Key Insights

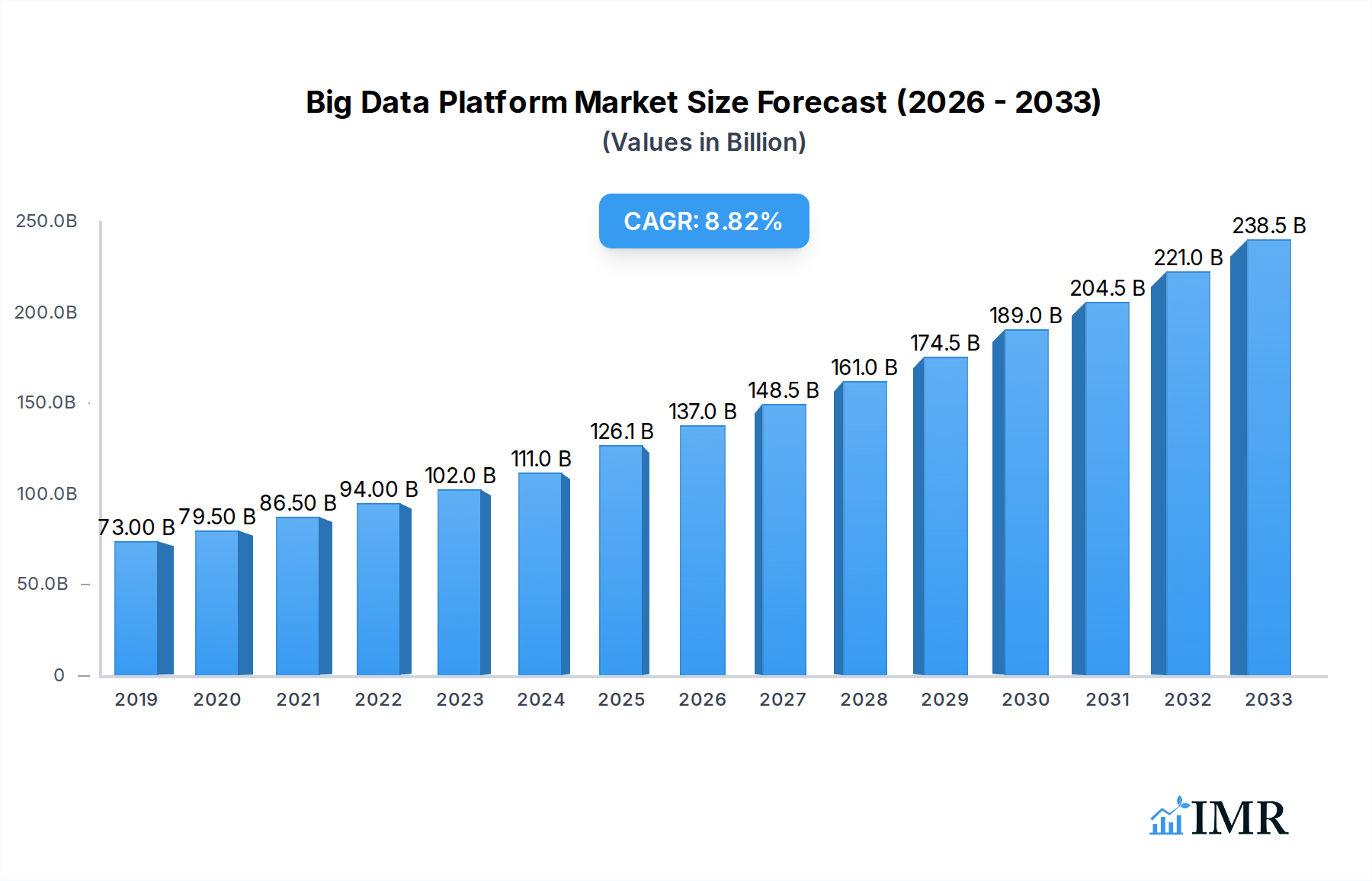

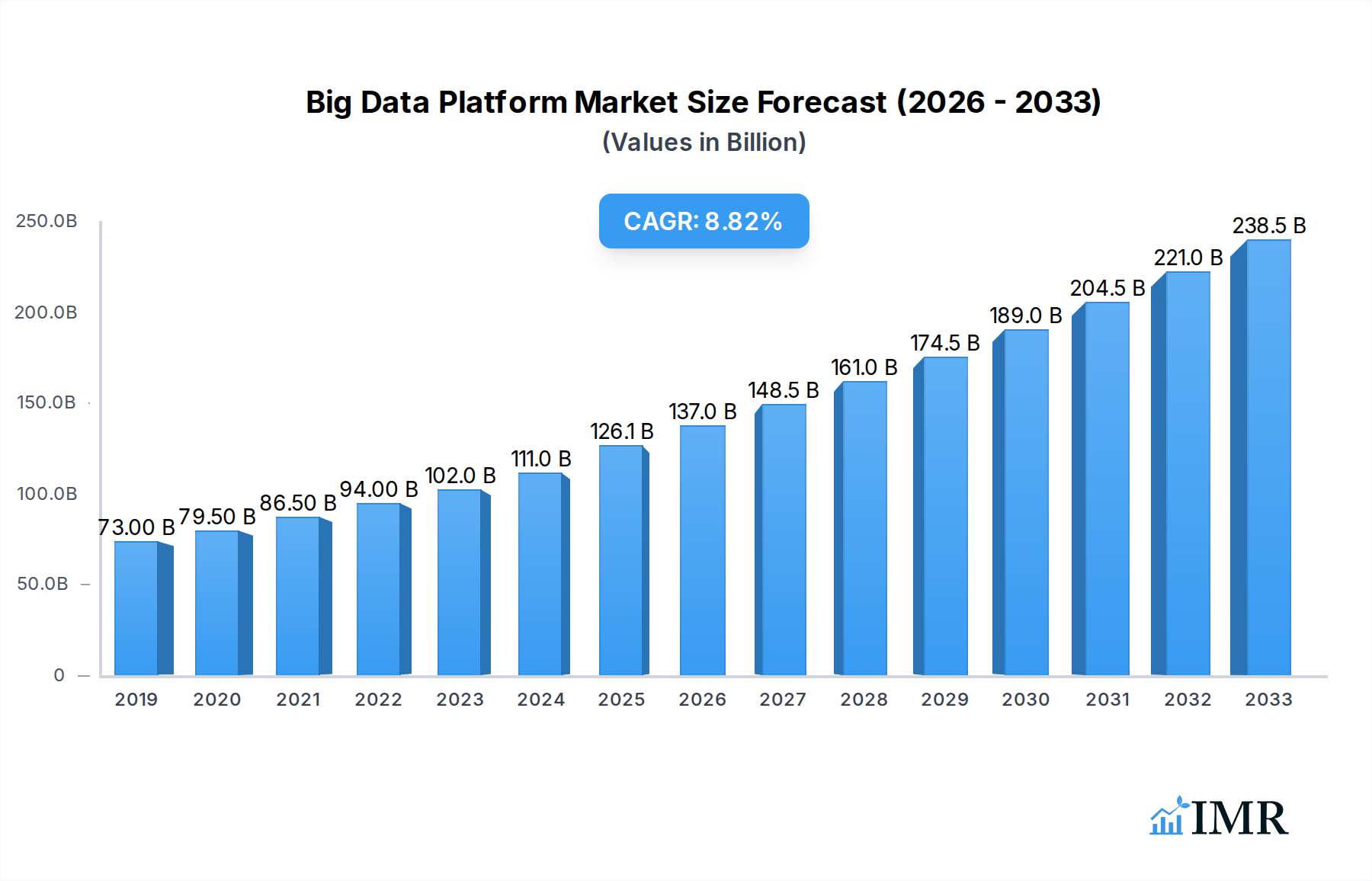

The Big Data Platform market is poised for significant expansion, projected to reach an impressive market size of $126,070 million by 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 9.5%. This growth trajectory, spanning from 2019 to 2033, underscores the escalating demand for sophisticated solutions to manage, process, and analyze the ever-increasing volume, velocity, and variety of data. Key growth drivers include the pervasive digital transformation across industries, the burgeoning adoption of cloud-based infrastructure, and the critical need for data-driven decision-making to gain competitive advantages. Organizations are increasingly leveraging big data platforms to unlock insights, optimize operations, enhance customer experiences, and develop innovative products and services. The inherent complexity of managing vast datasets, coupled with the evolving regulatory landscape concerning data privacy and security, also necessitates advanced platform capabilities, further fueling market adoption.

Big Data Platform Market Size (In Billion)

The market is segmented by application into crucial sectors such as Banking, Manufacturing, Professional Services, and Government, each with unique data challenges and opportunities. Cloud-based solutions are dominating the landscape due to their scalability, flexibility, and cost-effectiveness, though on-premise deployments continue to serve specific enterprise needs. Prominent players like Microsoft, Google, AWS, IBM, and SAP are at the forefront of innovation, offering comprehensive suites of tools and services. Emerging trends include the integration of AI and machine learning for advanced analytics, the rise of data fabric and data mesh architectures for decentralized data management, and a growing focus on real-time data processing and streaming analytics. While the market is characterized by intense competition and rapid technological advancements, potential restraints such as data governance complexities, a shortage of skilled data professionals, and the initial investment costs for robust platform implementation are areas that stakeholders are actively addressing to ensure sustained and inclusive growth.

Big Data Platform Company Market Share

Big Data Platform Market Dynamics & Structure

The global Big Data Platform market is characterized by a highly fragmented yet intensely competitive landscape, driven by continuous technological innovation and an increasing need for data-driven decision-making across all industries. Major players like Microsoft, Google, AWS, and IBM are at the forefront, leveraging extensive cloud infrastructure and robust AI capabilities to dominate the market. This concentration of power is balanced by a proliferation of specialized vendors, including Dell, Splunk, SAP, and Cloudera, who cater to specific niche requirements and application verticals.

Market Concentration & Innovation Drivers:

- The market exhibits a moderate to high concentration at the top tier, with the top 5-10 companies holding a significant collective market share, estimated at around 65% in 2025.

- Artificial Intelligence (AI) and Machine Learning (ML) are the primary innovation drivers, enabling advanced analytics, predictive modeling, and automation within big data platforms.

- The rise of data lakes, data warehouses, and data mesh architectures are transforming how organizations store, process, and access vast datasets.

- Scalability, real-time processing, and enhanced data governance are critical focal points for ongoing research and development.

Regulatory Frameworks & Competitive Substitutes:

- Increasingly stringent data privacy regulations (e.g., GDPR, CCPA) are shaping platform development, emphasizing security and compliance. This represents a significant barrier to entry for new players and a compliance challenge for existing ones.

- While dedicated big data platforms are primary solutions, traditional business intelligence (BI) tools and specialized analytics software serve as competitive substitutes for organizations with less complex data needs. The market share for these substitutes is estimated to be around 15% of the overall data analytics spend.

End-User Demographics & M&A Trends:

- End-user demographics are diverse, spanning small and medium-sized businesses (SMBs) to large enterprises, with a growing adoption in sectors like Banking, Manufacturing, Professional Services, and Government.

- Mergers and Acquisitions (M&A) are a prevalent strategy for consolidation and capability enhancement. The volume of M&A deals in the big data platform space is projected to reach approximately 45-55 significant transactions annually between 2025 and 2033, with deal values ranging from tens of millions to several billion units. Notable examples include acquisitions aimed at bolstering AI/ML capabilities or expanding cloud offerings.

Big Data Platform Growth Trends & Insights

The global Big Data Platform market is poised for extraordinary expansion, fueled by an insatiable appetite for data-driven insights and the relentless march of technological advancement. Projections indicate a Compound Annual Growth Rate (CAGR) of approximately 18.5% over the forecast period of 2025–2033, with the market size expected to surge from an estimated $XX billion in 2025 to over $XXX billion by 2033. This robust growth trajectory is underpinned by a confluence of factors, including the exponential increase in data generation, the democratization of advanced analytics tools, and the strategic imperative for organizations to harness Big Data for competitive advantage.

The adoption rate of Big Data Platforms is accelerating across all industry verticals. In the Banking sector, for instance, adoption rates are estimated to reach 85% by 2030, driven by the need for fraud detection, personalized customer experiences, and regulatory compliance. Similarly, Manufacturing is witnessing a significant uptake, with an estimated 70% adoption rate by 2030, leveraging Big Data for predictive maintenance, supply chain optimization, and quality control. The Professional Services sector is also heavily investing, with adoption projected to hit 78% by 2030, enabling enhanced client insights and operational efficiency. Even Government agencies are increasingly embracing Big Data for public service delivery, national security, and resource management, with adoption rates climbing to an estimated 60% by 2030.

Technological disruptions are continuously reshaping the Big Data Platform landscape. The maturation of cloud-native architectures has made scalable and cost-effective data processing more accessible than ever. The widespread integration of AI and ML algorithms is transforming raw data into actionable intelligence, powering everything from sophisticated recommender systems to advanced predictive analytics. Furthermore, the emergence of data fabrics and data meshes is addressing the complexities of distributed data environments, offering more agile and self-serve data management capabilities. These innovations are not merely incremental; they represent paradigm shifts in how data is consumed and leveraged.

Consumer behavior shifts are also playing a pivotal role. As individuals and businesses become more accustomed to personalized experiences and instant gratification, the demand for data-driven personalization and responsive services has intensified. Organizations are compelled to use Big Data platforms to understand these evolving preferences, leading to a greater focus on real-time analytics and customer journey mapping. The market penetration of Big Data Platforms is expected to move from roughly 40% of potential addressable market in 2025 to over 75% by 2033, indicating a broad and deep integration across the global economy. The accessibility of open-source technologies alongside commercial offerings is further democratizing access to these powerful tools, driving adoption in regions and organizations that might have previously been excluded due to cost or complexity.

Dominant Regions, Countries, or Segments in Big Data Platform

The global Big Data Platform market is experiencing robust growth, with several key regions, countries, and segments emerging as significant growth engines. Among the segments, Cloud-Based platforms are unequivocally dominating the market, projected to capture an estimated 70% of the total market share by 2025, and expected to grow at a CAGR of approximately 20% through 2033. This dominance is attributed to the inherent scalability, flexibility, cost-effectiveness, and ease of deployment offered by cloud solutions. Major cloud providers like AWS, Microsoft Azure, and Google Cloud are continuously investing in their big data offerings, providing a comprehensive suite of services that cater to a wide range of organizational needs, from data storage and processing to advanced analytics and AI/ML capabilities. The ability to scale resources up or down based on demand, coupled with a pay-as-you-go pricing model, makes cloud-based platforms particularly attractive to businesses of all sizes.

Within the application segments, the Banking sector stands out as a primary driver of Big Data Platform adoption and growth. By 2025, the Banking industry is estimated to represent around 25% of the total Big Data Platform market revenue, with a projected CAGR of 19%. Financial institutions are leveraging Big Data for critical functions such as fraud detection, risk management, customer analytics for personalized offerings, regulatory compliance (e.g., KYC, AML), and enhancing operational efficiency. The sheer volume and sensitivity of financial data, coupled with the stringent regulatory environment, necessitate sophisticated Big Data solutions to process, analyze, and secure this information effectively.

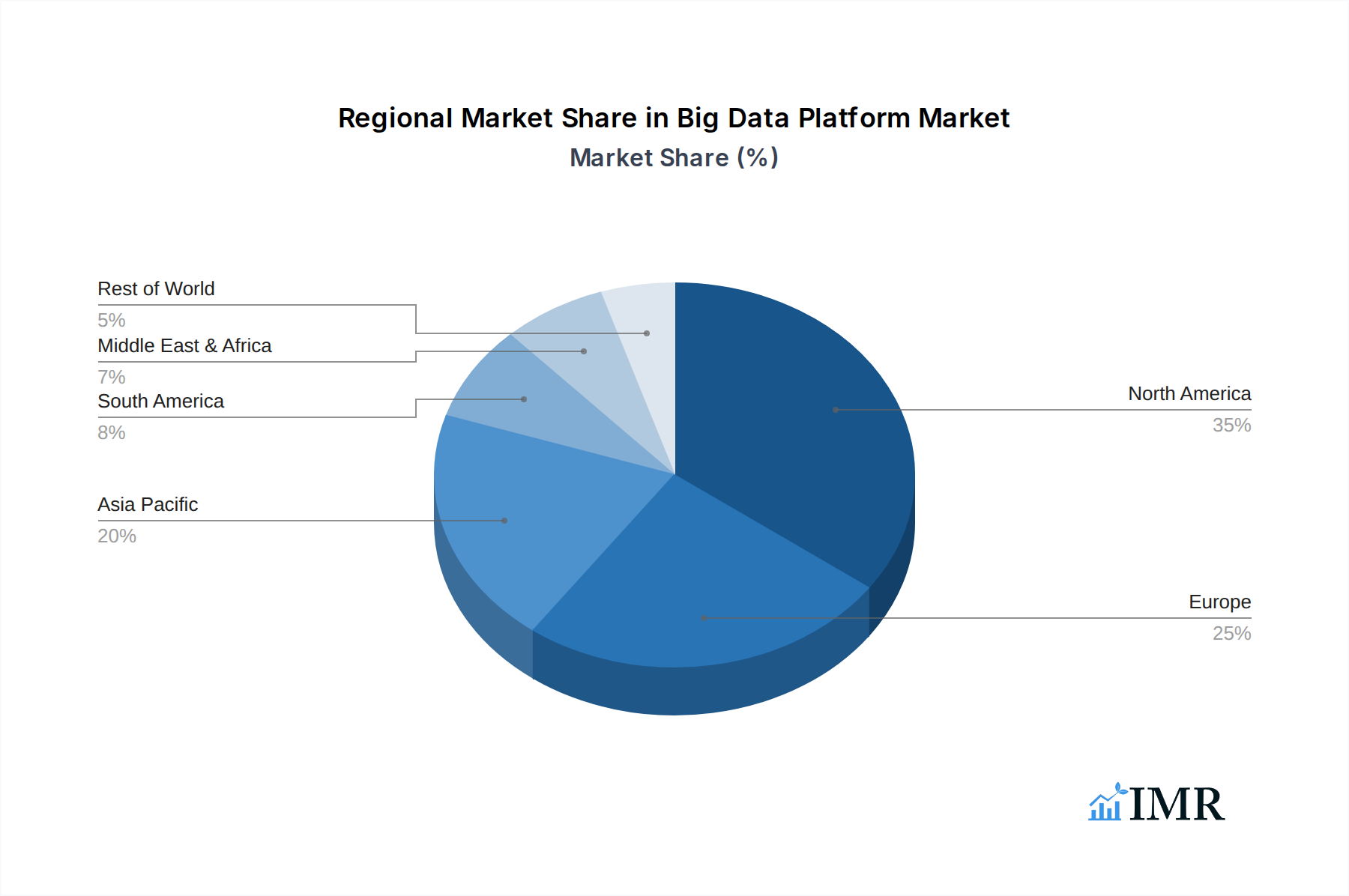

Geographically, North America continues to be the leading region, accounting for an estimated 35% of the global Big Data Platform market revenue in 2025, with a robust CAGR of 17.5%. This leadership is driven by a mature technology ecosystem, a high concentration of enterprises investing in digital transformation, and strong government support for innovation. The presence of major technology giants like Microsoft, Google, AWS, IBM, and Dell, along with a vibrant startup scene, fosters intense competition and rapid adoption of cutting-edge Big Data technologies. The United States, in particular, remains a powerhouse, with significant investments in Big Data across industries like technology, finance, healthcare, and e-commerce.

Asia Pacific is emerging as the fastest-growing region, with an estimated CAGR of 22% through 2033. This rapid expansion is fueled by the burgeoning digital economy in countries like China, India, and Southeast Asian nations. Increasing internet penetration, a growing middle class, and government initiatives promoting digitalization are spurring demand for Big Data solutions across various sectors, including e-commerce, telecommunications, and smart city development. Countries like China are rapidly advancing their domestic Big Data capabilities, with companies like Alibaba and Tencent making significant strides.

Key drivers for this regional and segmental dominance include:

- Economic Policies: Favorable government policies and incentives for technology adoption and data innovation in leading regions.

- Infrastructure Development: Extensive cloud infrastructure and high-speed internet connectivity supporting scalable Big Data solutions.

- Digital Transformation Initiatives: Widespread enterprise adoption of digital technologies and data-centric strategies.

- Talent Pool: Availability of skilled data scientists, engineers, and analysts to support Big Data platform implementation and utilization.

- Growing Data Volumes: The continuous exponential growth of data generated from diverse sources, necessitating advanced platforms for management and analysis.

Big Data Platform Product Landscape

The Big Data Platform product landscape is characterized by an evolving array of solutions designed to ingest, store, process, analyze, and visualize massive datasets. Vendors are continuously innovating to offer enhanced capabilities in areas such as real-time analytics, AI/ML integration, data governance, and hybrid cloud deployment. Key product developments include the advancement of data lakes and data warehouses into unified data platforms, offering greater flexibility and accessibility. Innovations in distributed computing frameworks like Apache Spark and Hadoop continue to enhance processing speeds and efficiency. Furthermore, platforms are increasingly integrating advanced AI and machine learning algorithms, enabling sophisticated predictive analytics, natural language processing, and automated decision-making. Security and data governance features are paramount, with robust solutions for data lineage, access control, and compliance being integral to modern Big Data Platforms.

Key Drivers, Barriers & Challenges in Big Data Platform

The Big Data Platform market is propelled by several key drivers, primarily centered around the transformative potential of data-driven insights. The increasing volume, velocity, and variety of data generated globally necessitate sophisticated platforms for effective management and analysis. AI and Machine Learning integration is a significant catalyst, enabling advanced predictive analytics, automation, and intelligent decision-making across industries. Digital transformation initiatives by businesses worldwide are a critical driver, pushing organizations to adopt Big Data solutions for competitive advantage, operational efficiency, and enhanced customer experiences. The growing need for real-time data processing to support dynamic business environments and the development of cloud-native, scalable solutions further fuel market expansion.

However, the market also faces significant barriers and challenges. Data security and privacy concerns remain a paramount challenge, with the increasing frequency of data breaches and evolving regulatory landscapes (e.g., GDPR, CCPA) requiring substantial investment in compliance and robust security measures. The shortage of skilled data professionals – data scientists, engineers, and analysts – poses a significant constraint on adoption and effective utilization of Big Data platforms, impacting the overall market growth potential. The complexity and cost of implementation and maintenance of large-scale Big Data infrastructures can be prohibitive for smaller organizations, acting as a barrier to entry. Furthermore, data integration challenges from disparate sources and the need for effective data governance policies create hurdles in unlocking the full value of Big Data.

Emerging Opportunities in Big Data Platform

Emerging opportunities in the Big Data Platform sector are abundant, driven by evolving technological capabilities and shifting market demands. The democratization of AI and ML through accessible platform features presents a significant opportunity for businesses to embed intelligent insights into their operations without requiring deep in-house expertise. The expansion of edge computing is creating new avenues for Big Data platforms to process data closer to its source, enabling real-time insights in remote or resource-constrained environments. Untapped markets in emerging economies represent substantial growth potential as these regions increasingly embrace digital transformation. Furthermore, the growing focus on data ethics and explainable AI (XAI) is opening up opportunities for platforms that prioritize transparency, fairness, and accountability in their analytical outputs. The development of specialized Big Data solutions for niche industries like personalized healthcare, sustainable agriculture, and smart manufacturing also presents compelling avenues for innovation and market penetration.

Growth Accelerators in the Big Data Platform Industry

The Big Data Platform industry's long-term growth is significantly accelerated by a combination of technological breakthroughs, strategic collaborations, and expanding market reach. The continuous evolution of cloud computing services provides a scalable and cost-effective foundation for Big Data platforms, enabling wider adoption and reducing infrastructure barriers. Advancements in AI and machine learning algorithms, particularly in areas like deep learning and natural language processing, are enhancing the analytical power and predictive capabilities of these platforms, driving deeper insights and more intelligent automation. Strategic partnerships between technology providers, consulting firms like Accenture, and hardware vendors are crucial for creating comprehensive end-to-end solutions and expanding market penetration. Furthermore, the development of open-source technologies and standardized data formats fosters interoperability and reduces vendor lock-in, accelerating innovation and adoption across the ecosystem.

Notable Milestones in Big Data Platform Sector

- 2019: Continued advancements in Apache Spark and Hadoop ecosystems, enhancing processing speeds and scalability.

- 2020: Increased focus on cloud-native Big Data solutions from major cloud providers like AWS, Azure, and Google Cloud.

- 2021: Significant growth in AI/ML integration within Big Data platforms, enabling more sophisticated analytics and automation.

- 2022: Heightened emphasis on data governance and compliance features due to evolving global regulations.

- 2023: Emergence and wider adoption of data mesh architectures for decentralized data management.

- 2024: Increased M&A activity as larger players acquire specialized Big Data analytics and AI startups.

- 2025 (Estimated): Maturation of hybrid and multi-cloud Big Data strategies, offering greater flexibility.

- 2026-2030 (Projected): Widespread adoption of edge analytics and AI-powered data discovery tools.

- 2031-2033 (Projected): Greater integration of Big Data platforms with IoT devices and blockchain for enhanced data integrity and real-time insights.

In-Depth Big Data Platform Market Outlook

The Big Data Platform market outlook is exceptionally positive, driven by sustained technological innovation and the imperative for data-driven decision-making across all industries. Growth accelerators such as advancements in AI/ML, the pervasive adoption of cloud computing, and the ongoing digital transformation of businesses will continue to fuel market expansion. Strategic partnerships, particularly those that combine specialized analytics capabilities with broad cloud infrastructure, will be instrumental in unlocking new market opportunities. The increasing demand for real-time insights, coupled with the ongoing development of more accessible and user-friendly platforms, will democratize access to powerful data analytics tools, further propelling market growth. The future of Big Data platforms lies in their ability to seamlessly integrate, analyze, and derive actionable intelligence from the ever-increasing volume of global data, thereby empowering organizations to achieve unprecedented levels of efficiency, innovation, and competitive advantage.

Big Data Platform Segmentation

-

1. Application

- 1.1. Banking

- 1.2. Manufacturing

- 1.3. Professional Services

- 1.4. Government

- 1.5. Others

-

2. Type

- 2.1. Cloud-Based

- 2.2. On-Premise

Big Data Platform Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Big Data Platform Regional Market Share

Geographic Coverage of Big Data Platform

Big Data Platform REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Big Data Platform Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Banking

- 5.1.2. Manufacturing

- 5.1.3. Professional Services

- 5.1.4. Government

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Cloud-Based

- 5.2.2. On-Premise

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Big Data Platform Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Banking

- 6.1.2. Manufacturing

- 6.1.3. Professional Services

- 6.1.4. Government

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Cloud-Based

- 6.2.2. On-Premise

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Big Data Platform Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Banking

- 7.1.2. Manufacturing

- 7.1.3. Professional Services

- 7.1.4. Government

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Cloud-Based

- 7.2.2. On-Premise

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Big Data Platform Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Banking

- 8.1.2. Manufacturing

- 8.1.3. Professional Services

- 8.1.4. Government

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Cloud-Based

- 8.2.2. On-Premise

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Big Data Platform Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Banking

- 9.1.2. Manufacturing

- 9.1.3. Professional Services

- 9.1.4. Government

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Cloud-Based

- 9.2.2. On-Premise

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Big Data Platform Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Banking

- 10.1.2. Manufacturing

- 10.1.3. Professional Services

- 10.1.4. Government

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Cloud-Based

- 10.2.2. On-Premise

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Microsoft

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Google

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 AWS

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 IBM

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Dell

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Splunk

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Micro Focus

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 SAP

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Accenture

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Informatica

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Teradata

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Oracle

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Cloudera

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Palantir

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 HPE

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Cisco

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 SAS

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Microsoft

List of Figures

- Figure 1: Global Big Data Platform Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Big Data Platform Revenue (million), by Application 2025 & 2033

- Figure 3: North America Big Data Platform Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Big Data Platform Revenue (million), by Type 2025 & 2033

- Figure 5: North America Big Data Platform Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Big Data Platform Revenue (million), by Country 2025 & 2033

- Figure 7: North America Big Data Platform Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Big Data Platform Revenue (million), by Application 2025 & 2033

- Figure 9: South America Big Data Platform Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Big Data Platform Revenue (million), by Type 2025 & 2033

- Figure 11: South America Big Data Platform Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Big Data Platform Revenue (million), by Country 2025 & 2033

- Figure 13: South America Big Data Platform Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Big Data Platform Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Big Data Platform Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Big Data Platform Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Big Data Platform Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Big Data Platform Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Big Data Platform Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Big Data Platform Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Big Data Platform Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Big Data Platform Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Big Data Platform Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Big Data Platform Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Big Data Platform Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Big Data Platform Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Big Data Platform Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Big Data Platform Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Big Data Platform Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Big Data Platform Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Big Data Platform Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Big Data Platform Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Big Data Platform Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Big Data Platform Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Big Data Platform Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Big Data Platform Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Big Data Platform Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Big Data Platform Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Big Data Platform Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Big Data Platform Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Big Data Platform Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Big Data Platform Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Big Data Platform Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Big Data Platform Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Big Data Platform Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Big Data Platform Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Big Data Platform Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Big Data Platform Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Big Data Platform Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Big Data Platform Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Big Data Platform?

The projected CAGR is approximately 9.5%.

2. Which companies are prominent players in the Big Data Platform?

Key companies in the market include Microsoft, Google, AWS, IBM, Dell, Splunk, Micro Focus, SAP, Accenture, Informatica, Teradata, Oracle, Cloudera, Palantir, HPE, Cisco, SAS.

3. What are the main segments of the Big Data Platform?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 126070 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Big Data Platform," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Big Data Platform report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Big Data Platform?

To stay informed about further developments, trends, and reports in the Big Data Platform, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence