Key Insights

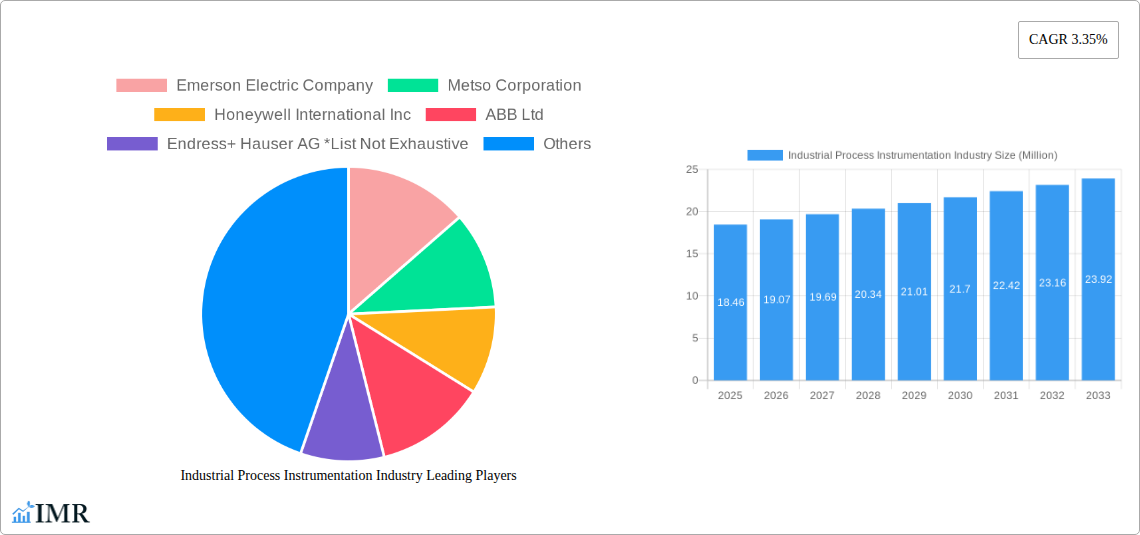

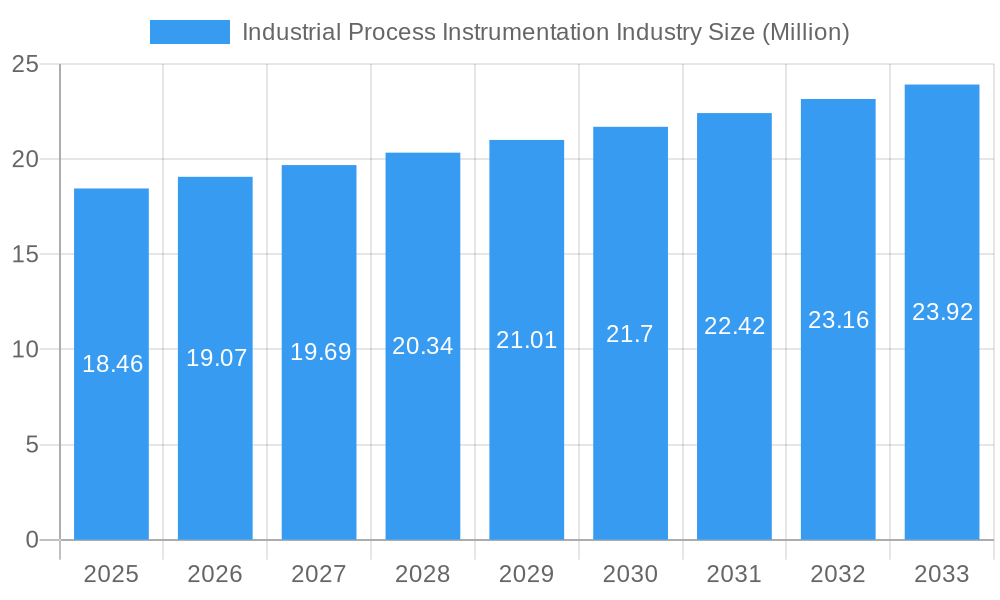

The Industrial Process Instrumentation market is poised for steady growth, projected to reach a substantial USD 18.46 million in value. This expansion is fueled by a Compound Annual Growth Rate (CAGR) of 3.35% over the study period of 2019-2033, with the base and estimated year of 2025 serving as a pivotal point. A primary driver for this growth is the increasing demand for automation and control in complex industrial processes across various sectors. The need for enhanced operational efficiency, stringent quality control, and improved safety standards are compelling industries to invest in sophisticated process instrumentation. Furthermore, the ongoing digital transformation, including the adoption of Industry 4.0 principles and the Industrial Internet of Things (IIoT), is creating new avenues for growth, enabling real-time data analysis and predictive maintenance. Technological advancements in sensor technology, wireless communication, and data analytics are making process instrumentation more intelligent, versatile, and cost-effective, further stimulating market penetration.

Industrial Process Instrumentation Industry Market Size (In Million)

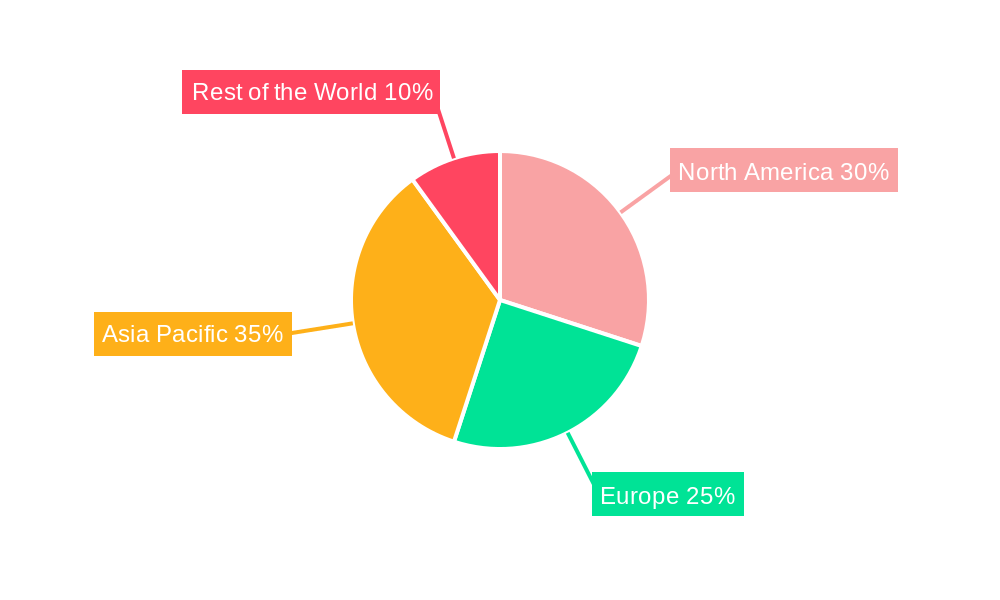

The market is segmented across key instruments such as transmitters and control valves, with technologies like Programmable Logic Controllers (PLCs), Distributed Control Systems (DCS), Supervisory Control and Data Acquisition (SCADA), and Manufacturing Execution Systems (MES) playing crucial roles. These technologies are indispensable for optimizing operations in diverse end-user industries including Water and Wastewater Treatment, Chemical Manufacturing, Energy & Utilities, Oil and Gas Extraction, and Metals and Mining. Geographically, while mature markets like North America and Europe continue to be significant contributors due to established industrial bases and technological adoption, the Asia Pacific region is expected to exhibit the highest growth potential, driven by rapid industrialization, increasing investments in infrastructure, and a burgeoning manufacturing sector. Emerging trends like the focus on sustainability and environmental monitoring are also expected to drive demand for advanced instrumentation solutions, while challenges related to high initial investment costs and the need for skilled workforce integration are anticipated to be managed through technological innovation and industry-specific training programs.

Industrial Process Instrumentation Industry Company Market Share

Unlock critical insights into the global Industrial Process Instrumentation market, a sector vital for optimizing efficiency, safety, and sustainability across diverse industries. This comprehensive report delves into market dynamics, growth trajectories, regional dominance, product innovation, key drivers, challenges, and emerging opportunities. With a detailed analysis spanning the historical period of 2019-2024, a base year of 2025, and a forecast period extending to 2033, this report provides an indispensable resource for stakeholders seeking to navigate and capitalize on the evolving landscape of industrial automation and control.

Industrial Process Instrumentation Industry Market Dynamics & Structure

The Industrial Process Instrumentation industry exhibits a moderately concentrated market structure, with key players like Emerson Electric Company, Metso Corporation, Honeywell International Inc, ABB Ltd, Endress+ Hauser AG, Mitsubishi Electric Corporation, Siemens AG, Danaher Corporation, Omron Corporation, Rockwell Automation Inc, and Yokogawa Electric Corporation holding significant influence. Technological innovation is a primary driver, propelled by the relentless pursuit of enhanced precision, real-time data, and predictive maintenance capabilities. The integration of IoT, AI, and advanced analytics is transforming traditional instrumentation into smart, connected devices. Regulatory frameworks, particularly those pertaining to safety, environmental compliance, and data security, are increasingly shaping product development and market access. Competitive product substitutes, while present in some basic applications, are largely outpaced by the advanced functionalities and integrated solutions offered by established players. End-user demographics are diverse, ranging from large-scale chemical manufacturers to essential water and wastewater treatment facilities, each with unique demands for reliability and performance. Mergers and acquisitions (M&A) trends, though not consistently high in volume, often involve strategic consolidations to acquire new technologies or expand market reach. For instance, a significant M&A activity in the last few years involved companies acquiring smaller, specialized IoT integration firms, indicating a growing trend towards intelligent automation solutions. Barriers to innovation include high research and development costs, long product development cycles, and the need for rigorous testing and certification to meet stringent industry standards.

Industrial Process Instrumentation Industry Growth Trends & Insights

The global Industrial Process Instrumentation market is poised for robust growth, driven by the increasing adoption of Industry 4.0 principles and the burgeoning demand for smart manufacturing solutions. Market size is projected to expand significantly, with a projected Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period. This expansion is underpinned by escalating investments in automation and digitalization across core end-user industries such as Oil and Gas Extraction, Energy & Utilities, and Chemical Manufacturing, which collectively represent a substantial portion of the market share. The adoption rate of advanced instrumentation, including smart transmitters and integrated control systems, is accelerating as businesses recognize their critical role in enhancing operational efficiency, reducing downtime, and improving product quality. Technological disruptions, notably the proliferation of the Industrial Internet of Things (IIoT) and the development of AI-powered analytical tools, are fundamentally reshaping the market. These advancements enable real-time data acquisition, predictive maintenance, and remote monitoring, offering unprecedented levels of control and visibility. Consumer behavior shifts are also influencing market dynamics, with a growing preference for integrated, scalable, and user-friendly solutions that facilitate seamless data integration and analysis. The demand for energy-efficient and environmentally friendly instrumentation is also on the rise, reflecting global sustainability initiatives. The increasing complexity of industrial processes and the need for stringent quality control further propel the demand for sophisticated process instrumentation.

Dominant Regions, Countries, or Segments in Industrial Process Instrumentation Industry

North America, particularly the United States, currently leads the Industrial Process Instrumentation market, driven by its advanced industrial infrastructure, significant investments in oil and gas extraction, and a strong emphasis on technological innovation. The region's mature chemical manufacturing sector and stringent environmental regulations further fuel the demand for sophisticated process control and monitoring solutions. Germany stands out in Europe as a dominant country, boasting a robust automotive manufacturing base and a strong presence of chemical and pharmaceutical industries that rely heavily on process instrumentation. Asia-Pacific, led by China and India, is emerging as the fastest-growing region, fueled by rapid industrialization, substantial government investments in infrastructure projects (including water and wastewater treatment), and the increasing adoption of automation in manufacturing.

Segments Driving Market Growth:

- End-User: Oil and Gas Extraction: This segment is a primary growth engine due to the critical need for precise measurement and control in exploration, production, and refining operations, ensuring safety and efficiency in harsh environments. Market share in this segment is estimated to be over 25%.

- End-User: Energy & Utilities: The increasing demand for reliable power generation and the modernization of grid infrastructure necessitate advanced instrumentation for monitoring and control of power plants and distribution networks. This segment accounts for approximately 20% of the market.

- Technology: Distributed Control System (DCS): DCS solutions are integral to complex industrial processes, offering centralized control and integration of various instrumentation components, thus driving their significant market presence and adoption rates.

- Instrument: Transmitter: The fundamental role of transmitters in converting process variables into usable signals makes them a cornerstone of any instrumentation system, leading to consistently high demand and market share.

- End-User: Chemical Manufacturing: This sector's reliance on precise process control for product quality, safety, and environmental compliance makes it a consistent driver of demand for advanced instrumentation.

Economic policies supporting industrial development, coupled with significant infrastructure upgrades in emerging economies, are key regional drivers. Furthermore, the presence of major global instrumentation manufacturers and their robust distribution networks in these dominant regions significantly bolsters market growth and penetration.

Industrial Process Instrumentation Industry Product Landscape

The Industrial Process Instrumentation industry is characterized by continuous product innovation focused on enhancing accuracy, reliability, and connectivity. Leading product categories include highly sophisticated Transmitters for pressure, temperature, flow, and level measurement, often incorporating advanced diagnostics and self-calibration capabilities. Control Valves, a critical component of process automation, are evolving with smart actuators, digital communication protocols, and improved energy efficiency. Technologies such as Programmable Logic Controllers (PLCs) are becoming more powerful and interconnected, enabling complex automation tasks. Distributed Control Systems (DCS) are offering greater integration and scalability, while Supervisory Control and Data Acquisition (SCADA) systems are enabling comprehensive remote monitoring and control. Manufacturing Execution Systems (MES) are increasingly integrated with instrumentation for real-time production management and optimization. Innovations like the Hawk Measurement Systems' Guided Wave Radar Position Transmitter with Power over Ethernet highlight the industry's move towards simplified installation and enhanced data transmission capabilities.

Key Drivers, Barriers & Challenges in Industrial Process Instrumentation Industry

Key Drivers:

- Industry 4.0 and Smart Manufacturing: The widespread adoption of connected devices, IIoT, and AI is a primary catalyst, driving demand for intelligent instrumentation that provides real-time data for optimization and predictive maintenance.

- Increasing Automation Needs: Industries are continuously seeking to improve efficiency, reduce labor costs, and enhance safety through greater automation, directly boosting the demand for process instrumentation.

- Stringent Regulatory Compliance: Evolving safety, environmental, and quality standards necessitate precise monitoring and control, driving the adoption of advanced instrumentation.

- Growth in Emerging Economies: Rapid industrialization and infrastructure development in regions like Asia-Pacific are creating significant demand for process instrumentation solutions.

- Focus on Energy Efficiency and Sustainability: Instrumentation plays a crucial role in optimizing energy consumption and minimizing emissions, aligning with global sustainability goals.

Barriers & Challenges:

- High Initial Investment Costs: Advanced instrumentation systems can involve significant upfront capital expenditure, posing a challenge for smaller enterprises.

- Cybersecurity Concerns: The increasing connectivity of instrumentation devices raises concerns about data security and the potential for cyber-attacks, requiring robust security measures.

- Skilled Workforce Shortage: The complexity of modern instrumentation systems requires a skilled workforce for installation, maintenance, and operation, which can be a limiting factor.

- Interoperability and Standardization Issues: Ensuring seamless integration between devices from different manufacturers can be challenging due to a lack of universal standards, although this is improving.

- Supply Chain Disruptions: Geopolitical events and global economic factors can lead to supply chain disruptions for critical components, impacting production and delivery timelines.

Emerging Opportunities in Industrial Process Instrumentation Industry

Emerging opportunities lie in the widespread adoption of AI and machine learning for predictive maintenance, anomaly detection, and process optimization, offering predictive analytics as a service. The growing focus on sustainability presents opportunities in instrumentation for emissions monitoring, water conservation, and energy management solutions. The expansion of IIoT platforms, coupled with the demand for edge computing capabilities, is creating a market for compact, intelligent instrumentation devices that can process data locally. Furthermore, the increasing need for robust instrumentation in harsh or remote environments, such as offshore oil rigs and renewable energy installations, presents untapped market potential. The development of wireless instrumentation technologies continues to offer new avenues for simplified installation and reduced cabling costs, especially in retrofitting existing facilities.

Growth Accelerators in the Industrial Process Instrumentation Industry Industry

Long-term growth in the Industrial Process Instrumentation industry will be significantly accelerated by continuous technological breakthroughs, particularly in sensor technology, data analytics, and artificial intelligence. The integration of these technologies will enable increasingly sophisticated predictive and prescriptive maintenance capabilities, reducing downtime and operational costs for end-users. Strategic partnerships between instrumentation manufacturers and software providers will be crucial for developing comprehensive Industry 4.0 solutions, offering seamless integration from the sensor level to enterprise resource planning (ERP) systems. Market expansion strategies, including the penetration of emerging economies with tailored solutions and the development of subscription-based service models, will further fuel sustained growth. The ongoing digital transformation across all industrial sectors ensures a persistent demand for advanced instrumentation that underpins operational excellence.

Key Players Shaping the Industrial Process Instrumentation Industry Market

- Emerson Electric Company

- Metso Corporation

- Honeywell International Inc

- ABB Ltd

- Endress+ Hauser AG

- Mitsubishi Electric Corporation

- Siemens AG

- Danaher Corporation

- Omron Corporation

- Rockwell Automation Inc

- Yokogawa Electric Corporation

Notable Milestones in Industrial Process Instrumentation Industry Sector

- July 2022 - Hawk Measurement Systems (HAWK) introduced the industry's first Guided Wave Radar Position Transmitter with Power through Ethernet communications, enhancing ease of installation and data transfer.

- May 2022 - SymphonyAI Industrial launched its AI-incorporated MOM 360 manufacturing operations management solution, aiming to enable Industry 4.0 objectives through AI-based workflow optimization.

- March 2022 - AMETEK Process Instruments launched a novel e-commerce platform for its US market, simplifying procurement for customers.

- January 2022 - Parker Hannifin introduced its EP Series Pro-Bloc valves, featuring dual block and bleed functionality compliant with EEMUA 182, enhancing safety and reliability in instrument valve applications.

In-Depth Industrial Process Instrumentation Industry Market Outlook

The future outlook for the Industrial Process Instrumentation market is exceptionally positive, driven by the accelerating digital transformation of industries worldwide. Growth accelerators include the widespread adoption of AI for predictive analytics, enhancing operational efficiency and reducing maintenance costs. The increasing global emphasis on sustainability will further boost demand for instrumentation that supports environmental monitoring and resource optimization. Strategic alliances and partnerships will play a pivotal role in developing integrated Industry 4.0 solutions, bridging the gap between physical processes and digital intelligence. Market expansion into emerging economies, coupled with the development of innovative service-based business models, will unlock new revenue streams and sustained growth opportunities. The continuous evolution of sensor technology and data processing capabilities promises to deliver even more sophisticated and intelligent instrumentation, solidifying its indispensable role in modern industrial operations.

Industrial Process Instrumentation Industry Segmentation

-

1. Instrument

- 1.1. Transmitter

- 1.2. Control Valve

-

2. Technology

- 2.1. Programmable Logic Controller (PLC)

- 2.2. Distributed Control System (DCS)

- 2.3. Supervisory Control and Data Acquisition (SCADA)

- 2.4. Manufacturing Execution System (MES)

-

3. End-User

- 3.1. Water and Wastewater Treatment

- 3.2. Chemical Manufacturing

- 3.3. Energy & Utilities

- 3.4. Oil and Gas Extraction

- 3.5. Metals and Mining

- 3.6. Other Process Industries

Industrial Process Instrumentation Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Industrial Process Instrumentation Industry Regional Market Share

Geographic Coverage of Industrial Process Instrumentation Industry

Industrial Process Instrumentation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.35% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing demand for energy-efficient production processes; High level of efficiency with minimum cost

- 3.3. Market Restrains

- 3.3.1. Higher cost of research and development; Higher cost of implementation and maintenance of solutions and devices

- 3.4. Market Trends

- 3.4.1. Water and Wastewater Treatment is Expected to Witness the Highest Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Industrial Process Instrumentation Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Instrument

- 5.1.1. Transmitter

- 5.1.2. Control Valve

- 5.2. Market Analysis, Insights and Forecast - by Technology

- 5.2.1. Programmable Logic Controller (PLC)

- 5.2.2. Distributed Control System (DCS)

- 5.2.3. Supervisory Control and Data Acquisition (SCADA)

- 5.2.4. Manufacturing Execution System (MES)

- 5.3. Market Analysis, Insights and Forecast - by End-User

- 5.3.1. Water and Wastewater Treatment

- 5.3.2. Chemical Manufacturing

- 5.3.3. Energy & Utilities

- 5.3.4. Oil and Gas Extraction

- 5.3.5. Metals and Mining

- 5.3.6. Other Process Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Instrument

- 6. North America Industrial Process Instrumentation Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Instrument

- 6.1.1. Transmitter

- 6.1.2. Control Valve

- 6.2. Market Analysis, Insights and Forecast - by Technology

- 6.2.1. Programmable Logic Controller (PLC)

- 6.2.2. Distributed Control System (DCS)

- 6.2.3. Supervisory Control and Data Acquisition (SCADA)

- 6.2.4. Manufacturing Execution System (MES)

- 6.3. Market Analysis, Insights and Forecast - by End-User

- 6.3.1. Water and Wastewater Treatment

- 6.3.2. Chemical Manufacturing

- 6.3.3. Energy & Utilities

- 6.3.4. Oil and Gas Extraction

- 6.3.5. Metals and Mining

- 6.3.6. Other Process Industries

- 6.1. Market Analysis, Insights and Forecast - by Instrument

- 7. Europe Industrial Process Instrumentation Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Instrument

- 7.1.1. Transmitter

- 7.1.2. Control Valve

- 7.2. Market Analysis, Insights and Forecast - by Technology

- 7.2.1. Programmable Logic Controller (PLC)

- 7.2.2. Distributed Control System (DCS)

- 7.2.3. Supervisory Control and Data Acquisition (SCADA)

- 7.2.4. Manufacturing Execution System (MES)

- 7.3. Market Analysis, Insights and Forecast - by End-User

- 7.3.1. Water and Wastewater Treatment

- 7.3.2. Chemical Manufacturing

- 7.3.3. Energy & Utilities

- 7.3.4. Oil and Gas Extraction

- 7.3.5. Metals and Mining

- 7.3.6. Other Process Industries

- 7.1. Market Analysis, Insights and Forecast - by Instrument

- 8. Asia Pacific Industrial Process Instrumentation Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Instrument

- 8.1.1. Transmitter

- 8.1.2. Control Valve

- 8.2. Market Analysis, Insights and Forecast - by Technology

- 8.2.1. Programmable Logic Controller (PLC)

- 8.2.2. Distributed Control System (DCS)

- 8.2.3. Supervisory Control and Data Acquisition (SCADA)

- 8.2.4. Manufacturing Execution System (MES)

- 8.3. Market Analysis, Insights and Forecast - by End-User

- 8.3.1. Water and Wastewater Treatment

- 8.3.2. Chemical Manufacturing

- 8.3.3. Energy & Utilities

- 8.3.4. Oil and Gas Extraction

- 8.3.5. Metals and Mining

- 8.3.6. Other Process Industries

- 8.1. Market Analysis, Insights and Forecast - by Instrument

- 9. Rest of the World Industrial Process Instrumentation Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Instrument

- 9.1.1. Transmitter

- 9.1.2. Control Valve

- 9.2. Market Analysis, Insights and Forecast - by Technology

- 9.2.1. Programmable Logic Controller (PLC)

- 9.2.2. Distributed Control System (DCS)

- 9.2.3. Supervisory Control and Data Acquisition (SCADA)

- 9.2.4. Manufacturing Execution System (MES)

- 9.3. Market Analysis, Insights and Forecast - by End-User

- 9.3.1. Water and Wastewater Treatment

- 9.3.2. Chemical Manufacturing

- 9.3.3. Energy & Utilities

- 9.3.4. Oil and Gas Extraction

- 9.3.5. Metals and Mining

- 9.3.6. Other Process Industries

- 9.1. Market Analysis, Insights and Forecast - by Instrument

- 10. Competitive Analysis

- 10.1. Global Market Share Analysis 2025

- 10.2. Company Profiles

- 10.2.1 Emerson Electric Company

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Metso Corporation

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Honeywell International Inc

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 ABB Ltd

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Endress+ Hauser AG *List Not Exhaustive

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Mitsubishi Electric Corporation

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Siemens AG

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Danaher Corporation

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Omron Corporation

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Rockwell Automation Inc

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Yokogawa Electric Corporation

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.1 Emerson Electric Company

List of Figures

- Figure 1: Global Industrial Process Instrumentation Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Industrial Process Instrumentation Industry Revenue (Million), by Instrument 2025 & 2033

- Figure 3: North America Industrial Process Instrumentation Industry Revenue Share (%), by Instrument 2025 & 2033

- Figure 4: North America Industrial Process Instrumentation Industry Revenue (Million), by Technology 2025 & 2033

- Figure 5: North America Industrial Process Instrumentation Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 6: North America Industrial Process Instrumentation Industry Revenue (Million), by End-User 2025 & 2033

- Figure 7: North America Industrial Process Instrumentation Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 8: North America Industrial Process Instrumentation Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Industrial Process Instrumentation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Industrial Process Instrumentation Industry Revenue (Million), by Instrument 2025 & 2033

- Figure 11: Europe Industrial Process Instrumentation Industry Revenue Share (%), by Instrument 2025 & 2033

- Figure 12: Europe Industrial Process Instrumentation Industry Revenue (Million), by Technology 2025 & 2033

- Figure 13: Europe Industrial Process Instrumentation Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 14: Europe Industrial Process Instrumentation Industry Revenue (Million), by End-User 2025 & 2033

- Figure 15: Europe Industrial Process Instrumentation Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 16: Europe Industrial Process Instrumentation Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Industrial Process Instrumentation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Industrial Process Instrumentation Industry Revenue (Million), by Instrument 2025 & 2033

- Figure 19: Asia Pacific Industrial Process Instrumentation Industry Revenue Share (%), by Instrument 2025 & 2033

- Figure 20: Asia Pacific Industrial Process Instrumentation Industry Revenue (Million), by Technology 2025 & 2033

- Figure 21: Asia Pacific Industrial Process Instrumentation Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: Asia Pacific Industrial Process Instrumentation Industry Revenue (Million), by End-User 2025 & 2033

- Figure 23: Asia Pacific Industrial Process Instrumentation Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 24: Asia Pacific Industrial Process Instrumentation Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Industrial Process Instrumentation Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Rest of the World Industrial Process Instrumentation Industry Revenue (Million), by Instrument 2025 & 2033

- Figure 27: Rest of the World Industrial Process Instrumentation Industry Revenue Share (%), by Instrument 2025 & 2033

- Figure 28: Rest of the World Industrial Process Instrumentation Industry Revenue (Million), by Technology 2025 & 2033

- Figure 29: Rest of the World Industrial Process Instrumentation Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 30: Rest of the World Industrial Process Instrumentation Industry Revenue (Million), by End-User 2025 & 2033

- Figure 31: Rest of the World Industrial Process Instrumentation Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 32: Rest of the World Industrial Process Instrumentation Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Rest of the World Industrial Process Instrumentation Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Instrument 2020 & 2033

- Table 2: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 3: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 4: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Instrument 2020 & 2033

- Table 6: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 7: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 8: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Instrument 2020 & 2033

- Table 10: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 11: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 12: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Instrument 2020 & 2033

- Table 14: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 15: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 16: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Instrument 2020 & 2033

- Table 18: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Technology 2020 & 2033

- Table 19: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 20: Global Industrial Process Instrumentation Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Industrial Process Instrumentation Industry?

The projected CAGR is approximately 3.35%.

2. Which companies are prominent players in the Industrial Process Instrumentation Industry?

Key companies in the market include Emerson Electric Company, Metso Corporation, Honeywell International Inc, ABB Ltd, Endress+ Hauser AG *List Not Exhaustive, Mitsubishi Electric Corporation, Siemens AG, Danaher Corporation, Omron Corporation, Rockwell Automation Inc, Yokogawa Electric Corporation.

3. What are the main segments of the Industrial Process Instrumentation Industry?

The market segments include Instrument, Technology , End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 18.46 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing demand for energy-efficient production processes; High level of efficiency with minimum cost.

6. What are the notable trends driving market growth?

Water and Wastewater Treatment is Expected to Witness the Highest Growth.

7. Are there any restraints impacting market growth?

Higher cost of research and development; Higher cost of implementation and maintenance of solutions and devices.

8. Can you provide examples of recent developments in the market?

July 2022 - Hawk Measurement Systems (HAWK), a pioneer in positioning, level, asset monitoring, and fiber optical monitoring systems, created the industry's first Guided Wave Radar Position Transmitter with Power through Ethernet communications.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Industrial Process Instrumentation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Industrial Process Instrumentation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Industrial Process Instrumentation Industry?

To stay informed about further developments, trends, and reports in the Industrial Process Instrumentation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence