Key Insights

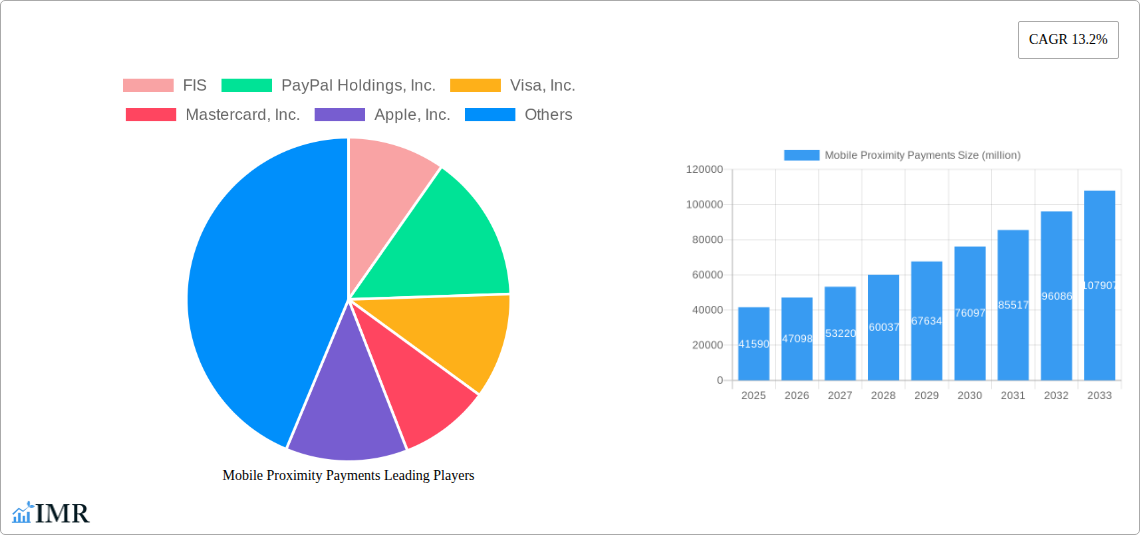

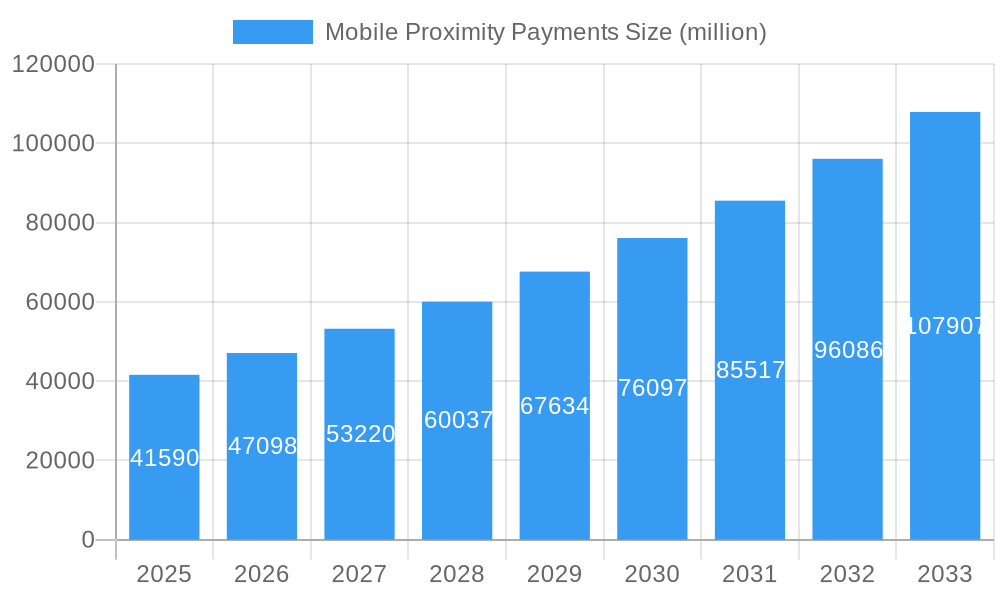

The global Mobile Proximity Payments market is projected to experience significant expansion, reaching an estimated USD 41,590 million in 2025. This robust growth is underpinned by a compelling Compound Annual Growth Rate (CAGR) of 13.2%, indicating a sustained upward trajectory throughout the forecast period of 2025-2033. This burgeoning market is fueled by several key drivers, including the increasing adoption of smartphones, the growing demand for convenient and secure transaction methods, and the widespread expansion of NFC and QR code payment infrastructure. Consumers are increasingly embracing contactless payment solutions for their speed and ease of use, particularly in high-traffic retail environments.

Mobile Proximity Payments Market Size (In Billion)

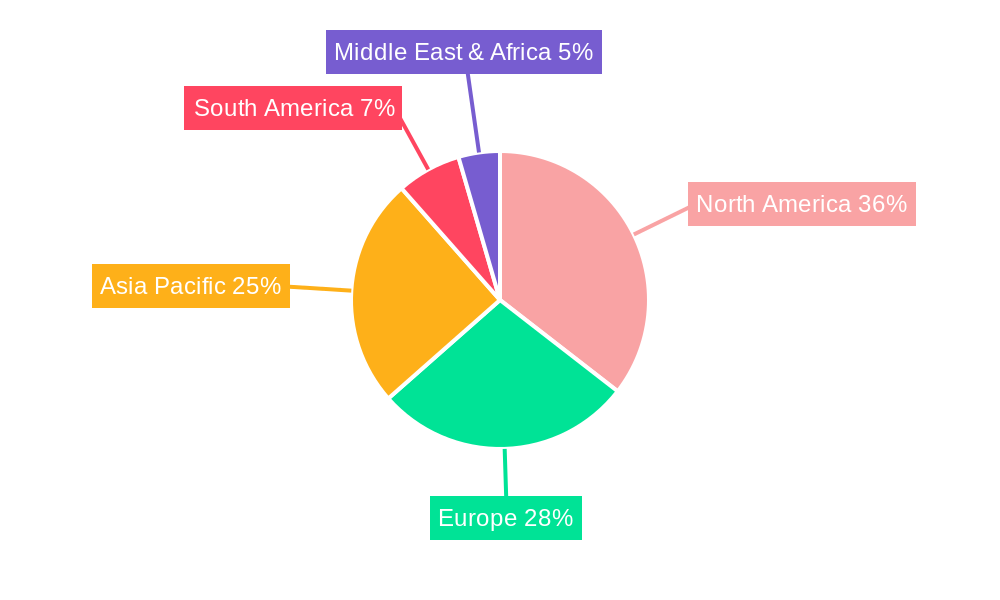

The market's segmentation by application highlights the dominance of Grocery Stores as a primary adoption point, followed by Bars and Restaurants, reflecting the everyday nature of mobile proximity payments in consumer spending. The Solution segment is expected to lead the type division, driven by advancements in mobile payment technologies and secure tokenization. Geographically, North America, led by the United States, is poised to remain a dominant force, while Asia Pacific is anticipated to witness the fastest growth, propelled by rapid digitalization and a burgeoning smartphone user base in countries like China and India. Emerging markets across all regions are expected to contribute significantly to this expansion, driven by government initiatives promoting digital economies and increased merchant adoption of mobile payment terminals.

Mobile Proximity Payments Company Market Share

Mobile Proximity Payments Market Report: Unlocking Growth in Contactless Transactions

This comprehensive report delivers an in-depth analysis of the global Mobile Proximity Payments market, a dynamic sector transforming how consumers and businesses engage in transactions. Spanning the Study Period of 2019–2033, with a Base Year of 2025, this report offers critical insights into market dynamics, growth trends, regional dominance, product innovation, key drivers, emerging opportunities, and the competitive landscape. It is meticulously structured to provide actionable intelligence for industry professionals, investors, and stakeholders navigating this rapidly evolving ecosystem. This report is for immediate use and requires no further modification.

Mobile Proximity Payments Market Dynamics & Structure

The global mobile proximity payments market exhibits a moderately concentrated structure, driven by significant technological innovation and a robust regulatory environment. Key players like FIS, PayPal Holdings, Inc., Visa, Inc., and Mastercard, Inc. exert considerable influence, alongside tech giants such as Apple, Inc., Google, LLC, and payment solution providers like Square, Inc., Ingenico, ACI Worldwide, Inc., and IDEMIA SAS. The market is propelled by the increasing adoption of Near Field Communication (NFC) and Bluetooth Low Energy (BLE) technologies, enhancing transaction speed and security. Regulatory frameworks, including PSD2 in Europe and similar initiatives globally, are fostering greater interoperability and consumer protection, further solidifying market growth. Competitive product substitutes, such as traditional card payments and cash, are gradually being displaced by the convenience and security offered by mobile proximity solutions. End-user demographics skew towards younger, tech-savvy consumers, though a broader demographic is rapidly embracing contactless payments. Merger and acquisition (M&A) trends remain active, with an estimated 150 M&A deals observed during the historical period (2019-2024), indicating a consolidation drive and strategic expansion.

- Market Concentration: Moderately concentrated with a few dominant players.

- Technological Innovation Drivers: NFC, BLE, tokenization, and advanced encryption.

- Regulatory Frameworks: PSD2, EMV standards, and data privacy regulations fostering trust.

- Competitive Product Substitutes: Declining market share of cash and traditional card payments.

- End-User Demographics: Young adults and digitally native consumers leading adoption, with significant growth in older demographics.

- M&A Trends: Active consolidation and strategic acquisitions to gain market share and technological capabilities.

Mobile Proximity Payments Growth Trends & Insights

The global mobile proximity payments market is on an unprecedented growth trajectory, projected to reach an estimated market size of $2,500 billion by 2033. This represents a remarkable Compound Annual Growth Rate (CAGR) of approximately 22% from the Base Year of 2025. The historical period (2019-2024) witnessed a steady increase in adoption, with market penetration growing from an estimated 35% in 2019 to an anticipated 65% by the end of 2024. This surge is predominantly fueled by evolving consumer behavior, with an increasing preference for contactless and secure payment methods. Technological disruptions, including the widespread availability of smartphones equipped with NFC capabilities and the development of sophisticated mobile payment applications, have been pivotal. The convenience of making payments with a tap of a smartphone or wearable device has resonated deeply with consumers seeking faster and more seamless checkout experiences. Furthermore, the ongoing COVID-19 pandemic accelerated the shift towards contactless transactions, reinforcing the demand for mobile proximity payment solutions across various industries. The market penetration in developed economies is expected to exceed 80% by 2033, while emerging markets will witness rapid adoption driven by increasing smartphone penetration and the development of robust digital payment infrastructures. This sustained growth is further supported by strategic partnerships between financial institutions, mobile carriers, and technology providers, creating a robust ecosystem that encourages innovation and wider accessibility. The estimated market size in the Base Year of 2025 is projected to be $1,100 billion, underscoring the significant expansion anticipated in the coming decade. The adoption rates are expected to continue their upward climb, driven by increasing merchant acceptance and a growing awareness of the benefits associated with mobile proximity payments.

Dominant Regions, Countries, or Segments in Mobile Proximity Payments

The Asia Pacific region is poised to be the dominant force in the global mobile proximity payments market, driven by its vast population, high smartphone penetration, and rapidly advancing digital economy. Countries like China, India, and South Korea are at the forefront of this growth, fueled by government initiatives promoting digital payments and a burgeoning e-commerce sector. In terms of application, Grocery Stores and Bars and Restaurants are emerging as the leading segments, accounting for an estimated 30% and 25% of the total transaction volume respectively in the Base Year of 2025. The convenience and speed offered by mobile proximity payments are particularly attractive in these high-frequency transaction environments.

Dominant Region: Asia Pacific, driven by China and India.

- Key Drivers: High smartphone penetration, supportive government policies, rapid urbanization, and a large unbanked population transitioning directly to digital finance.

- Market Share: Estimated to account for over 40% of the global market by 2033.

- Growth Potential: Significant untapped rural markets and increasing disposable incomes.

Dominant Application Segment: Grocery Stores.

- Key Drivers: High transaction volume, increasing consumer preference for contactless checkout, and integration with loyalty programs.

- Market Share (Grocery Stores): Projected to reach 35% of all mobile proximity transactions by 2033.

- Growth Potential: Expansion of self-checkout kiosks and integration with online grocery delivery services.

Dominant Type: Solution.

- Key Drivers: The increasing availability of integrated payment solutions within mobile wallets and POS systems, offering end-to-end transaction processing.

- Market Share (Solutions): Expected to comprise over 70% of the market by 2033, encompassing software, hardware, and platform solutions.

- Growth Potential: Development of specialized solutions for SMEs and emerging markets.

Other Significant Segments: Drug Stores and Entertainment Centers also exhibit strong growth, driven by the demand for quick and secure payment options, especially during peak hours. The "Others" segment, encompassing public transport, vending machines, and parking, is also expanding rapidly as infrastructure for contactless payments becomes more ubiquitous.

Mobile Proximity Payments Product Landscape

The mobile proximity payments product landscape is characterized by continuous innovation, focusing on enhanced security, user experience, and broader acceptance. Key product developments include advanced tokenization protocols, biometric authentication (fingerprint and facial recognition), and the seamless integration of payment functionalities into smartwatches and other wearable devices. Mobile wallets, such as Apple Pay, Google Pay, and Samsung Pay, are central to this landscape, offering a unified platform for various payment instruments. Performance metrics are consistently improving, with transaction processing times reduced to milliseconds, ensuring a smooth customer journey. Unique selling propositions revolve around heightened security features, loyalty program integration, and the ability to store multiple payment methods and cards within a single application. Technological advancements in NFC and secure element technology are further bolstering the reliability and speed of these solutions, making them indispensable in modern retail and service environments.

Key Drivers, Barriers & Challenges in Mobile Proximity Payments

Key Drivers:

The mobile proximity payments market is propelled by several key drivers. The escalating demand for contactless and touch-free transactions, amplified by health concerns and a desire for convenience, is a primary catalyst. Rapid advancements in mobile technology, including ubiquitous smartphone adoption and the integration of NFC chips, form a foundational driver. Furthermore, the growing acceptance and integration of mobile payment solutions by merchants worldwide, coupled with supportive government policies promoting digital economies and financial inclusion, are significantly accelerating market growth. The increasing popularity of e-commerce and the subsequent need for seamless online-to-offline payment experiences also contribute to this upward trend.

Barriers & Challenges:

Despite its robust growth, the market faces certain barriers and challenges. Security concerns and the risk of data breaches remain a persistent challenge, necessitating continuous investment in robust cybersecurity measures. An estimated 15% of consumers cite security as a primary barrier to adoption. Merchant adoption can be inconsistent, especially among small and medium-sized enterprises (SMEs), due to the perceived cost of new hardware and integration. Regulatory hurdles and variations in data privacy laws across different jurisdictions can also create complexities. Furthermore, the "digital divide" and a lack of reliable internet infrastructure in certain regions can limit widespread accessibility. Supply chain issues affecting the availability of NFC-enabled devices also pose a temporary constraint.

Emerging Opportunities in Mobile Proximity Payments

Emerging opportunities in the mobile proximity payments sector are diverse and promising. The integration of loyalty programs and personalized offers directly into mobile payment platforms presents a significant avenue for enhanced customer engagement and increased transaction frequency. The expansion of mobile proximity payments into previously underserved markets, such as public transportation ticketing, unattended retail (vending machines and kiosks), and micro-transactions for digital content, offers substantial growth potential. Furthermore, the development of sophisticated B2B mobile payment solutions for expense management and supplier payments represents a burgeoning area. The growing adoption of wearable technology, beyond smartwatches, for payment purposes, opens new frontiers for seamless and intuitive transactions, catering to evolving consumer preferences for convenience and personalization.

Growth Accelerators in the Mobile Proximity Payments Industry

Several catalysts are accelerating long-term growth in the mobile proximity payments industry. The relentless pace of technological innovation, including advancements in AI for fraud detection and personalized user experiences, is a key accelerator. Strategic partnerships between financial institutions, mobile network operators, and tech giants are fostering wider ecosystem adoption and interoperability. The increasing global focus on financial inclusion and the push towards cashless societies by governments worldwide are creating fertile ground for mobile payment solutions. Moreover, the continuous improvement in user interface design and the simplification of the payment process are crucial in driving mass consumer adoption and retention, further solidifying the market's upward trajectory.

Key Players Shaping the Mobile Proximity Payments Market

- FIS

- PayPal Holdings, Inc.

- Visa, Inc.

- Mastercard, Inc.

- Apple, Inc.

- Square, Inc.

- Google, LLC

- Ingenico

- ACI Worldwide, Inc.

- IDEMIA SAS

Notable Milestones in Mobile Proximity Payments Sector

- 2019 March: Launch of Apple Pay Cash person-to-person payments, enhancing mobile wallet functionality.

- 2020 January: Google Pay's significant expansion into new markets, broadening its global reach.

- 2020 April: Visa and Mastercard announce accelerated rollout of contactless payment technology due to COVID-19.

- 2021 February: Square's acquisition of Afterpay, bolstering its buy now, pay later capabilities integrated with mobile payments.

- 2022 July: Apple announces significant expansion of Apple Pay Later service, integrating BNPL into its mobile wallet.

- 2023 March: FIS announces strategic partnerships to enhance its cloud-based payment processing capabilities for mobile proximity.

- 2023 October: PayPal Holdings, Inc. introduces enhanced security features for its mobile app, focusing on fraud prevention.

- 2024 January: Ingenico rolls out new generation of contactless payment terminals designed for enhanced mobile integration.

- 2024 June: IDEMIA SAS partners with major banks to deploy advanced biometric payment solutions.

- 2025 Q1 (Projected): ACI Worldwide to launch its next-gen real-time payment platform, enabling seamless mobile proximity transactions.

In-Depth Mobile Proximity Payments Market Outlook

The future of mobile proximity payments is exceptionally bright, driven by an ever-increasing consumer demand for convenience and security, coupled with relentless technological advancements. The projected growth accelerators, including the expansion of wearable payment technology, the integration of AI for personalized financial services, and the ongoing push towards cashless economies globally, will continue to fuel market expansion. Strategic partnerships and supportive regulatory environments will further solidify the ecosystem, making mobile proximity payments the default choice for a vast majority of transactions. The market is poised for sustained, high-paced growth, offering significant opportunities for innovation and investment in the coming years.

Mobile Proximity Payments Segmentation

-

1. Application

- 1.1. Grocery Stores

- 1.2. Drug Stores

- 1.3. Bars and Restaurants

- 1.4. Entertainment Centers

- 1.5. Others

-

2. Type

- 2.1. Solution

- 2.2. Services

Mobile Proximity Payments Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Mobile Proximity Payments Regional Market Share

Geographic Coverage of Mobile Proximity Payments

Mobile Proximity Payments REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 38% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Grocery Stores

- 5.1.2. Drug Stores

- 5.1.3. Bars and Restaurants

- 5.1.4. Entertainment Centers

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Solution

- 5.2.2. Services

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Mobile Proximity Payments Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Grocery Stores

- 6.1.2. Drug Stores

- 6.1.3. Bars and Restaurants

- 6.1.4. Entertainment Centers

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Solution

- 6.2.2. Services

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Mobile Proximity Payments Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Grocery Stores

- 7.1.2. Drug Stores

- 7.1.3. Bars and Restaurants

- 7.1.4. Entertainment Centers

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Solution

- 7.2.2. Services

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Mobile Proximity Payments Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Grocery Stores

- 8.1.2. Drug Stores

- 8.1.3. Bars and Restaurants

- 8.1.4. Entertainment Centers

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Solution

- 8.2.2. Services

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Mobile Proximity Payments Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Grocery Stores

- 9.1.2. Drug Stores

- 9.1.3. Bars and Restaurants

- 9.1.4. Entertainment Centers

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Solution

- 9.2.2. Services

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Mobile Proximity Payments Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Grocery Stores

- 10.1.2. Drug Stores

- 10.1.3. Bars and Restaurants

- 10.1.4. Entertainment Centers

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Solution

- 10.2.2. Services

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Mobile Proximity Payments Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Grocery Stores

- 11.1.2. Drug Stores

- 11.1.3. Bars and Restaurants

- 11.1.4. Entertainment Centers

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Solution

- 11.2.2. Services

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 FIS

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 PayPal Holdings Inc.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Visa Inc.

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Mastercard Inc.

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Apple Inc.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Square Inc.

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Google LLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Ingenico

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 ACI Worldwide Inc.

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 IDEMIA SAS

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 FIS

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Mobile Proximity Payments Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Mobile Proximity Payments Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Mobile Proximity Payments Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Mobile Proximity Payments Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Mobile Proximity Payments Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Mobile Proximity Payments Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Mobile Proximity Payments Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Mobile Proximity Payments Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Mobile Proximity Payments Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Mobile Proximity Payments Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Mobile Proximity Payments Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Mobile Proximity Payments Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Mobile Proximity Payments Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Mobile Proximity Payments Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Mobile Proximity Payments Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Mobile Proximity Payments Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Mobile Proximity Payments Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Mobile Proximity Payments Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Mobile Proximity Payments Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Mobile Proximity Payments Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Mobile Proximity Payments Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Mobile Proximity Payments Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Mobile Proximity Payments Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Mobile Proximity Payments Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Mobile Proximity Payments Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Mobile Proximity Payments Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Mobile Proximity Payments Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Mobile Proximity Payments Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Mobile Proximity Payments Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Mobile Proximity Payments Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Mobile Proximity Payments Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Mobile Proximity Payments Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Mobile Proximity Payments Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Mobile Proximity Payments Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Mobile Proximity Payments Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Mobile Proximity Payments Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Mobile Proximity Payments Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Mobile Proximity Payments Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Mobile Proximity Payments Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Mobile Proximity Payments Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Mobile Proximity Payments Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Mobile Proximity Payments Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Mobile Proximity Payments Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Mobile Proximity Payments Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Mobile Proximity Payments Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Mobile Proximity Payments Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Mobile Proximity Payments Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Mobile Proximity Payments Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Mobile Proximity Payments Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Mobile Proximity Payments Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Mobile Proximity Payments?

The projected CAGR is approximately 38%.

2. Which companies are prominent players in the Mobile Proximity Payments?

Key companies in the market include FIS, PayPal Holdings, Inc., Visa, Inc., Mastercard, Inc., Apple, Inc., Square, Inc., Google, LLC, Ingenico, ACI Worldwide, Inc., IDEMIA SAS.

3. What are the main segments of the Mobile Proximity Payments?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 88.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Mobile Proximity Payments," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Mobile Proximity Payments report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Mobile Proximity Payments?

To stay informed about further developments, trends, and reports in the Mobile Proximity Payments, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence