Key Insights

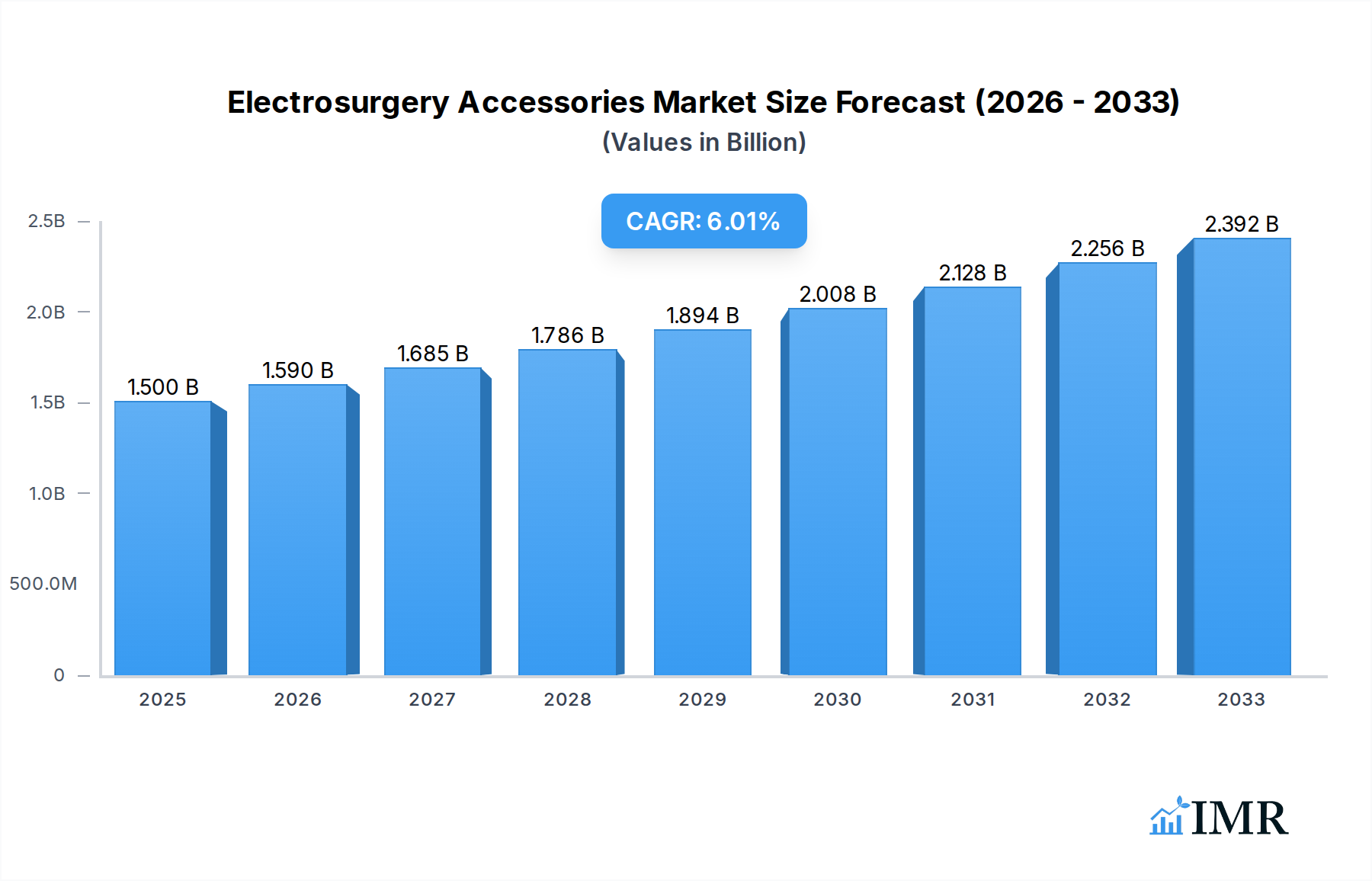

The global electrosurgery accessories market is poised for significant expansion, with an estimated market size of $1.5 billion in 2025, projected to grow at a robust CAGR of 6% through 2033. This sustained growth is primarily fueled by the increasing prevalence of chronic diseases, a rising number of minimally invasive surgical procedures, and advancements in electrosurgical technology offering enhanced precision and patient safety. The orthopedic and cosmetic surgery segments are expected to be key contributors, driven by an aging global population and a growing demand for aesthetic enhancements. Furthermore, the increasing adoption of bipolar instruments over monopolar ones, owing to their reduced risk of tissue charring and improved hemostasis, will also propel market dynamics.

Electrosurgery Accessories Market Size (In Billion)

The market is also witnessing a surge in demand for integrated solutions that enhance surgical efficiency and patient outcomes. Innovations in argon and smoke management systems are crucial as surgical smoke has been identified as a potential health hazard to both patients and surgical staff. Major market players are actively investing in research and development to introduce novel accessories and upgrade existing product lines, further stimulating market growth. While the market benefits from technological advancements and increasing surgical volumes, factors such as the high initial cost of advanced electrosurgical units and the need for specialized training may present some challenges. Nevertheless, the overarching trend towards less invasive surgeries and improved patient care strongly supports a positive trajectory for the electrosurgery accessories market.

Electrosurgery Accessories Company Market Share

Electrosurgery Accessories Market Dynamics & Structure

The global electrosurgery accessories market is characterized by moderate to high concentration, with a few dominant players like Medtronic PLC, Olympus Corporation, and Conmed Corporation holding significant market share. Technological innovation remains a primary driver, with ongoing advancements in bipolar and monopolar instruments, argon plasma coagulation systems, and smoke management solutions enhancing surgical precision and patient safety. Stringent regulatory frameworks governing medical devices, such as FDA approvals and CE marking, influence product development and market entry, ensuring adherence to high safety and efficacy standards. Competitive product substitutes include traditional surgical tools and emerging energy-based devices, necessitating continuous innovation from electrosurgery accessory manufacturers. End-user demographics are shifting towards an aging global population and increasing prevalence of chronic diseases, driving demand for minimally invasive procedures where electrosurgery plays a crucial role. Mergers and acquisitions (M&A) are a notable trend, as larger companies acquire smaller, innovative firms to expand their product portfolios and market reach. For example, the period between 2019 and 2024 saw an estimated 25 major M&A deals in the broader surgical device sector, with a significant portion impacting electrosurgery. Innovation barriers include the high cost of research and development, the need for extensive clinical trials, and the complex regulatory approval processes.

- Market Concentration: Dominated by key players, with an estimated 60% market share held by the top 5 companies.

- Technological Innovation: Driven by demand for enhanced precision, reduced tissue damage, and improved patient outcomes.

- Regulatory Frameworks: Strict adherence to global medical device regulations (e.g., FDA, CE) ensures product quality and safety.

- Competitive Substitutes: Traditional surgical instruments and alternative energy-based technologies present ongoing competition.

- End-User Demographics: Aging population and rising chronic disease rates fuel demand for electrosurgical procedures.

- M&A Trends: Strategic acquisitions are common for portfolio expansion and market consolidation.

Electrosurgery Accessories Growth Trends & Insights

The global electrosurgery accessories market is poised for robust growth, projected to expand significantly from its base year value of approximately $12.5 billion in 2025. This expansion is driven by a confluence of factors including the increasing adoption of minimally invasive surgical techniques across various medical specialties and advancements in electrosurgical technology. The market is expected to witness a Compound Annual Growth Rate (CAGR) of approximately 7.2% between 2025 and 2033. Adoption rates for advanced electrosurgical accessories, particularly bipolar and monopolar instruments designed for greater precision and reduced collateral damage, are accelerating. This trend is further fueled by the growing preference for faster patient recovery times and reduced hospital stays, which minimally invasive procedures, often utilizing electrosurgery, facilitate.

Technological disruptions are continuously shaping the market. Innovations such as integrated electrosurgical generators with advanced waveform capabilities, sophisticated instrument designs for delicate tissue manipulation, and sophisticated smoke evacuation systems are enhancing surgical efficacy and safety. The integration of artificial intelligence and robotics in surgical procedures also presents a future opportunity for electrosurgery accessories, enabling more precise control and real-time feedback during operations. Consumer behavior shifts are playing a vital role, with healthcare providers and surgeons increasingly prioritizing devices that offer superior performance, cost-effectiveness, and improved patient outcomes. The global health expenditure, estimated to be over $9.9 trillion in 2023, indicates a substantial investment in healthcare technologies, including electrosurgery.

The pediatric segment, while smaller, is also showing increased demand due to the rise in congenital defect surgeries. The cosmetic surgery segment, driven by increasing aesthetic consciousness globally, is a significant contributor to market growth, with procedures like liposuction and facial rejuvenation often employing electrosurgical devices. Gynecology is another key application area, where electrosurgery is widely used for procedures such as myomectomy and hysterectomy. The market penetration of advanced electrosurgery units is high in developed economies, but significant growth potential exists in emerging markets as healthcare infrastructure improves and access to advanced medical technologies expands. The total addressable market for surgical energy devices, of which electrosurgery accessories are a critical component, is projected to reach over $25 billion by 2030.

Dominant Regions, Countries, or Segments in Electrosurgery Accessories

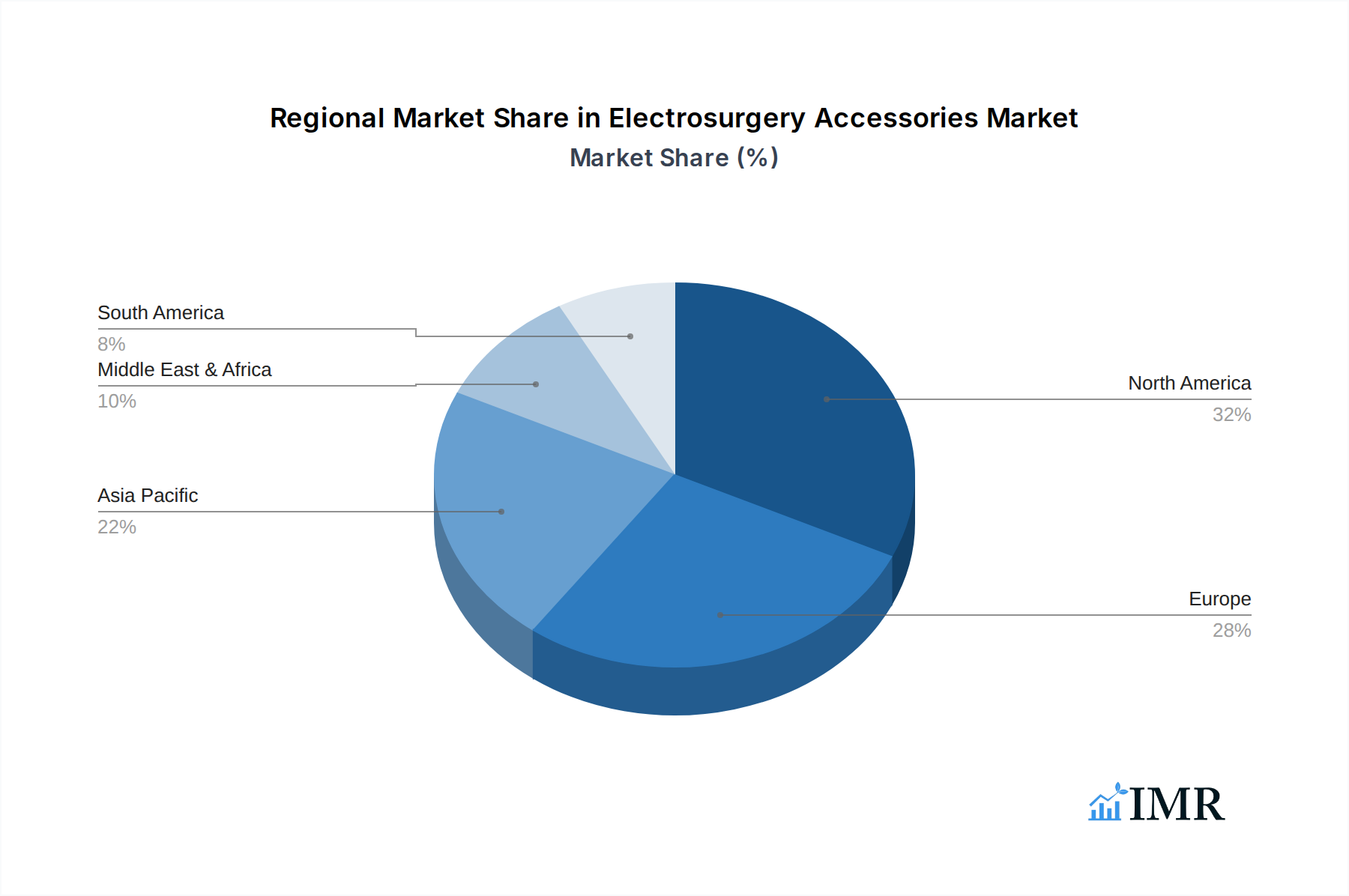

The North America region is currently the dominant force in the global electrosurgery accessories market, driven by a combination of strong healthcare infrastructure, high adoption rates of advanced medical technologies, and a significant patient pool seeking minimally invasive procedures. The United States, within North America, represents a substantial portion of this dominance, accounting for an estimated 45% of the regional market share. This leadership is bolstered by robust government funding for healthcare research and development, a favorable reimbursement landscape for surgical procedures, and a high concentration of leading medical device manufacturers and renowned surgical centers.

Within the Application segment, Orthopedic procedures are a primary growth driver, due to the increasing incidence of orthopedic conditions like arthritis and sports injuries, necessitating surgical interventions. The growing preference for arthroscopic surgery, which heavily relies on precise electrosurgical instruments for tissue dissection and ablation, further propels the demand in this segment. The orthopedic segment is estimated to contribute over 30% to the overall electrosurgery accessories market revenue.

In terms of Types, Instruments-Bipolar & Monopolar are the most significant contributors to market growth. Bipolar instruments, offering enhanced safety and precision for delicate tissues, are witnessing particularly strong demand in neurosurgery, cardiac surgery, and microsurgery. Monopolar instruments continue to be widely used for their versatility and cost-effectiveness in a broad range of general surgical applications. The market share for instruments is estimated to be around 55% of the total electrosurgery accessories market.

- Regional Dominance: North America, led by the United States, due to advanced healthcare infrastructure and high technology adoption.

- Key Country: United States, holding approximately 45% of the North American market share.

- Dominant Application: Orthopedic procedures, driven by the rise in minimally invasive surgery for injuries and degenerative conditions.

- Dominant Type: Instruments-Bipolar & Monopolar, crucial for precise tissue manipulation in diverse surgical settings.

- Growth Drivers: Economic policies favoring healthcare spending, advanced medical infrastructure, and patient preference for minimally invasive treatments.

- Market Share: Instruments-Bipolar & Monopolar estimated at 55% of the total electrosurgery accessories market.

Electrosurgery Accessories Product Landscape

The electrosurgery accessories product landscape is continuously evolving with a focus on miniaturization, enhanced precision, and integrated functionalities. Innovations in bipolar and monopolar instruments include designs with improved insulation, specialized tip geometries for various tissue types, and integrated suction capabilities. Argon and smoke management systems are becoming more sophisticated, offering advanced filtration to improve operating room air quality and enhanced control for effective lesion management. Products are increasingly designed for specific surgical applications, such as specialized instruments for delicate neurosurgical dissections or robust tools for orthopedic bone cutting. Unique selling propositions include reduced thermal spread, faster tissue coagulation, and improved surgeon ergonomics. Technological advancements are integrating real-time feedback mechanisms and data logging capabilities into some higher-end accessories.

Key Drivers, Barriers & Challenges in Electrosurgery Accessories

Key Drivers:

- Rising demand for minimally invasive surgery (MIS): MIS procedures are preferred for faster recovery and reduced scarring, directly increasing the need for electrosurgery accessories.

- Technological advancements: Development of more precise, safer, and versatile electrosurgical devices, including bipolar and monopolar instruments, argon systems, and smoke management solutions.

- Growing prevalence of chronic diseases and aging population: These demographics often require surgical interventions where electrosurgery is a common modality.

- Increasing healthcare expenditure globally: Greater investment in advanced medical technologies and surgical procedures.

Barriers & Challenges:

- High cost of advanced electrosurgery accessories: Can limit adoption in resource-constrained settings.

- Stringent regulatory approval processes: Lengthy and expensive procedures for new product introductions.

- Risk of surgical complications: Though minimized by modern accessories, potential for burns or nerve damage remains a concern.

- Competition from alternative energy sources: Emerging technologies may offer comparable or superior outcomes for specific applications.

- Supply chain disruptions: Global events can impact the availability and cost of raw materials and finished products, estimated to have caused a 5-10% increase in production costs in 2022-2023.

Emerging Opportunities in Electrosurgery Accessories

Emerging opportunities in the electrosurgery accessories market lie in the development of intelligent, connected devices that integrate with robotic surgical platforms and AI-driven diagnostic tools. There is a growing demand for single-use, sterile accessories to mitigate infection risks and simplify sterilization processes, particularly in outpatient surgical centers. Furthermore, the untapped potential in emerging economies, where healthcare infrastructure is rapidly developing, presents a significant avenue for market expansion. Innovative applications in specialized fields such as reconstructive surgery and interventional radiology are also gaining traction. The trend towards personalized medicine also opens doors for accessories tailored to specific patient anatomies or genetic predispositions.

Growth Accelerators in the Electrosurgery Accessories Industry

Long-term growth in the electrosurgery accessories industry is being accelerated by several key catalysts. Significant technological breakthroughs, such as the development of advanced bipolar energy devices with unparalleled precision and tissue selectivity, are enhancing surgical outcomes. Strategic partnerships between electrosurgical device manufacturers and leading hospitals or research institutions foster innovation and accelerate the translation of new technologies from lab to clinic. Market expansion strategies, including entering emerging markets with tailored product offerings and affordable pricing models, are also crucial for sustained growth. The increasing focus on value-based healthcare is driving the adoption of electrosurgery accessories that demonstrably improve patient outcomes while reducing overall healthcare costs.

Key Players Shaping the Electrosurgery Accessories Market

- Medtronic PLC

- Olympus Corporation

- Conmed Corporation

- B. Braun Melsungen AG

- Johnson & Johnson

- Bovie Medical Corporation

- Erbe Elektromedizin GmbH

- Applied Medical Resources Corporation

- Megadyne Medical Products, Inc.

- Bowa-Electronic GmbH & Co. Kg

Notable Milestones in Electrosurgery Accessories Sector

- 2019: Olympus Corporation launches a new generation of advanced bipolar instruments for minimally invasive surgery.

- 2020: Medtronic PLC expands its electrosurgical portfolio with the acquisition of a leading smoke management system manufacturer.

- 2021: Erbe Elektromedizin GmbH introduces an enhanced argon plasma coagulation system with improved safety features.

- 2022: Conmed Corporation unveils a novel monopolar instrument designed for enhanced precision in delicate tissue dissection.

- 2023: Bovie Medical Corporation receives FDA clearance for an innovative disposable electrosurgical electrode.

- 2024 (Q1): B. Braun Melsungen AG announces a strategic partnership to develop next-generation electrosurgery generators.

In-Depth Electrosurgery Accessories Market Outlook

The future outlook for the electrosurgery accessories market is exceptionally bright, driven by persistent demand for advanced surgical technologies and the ongoing expansion of minimally invasive procedures. Growth accelerators, including continuous innovation in bipolar and monopolar instruments, sophisticated argon and smoke management systems, and the integration of AI in surgical tools, will fuel market expansion. Strategic partnerships and the increasing focus on emerging markets present significant opportunities for revenue growth. The market is projected to continue its upward trajectory, driven by an aging global population, the rising incidence of chronic diseases, and a universal pursuit of improved patient outcomes and efficient healthcare delivery. This sustained growth will be underpinned by the industry's commitment to technological advancement and adapting to evolving global healthcare needs.

Electrosurgery Accessories Segmentation

-

1. Application

- 1.1. Orthopedic

- 1.2. Cosmetic

- 1.3. Gynecology

-

2. Types

- 2.1. Generators

- 2.2. Instruments-Bipolar & Monopolar

- 2.3. Argon & Smoke Management Systems

Electrosurgery Accessories Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Electrosurgery Accessories Regional Market Share

Geographic Coverage of Electrosurgery Accessories

Electrosurgery Accessories REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Electrosurgery Accessories Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Orthopedic

- 5.1.2. Cosmetic

- 5.1.3. Gynecology

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Generators

- 5.2.2. Instruments-Bipolar & Monopolar

- 5.2.3. Argon & Smoke Management Systems

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Electrosurgery Accessories Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Orthopedic

- 6.1.2. Cosmetic

- 6.1.3. Gynecology

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Generators

- 6.2.2. Instruments-Bipolar & Monopolar

- 6.2.3. Argon & Smoke Management Systems

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Electrosurgery Accessories Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Orthopedic

- 7.1.2. Cosmetic

- 7.1.3. Gynecology

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Generators

- 7.2.2. Instruments-Bipolar & Monopolar

- 7.2.3. Argon & Smoke Management Systems

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Electrosurgery Accessories Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Orthopedic

- 8.1.2. Cosmetic

- 8.1.3. Gynecology

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Generators

- 8.2.2. Instruments-Bipolar & Monopolar

- 8.2.3. Argon & Smoke Management Systems

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Electrosurgery Accessories Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Orthopedic

- 9.1.2. Cosmetic

- 9.1.3. Gynecology

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Generators

- 9.2.2. Instruments-Bipolar & Monopolar

- 9.2.3. Argon & Smoke Management Systems

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Electrosurgery Accessories Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Orthopedic

- 10.1.2. Cosmetic

- 10.1.3. Gynecology

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Generators

- 10.2.2. Instruments-Bipolar & Monopolar

- 10.2.3. Argon & Smoke Management Systems

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Medtronic PLC

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Olympus Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Conmed Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 B. Braun Melsungen AG

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Johnson & Johnson

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Bovie Medical Corporation

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Erbe Elektromedizin GmbH

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Applied Medical Resources Corporation

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Megadyne Medical Products

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Inc.

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Bowa-Electronic GmbH & Co. Kg

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Medtronic PLC

List of Figures

- Figure 1: Global Electrosurgery Accessories Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Electrosurgery Accessories Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Electrosurgery Accessories Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Electrosurgery Accessories Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Electrosurgery Accessories Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Electrosurgery Accessories Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Electrosurgery Accessories Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Electrosurgery Accessories Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Electrosurgery Accessories Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Electrosurgery Accessories Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Electrosurgery Accessories Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Electrosurgery Accessories Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Electrosurgery Accessories Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Electrosurgery Accessories Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Electrosurgery Accessories Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Electrosurgery Accessories Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Electrosurgery Accessories Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Electrosurgery Accessories Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Electrosurgery Accessories Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Electrosurgery Accessories Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Electrosurgery Accessories Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Electrosurgery Accessories Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Electrosurgery Accessories Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Electrosurgery Accessories Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Electrosurgery Accessories Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Electrosurgery Accessories Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Electrosurgery Accessories Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Electrosurgery Accessories Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Electrosurgery Accessories Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Electrosurgery Accessories Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Electrosurgery Accessories Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Electrosurgery Accessories Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Electrosurgery Accessories Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Electrosurgery Accessories Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Electrosurgery Accessories Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Electrosurgery Accessories Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Electrosurgery Accessories Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Electrosurgery Accessories Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Electrosurgery Accessories Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Electrosurgery Accessories Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Electrosurgery Accessories Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Electrosurgery Accessories Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Electrosurgery Accessories Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Electrosurgery Accessories Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Electrosurgery Accessories Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Electrosurgery Accessories Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Electrosurgery Accessories Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Electrosurgery Accessories Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Electrosurgery Accessories Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Electrosurgery Accessories Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Electrosurgery Accessories?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Electrosurgery Accessories?

Key companies in the market include Medtronic PLC, Olympus Corporation, Conmed Corporation, B. Braun Melsungen AG, Johnson & Johnson, Bovie Medical Corporation, Erbe Elektromedizin GmbH, Applied Medical Resources Corporation, Megadyne Medical Products, Inc., Bowa-Electronic GmbH & Co. Kg.

3. What are the main segments of the Electrosurgery Accessories?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Electrosurgery Accessories," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Electrosurgery Accessories report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Electrosurgery Accessories?

To stay informed about further developments, trends, and reports in the Electrosurgery Accessories, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence