernet Cable?

Key companies in the market include LEONI, TE Connectivity, Champlain Cable, Molex, Vector, NI, Bizlinktech, FibreCode GmbH, Rosenberger.

3. What are the main segments of the Automotive Ethernet Cable?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Ethernet Cable," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Ethernet Cable report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Ethernet Cable?

To stay informed about further developments, trends, and reports in the Automotive Ethernet Cable, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence