Key Insights

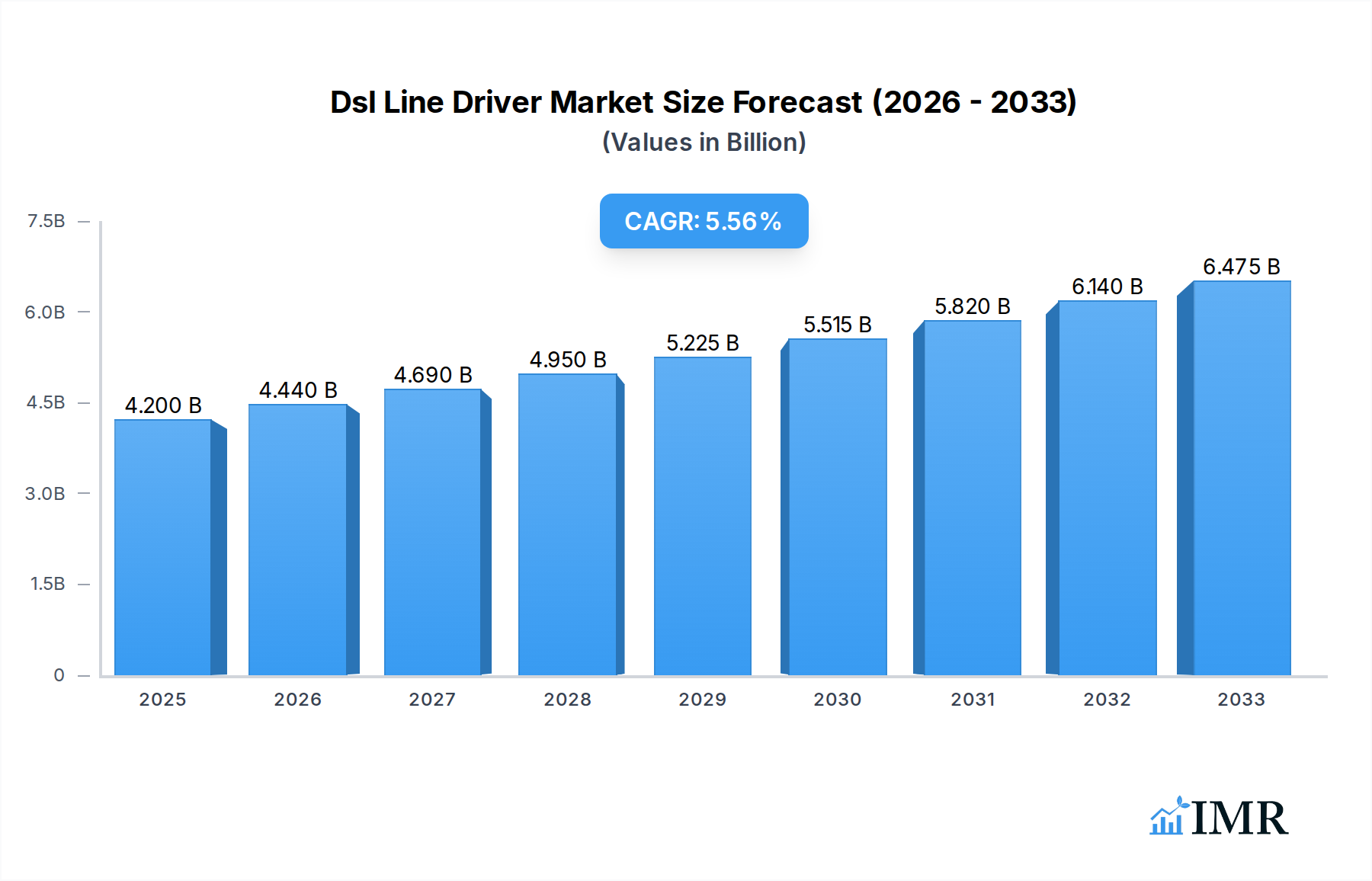

The global DSL Line Driver market is poised for significant expansion, projected to reach an estimated $4.2 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 5.5% anticipated through 2033. This growth trajectory is fueled by the increasing demand for high-speed internet connectivity across various industrial sectors, particularly in mechanical engineering, automotive, and the rapidly evolving aerospace industry. While the traditional residential broadband market is seeing a shift towards fiber optics, DSL technology continues to hold relevance and see upgrades, especially in industrial automation and specialized communication systems. The automotive sector's embrace of advanced driver-assistance systems (ADAS) and in-car infotainment also necessitates reliable, high-bandwidth communication, where DSL line drivers play a crucial role in ensuring signal integrity and data transmission efficiency. Furthermore, the oil and gas industry's need for remote monitoring and control in challenging environments, along with the stringent requirements of chemical industrial processes, are creating sustained demand. Emerging applications in medical devices for remote diagnostics and treatment, and in the electrical sector for smart grid infrastructure, are further bolstering market prospects.

Dsl Line Driver Market Size (In Billion)

Despite the overall positive outlook, the DSL Line Driver market faces certain headwinds. The primary restraint stems from the ongoing migration towards fiber-optic networks for residential and commercial broadband services, which offer superior bandwidth and lower latency. This competition necessitates a focus on niche industrial applications where DSL's existing infrastructure and specific performance characteristics offer distinct advantages. Additionally, the development of alternative communication technologies, such as 5G wireless for certain applications, poses a potential challenge. However, the resilience of DSL line drivers in specialized industrial settings, coupled with ongoing innovation in improving their performance and integration capabilities with existing infrastructure, are expected to mitigate these restraints. The market is also experiencing a trend towards miniaturization and increased power efficiency in DSL line driver components, catering to the evolving needs of compact electronic devices and energy-conscious industrial operations. Key market players like Texas Instruments, Microchip Technology Inc., and Analog Devices are at the forefront of developing advanced solutions to address these evolving demands and maintain market relevance.

Dsl Line Driver Company Market Share

Dsl Line Driver Market Dynamics & Structure

The DSL line driver market, a critical component for enabling high-speed data transmission over copper lines, exhibits a moderately concentrated structure with key players like Texas Instruments, Microchip Technology Inc., and Analog Devices dominating technological innovation and production. This concentration is driven by the significant R&D investments required for developing advanced DSL technologies like VDSL and its successors. Technological innovation remains a primary driver, with continuous advancements in signal processing, noise reduction, and power efficiency aimed at extending DSL reach and speed, even as fiber optic technologies gain traction. Regulatory frameworks, particularly those mandating broadband deployment and defining technical standards for DSL equipment, play a crucial role in shaping market access and product development. However, the increasing availability and adoption of competitive product substitutes such as fiber-to-the-home (FTTH) present a substantial challenge, impacting long-term growth prospects for pure DSL solutions.

- Market Concentration: Dominated by a few key players, indicating high entry barriers and significant R&D investment requirements.

- Technological Innovation Drivers: Focus on speed, reach extension, power efficiency, and integration of advanced signal processing for improved performance.

- Regulatory Frameworks: Influenced by government policies on broadband access, infrastructure deployment, and technical compliance standards.

- Competitive Product Substitutes: Growing threat from fiber optic technologies (FTTH) impacting market share and future demand for DSL.

- End-User Demographics: Diverse, ranging from telecommunications operators requiring robust infrastructure to industrial automation requiring reliable on-site communication.

- M&A Trends: Acquisitions focused on consolidating technological expertise and expanding product portfolios to address evolving connectivity needs.

Dsl Line Driver Growth Trends & Insights

The DSL line driver market is poised for a transformative period between 2019 and 2033, with the base year of 2025 serving as a critical benchmark for understanding current market size and immediate growth trajectories. The global DSL line driver market size is projected to reach USD 5.6 billion in 2025, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 3.2% during the forecast period of 2025–2033. This growth, while moderate, is sustained by the persistent need for reliable and cost-effective broadband connectivity, particularly in regions where fiber optic infrastructure deployment is economically challenging or technologically complex. Adoption rates for advanced DSL technologies, such as Very-high-bit-rate Digital Subscriber Line (VDSL) and its iterations like VDSL2, continue to be strong, driven by telecommunication companies upgrading their existing copper networks to offer higher bandwidth services without the complete overhaul required for fiber.

Technological disruptions are a constant factor, with ongoing research and development aimed at maximizing the capabilities of existing copper infrastructure. Innovations in DSL line driver technology focus on enhanced noise immunity, extended reach capabilities, and improved power management, enabling higher data rates and more stable connections over longer distances. Consumer behavior shifts, while generally favoring fiber, are also influenced by the perceived cost-effectiveness and the ubiquity of existing copper networks. Many consumers and businesses are content with the speeds offered by upgraded DSL services, especially when bundled with other telecommunications packages.

The historical period from 2019 to 2024 has seen a gradual but steady increase in market size, fueled by initial ADSL deployments and subsequent upgrades to VDSL. The estimated market size in 2024 was USD 5.4 billion. The adoption of DSL line drivers is also influenced by the increasing demand for bandwidth in industrial applications, such as industrial automation, surveillance systems, and communication within oil and gas facilities, where existing copper cabling often provides a more practical and cost-effective solution than laying new fiber. Market penetration of advanced DSL technologies continues to expand, as providers seek to balance the high capital expenditure of fiber rollouts with the incremental revenue generated by offering faster speeds over existing infrastructure. The estimated market penetration of VDSL technologies, a significant driver for DSL line driver adoption, is expected to reach xx% by 2025. The market dynamics are also influenced by the resilience of DSL in specific niche applications where specialized line drivers are essential for reliable communication, such as in older industrial control systems or in environments with challenging electromagnetic interference. The overall market growth is thus a complex interplay of infrastructure investment, technological evolution, competitive pressures from newer technologies, and the enduring economics of deploying and upgrading existing networks.

Dominant Regions, Countries, or Segments in Dsl Line Driver

The global DSL line driver market's dominance is multifaceted, with significant contributions stemming from various regions, countries, and application segments. Among the Application segments, Electrical applications stand out as a primary growth driver, projected to contribute approximately xx% to the overall market revenue in 2025. This dominance is fueled by the indispensable role of DSL line drivers in powering sophisticated electrical grids, industrial automation systems, and smart metering infrastructure. The need for reliable, high-speed data transmission in these environments, often characterized by extensive existing copper cabling and stringent reliability requirements, makes DSL line drivers a critical component. The Automotive sector also represents a substantial and growing segment, driven by the increasing integration of advanced driver-assistance systems (ADAS) and in-vehicle infotainment, which rely on robust communication networks.

In terms of Type, VDSL technology is the most significant contributor to market growth, accounting for an estimated xx% of the DSL line driver market in 2025. VDSL's ability to deliver significantly higher speeds over shorter copper loops compared to ADSL and SDSL makes it the preferred choice for telecommunication providers upgrading their last-mile networks to meet escalating bandwidth demands. The Electrical application segment, in particular, heavily relies on VDSL drivers for seamless data exchange within smart grid components and industrial control systems.

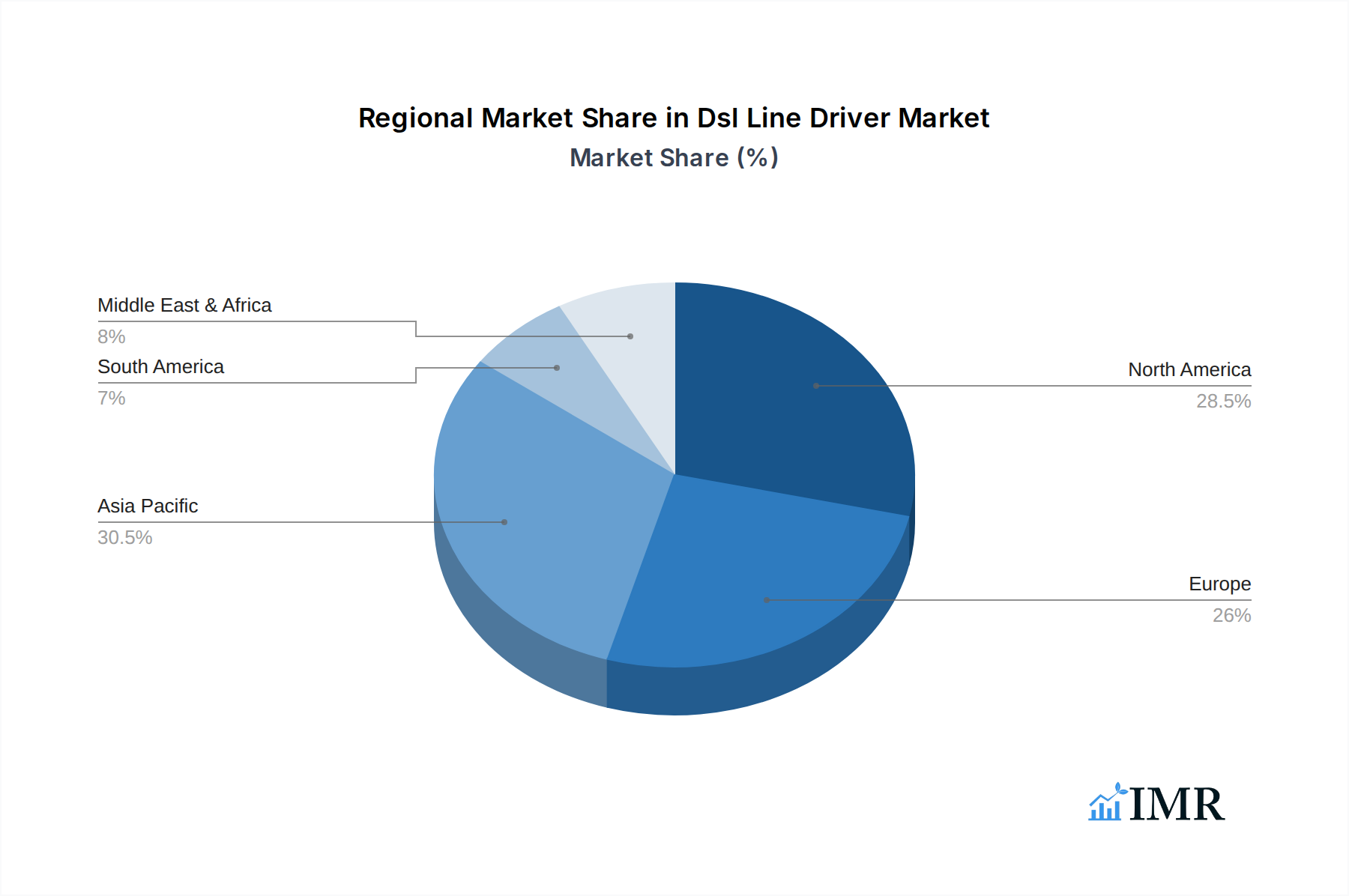

Geographically, Asia Pacific is emerging as a dominant region, driven by rapid industrialization, significant investments in telecommunications infrastructure, and a vast installed base of copper networks. Countries like China, India, and South Korea are leading the adoption of advanced DSL technologies to expand broadband access and support their burgeoning digital economies. The Electrical sector within Asia Pacific, encompassing manufacturing hubs and smart city initiatives, is a key consumer of DSL line drivers. North America and Europe also maintain strong market presence, primarily driven by upgrades to existing infrastructure and the demand for high-speed internet services in the Automotive and Electrical sectors.

- Key Application Drivers:

- Electrical: Essential for smart grids, industrial automation, and advanced control systems requiring reliable data transmission.

- Automotive: Supports ADAS, in-vehicle infotainment, and communication systems with increasing bandwidth needs.

- Oil and Gas: Crucial for communication within remote drilling sites and processing facilities, leveraging existing infrastructure.

- Dominant Type:

- VDSL: Offers superior speeds over copper, driving network upgrades and demand for advanced line drivers.

- Dominant Geographical Regions:

- Asia Pacific: Rapid industrialization, large copper network base, and government initiatives for broadband expansion.

- North America & Europe: Infrastructure upgrades, demand for high-speed internet, and established telecommunication networks.

- Market Share & Growth Potential: The Electrical application segment is expected to hold a market share of approximately xx% by 2025, with a projected CAGR of xx% over the forecast period, reflecting its critical role in modern infrastructure. VDSL technology is anticipated to dominate the DSL line driver market with a xx% share in 2025, growing at a CAGR of xx%.

Dsl Line Driver Product Landscape

The DSL line driver product landscape is characterized by continuous innovation focused on enhancing data transmission performance and compatibility with evolving network standards. Manufacturers are emphasizing the development of integrated solutions that reduce component count and power consumption, critical for deployments in space-constrained and power-sensitive environments. Unique selling propositions often revolve around superior signal integrity, advanced noise cancellation algorithms for extended reach, and robust overvoltage protection to ensure reliability in industrial settings. Technological advancements include the miniaturization of components, improved thermal management, and the integration of diagnostic capabilities for remote monitoring and troubleshooting. Products are increasingly tailored for specific applications, such as high-power drivers for long-loop VDSL deployments or specialized drivers designed for the stringent environmental and electromagnetic interference (EMI) requirements of the Automotive and Oil & Gas industries. The development of multi-line drivers and solutions supporting the latest ITU-T standards underscores the industry's commitment to maximizing the lifespan and performance of copper-based infrastructure.

Key Drivers, Barriers & Challenges in Dsl Line Driver

Key Drivers:

- Ubiquitous Copper Infrastructure: The vast existing network of copper lines provides a cost-effective foundation for DSL services, particularly for upgrades and in areas where fiber deployment is cost-prohibitive.

- Demand for High-Speed Broadband: Increasing consumption of bandwidth for streaming, online gaming, and remote work fuels the need for faster DSL speeds, driving demand for advanced line drivers.

- Industrial Automation & IoT Growth: The proliferation of connected devices and automated systems in sectors like Manufacturing, Oil & Gas, and Electrical necessitates reliable, high-performance communication solutions.

- Cost-Effectiveness of Upgrades: Upgrading existing DSL networks with advanced line drivers is generally less expensive and quicker than a full fiber optic deployment.

- Technological Advancements: Continuous improvements in DSL chipset technology, including signal processing and noise reduction, enable higher data rates and longer reach.

Key Barriers & Challenges:

- Competition from Fiber Optics: Fiber-to-the-home (FTTH) offers significantly higher bandwidth and future-proofing capabilities, posing a major threat to DSL market share.

- Distance Limitations: DSL speeds degrade significantly over longer copper loops, limiting the potential for ultra-high-speed services in certain areas.

- Interference and Noise: Copper lines are susceptible to electromagnetic interference (EMI) and crosstalk, which can degrade signal quality and require sophisticated line driver solutions.

- Regulatory Hurdles and Standards Evolution: Keeping pace with evolving telecommunication standards and securing regulatory approval for new DSL technologies can be complex and time-consuming.

- Infrastructure Degradation: The aging state of some copper networks can necessitate costly repairs or replacements, impacting the overall cost-effectiveness of DSL.

- Supply Chain Volatility: Geopolitical factors and component shortages can disrupt the supply of critical semiconductor components for DSL line drivers, affecting production and pricing.

Emerging Opportunities in Dsl Line Driver

Emerging opportunities in the DSL line driver market lie in niche applications and strategic integration. The continued deployment of smart grids and industrial IoT (IIoT) creates a sustained demand for robust and reliable DSL solutions where fiber deployment is impractical or overly expensive. This includes leveraging DSL line drivers in remote monitoring systems for oil and gas pipelines, within complex manufacturing facilities for real-time control, and for communication infrastructure in challenging geographical terrains. Furthermore, the development of hybrid network solutions, which intelligently combine DSL with other connectivity technologies, presents an opportunity for DSL line drivers to act as critical bridging components. There is also potential in the retrofitting of older industrial equipment with DSL capabilities, extending the lifespan and connectivity of legacy systems. The increasing focus on energy efficiency in industrial and electrical applications also opens avenues for DSL line drivers designed with ultra-low power consumption profiles.

Growth Accelerators in the Dsl Line Driver Industry

Several catalysts are accelerating growth within the DSL line driver industry. Firstly, strategic partnerships between telecommunications equipment manufacturers and semiconductor providers are crucial for co-developing and optimizing DSL solutions that meet evolving market demands. These collaborations foster innovation and ensure that DSL technology remains competitive. Secondly, targeted government initiatives and subsidies aimed at expanding broadband access, especially in rural or underserved areas, directly translate into increased demand for DSL line drivers as a cost-effective last-mile solution. Thirdly, the increasing adoption of VDSL and VDSL2 technologies by major telecommunications operators globally represents a significant growth accelerator, as these standards require more sophisticated and higher-performance line drivers. Finally, the continuous demand for bandwidth in industrial sectors for applications like remote sensing, predictive maintenance, and automation, where existing copper infrastructure is prevalent, acts as a persistent growth engine.

Key Players Shaping the Dsl Line Driver Market

- Texas Instruments

- Microchip Technology Inc.

- Analog Devices

- Renesas

- STMicroelectronics

- Arrow Electronics

- Semtech Corporation

- Advanced Micro Devices

- Virata

- Gartner

- BLACK BOX

- Intersil

- Bourns, Inc

- HIPERFACE DSL

Notable Milestones in Dsl Line Driver Sector

- 2019: Release of next-generation VDSL2 chipsets by key manufacturers, offering improved speed and reach.

- 2020: Increased investment in broadband infrastructure by governments worldwide, boosting demand for DSL upgrades.

- 2021: Launch of new DSL line drivers with enhanced power efficiency and smaller form factors, catering to industrial IoT applications.

- 2022: Significant advancements in signal processing algorithms to combat noise and interference in copper networks.

- 2023: Growing adoption of DSL solutions in the automotive sector for in-vehicle networking and ADAS communication.

- 2024: Increased focus on developing hybrid connectivity solutions that integrate DSL with other wireless and wired technologies.

In-Depth Dsl Line Driver Market Outlook

The future of the DSL line driver market is characterized by its strategic importance in enabling pervasive connectivity and supporting critical industrial applications. While the long-term dominance of fiber optics is undeniable, the DSL line driver market will continue to thrive by catering to segments where fiber deployment is economically or logistically unfeasible. Growth accelerators such as government broadband initiatives, the insatiable demand for industrial automation, and the cost-effectiveness of upgrading existing copper infrastructure will underpin market expansion. Strategic partnerships and continuous technological innovation in areas like signal integrity, power efficiency, and integration with emerging IoT frameworks will be paramount for market players. The market outlook suggests a sustained, albeit evolving, role for DSL line drivers, particularly in industrial, automotive, and essential utility applications, ensuring its continued relevance in the global connectivity landscape.

Dsl Line Driver Segmentation

-

1. Application

- 1.1. Mechanical Engineering

- 1.2. Automotive

- 1.3. Aeronautics

- 1.4. Marine

- 1.5. Oil And Gas

- 1.6. Chemical Industrial

- 1.7. Medical

- 1.8. Electrical

-

2. Type

- 2.1. ADSL

- 2.2. SDSL

- 2.3. VDSL

- 2.4. HDSL

Dsl Line Driver Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Dsl Line Driver Regional Market Share

Geographic Coverage of Dsl Line Driver

Dsl Line Driver REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Mechanical Engineering

- 5.1.2. Automotive

- 5.1.3. Aeronautics

- 5.1.4. Marine

- 5.1.5. Oil And Gas

- 5.1.6. Chemical Industrial

- 5.1.7. Medical

- 5.1.8. Electrical

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. ADSL

- 5.2.2. SDSL

- 5.2.3. VDSL

- 5.2.4. HDSL

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Dsl Line Driver Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Mechanical Engineering

- 6.1.2. Automotive

- 6.1.3. Aeronautics

- 6.1.4. Marine

- 6.1.5. Oil And Gas

- 6.1.6. Chemical Industrial

- 6.1.7. Medical

- 6.1.8. Electrical

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. ADSL

- 6.2.2. SDSL

- 6.2.3. VDSL

- 6.2.4. HDSL

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Dsl Line Driver Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Mechanical Engineering

- 7.1.2. Automotive

- 7.1.3. Aeronautics

- 7.1.4. Marine

- 7.1.5. Oil And Gas

- 7.1.6. Chemical Industrial

- 7.1.7. Medical

- 7.1.8. Electrical

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. ADSL

- 7.2.2. SDSL

- 7.2.3. VDSL

- 7.2.4. HDSL

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Dsl Line Driver Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Mechanical Engineering

- 8.1.2. Automotive

- 8.1.3. Aeronautics

- 8.1.4. Marine

- 8.1.5. Oil And Gas

- 8.1.6. Chemical Industrial

- 8.1.7. Medical

- 8.1.8. Electrical

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. ADSL

- 8.2.2. SDSL

- 8.2.3. VDSL

- 8.2.4. HDSL

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Dsl Line Driver Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Mechanical Engineering

- 9.1.2. Automotive

- 9.1.3. Aeronautics

- 9.1.4. Marine

- 9.1.5. Oil And Gas

- 9.1.6. Chemical Industrial

- 9.1.7. Medical

- 9.1.8. Electrical

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. ADSL

- 9.2.2. SDSL

- 9.2.3. VDSL

- 9.2.4. HDSL

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Dsl Line Driver Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Mechanical Engineering

- 10.1.2. Automotive

- 10.1.3. Aeronautics

- 10.1.4. Marine

- 10.1.5. Oil And Gas

- 10.1.6. Chemical Industrial

- 10.1.7. Medical

- 10.1.8. Electrical

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. ADSL

- 10.2.2. SDSL

- 10.2.3. VDSL

- 10.2.4. HDSL

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Dsl Line Driver Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Mechanical Engineering

- 11.1.2. Automotive

- 11.1.3. Aeronautics

- 11.1.4. Marine

- 11.1.5. Oil And Gas

- 11.1.6. Chemical Industrial

- 11.1.7. Medical

- 11.1.8. Electrical

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. ADSL

- 11.2.2. SDSL

- 11.2.3. VDSL

- 11.2.4. HDSL

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Texas Instruments

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Microchip Technology Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Analog Devices

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Renesas

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 STMicroelectronics

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Arrow Electronics

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Semtech Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Advanced Micro Devices

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Virata

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Gartner

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 BLACK BOX

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Intersil

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Bourns Inc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 HIPERFACE DSL

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Texas Instruments

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Dsl Line Driver Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Dsl Line Driver Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Dsl Line Driver Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Dsl Line Driver Volume (K), by Application 2025 & 2033

- Figure 5: North America Dsl Line Driver Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Dsl Line Driver Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Dsl Line Driver Revenue (undefined), by Type 2025 & 2033

- Figure 8: North America Dsl Line Driver Volume (K), by Type 2025 & 2033

- Figure 9: North America Dsl Line Driver Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Dsl Line Driver Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Dsl Line Driver Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Dsl Line Driver Volume (K), by Country 2025 & 2033

- Figure 13: North America Dsl Line Driver Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Dsl Line Driver Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Dsl Line Driver Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Dsl Line Driver Volume (K), by Application 2025 & 2033

- Figure 17: South America Dsl Line Driver Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Dsl Line Driver Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Dsl Line Driver Revenue (undefined), by Type 2025 & 2033

- Figure 20: South America Dsl Line Driver Volume (K), by Type 2025 & 2033

- Figure 21: South America Dsl Line Driver Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Dsl Line Driver Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Dsl Line Driver Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Dsl Line Driver Volume (K), by Country 2025 & 2033

- Figure 25: South America Dsl Line Driver Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Dsl Line Driver Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Dsl Line Driver Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Dsl Line Driver Volume (K), by Application 2025 & 2033

- Figure 29: Europe Dsl Line Driver Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Dsl Line Driver Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Dsl Line Driver Revenue (undefined), by Type 2025 & 2033

- Figure 32: Europe Dsl Line Driver Volume (K), by Type 2025 & 2033

- Figure 33: Europe Dsl Line Driver Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Dsl Line Driver Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Dsl Line Driver Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Dsl Line Driver Volume (K), by Country 2025 & 2033

- Figure 37: Europe Dsl Line Driver Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Dsl Line Driver Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Dsl Line Driver Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Dsl Line Driver Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Dsl Line Driver Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Dsl Line Driver Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Dsl Line Driver Revenue (undefined), by Type 2025 & 2033

- Figure 44: Middle East & Africa Dsl Line Driver Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Dsl Line Driver Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Dsl Line Driver Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Dsl Line Driver Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Dsl Line Driver Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Dsl Line Driver Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Dsl Line Driver Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Dsl Line Driver Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Dsl Line Driver Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Dsl Line Driver Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Dsl Line Driver Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Dsl Line Driver Revenue (undefined), by Type 2025 & 2033

- Figure 56: Asia Pacific Dsl Line Driver Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Dsl Line Driver Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Dsl Line Driver Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Dsl Line Driver Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Dsl Line Driver Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Dsl Line Driver Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Dsl Line Driver Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Dsl Line Driver Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Dsl Line Driver Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Dsl Line Driver Revenue undefined Forecast, by Type 2020 & 2033

- Table 4: Global Dsl Line Driver Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Dsl Line Driver Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Dsl Line Driver Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Dsl Line Driver Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Dsl Line Driver Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Dsl Line Driver Revenue undefined Forecast, by Type 2020 & 2033

- Table 10: Global Dsl Line Driver Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Dsl Line Driver Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Dsl Line Driver Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Dsl Line Driver Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Dsl Line Driver Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Dsl Line Driver Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: Global Dsl Line Driver Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Dsl Line Driver Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Dsl Line Driver Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Dsl Line Driver Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Dsl Line Driver Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Dsl Line Driver Revenue undefined Forecast, by Type 2020 & 2033

- Table 34: Global Dsl Line Driver Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Dsl Line Driver Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Dsl Line Driver Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Dsl Line Driver Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Dsl Line Driver Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Dsl Line Driver Revenue undefined Forecast, by Type 2020 & 2033

- Table 58: Global Dsl Line Driver Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Dsl Line Driver Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Dsl Line Driver Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Dsl Line Driver Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Dsl Line Driver Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Dsl Line Driver Revenue undefined Forecast, by Type 2020 & 2033

- Table 76: Global Dsl Line Driver Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Dsl Line Driver Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Dsl Line Driver Volume K Forecast, by Country 2020 & 2033

- Table 79: China Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Dsl Line Driver Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Dsl Line Driver Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Dsl Line Driver?

The projected CAGR is approximately 5.5%.

2. Which companies are prominent players in the Dsl Line Driver?

Key companies in the market include Texas Instruments, Microchip Technology Inc, Analog Devices, Renesas, STMicroelectronics, Arrow Electronics, Semtech Corporation, Advanced Micro Devices, Virata, Gartner, BLACK BOX, Intersil, Bourns, Inc, HIPERFACE DSL.

3. What are the main segments of the Dsl Line Driver?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Dsl Line Driver," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Dsl Line Driver report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Dsl Line Driver?

To stay informed about further developments, trends, and reports in the Dsl Line Driver, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence