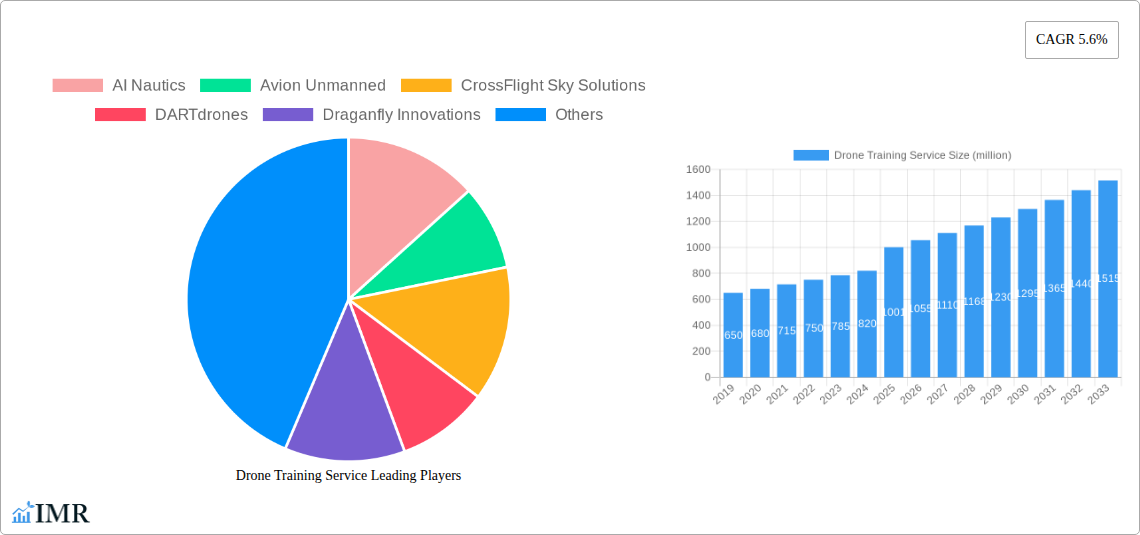

Key Insights

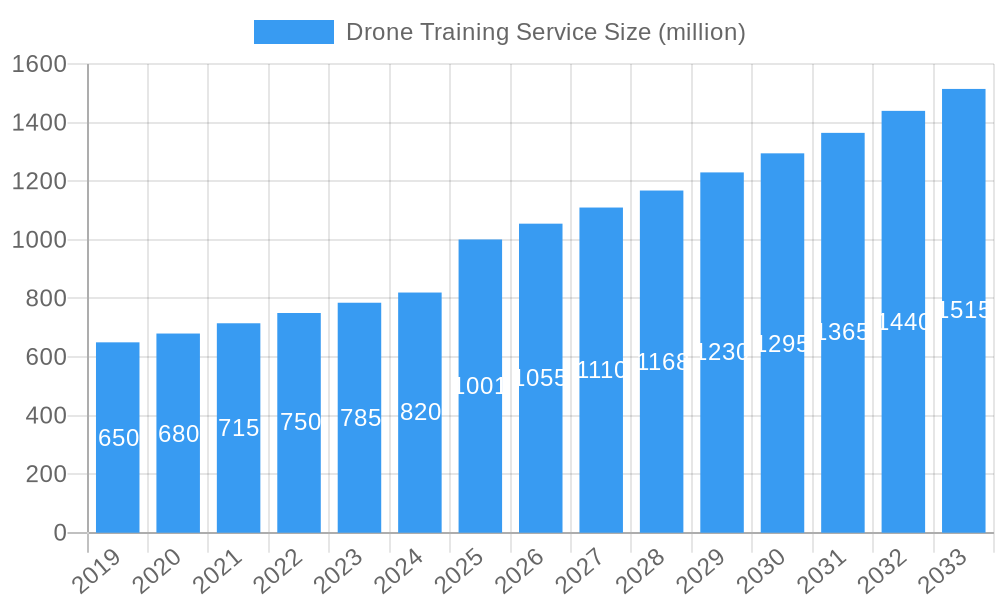

The global Drone Training Service market is poised for significant expansion, projected to reach approximately $1,001 million by 2025. This growth trajectory is underpinned by a robust Compound Annual Growth Rate (CAGR) of 5.6% anticipated between 2019 and 2033. The market's dynamism is fueled by the increasing adoption of drones across diverse sectors, necessitating skilled operation and regulatory compliance. Key drivers include the burgeoning demand for commercial drone applications, such as aerial surveying, inspection, delivery, and security, which directly translate into a need for specialized training. Furthermore, the evolving regulatory landscape, with governments worldwide establishing clearer guidelines for drone usage, is compelling individuals and organizations to invest in certified training programs to ensure safe and legal operations. The growing emphasis on unmanned aerial vehicle (UAV) technology in both enterprise and personal applications, coupled with the convenience offered by online training modules, is expected to further propel market growth.

Drone Training Service Market Size (In Million)

The market is segmented into various applications, including enterprise, personal, and group training, catering to a broad spectrum of users. Within these segments, both online and offline training modalities are gaining traction, offering flexibility and accessibility. While the market is experiencing strong growth, certain restraints may emerge, such as the initial cost of professional drone training and the potential for rapid technological obsolescence requiring continuous skill updates. However, the overarching trend favors increased investment in drone technology and, consequently, in the training services that enable its effective and safe utilization. Key players like Draganfly Innovations, DroneDeploy, and AI Nautics are actively shaping the market through innovative training solutions and technological advancements, further stimulating market development and expanding the reach of drone operations globally.

Drone Training Service Company Market Share

Drone Training Service Market Dynamics & Structure

The drone training service market is characterized by a moderate to high concentration, driven by a blend of established industry players and emerging specialists. Technological innovation acts as a primary catalyst, with advancements in AI-powered flight control, advanced sensor integration, and immersive simulation technologies continually redefining training methodologies. Regulatory frameworks, while evolving, also play a significant role, shaping curriculum development and certification requirements. Competitive product substitutes, such as self-paced online modules and informal workshops, exist but often lack the comprehensive accreditation and hands-on experience offered by structured training programs. End-user demographics are increasingly diverse, encompassing enterprise-level professionals seeking to enhance operational efficiency, personal users pursuing recreational or small-scale commercial applications, and groups requiring tailored solutions for specific industries. Mergers and acquisitions (M&A) are becoming more prevalent as larger companies seek to expand their service portfolios and geographical reach, integrating specialized training providers to strengthen their market position. For instance, a recent acquisition in Q4 2024 by a leading drone solutions provider aimed to bolster its enterprise training capabilities.

- Market Concentration: Dominated by a mix of specialized drone training institutes and larger aerospace/technology firms expanding into the sector.

- Technological Innovation Drivers: AI-driven analytics for performance feedback, VR/AR for realistic simulation, and advanced drone platform integration into training modules.

- Regulatory Frameworks: FAA regulations in the US and EASA in Europe significantly influence curriculum and certification pathways, driving demand for compliant training.

- Competitive Product Substitutes: Online courses, pilot forums, and equipment manuals offer supplementary learning but are generally not substitutes for certified training.

- End-User Demographics: Enterprise clients (agriculture, construction, public safety), prosumers (photography, inspection), and recreational pilots.

- M&A Trends: Increasing consolidation as established players acquire niche training providers to gain market share and expertise.

Drone Training Service Growth Trends & Insights

The drone training service market is projected for substantial growth, driven by an escalating demand for skilled drone operators across a multitude of industries. The market size is expected to grow from an estimated $1,500 million in the base year 2025 to an impressive $4,500 million by the end of the forecast period in 2033, representing a Compound Annual Growth Rate (CAGR) of approximately 11.8%. Adoption rates are accelerating rapidly, particularly within the enterprise segment, where businesses recognize the transformative potential of drones for data collection, inspection, logistics, and security. Technological disruptions, such as the development of more autonomous flight systems and sophisticated drone hardware, necessitate continuous upskilling and reskilling of operators, further fueling the demand for advanced training programs. Consumer behavior shifts are also evident, with a growing appreciation for certified training that ensures safety, compliance, and operational efficiency. The historical period from 2019 to 2024 witnessed steady growth, with early adopters laying the groundwork for the widespread market penetration observed today.

The increasing adoption of drones across various sectors, including but not limited to agriculture, construction, filmmaking, and public safety, directly correlates with the burgeoning need for specialized training. As drone technology becomes more accessible and sophisticated, the complexity of operating these machines safely and effectively increases, creating a critical demand for structured educational programs. This demand is further amplified by evolving regulatory landscapes that mandate certified training for commercial drone operations. For instance, the implementation of new FAA Part 107 recurrent training requirements has spurred significant interest in online and blended learning formats. The market penetration of certified drone pilots is still relatively low compared to the overall adoption of drone technology, indicating a vast untapped potential for training service providers.

Technological advancements are not only driving the need for training but also shaping its delivery. The integration of virtual reality (VR) and augmented reality (AR) into training modules offers immersive and realistic flight simulations, allowing trainees to practice complex maneuvers and emergency procedures in a safe, controlled environment. This enhances learning outcomes and reduces the risk associated with real-world flight training. Furthermore, the development of AI-powered analytics tools provides personalized feedback on pilot performance, identifying areas for improvement and optimizing training plans. The shift towards data-driven decision-making in all industries also means that drone operators need to be proficient not only in piloting but also in data acquisition, processing, and interpretation, adding another layer to the training requirements.

Consumer behavior is evolving to prioritize safety, efficiency, and compliance. Individuals and organizations are increasingly seeking training that offers verifiable credentials and a robust understanding of operational best practices, rather than informal or self-taught methods. This shift is driven by a growing awareness of the potential risks associated with untrained operation, including accidents, regulatory fines, and data integrity issues. The accessibility of online training platforms has democratized access to drone education, allowing a broader audience to acquire the necessary skills. However, the need for hands-on, practical experience remains paramount, leading to a growing demand for blended learning models that combine online theoretical instruction with in-person practical flight sessions. This hybrid approach caters to diverse learning preferences and ensures comprehensive skill development.

Dominant Regions, Countries, or Segments in Drone Training Service

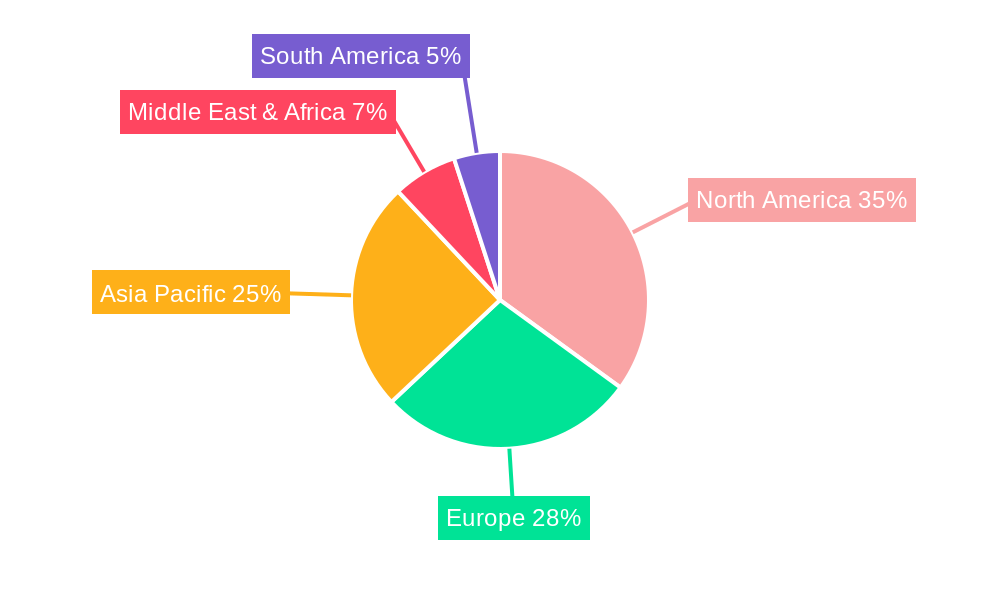

The Enterprise Application segment, specifically within the Online Training type, is emerging as the most dominant force driving growth in the global drone training service market. This dominance is propelled by a confluence of robust economic policies, substantial investments in drone technology by corporations, and the inherent need for scalable, efficient, and compliant training solutions for commercial operations. The United States currently leads the market, fueled by its advanced technological infrastructure, extensive drone industry ecosystem, and a strong regulatory framework that encourages certified professional training. North America, as a region, exhibits this trend most prominently, accounting for an estimated 40% of the global drone training market share.

- Dominant Application Segment: Enterprise applications are leading the market due to their widespread adoption in sectors like construction, agriculture, infrastructure inspection, public safety, and logistics. These industries require trained professionals for efficient data acquisition, site surveys, asset monitoring, and emergency response, directly translating into a high demand for specialized drone training services. The enterprise segment is projected to contribute approximately 70% of the total market revenue by 2028.

- Dominant Training Type: Online training is experiencing a meteoric rise due to its inherent flexibility, scalability, and cost-effectiveness. It allows a large number of professionals to acquire essential knowledge and certifications without the constraints of geographical location or fixed schedules. This mode of delivery is particularly favored by enterprises looking to train dispersed workforces. Online training is expected to capture over 65% of the market share by 2030.

- Leading Region: North America, spearheaded by the United States, commands the largest market share, estimated at over $600 million in 2025. This is attributed to early adoption of drone technology, extensive commercial drone deployments, and a proactive regulatory environment that necessitates skilled operators.

- Key Drivers in North America:

- Economic Policies: Government initiatives promoting drone adoption and industry growth, including R&D grants and tax incentives.

- Infrastructure: Well-established aerospace and technology sectors, providing a strong foundation for drone training development and delivery.

- Industry Demand: High prevalence of drone usage in key industries such as construction (valued at $200 million in training expenditure), agriculture ($150 million), and public safety ($120 million).

- Regulatory Landscape: Clearer FAA regulations and certification pathways that mandate professional training for commercial operators.

The growth potential within the enterprise segment is immense, as more industries recognize the return on investment offered by drone technology. Companies are increasingly investing in in-house drone programs, requiring standardized and comprehensive training for their personnel. This trend is further bolstered by advancements in drone capabilities, such as longer flight times, higher payload capacities, and more sophisticated sensor payloads, which expand the scope of enterprise applications. The shift towards data-driven operations across all business verticals necessitates skilled operators capable of not only flying drones but also managing and interpreting the data they collect. The online training format ensures that this upskilling can happen at scale, efficiently and cost-effectively.

Drone Training Service Product Landscape

The drone training service product landscape is evolving rapidly, with a focus on delivering specialized curricula tailored to diverse industry needs. Innovations include highly interactive online modules incorporating AI-driven feedback, virtual reality flight simulators for risk-free practice of complex scenarios, and blended learning programs that combine theoretical knowledge with hands-on flight experience. Performance metrics emphasized include enhanced pilot proficiency, improved safety records, and compliance with regulatory standards. Unique selling propositions revolve around industry-specific certifications, expert instructors with real-world experience, and flexible training schedules. Technological advancements are integrating simulation software with actual drone data to provide more realistic training environments.

Key Drivers, Barriers & Challenges in Drone Training Service

Key Drivers:

- Technological Advancements: The continuous evolution of drone hardware and software, including AI, sensor technology, and autonomy, necessitates ongoing training for operators.

- Increasing Drone Adoption: Growing deployment of drones across industries like agriculture, construction, public safety, and logistics fuels the demand for skilled pilots.

- Regulatory Mandates: Evolving government regulations and certification requirements for commercial drone operations make professional training indispensable.

- Safety and Efficiency Demands: The imperative for safe, efficient, and compliant drone operations drives the need for structured training programs.

Key Barriers & Challenges:

- High Initial Investment: Developing comprehensive training programs, including simulators and hands-on flight equipment, requires significant upfront capital.

- Regulatory Uncertainty: The dynamic nature of drone regulations across different jurisdictions can create complexities for training providers.

- Talent Acquisition and Retention: Attracting and retaining highly qualified instructors with both technical expertise and teaching skills can be challenging.

- Market Saturation: Increasing competition from new entrants and established players can lead to pricing pressures and challenges in differentiating services. Supply chain issues for training equipment can also pose a temporary restraint, impacting offline training delivery. The cost of maintaining cutting-edge simulation technology is also a significant operational hurdle.

Emerging Opportunities in Drone Training Service

Emerging opportunities in the drone training service sector lie in the development of specialized training modules for niche applications, such as advanced aerial surveying, drone-based infrastructure inspection for critical assets, and sophisticated swarm robotics training. The growing demand for certified drone pilots in emerging markets in Asia-Pacific and Latin America presents significant untapped potential. Furthermore, the integration of drone data analytics and AI-driven insights into training curricula offers a value-added service for enterprises seeking to maximize their drone investments. The increasing focus on drone sustainability and ethical operation also opens avenues for specialized training programs.

Growth Accelerators in the Drone Training Service Industry

The long-term growth of the drone training service industry is being significantly accelerated by several key factors. Technological breakthroughs in drone miniaturization and enhanced sensor capabilities are expanding the application spectrum, thereby increasing the need for trained operators. Strategic partnerships between drone manufacturers, training providers, and enterprise clients are crucial for developing industry-aligned curricula and ensuring widespread adoption. Furthermore, market expansion strategies, including the development of accessible online platforms and localized training centers in underserved regions, are unlocking new revenue streams and driving global growth. The increasing demand for specialized skills in areas like BVLOS (Beyond Visual Line of Sight) operations is a prime example of a growth accelerator.

Key Players Shaping the Drone Training Service Market

- AI Nautics

- Avion Unmanned

- CrossFlight Sky Solutions

- DARTdrones

- Draganfly Innovations

- Drone Co

- Drone USA

- DroneDeploy

- Dronegenuity

- Dronitek

- FTG Drones

- RiP Group

- SkyOp LLC

- Steel City Drones

- Telesis Systems, Inc

Notable Milestones in Drone Training Service Sector

- 2022 Q1: DARTdrones launches comprehensive online certification prep course for FAA Part 107, seeing a 30% increase in sign-ups.

- 2022 Q3: Draganfly Innovations partners with a university to develop an advanced drone piloting and maintenance curriculum.

- 2023 Q1: DroneDeploy introduces new training modules focused on AI-powered data analysis for construction projects.

- 2023 Q4: A significant merger between Avion Unmanned and SkyOp LLC creates a larger entity with expanded training offerings and geographic reach.

- 2024 Q2: FAA introduces updated recurrent training requirements, leading to a surge in demand for online refresher courses from providers like Dronegenuity.

In-Depth Drone Training Service Market Outlook

The future outlook for the drone training service market remains exceptionally bright, driven by sustained technological advancements and increasing global drone adoption. Growth accelerators such as the expansion of drone applications into new sectors and the development of sophisticated AI-driven training simulations will continue to fuel demand. Strategic partnerships between training providers and industry leaders will ensure the development of relevant and high-quality curricula, catering to the evolving needs of the market. Market expansion strategies focusing on emerging economies and specialized training niches will unlock significant future growth potential, solidifying the importance of skilled drone operation in the years to come. The market is projected to reach approximately $8,000 million by 2033.

Drone Training Service Segmentation

-

1. Application

- 1.1. Enterprise

- 1.2. Personal

- 1.3. Group

-

2. Type

- 2.1. Online Training

- 2.2. Offline Training

Drone Training Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Drone Training Service Regional Market Share

Geographic Coverage of Drone Training Service

Drone Training Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 27.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Enterprise

- 5.1.2. Personal

- 5.1.3. Group

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Online Training

- 5.2.2. Offline Training

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Drone Training Service Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Enterprise

- 6.1.2. Personal

- 6.1.3. Group

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Online Training

- 6.2.2. Offline Training

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Drone Training Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Enterprise

- 7.1.2. Personal

- 7.1.3. Group

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Online Training

- 7.2.2. Offline Training

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Drone Training Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Enterprise

- 8.1.2. Personal

- 8.1.3. Group

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Online Training

- 8.2.2. Offline Training

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Drone Training Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Enterprise

- 9.1.2. Personal

- 9.1.3. Group

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Online Training

- 9.2.2. Offline Training

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Drone Training Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Enterprise

- 10.1.2. Personal

- 10.1.3. Group

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Online Training

- 10.2.2. Offline Training

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Drone Training Service Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Enterprise

- 11.1.2. Personal

- 11.1.3. Group

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Online Training

- 11.2.2. Offline Training

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 AI Nautics

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Avion Unmanned

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 CrossFlight Sky Solutions

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DARTdrones

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Draganfly Innovations

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Drone Co

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Drone USA

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 DroneDeploy

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Dronegenuity

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Dronitek

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 FTG Drones

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 RiP Group

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 SkyOp LLC

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Steel City Drones

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Telesis Systems Inc

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 AI Nautics

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Drone Training Service Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Drone Training Service Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Drone Training Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Drone Training Service Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Drone Training Service Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Drone Training Service Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Drone Training Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Drone Training Service Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Drone Training Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Drone Training Service Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Drone Training Service Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Drone Training Service Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Drone Training Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Drone Training Service Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Drone Training Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Drone Training Service Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Drone Training Service Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Drone Training Service Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Drone Training Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Drone Training Service Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Drone Training Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Drone Training Service Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Drone Training Service Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Drone Training Service Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Drone Training Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Drone Training Service Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Drone Training Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Drone Training Service Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Drone Training Service Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Drone Training Service Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Drone Training Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Drone Training Service Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Drone Training Service Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Drone Training Service Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Drone Training Service Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Drone Training Service Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Drone Training Service Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Drone Training Service Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Drone Training Service Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Drone Training Service Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Drone Training Service Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Drone Training Service Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Drone Training Service Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Drone Training Service Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Drone Training Service Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Drone Training Service Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Drone Training Service Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Drone Training Service Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Drone Training Service Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Drone Training Service Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Drone Training Service?

The projected CAGR is approximately 27.7%.

2. Which companies are prominent players in the Drone Training Service?

Key companies in the market include AI Nautics, Avion Unmanned, CrossFlight Sky Solutions, DARTdrones, Draganfly Innovations, Drone Co, Drone USA, DroneDeploy, Dronegenuity, Dronitek, FTG Drones, RiP Group, SkyOp LLC, Steel City Drones, Telesis Systems, Inc.

3. What are the main segments of the Drone Training Service?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 17 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Drone Training Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Drone Training Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Drone Training Service?

To stay informed about further developments, trends, and reports in the Drone Training Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence