Key Insights

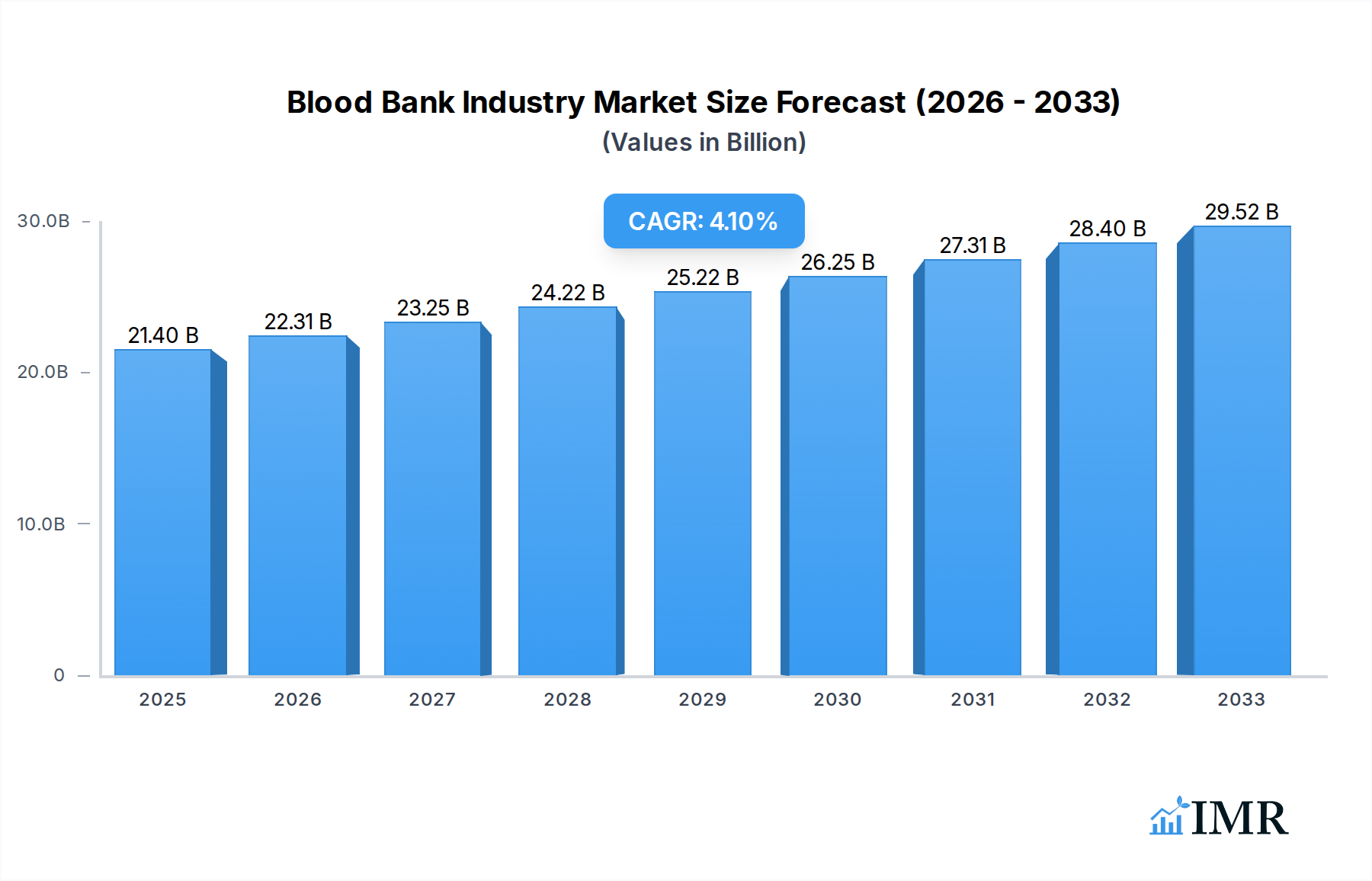

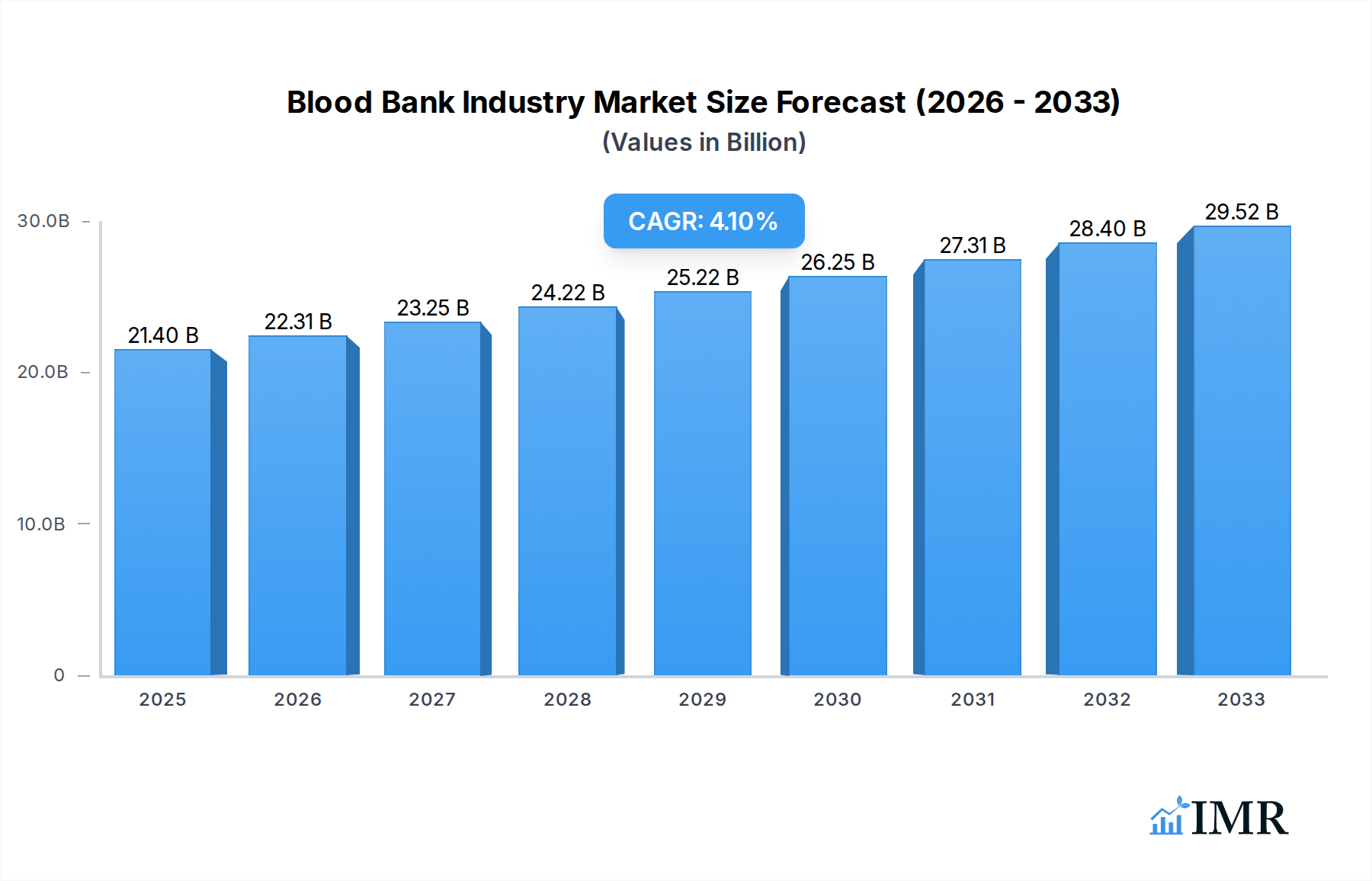

The global Blood Bank Industry is poised for significant expansion, with a projected market size of USD 21.4 billion in 2025. This growth is fueled by a steady Compound Annual Growth Rate (CAGR) of 4.3%, indicating a robust and expanding market throughout the forecast period of 2025-2033. Key drivers contributing to this upward trajectory include the increasing prevalence of chronic diseases requiring blood transfusions, advancements in blood processing and storage technologies, and a growing awareness regarding the critical importance of blood donation for healthcare. The demand for various blood products, including Red Blood Cells, Platelets, and Plasma, continues to rise due to complex medical procedures and an aging global population. Furthermore, the expansion of healthcare infrastructure, particularly in emerging economies, is creating new opportunities for blood banking services and products.

Blood Bank Industry Market Size (In Billion)

The market's growth is further propelled by evolving trends such as the adoption of sophisticated apheresis techniques for component collection, enhanced quality control measures, and the development of pathogen reduction technologies to ensure blood safety. While the industry benefits from these advancements, it also navigates certain restraints. These include the persistent challenges in donor recruitment and retention, the stringent regulatory frameworks governing blood banking operations, and the operational costs associated with maintaining specialized facilities and cold chain logistics. However, the increasing collaboration between public and private blood banks, alongside the development of innovative donation campaigns, are actively mitigating these challenges. The market is segmented across various product types, bank types, and end-users, with hospitals remaining the dominant end-user segment, underscoring the pivotal role of blood banks in acute and chronic patient care.

Blood Bank Industry Company Market Share

This comprehensive report provides an in-depth analysis of the global Blood Bank Industry, offering critical insights into market dynamics, growth trajectories, and competitive landscapes. Covering the historical period from 2019 to 2024 and projecting growth through 2033 with a base year of 2025, this report is an indispensable resource for stakeholders seeking to understand and capitalize on the evolving blood banking sector. With a focus on high-traffic keywords, including "blood donation market," "blood products," "blood storage solutions," and "blood transfusion services," this report ensures maximum search engine visibility and engagement with industry professionals. We delve into both parent and child markets, providing a holistic view of the industry's structure and potential. All quantitative data is presented in billion units for clarity and comparability.

Blood Bank Industry Market Dynamics & Structure

The Blood Bank Industry exhibits a complex market structure characterized by a moderate level of concentration, with key players dominating significant portions of the global market. Technological innovation remains a pivotal driver, with advancements in blood processing, storage, and testing technologies continuously reshaping operational efficiencies and safety standards. The regulatory framework, encompassing stringent guidelines from national health organizations and international bodies, plays a crucial role in ensuring blood safety and accessibility, thereby influencing market entry and operational compliance.

- Market Concentration: Dominated by a few large non-profit organizations and private companies, but with a growing number of regional and specialized players.

- Technological Innovation: Focus on improved apheresis machines, advanced blood component separation techniques, nucleic acid testing (NAT), and cold chain logistics.

- Regulatory Frameworks: Stringent adherence to FDA (USA), EMA (Europe), and other national health authority regulations for blood collection, testing, processing, and distribution.

- Competitive Product Substitutes: While direct substitutes for human blood are limited, advancements in artificial blood or oxygen carriers are closely monitored as potential long-term disruptors.

- End-User Demographics: Primarily driven by hospital demand for blood transfusions, surgeries, and trauma care, with increasing utilization in specialized medical procedures.

- Mergers & Acquisitions (M&A) Trends: A steady stream of M&A activity aimed at consolidating market share, expanding geographical reach, and acquiring innovative technologies.

Blood Bank Industry Growth Trends & Insights

The global Blood Bank Industry is poised for significant expansion, driven by an increasing demand for blood products and advancements in transfusion medicine. The market size is projected to witness a robust Compound Annual Growth Rate (CAGR) over the forecast period, fueled by rising healthcare expenditure, an aging global population, and a higher incidence of chronic diseases and complex medical procedures. Adoption rates of advanced blood management technologies are steadily increasing, enhancing efficiency and safety in blood banks. Technological disruptions, such as automated collection systems and improved diagnostic tools, are optimizing the entire blood supply chain. Consumer behavior shifts, particularly increased awareness campaigns promoting blood donation and a growing understanding of the critical role of blood banks in public health, are contributing positively to market growth.

The industry is witnessing a surge in demand for specific blood components, especially platelets and plasma, due to their critical role in treating various hematological disorders, cancer therapies, and emergency trauma. The growing prevalence of surgeries, both elective and emergency, further accentuates the need for a stable and readily available blood supply. Furthermore, advancements in research and development are unlocking new therapeutic applications for blood derivatives, such as plasma-derived medicines, driving demand and market value. The strategic focus on reducing blood wastage through sophisticated inventory management systems and optimized transfusion protocols also indirectly supports market growth by ensuring resource efficiency. Global health initiatives aimed at improving blood transfusion services in developing nations are also significant growth accelerators.

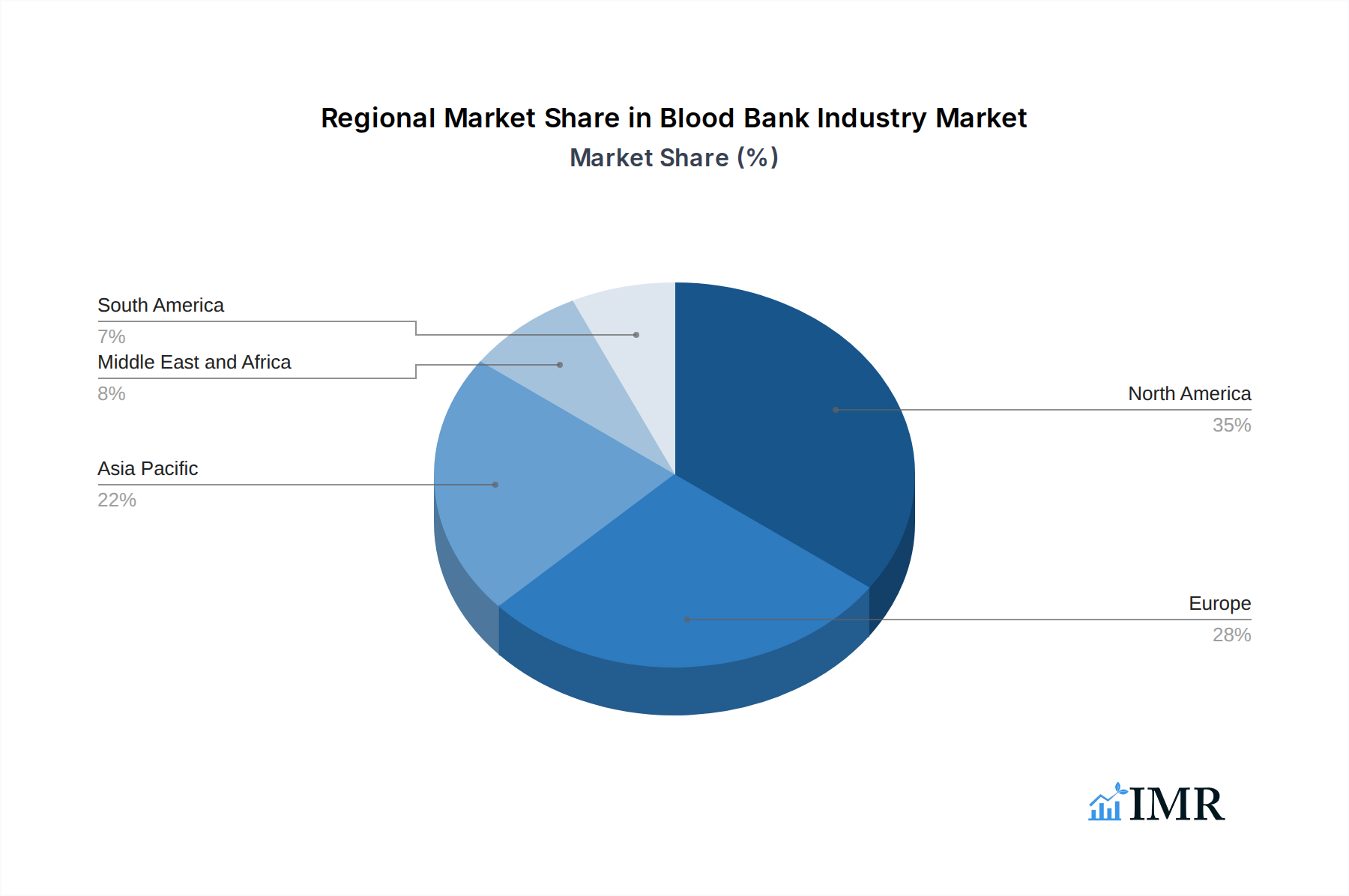

Dominant Regions, Countries, or Segments in Blood Bank Industry

The North America region currently holds a dominant position in the Blood Bank Industry, primarily driven by the United States. This dominance is attributable to several key factors, including a well-established healthcare infrastructure, high per capita healthcare spending, and a robust network of blood collection and processing centers. The presence of leading blood banks and manufacturers of blood processing equipment, coupled with advanced regulatory oversight, further solidifies its market leadership.

- Dominant Segment (Product): Red Blood Cells

- Key Drivers: Highest demand due to widespread use in treating anemia, blood loss from surgery, and trauma. Advancements in storage and preservation techniques ensure availability.

- Market Share: Consistently the largest segment by volume and value within the blood products market.

- Dominant Segment (Bank Type): Public

- Key Drivers: Majority of blood collection is conducted by public non-profit organizations, ensuring broad accessibility and community-based donation drives. Strong government support and public trust.

- Dominant Segment (End User): Hospitals

- Key Drivers: Primary recipients of blood products, accounting for the largest share of consumption due to surgical procedures, emergency care, and chronic disease management.

- Growth Potential: Continuous demand driven by an increasing number of medical procedures and an aging population requiring transfusions.

Europe also represents a significant market, with countries like Germany and the United Kingdom showing substantial contributions. This is supported by strong national blood transfusion services and a commitment to public health. Asia-Pacific is emerging as a high-growth region, with countries like China and India experiencing rapid expansion due to increasing healthcare investments, a growing patient pool, and improving awareness about blood donation.

Blood Bank Industry Product Landscape

The product landscape in the Blood Bank Industry is diverse, encompassing essential blood components vital for patient care. Red blood cells (RBCs) are the most frequently transfused product, crucial for oxygen transport. Platelets are indispensable for controlling bleeding in patients with low platelet counts, often undergoing chemotherapy or suffering from certain blood disorders. Plasma serves as a source for critical clotting factors and other proteins, vital for treating coagulation disorders and managing severe trauma. Innovations in this sector focus on enhancing the shelf-life of blood components, developing pathogen-reduced products for increased safety, and improving the efficiency of apheresis for concentrated collection of specific components like platelets.

Key Drivers, Barriers & Challenges in Blood Bank Industry

Key Drivers:

- Rising Demand for Blood Products: Increasing surgical procedures, chronic disease prevalence, and trauma cases worldwide are driving consistent demand.

- Technological Advancements: Innovations in blood processing, storage, and testing technologies are improving efficiency, safety, and product yield.

- Government Initiatives & Awareness Campaigns: Strong support from governments and effective public awareness campaigns are crucial for increasing blood donation rates.

- Aging Global Population: The growing elderly demographic is more susceptible to conditions requiring blood transfusions.

Barriers & Challenges:

- Short Shelf-Life of Blood Products: The limited viability of components like platelets necessitates constant replenishment and efficient logistics, posing supply chain challenges.

- Blood Shortages: Maintaining an adequate and consistent blood supply remains a persistent challenge due to donor fatigue, logistical issues, and unexpected surges in demand.

- Stringent Regulatory Requirements: Compliance with evolving safety and testing regulations adds significant operational costs and complexity.

- Donor Recruitment & Retention: The continuous need to recruit new donors and retain existing ones is a perpetual challenge.

- Cold Chain Management: Maintaining the integrity of blood products throughout the supply chain requires sophisticated and costly cold chain infrastructure.

Emerging Opportunities in Blood Bank Industry

Emerging opportunities in the Blood Bank Industry lie in the development of advanced blood storage solutions that extend the shelf-life of components, thereby reducing wastage and improving availability. The growing focus on personalized medicine also presents opportunities for developing specialized blood products tailored to individual patient needs. Furthermore, the increasing adoption of automation and artificial intelligence in blood screening and processing promises enhanced efficiency and accuracy. The expansion of blood banking services in emerging economies, coupled with the increasing demand for plasma-derived therapies, represents significant untapped market potential.

Growth Accelerators in the Blood Bank Industry Industry

Technological breakthroughs in blood processing and preservation are key growth accelerators, enabling longer storage periods and higher yields of critical blood components. Strategic partnerships between blood collection agencies, hospitals, and technology providers are fostering innovation and optimizing supply chain efficiencies. Market expansion strategies, particularly in developing regions with unmet healthcare needs, are unlocking new avenues for growth. The increasing research into novel applications of blood derivatives and advancements in transfusion medicine continue to fuel market expansion.

Key Players Shaping the Blood Bank Industry Market

- Australian Red Cross

- American Association of Blood Banks

- Vitalant

- Canadian Blood Services

- Fresenius Kabi

- Maco Pharma

- Terumo BCT

- Bio-Rad Laboratories

- Blood Bank of Alaska

- Ortho-Clinical

- Haemonetics

Notable Milestones in Blood Bank Industry Sector

- April 2022: The Scottish National Blood Transfusion Services launched an advertising campaign, "people like you," featuring blood donors from across Scotland. This campaign had the objective to recruit new blood donors and serve the hospitals with the blood demand in the hospitals.

- September 2021: The Illinois Medical District (IMD) in Chicago partnered with the American Red Cross to encourage people from racial and ethnic minorities to donate blood.

In-Depth Blood Bank Industry Market Outlook

The future outlook for the Blood Bank Industry is exceptionally promising, driven by sustained demand for essential blood products and continuous innovation. Growth accelerators such as advancements in apheresis technology, pathogen reduction techniques, and artificial intelligence-driven inventory management systems are set to enhance efficiency and safety. Strategic collaborations between global health organizations and private entities will be crucial for expanding access to blood services in underserved regions. The increasing focus on plasma-derived therapies and the development of synthetic blood substitutes, though nascent, represent significant future market potential. Addressing the persistent challenges of blood shortages and optimizing cold chain logistics will remain paramount for realizing the full growth trajectory of this vital sector.

Blood Bank Industry Segmentation

-

1. Product

- 1.1. Red Blood Cells

- 1.2. Whole Blood

- 1.3. Platelet

- 1.4. White Blood Cells

- 1.5. Plasma

-

2. Bank Type

- 2.1. Private

- 2.2. Public

-

3. End User

- 3.1. Hospitals

- 3.2. Ambulatory Surgical Centers

- 3.3. Other End Users

Blood Bank Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Blood Bank Industry Regional Market Share

Geographic Coverage of Blood Bank Industry

Blood Bank Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Red Blood Cells

- 5.1.2. Whole Blood

- 5.1.3. Platelet

- 5.1.4. White Blood Cells

- 5.1.5. Plasma

- 5.2. Market Analysis, Insights and Forecast - by Bank Type

- 5.2.1. Private

- 5.2.2. Public

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Hospitals

- 5.3.2. Ambulatory Surgical Centers

- 5.3.3. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Global Blood Bank Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Red Blood Cells

- 6.1.2. Whole Blood

- 6.1.3. Platelet

- 6.1.4. White Blood Cells

- 6.1.5. Plasma

- 6.2. Market Analysis, Insights and Forecast - by Bank Type

- 6.2.1. Private

- 6.2.2. Public

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Hospitals

- 6.3.2. Ambulatory Surgical Centers

- 6.3.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. North America Blood Bank Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Red Blood Cells

- 7.1.2. Whole Blood

- 7.1.3. Platelet

- 7.1.4. White Blood Cells

- 7.1.5. Plasma

- 7.2. Market Analysis, Insights and Forecast - by Bank Type

- 7.2.1. Private

- 7.2.2. Public

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Hospitals

- 7.3.2. Ambulatory Surgical Centers

- 7.3.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Europe Blood Bank Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Red Blood Cells

- 8.1.2. Whole Blood

- 8.1.3. Platelet

- 8.1.4. White Blood Cells

- 8.1.5. Plasma

- 8.2. Market Analysis, Insights and Forecast - by Bank Type

- 8.2.1. Private

- 8.2.2. Public

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Hospitals

- 8.3.2. Ambulatory Surgical Centers

- 8.3.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Asia Pacific Blood Bank Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Red Blood Cells

- 9.1.2. Whole Blood

- 9.1.3. Platelet

- 9.1.4. White Blood Cells

- 9.1.5. Plasma

- 9.2. Market Analysis, Insights and Forecast - by Bank Type

- 9.2.1. Private

- 9.2.2. Public

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Hospitals

- 9.3.2. Ambulatory Surgical Centers

- 9.3.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. Middle East and Africa Blood Bank Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Red Blood Cells

- 10.1.2. Whole Blood

- 10.1.3. Platelet

- 10.1.4. White Blood Cells

- 10.1.5. Plasma

- 10.2. Market Analysis, Insights and Forecast - by Bank Type

- 10.2.1. Private

- 10.2.2. Public

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Hospitals

- 10.3.2. Ambulatory Surgical Centers

- 10.3.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. South America Blood Bank Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product

- 11.1.1. Red Blood Cells

- 11.1.2. Whole Blood

- 11.1.3. Platelet

- 11.1.4. White Blood Cells

- 11.1.5. Plasma

- 11.2. Market Analysis, Insights and Forecast - by Bank Type

- 11.2.1. Private

- 11.2.2. Public

- 11.3. Market Analysis, Insights and Forecast - by End User

- 11.3.1. Hospitals

- 11.3.2. Ambulatory Surgical Centers

- 11.3.3. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Product

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Australian Red Cross

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 American Association of Blood Banks

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Vitalant

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Canadian Blood Services

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Fresenius Kabi

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Maco Pharma

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Teruma BCT

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Bio-Rad Laboratories

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Blood Bank of Alaska

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Ortho-Clinical

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Haemonetics

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Australian Red Cross

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Blood Bank Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Blood Bank Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Blood Bank Industry Revenue (billion), by Product 2025 & 2033

- Figure 4: North America Blood Bank Industry Volume (K Unit), by Product 2025 & 2033

- Figure 5: North America Blood Bank Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Blood Bank Industry Volume Share (%), by Product 2025 & 2033

- Figure 7: North America Blood Bank Industry Revenue (billion), by Bank Type 2025 & 2033

- Figure 8: North America Blood Bank Industry Volume (K Unit), by Bank Type 2025 & 2033

- Figure 9: North America Blood Bank Industry Revenue Share (%), by Bank Type 2025 & 2033

- Figure 10: North America Blood Bank Industry Volume Share (%), by Bank Type 2025 & 2033

- Figure 11: North America Blood Bank Industry Revenue (billion), by End User 2025 & 2033

- Figure 12: North America Blood Bank Industry Volume (K Unit), by End User 2025 & 2033

- Figure 13: North America Blood Bank Industry Revenue Share (%), by End User 2025 & 2033

- Figure 14: North America Blood Bank Industry Volume Share (%), by End User 2025 & 2033

- Figure 15: North America Blood Bank Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: North America Blood Bank Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Blood Bank Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Blood Bank Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Blood Bank Industry Revenue (billion), by Product 2025 & 2033

- Figure 20: Europe Blood Bank Industry Volume (K Unit), by Product 2025 & 2033

- Figure 21: Europe Blood Bank Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Europe Blood Bank Industry Volume Share (%), by Product 2025 & 2033

- Figure 23: Europe Blood Bank Industry Revenue (billion), by Bank Type 2025 & 2033

- Figure 24: Europe Blood Bank Industry Volume (K Unit), by Bank Type 2025 & 2033

- Figure 25: Europe Blood Bank Industry Revenue Share (%), by Bank Type 2025 & 2033

- Figure 26: Europe Blood Bank Industry Volume Share (%), by Bank Type 2025 & 2033

- Figure 27: Europe Blood Bank Industry Revenue (billion), by End User 2025 & 2033

- Figure 28: Europe Blood Bank Industry Volume (K Unit), by End User 2025 & 2033

- Figure 29: Europe Blood Bank Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: Europe Blood Bank Industry Volume Share (%), by End User 2025 & 2033

- Figure 31: Europe Blood Bank Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: Europe Blood Bank Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Blood Bank Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Blood Bank Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Blood Bank Industry Revenue (billion), by Product 2025 & 2033

- Figure 36: Asia Pacific Blood Bank Industry Volume (K Unit), by Product 2025 & 2033

- Figure 37: Asia Pacific Blood Bank Industry Revenue Share (%), by Product 2025 & 2033

- Figure 38: Asia Pacific Blood Bank Industry Volume Share (%), by Product 2025 & 2033

- Figure 39: Asia Pacific Blood Bank Industry Revenue (billion), by Bank Type 2025 & 2033

- Figure 40: Asia Pacific Blood Bank Industry Volume (K Unit), by Bank Type 2025 & 2033

- Figure 41: Asia Pacific Blood Bank Industry Revenue Share (%), by Bank Type 2025 & 2033

- Figure 42: Asia Pacific Blood Bank Industry Volume Share (%), by Bank Type 2025 & 2033

- Figure 43: Asia Pacific Blood Bank Industry Revenue (billion), by End User 2025 & 2033

- Figure 44: Asia Pacific Blood Bank Industry Volume (K Unit), by End User 2025 & 2033

- Figure 45: Asia Pacific Blood Bank Industry Revenue Share (%), by End User 2025 & 2033

- Figure 46: Asia Pacific Blood Bank Industry Volume Share (%), by End User 2025 & 2033

- Figure 47: Asia Pacific Blood Bank Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Asia Pacific Blood Bank Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Blood Bank Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Blood Bank Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Blood Bank Industry Revenue (billion), by Product 2025 & 2033

- Figure 52: Middle East and Africa Blood Bank Industry Volume (K Unit), by Product 2025 & 2033

- Figure 53: Middle East and Africa Blood Bank Industry Revenue Share (%), by Product 2025 & 2033

- Figure 54: Middle East and Africa Blood Bank Industry Volume Share (%), by Product 2025 & 2033

- Figure 55: Middle East and Africa Blood Bank Industry Revenue (billion), by Bank Type 2025 & 2033

- Figure 56: Middle East and Africa Blood Bank Industry Volume (K Unit), by Bank Type 2025 & 2033

- Figure 57: Middle East and Africa Blood Bank Industry Revenue Share (%), by Bank Type 2025 & 2033

- Figure 58: Middle East and Africa Blood Bank Industry Volume Share (%), by Bank Type 2025 & 2033

- Figure 59: Middle East and Africa Blood Bank Industry Revenue (billion), by End User 2025 & 2033

- Figure 60: Middle East and Africa Blood Bank Industry Volume (K Unit), by End User 2025 & 2033

- Figure 61: Middle East and Africa Blood Bank Industry Revenue Share (%), by End User 2025 & 2033

- Figure 62: Middle East and Africa Blood Bank Industry Volume Share (%), by End User 2025 & 2033

- Figure 63: Middle East and Africa Blood Bank Industry Revenue (billion), by Country 2025 & 2033

- Figure 64: Middle East and Africa Blood Bank Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Middle East and Africa Blood Bank Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Blood Bank Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: South America Blood Bank Industry Revenue (billion), by Product 2025 & 2033

- Figure 68: South America Blood Bank Industry Volume (K Unit), by Product 2025 & 2033

- Figure 69: South America Blood Bank Industry Revenue Share (%), by Product 2025 & 2033

- Figure 70: South America Blood Bank Industry Volume Share (%), by Product 2025 & 2033

- Figure 71: South America Blood Bank Industry Revenue (billion), by Bank Type 2025 & 2033

- Figure 72: South America Blood Bank Industry Volume (K Unit), by Bank Type 2025 & 2033

- Figure 73: South America Blood Bank Industry Revenue Share (%), by Bank Type 2025 & 2033

- Figure 74: South America Blood Bank Industry Volume Share (%), by Bank Type 2025 & 2033

- Figure 75: South America Blood Bank Industry Revenue (billion), by End User 2025 & 2033

- Figure 76: South America Blood Bank Industry Volume (K Unit), by End User 2025 & 2033

- Figure 77: South America Blood Bank Industry Revenue Share (%), by End User 2025 & 2033

- Figure 78: South America Blood Bank Industry Volume Share (%), by End User 2025 & 2033

- Figure 79: South America Blood Bank Industry Revenue (billion), by Country 2025 & 2033

- Figure 80: South America Blood Bank Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: South America Blood Bank Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Blood Bank Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Blood Bank Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 2: Global Blood Bank Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 3: Global Blood Bank Industry Revenue billion Forecast, by Bank Type 2020 & 2033

- Table 4: Global Blood Bank Industry Volume K Unit Forecast, by Bank Type 2020 & 2033

- Table 5: Global Blood Bank Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Blood Bank Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 7: Global Blood Bank Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Global Blood Bank Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Blood Bank Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 10: Global Blood Bank Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 11: Global Blood Bank Industry Revenue billion Forecast, by Bank Type 2020 & 2033

- Table 12: Global Blood Bank Industry Volume K Unit Forecast, by Bank Type 2020 & 2033

- Table 13: Global Blood Bank Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 14: Global Blood Bank Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 15: Global Blood Bank Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Blood Bank Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: United States Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Canada Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Mexico Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Blood Bank Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 24: Global Blood Bank Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 25: Global Blood Bank Industry Revenue billion Forecast, by Bank Type 2020 & 2033

- Table 26: Global Blood Bank Industry Volume K Unit Forecast, by Bank Type 2020 & 2033

- Table 27: Global Blood Bank Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 28: Global Blood Bank Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 29: Global Blood Bank Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Global Blood Bank Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Germany Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: France Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Italy Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Spain Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Blood Bank Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 44: Global Blood Bank Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 45: Global Blood Bank Industry Revenue billion Forecast, by Bank Type 2020 & 2033

- Table 46: Global Blood Bank Industry Volume K Unit Forecast, by Bank Type 2020 & 2033

- Table 47: Global Blood Bank Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 48: Global Blood Bank Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 49: Global Blood Bank Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: Global Blood Bank Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: China Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: India Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Australia Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: South Korea Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Blood Bank Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 64: Global Blood Bank Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 65: Global Blood Bank Industry Revenue billion Forecast, by Bank Type 2020 & 2033

- Table 66: Global Blood Bank Industry Volume K Unit Forecast, by Bank Type 2020 & 2033

- Table 67: Global Blood Bank Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 68: Global Blood Bank Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 69: Global Blood Bank Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 70: Global Blood Bank Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: GCC Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 74: South Africa Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Global Blood Bank Industry Revenue billion Forecast, by Product 2020 & 2033

- Table 78: Global Blood Bank Industry Volume K Unit Forecast, by Product 2020 & 2033

- Table 79: Global Blood Bank Industry Revenue billion Forecast, by Bank Type 2020 & 2033

- Table 80: Global Blood Bank Industry Volume K Unit Forecast, by Bank Type 2020 & 2033

- Table 81: Global Blood Bank Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 82: Global Blood Bank Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 83: Global Blood Bank Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 84: Global Blood Bank Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: Brazil Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: Argentina Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Blood Bank Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Blood Bank Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Blood Bank Industry?

The projected CAGR is approximately 4.3%.

2. Which companies are prominent players in the Blood Bank Industry?

Key companies in the market include Australian Red Cross, American Association of Blood Banks, Vitalant, Canadian Blood Services, Fresenius Kabi, Maco Pharma, Teruma BCT, Bio-Rad Laboratories, Blood Bank of Alaska, Ortho-Clinical, Haemonetics.

3. What are the main segments of the Blood Bank Industry?

The market segments include Product, Bank Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 21.4 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Number of Surgeries and Accidents; High Prevalence of Hematologic Diseases; Technological Advancements in Blood Banking Technology.

6. What are the notable trends driving market growth?

The Red Blood Cells Segment is Estimated to Witness Healthy Growth in this Market Over the Forecast Period.

7. Are there any restraints impacting market growth?

Stringent Rules and Regulations.

8. Can you provide examples of recent developments in the market?

April 2022: The Scottish National Blood Transfusion Services launched an advertising campaign, " people like you," featuring blood donors from across Scotland. This campaign had the objective to recruit new blood donors and serve the hospitals with the blood demand in the hospitals.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Blood Bank Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Blood Bank Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Blood Bank Industry?

To stay informed about further developments, trends, and reports in the Blood Bank Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence