Key Insights

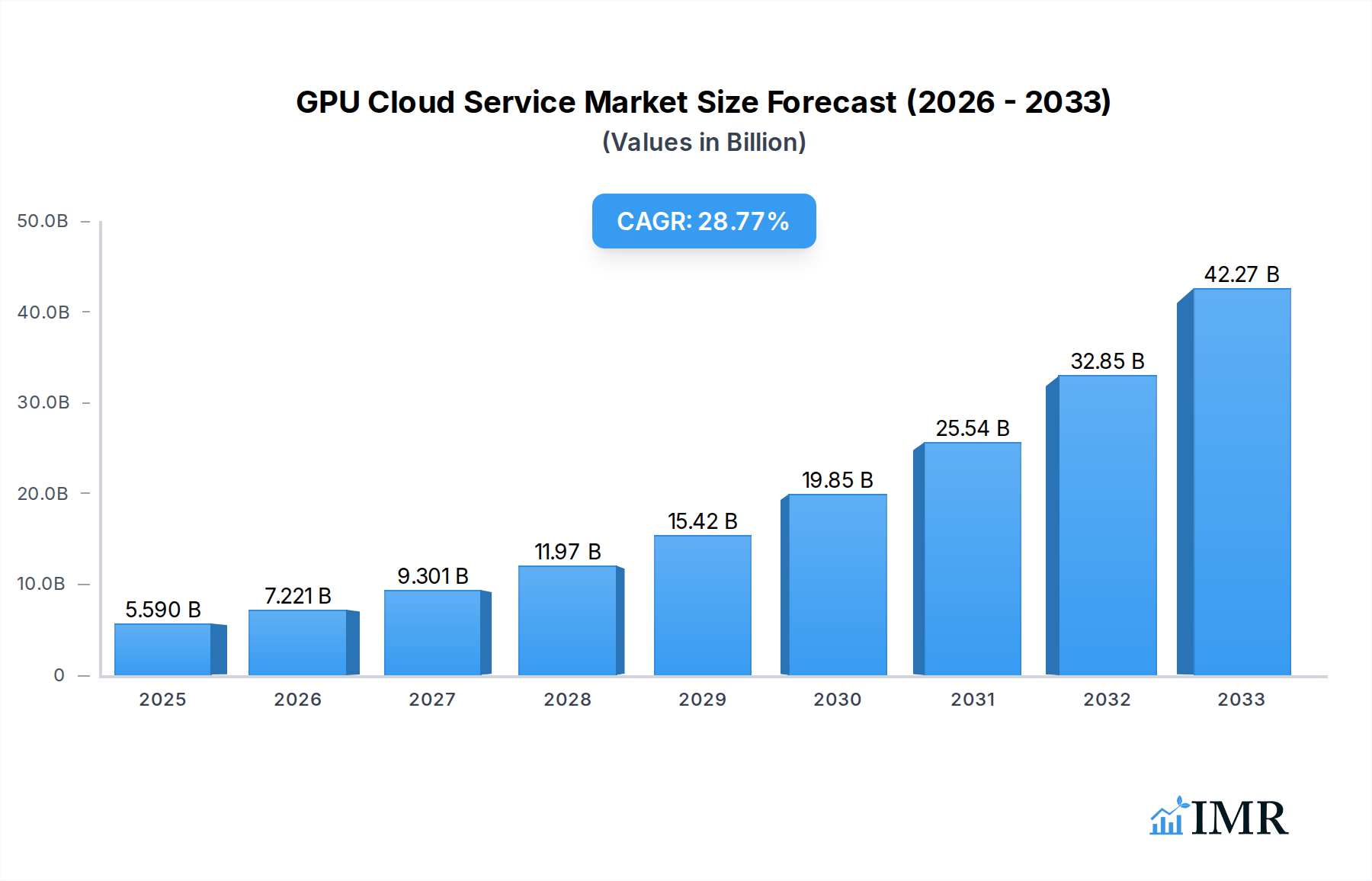

The global GPU Cloud Service market is poised for remarkable expansion, projected to reach $5.59 billion in 2025, driven by an explosive CAGR of 29.42%. This significant growth is fueled by the escalating demand for high-performance computing across diverse applications. Scientific computing, particularly in fields like climate modeling, drug discovery, and complex simulations, is a primary catalyst. The burgeoning advancements in Artificial Intelligence (AI) and Machine Learning (ML), especially in deep learning, are heavily reliant on the parallel processing power offered by GPUs, creating a substantial demand for cloud-based GPU infrastructure. Furthermore, the increasing need for sophisticated visual processing in areas such as gaming, virtual reality (VR), augmented reality (AR), and professional content creation—including rendering complex visual effects and architectural walkthroughs—is another key driver. The market's trajectory is also being shaped by the ongoing digital transformation across industries, pushing more organizations towards cloud-native solutions for their computationally intensive workloads.

GPU Cloud Service Market Size (In Billion)

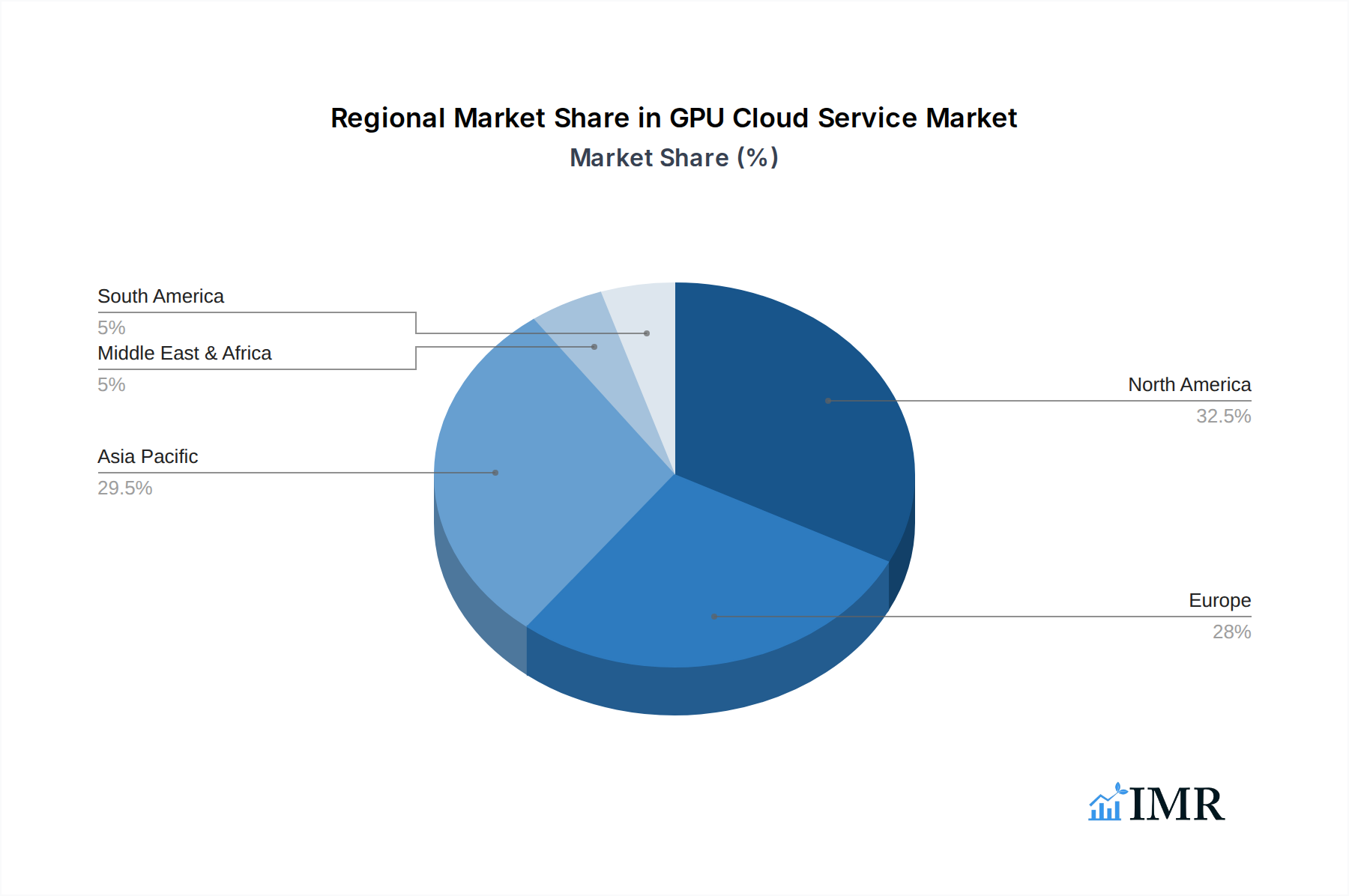

The market segmentation reveals a dynamic landscape. Within applications, Scientific Computing and Deep Learning are anticipated to lead the charge, followed closely by Visual Processing. The "Calculated" and "Rendering Type" segments are expected to see substantial growth, underscoring the demand for raw processing power and specialized visual computation. Leading the charge in this market are tech giants like NVIDIA, a dominant force in GPU hardware and increasingly in cloud offerings, alongside major cloud providers such as Amazon Elastic Compute Cloud, Google Compute Engine, and Microsoft Azure (implied by "IBM Cloud" and "Oracle" as competitors, though Azure is a key player). Emerging players like RockCloud, Genesis Cloud, Paperspace, INSPUR GROUP, and Tencent Cloud Computing are also carving out significant market share, particularly in specific regional or niche applications. Geographically, Asia Pacific, led by China and India, is expected to witness the fastest growth due to rapid digitalization and a burgeoning tech ecosystem. North America and Europe remain mature markets with sustained demand, while emerging economies in other regions present significant untapped potential.

GPU Cloud Service Company Market Share

GPU Cloud Service Market Report: Unlocking the Future of High-Performance Computing

This comprehensive report delves into the dynamic and rapidly expanding GPU Cloud Service market, a critical infrastructure powering advancements in Artificial Intelligence, scientific research, and visual computing. With an estimated global market size projected to reach USD 150 billion by 2025, the sector is experiencing unprecedented growth, driven by escalating demand for raw computational power. Our analysis spans from 2019 to 2033, with a base year of 2025 and a detailed forecast period of 2025–2033, building upon historical data from 2019–2024. This report will equip industry professionals, investors, and strategists with actionable insights into market structure, growth trajectories, regional dominance, product innovations, key challenges, and burgeoning opportunities.

GPU Cloud Service Market Dynamics & Structure

The GPU cloud service market is characterized by a moderately concentrated structure, with a few dominant players like NVIDIA, Amazon Elastic Compute Cloud, and Google Compute Engine (GCE) holding significant market share. Technological innovation serves as the primary driver, with continuous advancements in GPU architectures, parallel processing capabilities, and AI acceleration fueling demand. Regulatory frameworks, while evolving, are largely supportive of cloud adoption, focusing on data security and compliance. Competitive product substitutes include on-premises GPU deployments and specialized hardware, but the scalability and cost-effectiveness of cloud solutions present a compelling advantage. End-user demographics are increasingly diverse, encompassing enterprises across scientific computing, deep learning, and visual processing sectors, as well as individual researchers and developers. Merger and acquisition (M&A) activity is on the rise, with strategic acquisitions aimed at expanding service offerings and market reach. For instance, the historical period saw an average of 15 M&A deals annually in the early years, with this number projected to increase by 25% in the forecast period. Innovation barriers primarily revolve around the significant capital investment required for cutting-edge GPU hardware and the complexity of managing large-scale GPU infrastructure.

- Market Concentration: Dominated by a few hyperscalers, with increasing participation from specialized GPU cloud providers.

- Technological Innovation: Driven by AI advancements, new GPU architectures, and increased demand for parallel processing.

- Regulatory Landscape: Generally supportive, with a growing emphasis on data sovereignty and AI ethics.

- Competitive Landscape: Intense competition from hyperscalers, specialized providers, and on-premises solutions.

- End-User Demographics: Broadening to include scientific research, enterprise AI, media & entertainment, and autonomous systems.

- M&A Trends: Strategic acquisitions focused on talent, technology, and market expansion.

GPU Cloud Service Growth Trends & Insights

The GPU cloud service market is on an explosive growth trajectory, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 35% from 2025 to 2033. This remarkable growth is fueled by the insatiable demand for computational power essential for training and deploying sophisticated deep learning models, accelerating scientific simulations, and enabling real-time visual rendering. By 2025, the global market is anticipated to reach USD 150 billion, a significant leap from historical figures. Adoption rates are soaring across industries, with enterprises increasingly recognizing the agility, scalability, and cost-efficiency of GPU-accelerated cloud services compared to traditional on-premises solutions. Technological disruptions, particularly in the development of more powerful and energy-efficient GPUs, continue to push the boundaries of what is possible. For example, the introduction of new tensor cores and ray-tracing capabilities in GPUs has opened up new application frontiers. Consumer behavior is shifting towards leveraging cloud-based GPU services for tasks that were previously resource-prohibitive, such as complex data analytics, personalized AI services, and high-fidelity virtual reality experiences. The market penetration of GPU cloud services within the broader cloud computing landscape is expected to deepen considerably, moving from approximately 15% in 2023 to an estimated 30% by 2033. This surge is also propelled by the increasing availability of managed GPU cloud platforms, which abstract away the complexities of hardware management, making GPU power accessible to a wider audience. The evolution of AI algorithms and the proliferation of data are creating a virtuous cycle, where the need for more powerful compute drives innovation in GPUs and cloud infrastructure, which in turn enables more advanced AI applications and further data generation. The parent market, encompassing all cloud computing services, is projected to exceed USD 1 trillion by 2028, with GPU cloud services representing a significant and rapidly growing segment within this larger ecosystem. The child markets, such as specialized AI training platforms and rendering farms, are also witnessing exponential growth, directly benefiting from the advancements and accessibility provided by the underlying GPU cloud infrastructure.

Dominant Regions, Countries, or Segments in GPU Cloud Service

The Deep Learning segment, particularly within the Application category, is a primary engine driving the growth of the GPU cloud service market, commanding an estimated 45% market share in 2025. This dominance stems from the exponential rise of Artificial Intelligence and Machine Learning, where the parallel processing capabilities of GPUs are indispensable for training complex neural networks. This segment alone is projected to reach USD 67.5 billion in market value by 2025.

North America, particularly the United States, stands as the dominant region, accounting for approximately 40% of the global GPU cloud service market in 2025. This leadership is attributed to several key factors:

- Hub of Technological Innovation: Silicon Valley and other tech hubs are home to major AI research institutions and leading tech companies, fostering a strong demand for advanced GPU computing.

- Venture Capital Investment: Significant venture capital funding flows into AI and cloud startups, accelerating the adoption of GPU cloud services.

- Strong Enterprise Adoption: Large enterprises across various sectors are heavily investing in AI capabilities, driving the demand for scalable GPU resources.

- Government Initiatives: Supportive policies and funding for AI research and development contribute to market expansion.

Within the Types of GPU cloud services, the Calculated segment, encompassing general-purpose GPU computing for a wide range of applications, represents a significant portion of the market, estimated at 30% in 2025. However, the Rendering Type segment is experiencing rapid growth, driven by advancements in real-time graphics, virtual reality, and high-fidelity visual effects in media and entertainment. This segment is projected to grow at a CAGR of 40% during the forecast period.

The Scientific Computing application, while smaller than Deep Learning, is a crucial and steadily growing segment, accounting for around 25% of the market share in 2025. This includes high-performance computing (HPC) for drug discovery, climate modeling, and physics simulations.

- Deep Learning Dominance:

- Essential for training and inference of AI models.

- Significant growth fueled by advancements in AI algorithms.

- Market size projected to reach USD 67.5 billion by 2025.

- North America's Leadership:

- Concentration of AI talent and research.

- High levels of venture capital investment in cloud and AI.

- Aggressive adoption by enterprises for AI initiatives.

- Calculated Type Segment Strength:

- Versatile for various computational tasks.

- Foundation for many cloud-based applications.

- Rendering Type Growth Acceleration:

- Driven by media, entertainment, and gaming industries.

- Enabling real-time graphics and immersive experiences.

- Scientific Computing's Steady Expansion:

- Crucial for research in fields like medicine, physics, and climate science.

- HPC workloads benefit immensely from GPU acceleration.

GPU Cloud Service Product Landscape

The GPU cloud service product landscape is defined by continuous innovation, with providers like NVIDIA, Google Compute Engine (GCE), and Amazon Elastic Compute Cloud (EC2) offering highly performant and specialized GPU instances. Innovations center on delivering increased processing power through the latest GPU architectures, such as NVIDIA's Hopper and Ampere series, offering enhanced AI acceleration and ray tracing capabilities. These platforms provide on-demand access to powerful GPUs for tasks ranging from complex scientific simulations and large-scale deep learning model training to real-time visual rendering for gaming and virtual reality. Unique selling propositions include specialized instances optimized for specific workloads, integrated AI software stacks, and competitive pricing models. For instance, Paperspace offers specialized GPU configurations for deep learning workflows, while IBM Cloud provides high-performance instances for demanding enterprise applications. Performance metrics such as FLOPS (Floating-point Operations Per Second) and memory bandwidth are continuously improving, enabling users to tackle more computationally intensive problems faster and more efficiently.

Key Drivers, Barriers & Challenges in GPU Cloud Service

The GPU cloud service market is propelled by several key drivers, most notably the exponential growth of Artificial Intelligence and Machine Learning, necessitating immense computational power for training and inference. The increasing demand for high-fidelity visual processing in gaming, media, and augmented/virtual reality also significantly fuels adoption. Furthermore, the accelerating pace of scientific research, particularly in areas like drug discovery and climate modeling, relies heavily on GPU-accelerated simulations.

- Drivers:

- AI/ML Demand: Essential for model training and inference.

- Visual Computing: Driving growth in gaming, VR/AR, and media.

- Scientific Research: Enabling complex simulations in various fields.

- Scalability & Cost-Effectiveness: Cloud solutions offer flexibility and reduced upfront investment.

Key challenges and restraints in the GPU cloud service industry include the significant cost of high-end GPU hardware, which can lead to substantial operational expenses for providers and end-users. Supply chain disruptions for advanced GPUs can impact availability and drive up prices. Regulatory hurdles related to data privacy and AI ethics can create complexity. Furthermore, fierce competition among established hyperscalers and specialized GPU cloud providers, such as RockCloud and Genesis Cloud, intensifies price pressures and demands continuous innovation. The energy consumption of large-scale GPU deployments also presents an environmental and cost challenge.

- Barriers & Challenges:

- High Hardware Costs: Significant capital expenditure for advanced GPUs.

- Supply Chain Volatility: Potential for shortages and price fluctuations.

- Regulatory Compliance: Navigating data privacy and AI ethics.

- Intense Competition: Price wars and the need for constant differentiation.

- Energy Consumption: Environmental and cost implications of large-scale operations.

Emerging Opportunities in GPU Cloud Service

Emerging opportunities in the GPU cloud service sector lie in the burgeoning fields of edge AI, where low-latency inference at the edge requires distributed GPU processing, and the metaverse, which demands massive real-time rendering capabilities. The increasing adoption of hybrid and multi-cloud strategies by enterprises presents an opportunity for providers offering interoperability and seamless management across different cloud environments. Furthermore, the development of specialized GPU instances tailored for specific industry verticals, such as precision medicine or autonomous vehicle development, represents a significant untapped market. The growing interest in sustainable computing is also creating opportunities for providers who can offer energy-efficient GPU solutions.

Growth Accelerators in the GPU Cloud Service Industry

Several catalysts are accelerating long-term growth in the GPU cloud service industry. Technological breakthroughs, such as advancements in AI chip design and the development of more efficient cooling systems, will further reduce costs and increase performance. Strategic partnerships between GPU manufacturers, cloud providers, and software developers are crucial for creating integrated solutions and expanding market reach. For example, collaborations between NVIDIA and major cloud providers have led to the optimization of software stacks for their respective hardware. Market expansion strategies targeting emerging economies and industries that are just beginning to embrace AI and high-performance computing will also drive sustained growth. The increasing availability of pre-trained AI models and readily deployable ML frameworks further lowers the barrier to entry, encouraging wider adoption.

Key Players Shaping the GPU Cloud Service Market

- NVIDIA

- Amazon Elastic Compute Cloud

- Google Compute Engine (GCE)

- IBM Cloud

- Oracle Cloud Infrastructure

- Paperspace

- RockCloud

- Genesis Cloud

- INSPUR GROUP

- Tencent Cloud Computing

- Guangdong Efly Cloud Computing

- Shenzhen Rayvision Technology

- NIUERP

- fastone

- QingCloud Technologies

Notable Milestones in GPU Cloud Service Sector

- 2019: NVIDIA announces its NVIDIA AI Enterprise software suite, optimizing AI development and deployment on cloud platforms.

- 2020: Amazon Web Services (AWS) introduces new GPU-accelerated EC2 instances, enhancing performance for deep learning workloads.

- 2021: Google Cloud expands its GPU offerings with NVIDIA A100 Tensor Core GPUs, supporting cutting-edge AI research.

- 2022: IBM Cloud enhances its Bare Metal servers with next-generation GPUs, catering to high-performance computing demands.

- 2023: Paperspace launches new GPU instances optimized for large language model training and deployment.

- Early 2024: Genesis Cloud announces significant expansion of its GPU compute capacity to meet escalating AI demand.

- Mid-2024: RockCloud introduces specialized GPU clusters for demanding visual processing and rendering tasks.

In-Depth GPU Cloud Service Market Outlook

The future outlook for the GPU cloud service market is exceptionally bright, driven by sustained innovation and widening adoption across diverse industries. Growth accelerators such as the continuous evolution of AI, the expansion of the metaverse, and the increasing need for real-time data processing will ensure robust demand. Strategic partnerships and the development of specialized, industry-specific GPU solutions will unlock new market segments and revenue streams. The industry is poised for significant expansion, with an increasing focus on sustainability and energy efficiency shaping future offerings. The convergence of AI, HPC, and advanced visualization will continue to define the market's trajectory, making GPU cloud services an indispensable component of the global digital economy.

GPU Cloud Service Segmentation

-

1. Application

- 1.1. Scientific Computing

- 1.2. Deep Learning

- 1.3. Visual Processing

-

2. Types

- 2.1. Calculated

- 2.2. Rendering Type

- 2.3. Other

GPU Cloud Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

GPU Cloud Service Regional Market Share

Geographic Coverage of GPU Cloud Service

GPU Cloud Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 29.42% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global GPU Cloud Service Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Scientific Computing

- 5.1.2. Deep Learning

- 5.1.3. Visual Processing

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Calculated

- 5.2.2. Rendering Type

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America GPU Cloud Service Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Scientific Computing

- 6.1.2. Deep Learning

- 6.1.3. Visual Processing

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Calculated

- 6.2.2. Rendering Type

- 6.2.3. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America GPU Cloud Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Scientific Computing

- 7.1.2. Deep Learning

- 7.1.3. Visual Processing

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Calculated

- 7.2.2. Rendering Type

- 7.2.3. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe GPU Cloud Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Scientific Computing

- 8.1.2. Deep Learning

- 8.1.3. Visual Processing

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Calculated

- 8.2.2. Rendering Type

- 8.2.3. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa GPU Cloud Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Scientific Computing

- 9.1.2. Deep Learning

- 9.1.3. Visual Processing

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Calculated

- 9.2.2. Rendering Type

- 9.2.3. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific GPU Cloud Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Scientific Computing

- 10.1.2. Deep Learning

- 10.1.3. Visual Processing

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Calculated

- 10.2.2. Rendering Type

- 10.2.3. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 NVIDIA

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 RockCloud

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Genesis cloud

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 IBM Cloud

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Oracle

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Google compute engine (GCE)

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Paperspace

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Amazon Elastic Compute Cloud

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 INSPUR GROUP

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tencent Cloud Computing

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Guangdong Efly Cloud Computing

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Shenzhen Rayvision Technology

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 NIUERP

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 fastone

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 QingCloud Technologies

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 NVIDIA

List of Figures

- Figure 1: Global GPU Cloud Service Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America GPU Cloud Service Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America GPU Cloud Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America GPU Cloud Service Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America GPU Cloud Service Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America GPU Cloud Service Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America GPU Cloud Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America GPU Cloud Service Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America GPU Cloud Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America GPU Cloud Service Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America GPU Cloud Service Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America GPU Cloud Service Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America GPU Cloud Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe GPU Cloud Service Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe GPU Cloud Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe GPU Cloud Service Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe GPU Cloud Service Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe GPU Cloud Service Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe GPU Cloud Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa GPU Cloud Service Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa GPU Cloud Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa GPU Cloud Service Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa GPU Cloud Service Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa GPU Cloud Service Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa GPU Cloud Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific GPU Cloud Service Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific GPU Cloud Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific GPU Cloud Service Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific GPU Cloud Service Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific GPU Cloud Service Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific GPU Cloud Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global GPU Cloud Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global GPU Cloud Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global GPU Cloud Service Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global GPU Cloud Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global GPU Cloud Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global GPU Cloud Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global GPU Cloud Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global GPU Cloud Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global GPU Cloud Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global GPU Cloud Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global GPU Cloud Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global GPU Cloud Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global GPU Cloud Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global GPU Cloud Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global GPU Cloud Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global GPU Cloud Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global GPU Cloud Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global GPU Cloud Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific GPU Cloud Service Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the GPU Cloud Service?

The projected CAGR is approximately 29.42%.

2. Which companies are prominent players in the GPU Cloud Service?

Key companies in the market include NVIDIA, RockCloud, Genesis cloud, IBM Cloud, Oracle, Google compute engine (GCE), Paperspace, Amazon Elastic Compute Cloud, INSPUR GROUP, Tencent Cloud Computing, Guangdong Efly Cloud Computing, Shenzhen Rayvision Technology, NIUERP, fastone, QingCloud Technologies.

3. What are the main segments of the GPU Cloud Service?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "GPU Cloud Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the GPU Cloud Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the GPU Cloud Service?

To stay informed about further developments, trends, and reports in the GPU Cloud Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence