Key Insights

The Belgian Payments Industry is experiencing robust expansion, driven by accelerated digital transformation, the booming e-commerce sector, and a strong consumer preference for convenient, secure, and instant payment solutions. Valued at an estimated €78.34 billion in 2024, the market is projected to grow at a compelling Compound Annual Growth Rate (CAGR) of 8.5% through 2033. This growth is significantly bolstered by regulatory frameworks like PSD2, which foster open banking and encourage innovation, alongside increasing adoption of contactless payment technologies and mobile-first financial services. The widespread availability of high-speed internet and smartphone penetration further propels the shift from traditional cash transactions to sophisticated digital alternatives, making Belgium a dynamic landscape for payment innovation.

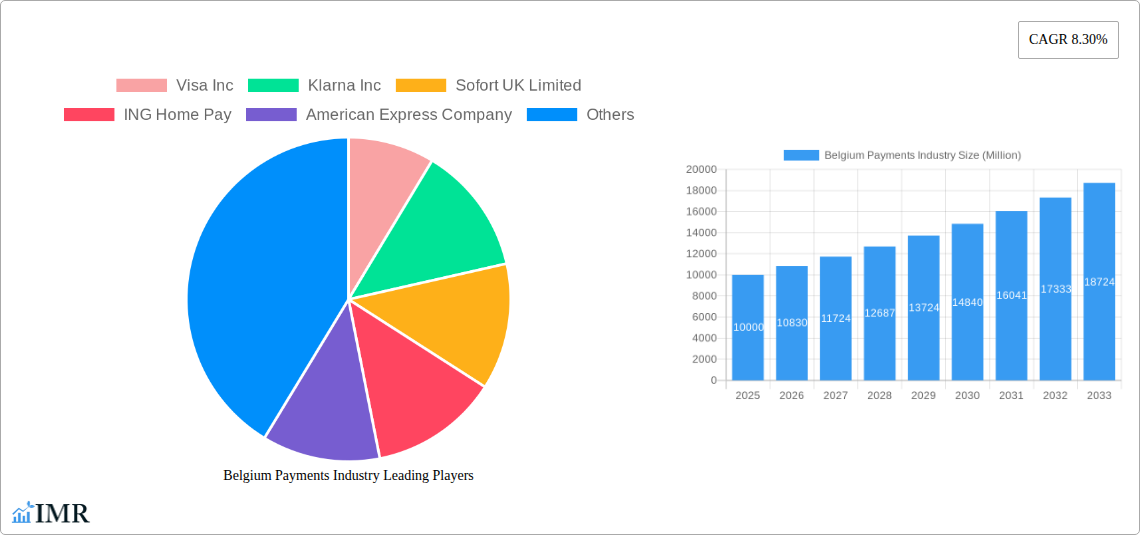

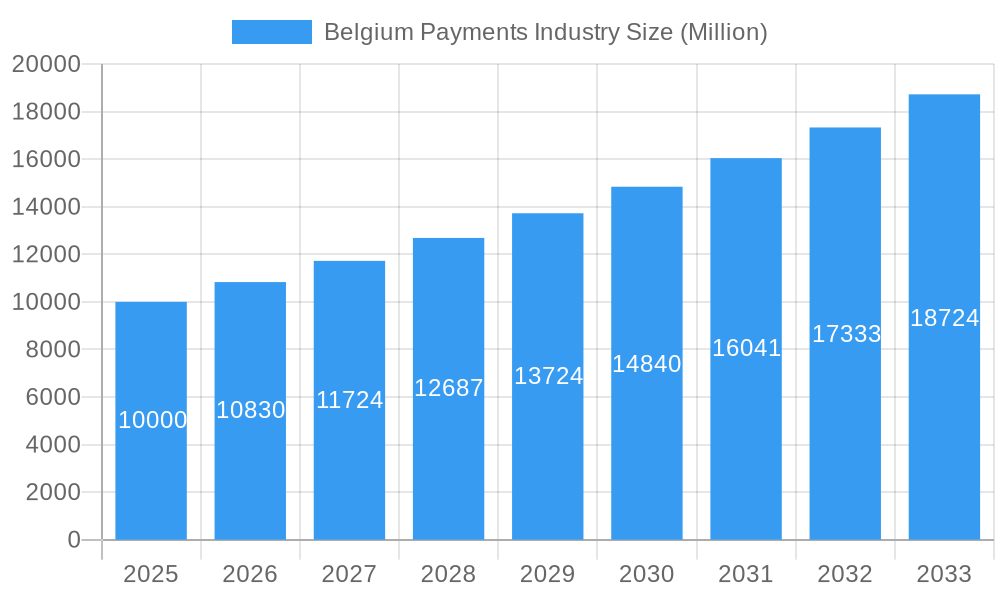

Belgium Payments Industry Market Size (In Billion)

Key trends shaping the Belgian payments ecosystem include the rising popularity of Buy Now Pay Later (BNPL) options, a significant surge in real-time bank transfers and Account-to-Account (A2A) payments, and the continuous evolution of mobile Point-of-Sale (POS) solutions. The market segments encompass diverse payment channels such as E-commerce Payments (including card-based, digital wallets, BNPL, and bank transfers) and Point-of-Sale (POS) Payments (covering traditional card payments, contactless, and mobile POS). Additionally, the industry is segmented by Payment Solution Types, focusing on e-commerce checkout and POS terminal solutions, and by End User, serving merchants, retailers, e-commerce platforms, and large enterprises. Major players like Visa Inc., Mastercard Inc., PayPal Payments, Klarna Inc., and American Express Company, alongside key local institutions such as Bancontact Payconiq Company, KBC Group N V, Belfius, ING Home Pay, and Sofort UK Limited, are actively competing to deliver innovative and seamless payment experiences, solidifying Belgium's position as a vibrant hub for digital financial services.

Belgium Payments Industry Company Market Share

Discover unparalleled insights into the dynamic Belgium Payments Industry with our comprehensive strategic report. Navigating a landscape shaped by rapid digitalization and evolving consumer preferences, this analysis provides an exhaustive deep dive into market dynamics, growth drivers, and emerging opportunities. From the overarching E-commerce Payments Belgium (parent market) to the booming Digital Wallets & BNPL Belgium (child market), our report offers a granular view of the forces propelling the Belgian financial ecosystem. Leveraging an extensive study period from 2019–2033, with 2025 as the base and estimated year, and a forecast extending to 2033, this definitive guide is indispensable for businesses, investors, and policymakers aiming to capitalize on the robust growth trajectory of digital payments Belgium.

Belgium Payments Industry Market Dynamics & Structure

The Belgium Payments Industry is characterized by a blend of established financial institutions and agile fintech innovators, fostering a vibrant competitive landscape. Market concentration remains moderate, with traditional banking giants like KBC Group N V and Belfius holding significant sway, while global players such as Visa Inc, Mastercard Inc, and American Express Company dominate the card network infrastructure. Simultaneously, specialized payment providers like Bancontact Payconiq Company have carved out a substantial market share, particularly in local POS and P2P transactions. Technological innovation drivers are primarily centered around enhancing user experience, security, and interoperability. This includes advancements in real-time payments, biometric authentication, and AI-driven fraud detection, which are reshaping payment processing Belgium. Regulatory frameworks, largely influenced by PSD2 and upcoming DORA regulations, are creating both opportunities for open banking and challenges related to compliance and data security. The competitive product substitutes range from traditional cash usage, still prevalent in certain segments, to innovative P2P solutions and sophisticated A2A payments Belgium. End-user demographics reveal a clear shift towards digital adoption across all age groups, propelled by convenience and the widespread availability of smartphones.

M&A trends indicate a strategic focus on expanding digital capabilities and market reach. For instance, smaller fintechs offering niche solutions are frequently acquired by larger banks or payment processors seeking to integrate innovative technologies. Annual M&A deal volumes in the sector have approached an estimated €2.3 billion in recent years, signaling an active pursuit of growth and consolidation. Innovation barriers, however, include the complexities of legacy infrastructure for incumbent banks and the high cost of compliance for new entrants. Despite these, the drive for efficiency and customer-centricity continues to fuel significant investment in next-generation payment solutions Belgium. The market share for card-based payments is dominated by Visa and Mastercard, collectively accounting for an estimated xx% of transaction volumes, while Bancontact Payconiq holds a leading position in domestic debit transactions with an estimated xx% share. PayPal Payments Private Limited maintains a strong foothold in cross-border and e-commerce payments Belgium, holding an estimated xx% market share in digital wallet transactions. This dynamic interplay ensures continuous evolution within the market structure.

Belgium Payments Industry Growth Trends & Insights

Leveraging robust market intelligence and extensive data analytics, the Belgium Payments Industry has witnessed remarkable growth, transforming from a largely cash-dependent economy into a burgeoning hub for digital payments Belgium. The overall market size evolved from an estimated €185 billion in 2019 to an impressive €265 billion in 2025. Projections indicate a sustained expansion, reaching approximately €510 billion by 2033, demonstrating a compelling Compound Annual Growth Rate (CAGR) of around 9.5% during the forecast period of 2025–2033. This impressive trajectory is underpinned by soaring adoption rates of digital payment methods across various sectors.

Technological disruptions, such as the widespread integration of contactless payments Belgium and the rapid rise of BNPL Belgium solutions, have fundamentally reshaped consumer behavior. The convenience and speed offered by these innovations have led to a significant decline in cash usage, particularly for smaller transactions. Furthermore, the COVID-19 pandemic acted as a powerful accelerant, pushing both consumers and merchants towards digital alternatives, cementing the shift towards an increasingly cashless society. Adoption of mobile payments and digital wallets has surged, with market penetration for these solutions exceeding xx% among active internet users. Consumers are increasingly valuing frictionless checkout experiences, security, and the ability to manage finances on the go, driving demand for advanced Fintech Belgium offerings. The proliferation of smartphones and enhanced internet connectivity have also played a crucial role in enabling this transformation. The shift is not only observed in consumer-facing transactions but also in business-to-business (B2B) payments, where real-time bank transfers and integrated invoicing solutions are gaining traction, improving efficiency and liquidity management for enterprises. This sustained momentum points towards a profoundly digital future for payments across Belgium.

Dominant Regions, Countries, or Segments in Belgium Payments Industry

Within the broader Belgium Payments Industry, the E-commerce Payments segment stands out as the primary driver of market growth, representing the dominant "parent market" with significant growth potential and sustained innovation. This segment encompasses a diverse range of transaction types, including Card-Based payments, Digital Wallets & BNPL, and Bank Transfers. Its dominance is largely attributable to the continued digital transformation of retail, accelerated by global trends and enhanced local infrastructure. Within E-commerce Payments, the Digital Wallets & BNPL sub-segment emerges as a key "child market," exhibiting exceptional growth and attracting substantial investment. This powerful combination is shaping the future of how Belgians transact online.

- Growing Online Retail Penetration: Belgium has seen a consistent increase in online shopping, with e-commerce accounting for an estimated xx% of total retail sales, pushing demand for seamless online payment solutions.

- Consumer Preference for Digital Convenience: Belgian consumers are increasingly opting for digital wallets (e.g., PayPal, Bancontact Payconiq, Apple Pay via ING) and Buy Now, Pay Later (BNPL) options (e.g., Klarna Inc) for their flexibility and ease of use. This trend directly fuels the growth of the child market.

- Infrastructure & Policy Support: Robust internet infrastructure and supportive EU-level regulations like PSD2 have facilitated the adoption of diverse online payment methods, encouraging innovation and competition among providers.

- Technological Advancements: Continuous innovation in secure online payment gateways, mobile app integration, and instant payment processing enhances the user experience and drives further adoption.

- Strategic Merchant Adoption: A vast number of merchants and retailers across Belgium, from small businesses to large enterprises, have integrated advanced e-commerce checkout solutions to cater to digital-first consumers.

The E-commerce Payments segment's market share is estimated to be around €110 billion in 2025, representing an approximate xx% of the total Belgium Payments Industry market value. The Digital Wallets & BNPL child market within this segment is projected to grow at an even faster CAGR of xx% during the forecast period, reflecting its increasing prominence. This segment's dominance is further solidified by the widespread availability of secure and user-friendly platforms, coupled with aggressive marketing by both established players and new entrants. As consumers increasingly expect personalized and flexible payment options, the E-commerce Payments, particularly Digital Wallets & BNPL, will continue to be a critical engine for innovation and expansion across the Belgian financial technology landscape.

Belgium Payments Industry Product Landscape

The Belgium Payments Industry is at the forefront of product innovation, driven by a commitment to seamless, secure, and user-friendly transactions. Key innovations include the proliferation of advanced POS terminal solutions that support not only traditional card payments but also contactless, mobile, and QR code-based methods. This integration enhances efficiency for merchants and convenience for consumers. In the e-commerce checkout solutions space, providers are focusing on one-click payments, integrated BNPL options, and localized payment methods like Bancontact, ensuring a frictionless online shopping experience. Performance metrics highlight increasing transaction speeds and enhanced fraud detection capabilities, reducing processing times to milliseconds and improving security significantly. Unique selling propositions revolve around instant payment confirmation, multi-currency support, and personalized financial insights for users. Technological advancements such as tokenization, biometric authentication, and AI-driven predictive analytics are setting new benchmarks for security and convenience in the Belgian market.

Key Drivers, Barriers & Challenges in Belgium Payments Industry

The Belgium Payments Industry is propelled by several robust drivers. Technological advancements are paramount, with the continuous evolution of mobile payment technologies, AI-driven fraud detection, and blockchain-based solutions enhancing transaction security and efficiency. The shift towards a cashless society, amplified by the pandemic, has significantly accelerated the adoption of digital payments Belgium. Economic policies promoting financial inclusion and digital transformation, alongside supportive regulatory frameworks like PSD2, foster innovation and competition among payment service providers. Furthermore, the growing demand for instant and seamless payment experiences across both consumer and business segments, particularly in e-commerce payments Belgium and real-time bank transfers, continues to fuel market expansion. Strategic partnerships between fintechs and traditional banks are also critical in bringing innovative solutions to a broader customer base.

Despite these drivers, the industry faces notable barriers and challenges. Regulatory hurdles, particularly compliance with evolving EU directives like DORA, can be complex and costly for businesses, impacting new product development and market entry. Competitive pressures from both global tech giants and agile local fintechs demand continuous innovation and significant investment in R&D, potentially squeezing margins for smaller players. Supply chain issues, although less direct, can affect hardware availability for POS terminal solutions and underlying IT infrastructure. Data privacy concerns remain a significant challenge, requiring robust cybersecurity measures and transparent data handling practices to maintain consumer trust. The fragmentation of payment methods, while offering choice, can also create complexity for merchants in managing multiple integrations and for consumers in understanding various options, hindering broader adoption in certain segments.

Emerging Opportunities in Belgium Payments Industry

The Belgium Payments Industry is ripe with emerging opportunities, particularly in untapped markets and innovative applications. The rapid growth of the gig economy and freelance sector presents a significant opportunity for tailored instant payment solutions and cross-border remittance services. The burgeoning demand for embedded finance, where payment functionalities are seamlessly integrated into non-financial platforms, offers new avenues for revenue generation and customer engagement. Furthermore, the increasing adoption of open banking initiatives creates a fertile ground for personalized financial products and services, leveraging secure data sharing. The focus on sustainability also opens opportunities for 'green' payment solutions, appealing to environmentally conscious consumers and businesses. The continued expansion of BNPL Belgium into new retail segments, beyond traditional e-commerce, represents another lucrative untapped market, catering to evolving consumer preferences for flexible credit options.

Growth Accelerators in the Belgium Payments Industry Industry

Several catalysts are driving long-term growth in the Belgium Payments Industry. Technological breakthroughs, such as advanced AI and machine learning in fraud detection and customer service, significantly enhance trust and efficiency, accelerating adoption. The ongoing proliferation of IoT devices and smart infrastructure will create new payment touchpoints, expanding the scope of contactless & mobile POS payments Belgium. Strategic partnerships between banks, fintechs, and e-commerce platforms are crucial in creating integrated ecosystems that offer comprehensive and seamless payment experiences. For instance, collaborations enabling instant A2A payments for businesses or embedded finance solutions are key. Market expansion strategies focusing on underserved SME segments and specialized B2B payment solutions, which simplify complex supply chain transactions, will unlock substantial latent demand. Furthermore, consumer demand for hyper-personalized financial services and loyalty programs integrated with payment solutions will continue to fuel innovation and market penetration.

Key Players Shaping the Belgium Payments Industry Market

- Visa Inc

- Klarna Inc

- Sofort UK Limited

- ING Home Pay

- American Express Company

- PayPal Payments Private Limited

- Bancontact Payconiq Company

- KBC Group N V

- Mastercard Inc

- Belfius

- Others

Notable Milestones in Belgium Payments Industry Sector

- August 2021: ING Belgium announced that it had added support for Apple Pay by bringing the contactless payment system to 1.4 million customers who use the ING Banking app with their cards. This development significantly boosted the adoption of mobile contactless payments in Belgium, increasing convenience for a large customer base and reinforcing the shift towards digital wallet usage over traditional physical cards. It also intensified competition in the mobile payments space among Belgian banks and payment providers.

In-Depth Belgium Payments Industry Market Outlook

The outlook for the Belgium Payments Industry remains exceptionally positive, fueled by a confluence of growth accelerators that promise sustained expansion and innovation. The continued drive towards digital payments Belgium, propelled by technological advancements in AI, blockchain, and mobile connectivity, will create new paradigms for how individuals and businesses transact. Strategic opportunities lie in the further integration of Fintech Belgium solutions with traditional banking services, fostering an ecosystem of open finance and embedded payment solutions. Untapped markets, particularly within the SME sector for optimized A2A payments Belgium and cross-border transactions, offer fertile ground for specialized service providers. As consumer preferences continue to evolve towards personalized, instant, and secure payment experiences, the industry is poised for transformative growth, ensuring Belgium remains at the forefront of European payment innovation and digital financial inclusion.

Belgium Payments Industry Segmentation

-

1. Payment Channel

-

1.1. E-commerce Payments

- 1.1.1. Card-Based

- 1.1.2. Digital Wallets & BNPL

- 1.1.3. Bank Transfer

-

1.2. Point-of-Sale (POS) Payments

- 1.2.1. Card Payments (Debit/Credit)

- 1.2.2. Contactless & Mobile POS Payments

-

1.3. Account-to-Account (A2A) Payments

- 1.3.1. Invoice Payments

- 1.3.2. Real-time Bank Transfers

-

1.1. E-commerce Payments

-

2. Payment Solution Type

- 2.1. E-commerce Checkout Solutions

- 2.2. POS Terminal Solutions

-

3. End User

- 3.1. Merchants & Retailers

- 3.2. E-commerce Platforms & Marketplaces

- 3.3. Enterprises & Corporates

- 3.4. Others

Belgium Payments Industry Segmentation By Geography

- 1. Belgium

Belgium Payments Industry Regional Market Share

Geographic Coverage of Belgium Payments Industry

Belgium Payments Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Payment Channel

- 5.1.1. E-commerce Payments

- 5.1.1.1. Card-Based

- 5.1.1.2. Digital Wallets & BNPL

- 5.1.1.3. Bank Transfer

- 5.1.2. Point-of-Sale (POS) Payments

- 5.1.2.1. Card Payments (Debit/Credit)

- 5.1.2.2. Contactless & Mobile POS Payments

- 5.1.3. Account-to-Account (A2A) Payments

- 5.1.3.1. Invoice Payments

- 5.1.3.2. Real-time Bank Transfers

- 5.1.1. E-commerce Payments

- 5.2. Market Analysis, Insights and Forecast - by Payment Solution Type

- 5.2.1. E-commerce Checkout Solutions

- 5.2.2. POS Terminal Solutions

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Merchants & Retailers

- 5.3.2. E-commerce Platforms & Marketplaces

- 5.3.3. Enterprises & Corporates

- 5.3.4. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Belgium

- 5.1. Market Analysis, Insights and Forecast - by Payment Channel

- 6. Belgium Payments Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Payment Channel

- 6.1.1. E-commerce Payments

- 6.1.1.1. Card-Based

- 6.1.1.2. Digital Wallets & BNPL

- 6.1.1.3. Bank Transfer

- 6.1.2. Point-of-Sale (POS) Payments

- 6.1.2.1. Card Payments (Debit/Credit)

- 6.1.2.2. Contactless & Mobile POS Payments

- 6.1.3. Account-to-Account (A2A) Payments

- 6.1.3.1. Invoice Payments

- 6.1.3.2. Real-time Bank Transfers

- 6.1.1. E-commerce Payments

- 6.2. Market Analysis, Insights and Forecast - by Payment Solution Type

- 6.2.1. E-commerce Checkout Solutions

- 6.2.2. POS Terminal Solutions

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Merchants & Retailers

- 6.3.2. E-commerce Platforms & Marketplaces

- 6.3.3. Enterprises & Corporates

- 6.3.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Payment Channel

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Visa Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Klarna Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Sofort UK Limited

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 ING Home Pay

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 American Express Company

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 PayPal Payments Private Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Bancontact Payconiq Company

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 KBC Group N V

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Mastercard Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Belfius

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Others

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Visa Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Belgium Payments Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Belgium Payments Industry Share (%) by Company 2025

List of Tables

- Table 1: Belgium Payments Industry Revenue billion Forecast, by Payment Channel 2020 & 2033

- Table 2: Belgium Payments Industry Revenue billion Forecast, by Payment Solution Type 2020 & 2033

- Table 3: Belgium Payments Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 4: Belgium Payments Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Belgium Payments Industry Revenue billion Forecast, by Payment Channel 2020 & 2033

- Table 6: Belgium Payments Industry Revenue billion Forecast, by Payment Solution Type 2020 & 2033

- Table 7: Belgium Payments Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 8: Belgium Payments Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Belgium Payments Industry?

The projected CAGR is approximately 8.5%.

2. Which companies are prominent players in the Belgium Payments Industry?

Key companies in the market include Visa Inc, Klarna Inc, Sofort UK Limited, ING Home Pay, American Express Company, PayPal Payments Private Limited, Bancontact Payconiq Company, KBC Group N V, Mastercard Inc, Belfius, Others.

3. What are the main segments of the Belgium Payments Industry?

The market segments include Payment Channel, Payment Solution Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 85 billion as of 2022.

5. What are some drivers contributing to market growth?

Increase in e-Commerce adoption is expected to drive the Payments Market in Belgium; Rise in contactless card payments.

6. What are the notable trends driving market growth?

Increase in E-commerce is Expected to Drive the Payments Market in Belgium.

7. Are there any restraints impacting market growth?

Lack of Skilled Personnel and Training Facilities.

8. Can you provide examples of recent developments in the market?

August 2021 - ING Belgium announced that it had added support for Apple Pay by bringing the contactless payment system to 1.4 million customers who use the ING Banking app with their cards.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Belgium Payments Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Belgium Payments Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Belgium Payments Industry?

To stay informed about further developments, trends, and reports in the Belgium Payments Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence