Key Insights

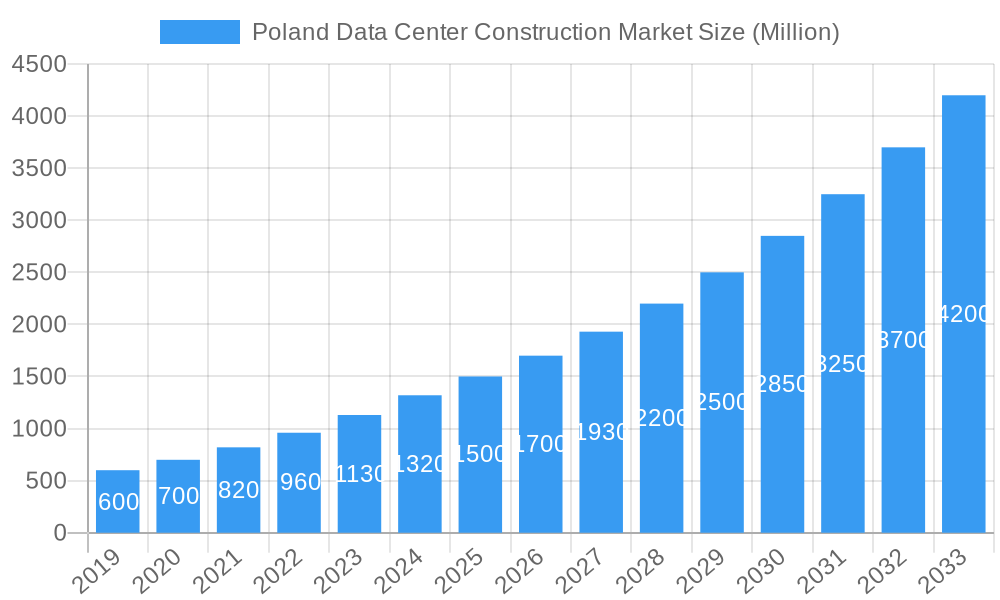

The Poland Data Center Construction Market is projected for robust expansion, anticipated to reach approximately $1.16 billion by 2025, driven by a compelling Compound Annual Growth Rate (CAGR) of 21%. This growth is underpinned by escalating demand for digital services, cloud computing, and the accelerated adoption of Artificial Intelligence (AI) and big data analytics. Key growth catalysts include the ongoing digitization of enterprises, the imperative for enhanced data security and sovereignty, and substantial investments in hyperscale and colocation facilities. The strategic development of critical infrastructure, particularly in power distribution units (PDUs), transfer switches, switchgear, and advanced cooling solutions like immersion and direct-to-chip technologies, is essential for meeting the increasing power and thermal demands of modern data centers. The market also observes a strong preference for Tier-III and Tier-IV certified facilities, emphasizing high availability and reliability.

Poland Data Center Construction Market Market Size (In Billion)

Market segmentation reveals a significant focus on electrical infrastructure, including power distribution and backup power systems, alongside mechanical infrastructure, with advanced cooling and rack solutions being crucial. The IT and Telecommunications sector, alongside Banking, Financial Services, and Insurance (BFSI), are primary end-users driving demand for sophisticated data center capabilities. Government and Defense sectors are also increasing their engagement due to national security objectives and digital transformation imperatives. Emerging trends such as edge computing and sustainable data center designs incorporating renewable energy sources are poised to further influence market dynamics. While significant capital investment and the availability of skilled personnel may present challenges, the strong growth trajectory and the strategic importance of data centers in Poland's digital economy indicate a highly favorable outlook for the construction market.

Poland Data Center Construction Market Company Market Share

Poland Data Center Construction Market: Comprehensive Analysis and Forecast (2019-2033)

This in-depth report delivers a definitive analysis of the Poland Data Center Construction Market, offering critical insights into its current landscape and future trajectory. Spanning a study period from 2019 to 2033, with a base year of 2025, this research provides a robust understanding of market dynamics, growth trends, segment dominance, product innovations, key drivers, emerging opportunities, and strategic outlook. This report is your essential guide to navigating the evolving Polish data center ecosystem.

Poland Data Center Construction Market Market Dynamics & Structure

The Poland data center construction market is characterized by a moderate to high level of concentration, with key players actively investing in expansion and new facility development. Technological innovation is a primary driver, propelled by the increasing demand for higher processing power, advanced cooling solutions (such as immersion cooling and direct-to-chip cooling), and efficient power distribution. Regulatory frameworks, particularly those related to data privacy (GDPR) and environmental sustainability, are shaping construction standards and operational practices. While competitive product substitutes exist, the unique requirements for hyperscale and enterprise-grade data centers limit their immediate impact. End-user demographics are increasingly shifting towards IT and Telecommunications, and Banking, Financial Services, and Insurance (BFSI) sectors, demanding robust, secure, and scalable infrastructure. Mergers and acquisitions (M&A) activity is a notable trend, with companies seeking to expand their footprint and service offerings. For instance, the acquisition of land for new data centers by established operators signals consolidation and strategic growth. The market's evolution is further influenced by the continuous need for energy-efficient designs and the integration of renewable energy sources.

- Market Concentration: Dominated by a few key developers and investors, with increasing M&A activity indicating consolidation.

- Technological Innovation: Driven by demand for high-density computing, advanced cooling technologies (e.g., Liquid Cooling), and sustainable energy solutions.

- Regulatory Frameworks: GDPR compliance and increasing environmental regulations are shaping design and operational standards.

- End-User Shift: Growing demand from IT & Telecommunications, BFSI, and expanding cloud service providers.

- M&A Trends: Companies are actively acquiring land and existing facilities to scale operations and gain market share.

Poland Data Center Construction Market Growth Trends & Insights

The Poland data center construction market is poised for substantial growth, driven by a confluence of accelerating digital transformation, the expanding cloud computing landscape, and the burgeoning demand for colocation services. The market size has witnessed consistent expansion over the historical period (2019-2024), a trend anticipated to continue with a significant Compound Annual Growth Rate (CAGR) projected for the forecast period (2025-2033). Adoption rates for modern data center infrastructure, including hyperscale and edge facilities, are on an upward trajectory. Technological disruptions, such as the widespread adoption of AI, IoT, and big data analytics, are creating an insatiable appetite for high-performance computing and storage capabilities, directly fueling the need for new and upgraded data center capacity. Consumer behavior shifts, characterized by an increased reliance on digital services and remote work, further bolster this demand. For example, the growth in online streaming, e-commerce, and sophisticated gaming platforms necessitates low-latency, high-bandwidth connectivity, which can only be supported by a robust data center network. The increasing digitalization of Polish industries, from manufacturing to public administration, also plays a crucial role. Furthermore, the strategic location of Poland within Europe, coupled with competitive operational costs, is attracting international investors and cloud providers, accelerating the market's expansion. The ongoing digitalization of businesses and the increasing adoption of hybrid cloud strategies are key indicators of the sustained growth potential within the Polish data center construction sector.

Dominant Regions, Countries, or Segments in Poland Data Center Construction Market

The IT and Telecommunications end-user segment is emerging as a dominant force driving growth in the Poland Data Center Construction Market. This dominance stems from the escalating demand for cloud services, data storage, and processing power required by telecommunication providers, hyperscale cloud operators, and IT outsourcing companies. The increasing adoption of 5G technology, the expansion of fiber optic networks, and the proliferation of digital services are all directly contributing to the need for more advanced and capacious data center facilities within Poland.

Within the Infrastructure segmentation, Electrical Infrastructure plays a pivotal role. Specifically, Power Backup Solutions, encompassing Uninterruptible Power Supplies (UPS) and Generators, are critical components. The reliability and uptime of data centers are paramount, making robust power backup systems indispensable. The increasing density of IT equipment and the growing number of high-tier data centers (Tier-III and Tier-IV) demand sophisticated and redundant power solutions to ensure continuous operation.

Furthermore, the Mechanical Infrastructure, particularly Cooling Systems, is a significant growth driver. As IT hardware becomes more powerful and racks become denser, efficient cooling solutions are essential to manage heat dissipation and maintain optimal operating temperatures. Advancements in cooling technologies, including in-row and in-rack cooling solutions, and the emerging interest in immersion cooling, are pivotal in supporting the next generation of data center build-outs.

The Tier-III and Tier-IV data center classifications are also experiencing significant traction. These higher-tier facilities offer greater redundancy and uptime, catering to the stringent requirements of enterprises, financial institutions, and government bodies that cannot afford operational disruptions. The construction of these advanced facilities requires substantial investment in both electrical and mechanical infrastructure, further solidifying their importance in market growth.

- Dominant End User: IT and Telecommunications, fueled by cloud adoption and 5G rollout.

- Key Infrastructure Segment: Electrical Infrastructure, with a strong emphasis on Power Backup Solutions (UPS, Generators) for critical uptime.

- Growing Mechanical Infrastructure: Cooling Systems are vital for managing high-density computing, with innovations like in-row and immersion cooling gaining traction.

- Tier Standard Focus: Increasing construction of Tier-III and Tier-IV facilities to meet enterprise and government demands for high availability.

- Geographic Concentration: While not explicitly detailed in the prompt, major urban centers and industrial zones are likely to see concentrated development due to connectivity and power infrastructure availability.

Poland Data Center Construction Market Product Landscape

The Poland data center construction market is witnessing a surge in sophisticated infrastructure products designed for enhanced efficiency, reliability, and scalability. Innovations in Power Distribution Solutions include advanced Power Distribution Units (PDUs) with intelligent monitoring capabilities, seamless transfer switches (Static and Automatic), and modular switchgear for low-voltage and medium-voltage applications. In Power Backup Solutions, high-capacity UPS systems and state-of-the-art generators are becoming standard. For Mechanical Infrastructure, the focus is on advanced cooling systems, with Immersion Cooling and Direct-to-chip Cooling emerging as key technologies for managing high-density racks. In-row and in-rack cooling solutions continue to be vital for optimized airflow management. The overall product landscape is characterized by a drive towards modularity, energy efficiency, and intelligent management systems, enabling data center operators to meet the evolving demands of modern digital workloads.

Key Drivers, Barriers & Challenges in Poland Data Center Construction Market

The Key Drivers propelling the Poland data center construction market are multifaceted. The rapid adoption of cloud computing services by Polish businesses, fueled by the need for scalability and cost-efficiency, is a primary catalyst. The burgeoning IT and Telecommunications sector, driven by 5G network deployment and increasing data traffic, necessitates significant infrastructure expansion. Government initiatives promoting digitalization and technological advancement also play a crucial role. Furthermore, Poland's strategic geographical location in Central Europe makes it an attractive hub for data center investment, offering access to key markets. The demand for high-density computing to support AI, big data, and IoT applications is also a significant growth accelerator.

Conversely, the market faces several Barriers and Challenges. High initial capital expenditure for constructing state-of-the-art data centers remains a significant hurdle, especially for smaller players. Supply chain disruptions, including the availability of specialized components and skilled labor, can lead to project delays and increased costs. Stringent regulatory compliance, particularly concerning environmental standards and energy efficiency, requires careful planning and investment. Rising energy costs and the imperative for sustainable operations present ongoing operational challenges. Additionally, cybersecurity concerns and the need for robust physical security measures add complexity to construction and operational planning. Competition from established European data center hubs also presents a challenge.

Emerging Opportunities in Poland Data Center Construction Market

Emerging opportunities in the Poland data center construction market lie in the growing demand for edge data centers, catering to the increasing need for low-latency processing for IoT devices and real-time applications. The expansion of hyperscale data centers by global cloud providers continues to present significant opportunities for construction and infrastructure development. Furthermore, the increasing focus on sustainability and green energy creates a niche for data centers powered by renewable sources, offering attractive investment prospects. The digitalization of industries like manufacturing and healthcare is also opening doors for customized data center solutions. The development of carrier-neutral colocation facilities that support diverse connectivity options is another burgeoning area.

Growth Accelerators in the Poland Data Center Construction Market Industry

Several catalysts are accelerating long-term growth in the Poland Data Center Construction Market. The continued advancement and widespread adoption of Artificial Intelligence (AI) and Machine Learning (ML) demand massive computing power, directly translating into a need for more advanced data center facilities. Strategic partnerships between construction firms, technology providers, and colocation operators are streamlining project execution and fostering innovation. Market expansion strategies by existing players, including the acquisition of land for future development and the expansion of existing campuses, are key growth drivers. The Polish government's commitment to fostering a digital economy and attracting foreign investment in technology infrastructure further bolsters this growth trajectory. The increasing trend towards hybrid and multi-cloud strategies by enterprises necessitates flexible and interconnected data center ecosystems.

Key Players Shaping the Poland Data Center Construction Market Market

- Per Aarsleff A/S

- Turner & Townsend Limited

- Coolair Equipment Limited

- Johnson Controls International PLC

- IBM Corporation

- Legrand SA

- Bouygues Construction SA

- ALFA LAVAL AB

- Schneider Electric SE

- STULZ GmbH

- DPR CONSTRUCTION INC

- Arup Group Limited

- Kirby Group Engineering

- AECOM

- Coromatic AB Sweden

Notable Milestones in Poland Data Center Construction Market Sector

- December 2022: Atman purchased land, the 5.5-hectare site in Duchnice near Ożarów Mazowiecki, to build another data center. The Atman Data Center Warsaw-3 campus was scheduled to open in Q4 2024 with a target IT capacity of 43 MW.

- August 2022: A recently established colocation facility expanded the Atman Data Center Warsaw-1. The F7 building has a dedicated power capacity of 7.2 MW for customers' IT equipment. The new server rooms of 2,916 sq. m will commission in February 2024.

In-Depth Poland Data Center Construction Market Market Outlook

The future outlook for the Poland Data Center Construction Market is exceptionally robust, driven by persistent demand for digital infrastructure. Growth accelerators such as the pervasive adoption of AI, IoT, and 5G technologies will continue to fuel the need for advanced data center capacity. Strategic investments in new builds and expansions by both domestic and international players, coupled with increasing government support for digitalization, are poised to shape the market. Opportunities in edge computing and sustainable data center solutions will offer new avenues for growth. The market's ability to adapt to evolving technological demands and stringent environmental regulations will be critical for sustained success, positioning Poland as a significant player in the European data center landscape.

Poland Data Center Construction Market Segmentation

-

1. Infrastructure

-

1.1. Market Segmentation - By Electrical Infrastructure

-

1.1.1. Power Distribution Solution

- 1.1.1.1. PDUs - B

-

1.1.1.2. Transfer Switches

- 1.1.1.2.1. Static

- 1.1.1.2.2. Automatic (ATS)

-

1.1.1.3. Switchgear

- 1.1.1.3.1. Low-voltage

- 1.1.1.3.2. Medium-voltage

- 1.1.1.4. Power Panels and Components

- 1.1.1.5. Others

-

1.1.2. Power Backup Solutions

- 1.1.2.1. UPS

- 1.1.2.2. Generators

- 1.1.3. Service

-

1.1.1. Power Distribution Solution

-

1.2. Market Segmentation - By Mechanical Infrastructure

-

1.2.1. Cooling Systems

- 1.2.1.1. Immersion Cooling

- 1.2.1.2. Direct-to-chip Cooling

- 1.2.1.3. Rear Door Heat Exchanger

- 1.2.1.4. In-row and In-rack Cooling

- 1.2.1.5. Other Mechanical Infrastructures

- 1.2.2. Racks

-

1.2.1. Cooling Systems

-

1.1. Market Segmentation - By Electrical Infrastructure

-

2. Electrical Infrastructure

-

2.1. Power Distribution Solution

- 2.1.1. PDUs - B

-

2.1.2. Transfer Switches

- 2.1.2.1. Static

- 2.1.2.2. Automatic (ATS)

-

2.1.3. Switchgear

- 2.1.3.1. Low-voltage

- 2.1.3.2. Medium-voltage

- 2.1.4. Power Panels and Components

- 2.1.5. Others

-

2.2. Power Backup Solutions

- 2.2.1. UPS

- 2.2.2. Generators

- 2.3. Service

-

2.1. Power Distribution Solution

-

3. Power Distribution Solution

- 3.1. PDUs - B

-

3.2. Transfer Switches

- 3.2.1. Static

- 3.2.2. Automatic (ATS)

-

3.3. Switchgear

- 3.3.1. Low-voltage

- 3.3.2. Medium-voltage

- 3.4. Power Panels and Components

- 3.5. Others

-

4. Power Backup Solutions

- 4.1. UPS

- 4.2. Generators

- 5. Service

-

6. Mechanical Infrastructure

-

6.1. Cooling Systems

- 6.1.1. Immersion Cooling

- 6.1.2. Direct-to-chip Cooling

- 6.1.3. Rear Door Heat Exchanger

- 6.1.4. In-row and In-rack Cooling

- 6.1.5. Other Mechanical Infrastructures

- 6.2. Racks

-

6.1. Cooling Systems

-

7. Cooling Systems

- 7.1. Immersion Cooling

- 7.2. Direct-to-chip Cooling

- 7.3. Rear Door Heat Exchanger

- 7.4. In-row and In-rack Cooling

- 7.5. Other Mechanical Infrastructures

- 8. Racks

- 9. Other Mechanical Infrastructures

-

10. Tier Type

- 10.1. Tier-I and-II

- 10.2. Tier-III

- 10.3. Tier-IV

- 11. Tier-I and-II

- 12. Tier-III

- 13. Tier-IV

-

14. End User

- 14.1. Banking, Financial Services, and Insurance

- 14.2. IT and Telecommunications

- 14.3. Government and Defense

- 14.4. Healthcare

- 14.5. Other End Users

- 15. Banking, Financial Services, and Insurance

- 16. IT and Telecommunications

- 17. Government and Defense

- 18. Healthcare

- 19. Other End Users

Poland Data Center Construction Market Segmentation By Geography

- 1. Poland

Poland Data Center Construction Market Regional Market Share

Geographic Coverage of Poland Data Center Construction Market

Poland Data Center Construction Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 5G Developments Fuelling Data Center Investments; Growing Cloud Servce adoption; Green Data Centers rising awarness of Carbon-Neutrality leading to Infrastructure upgrades

- 3.3. Market Restrains

- 3.3.1. Security Challenges Impacting Growth of Data Centers

- 3.4. Market Trends

- 3.4.1. IT and Telecom to have significant market share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Poland Data Center Construction Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Infrastructure

- 5.1.1. Market Segmentation - By Electrical Infrastructure

- 5.1.1.1. Power Distribution Solution

- 5.1.1.1.1. PDUs - B

- 5.1.1.1.2. Transfer Switches

- 5.1.1.1.2.1. Static

- 5.1.1.1.2.2. Automatic (ATS)

- 5.1.1.1.3. Switchgear

- 5.1.1.1.3.1. Low-voltage

- 5.1.1.1.3.2. Medium-voltage

- 5.1.1.1.4. Power Panels and Components

- 5.1.1.1.5. Others

- 5.1.1.2. Power Backup Solutions

- 5.1.1.2.1. UPS

- 5.1.1.2.2. Generators

- 5.1.1.3. Service

- 5.1.1.1. Power Distribution Solution

- 5.1.2. Market Segmentation - By Mechanical Infrastructure

- 5.1.2.1. Cooling Systems

- 5.1.2.1.1. Immersion Cooling

- 5.1.2.1.2. Direct-to-chip Cooling

- 5.1.2.1.3. Rear Door Heat Exchanger

- 5.1.2.1.4. In-row and In-rack Cooling

- 5.1.2.1.5. Other Mechanical Infrastructures

- 5.1.2.2. Racks

- 5.1.2.1. Cooling Systems

- 5.1.1. Market Segmentation - By Electrical Infrastructure

- 5.2. Market Analysis, Insights and Forecast - by Electrical Infrastructure

- 5.2.1. Power Distribution Solution

- 5.2.1.1. PDUs - B

- 5.2.1.2. Transfer Switches

- 5.2.1.2.1. Static

- 5.2.1.2.2. Automatic (ATS)

- 5.2.1.3. Switchgear

- 5.2.1.3.1. Low-voltage

- 5.2.1.3.2. Medium-voltage

- 5.2.1.4. Power Panels and Components

- 5.2.1.5. Others

- 5.2.2. Power Backup Solutions

- 5.2.2.1. UPS

- 5.2.2.2. Generators

- 5.2.3. Service

- 5.2.1. Power Distribution Solution

- 5.3. Market Analysis, Insights and Forecast - by Power Distribution Solution

- 5.3.1. PDUs - B

- 5.3.2. Transfer Switches

- 5.3.2.1. Static

- 5.3.2.2. Automatic (ATS)

- 5.3.3. Switchgear

- 5.3.3.1. Low-voltage

- 5.3.3.2. Medium-voltage

- 5.3.4. Power Panels and Components

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by Power Backup Solutions

- 5.4.1. UPS

- 5.4.2. Generators

- 5.5. Market Analysis, Insights and Forecast - by Service

- 5.6. Market Analysis, Insights and Forecast - by Mechanical Infrastructure

- 5.6.1. Cooling Systems

- 5.6.1.1. Immersion Cooling

- 5.6.1.2. Direct-to-chip Cooling

- 5.6.1.3. Rear Door Heat Exchanger

- 5.6.1.4. In-row and In-rack Cooling

- 5.6.1.5. Other Mechanical Infrastructures

- 5.6.2. Racks

- 5.6.1. Cooling Systems

- 5.7. Market Analysis, Insights and Forecast - by Cooling Systems

- 5.7.1. Immersion Cooling

- 5.7.2. Direct-to-chip Cooling

- 5.7.3. Rear Door Heat Exchanger

- 5.7.4. In-row and In-rack Cooling

- 5.7.5. Other Mechanical Infrastructures

- 5.8. Market Analysis, Insights and Forecast - by Racks

- 5.9. Market Analysis, Insights and Forecast - by Other Mechanical Infrastructures

- 5.10. Market Analysis, Insights and Forecast - by Tier Type

- 5.10.1. Tier-I and-II

- 5.10.2. Tier-III

- 5.10.3. Tier-IV

- 5.11. Market Analysis, Insights and Forecast - by Tier-I and-II

- 5.12. Market Analysis, Insights and Forecast - by Tier-III

- 5.13. Market Analysis, Insights and Forecast - by Tier-IV

- 5.14. Market Analysis, Insights and Forecast - by End User

- 5.14.1. Banking, Financial Services, and Insurance

- 5.14.2. IT and Telecommunications

- 5.14.3. Government and Defense

- 5.14.4. Healthcare

- 5.14.5. Other End Users

- 5.15. Market Analysis, Insights and Forecast - by Banking, Financial Services, and Insurance

- 5.16. Market Analysis, Insights and Forecast - by IT and Telecommunications

- 5.17. Market Analysis, Insights and Forecast - by Government and Defense

- 5.18. Market Analysis, Insights and Forecast - by Healthcare

- 5.19. Market Analysis, Insights and Forecast - by Other End Users

- 5.20. Market Analysis, Insights and Forecast - by Region

- 5.20.1. Poland

- 5.1. Market Analysis, Insights and Forecast - by Infrastructure

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Per Aarsleff A/S

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Turner & Townsend Limited

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Coolair Equipment Limited

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Johnson Controls International PLC

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 IBM Corporation

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Legrand SA

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Bouygues Construction SA

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 ALFA LAVAL AB

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Schneider Electric SE

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 STULZ GmbH

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 DPR CONSTRUCTION INC

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.12 Arup Group Limited

- 6.2.12.1. Overview

- 6.2.12.2. Products

- 6.2.12.3. SWOT Analysis

- 6.2.12.4. Recent Developments

- 6.2.12.5. Financials (Based on Availability)

- 6.2.13 Kirby Group Engineering

- 6.2.13.1. Overview

- 6.2.13.2. Products

- 6.2.13.3. SWOT Analysis

- 6.2.13.4. Recent Developments

- 6.2.13.5. Financials (Based on Availability)

- 6.2.14 AECOM

- 6.2.14.1. Overview

- 6.2.14.2. Products

- 6.2.14.3. SWOT Analysis

- 6.2.14.4. Recent Developments

- 6.2.14.5. Financials (Based on Availability)

- 6.2.15 Coromatic AB Sweden

- 6.2.15.1. Overview

- 6.2.15.2. Products

- 6.2.15.3. SWOT Analysis

- 6.2.15.4. Recent Developments

- 6.2.15.5. Financials (Based on Availability)

- 6.2.1 Per Aarsleff A/S

List of Figures

- Figure 1: Poland Data Center Construction Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Poland Data Center Construction Market Share (%) by Company 2025

List of Tables

- Table 1: Poland Data Center Construction Market Revenue billion Forecast, by Infrastructure 2020 & 2033

- Table 2: Poland Data Center Construction Market Volume K Unit Forecast, by Infrastructure 2020 & 2033

- Table 3: Poland Data Center Construction Market Revenue billion Forecast, by Electrical Infrastructure 2020 & 2033

- Table 4: Poland Data Center Construction Market Volume K Unit Forecast, by Electrical Infrastructure 2020 & 2033

- Table 5: Poland Data Center Construction Market Revenue billion Forecast, by Power Distribution Solution 2020 & 2033

- Table 6: Poland Data Center Construction Market Volume K Unit Forecast, by Power Distribution Solution 2020 & 2033

- Table 7: Poland Data Center Construction Market Revenue billion Forecast, by Power Backup Solutions 2020 & 2033

- Table 8: Poland Data Center Construction Market Volume K Unit Forecast, by Power Backup Solutions 2020 & 2033

- Table 9: Poland Data Center Construction Market Revenue billion Forecast, by Service 2020 & 2033

- Table 10: Poland Data Center Construction Market Volume K Unit Forecast, by Service 2020 & 2033

- Table 11: Poland Data Center Construction Market Revenue billion Forecast, by Mechanical Infrastructure 2020 & 2033

- Table 12: Poland Data Center Construction Market Volume K Unit Forecast, by Mechanical Infrastructure 2020 & 2033

- Table 13: Poland Data Center Construction Market Revenue billion Forecast, by Cooling Systems 2020 & 2033

- Table 14: Poland Data Center Construction Market Volume K Unit Forecast, by Cooling Systems 2020 & 2033

- Table 15: Poland Data Center Construction Market Revenue billion Forecast, by Racks 2020 & 2033

- Table 16: Poland Data Center Construction Market Volume K Unit Forecast, by Racks 2020 & 2033

- Table 17: Poland Data Center Construction Market Revenue billion Forecast, by Other Mechanical Infrastructures 2020 & 2033

- Table 18: Poland Data Center Construction Market Volume K Unit Forecast, by Other Mechanical Infrastructures 2020 & 2033

- Table 19: Poland Data Center Construction Market Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 20: Poland Data Center Construction Market Volume K Unit Forecast, by Tier Type 2020 & 2033

- Table 21: Poland Data Center Construction Market Revenue billion Forecast, by Tier-I and-II 2020 & 2033

- Table 22: Poland Data Center Construction Market Volume K Unit Forecast, by Tier-I and-II 2020 & 2033

- Table 23: Poland Data Center Construction Market Revenue billion Forecast, by Tier-III 2020 & 2033

- Table 24: Poland Data Center Construction Market Volume K Unit Forecast, by Tier-III 2020 & 2033

- Table 25: Poland Data Center Construction Market Revenue billion Forecast, by Tier-IV 2020 & 2033

- Table 26: Poland Data Center Construction Market Volume K Unit Forecast, by Tier-IV 2020 & 2033

- Table 27: Poland Data Center Construction Market Revenue billion Forecast, by End User 2020 & 2033

- Table 28: Poland Data Center Construction Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 29: Poland Data Center Construction Market Revenue billion Forecast, by Banking, Financial Services, and Insurance 2020 & 2033

- Table 30: Poland Data Center Construction Market Volume K Unit Forecast, by Banking, Financial Services, and Insurance 2020 & 2033

- Table 31: Poland Data Center Construction Market Revenue billion Forecast, by IT and Telecommunications 2020 & 2033

- Table 32: Poland Data Center Construction Market Volume K Unit Forecast, by IT and Telecommunications 2020 & 2033

- Table 33: Poland Data Center Construction Market Revenue billion Forecast, by Government and Defense 2020 & 2033

- Table 34: Poland Data Center Construction Market Volume K Unit Forecast, by Government and Defense 2020 & 2033

- Table 35: Poland Data Center Construction Market Revenue billion Forecast, by Healthcare 2020 & 2033

- Table 36: Poland Data Center Construction Market Volume K Unit Forecast, by Healthcare 2020 & 2033

- Table 37: Poland Data Center Construction Market Revenue billion Forecast, by Other End Users 2020 & 2033

- Table 38: Poland Data Center Construction Market Volume K Unit Forecast, by Other End Users 2020 & 2033

- Table 39: Poland Data Center Construction Market Revenue billion Forecast, by Region 2020 & 2033

- Table 40: Poland Data Center Construction Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 41: Poland Data Center Construction Market Revenue billion Forecast, by Infrastructure 2020 & 2033

- Table 42: Poland Data Center Construction Market Volume K Unit Forecast, by Infrastructure 2020 & 2033

- Table 43: Poland Data Center Construction Market Revenue billion Forecast, by Electrical Infrastructure 2020 & 2033

- Table 44: Poland Data Center Construction Market Volume K Unit Forecast, by Electrical Infrastructure 2020 & 2033

- Table 45: Poland Data Center Construction Market Revenue billion Forecast, by Power Distribution Solution 2020 & 2033

- Table 46: Poland Data Center Construction Market Volume K Unit Forecast, by Power Distribution Solution 2020 & 2033

- Table 47: Poland Data Center Construction Market Revenue billion Forecast, by Power Backup Solutions 2020 & 2033

- Table 48: Poland Data Center Construction Market Volume K Unit Forecast, by Power Backup Solutions 2020 & 2033

- Table 49: Poland Data Center Construction Market Revenue billion Forecast, by Service 2020 & 2033

- Table 50: Poland Data Center Construction Market Volume K Unit Forecast, by Service 2020 & 2033

- Table 51: Poland Data Center Construction Market Revenue billion Forecast, by Mechanical Infrastructure 2020 & 2033

- Table 52: Poland Data Center Construction Market Volume K Unit Forecast, by Mechanical Infrastructure 2020 & 2033

- Table 53: Poland Data Center Construction Market Revenue billion Forecast, by Cooling Systems 2020 & 2033

- Table 54: Poland Data Center Construction Market Volume K Unit Forecast, by Cooling Systems 2020 & 2033

- Table 55: Poland Data Center Construction Market Revenue billion Forecast, by Racks 2020 & 2033

- Table 56: Poland Data Center Construction Market Volume K Unit Forecast, by Racks 2020 & 2033

- Table 57: Poland Data Center Construction Market Revenue billion Forecast, by Other Mechanical Infrastructures 2020 & 2033

- Table 58: Poland Data Center Construction Market Volume K Unit Forecast, by Other Mechanical Infrastructures 2020 & 2033

- Table 59: Poland Data Center Construction Market Revenue billion Forecast, by Tier Type 2020 & 2033

- Table 60: Poland Data Center Construction Market Volume K Unit Forecast, by Tier Type 2020 & 2033

- Table 61: Poland Data Center Construction Market Revenue billion Forecast, by Tier-I and-II 2020 & 2033

- Table 62: Poland Data Center Construction Market Volume K Unit Forecast, by Tier-I and-II 2020 & 2033

- Table 63: Poland Data Center Construction Market Revenue billion Forecast, by Tier-III 2020 & 2033

- Table 64: Poland Data Center Construction Market Volume K Unit Forecast, by Tier-III 2020 & 2033

- Table 65: Poland Data Center Construction Market Revenue billion Forecast, by Tier-IV 2020 & 2033

- Table 66: Poland Data Center Construction Market Volume K Unit Forecast, by Tier-IV 2020 & 2033

- Table 67: Poland Data Center Construction Market Revenue billion Forecast, by End User 2020 & 2033

- Table 68: Poland Data Center Construction Market Volume K Unit Forecast, by End User 2020 & 2033

- Table 69: Poland Data Center Construction Market Revenue billion Forecast, by Banking, Financial Services, and Insurance 2020 & 2033

- Table 70: Poland Data Center Construction Market Volume K Unit Forecast, by Banking, Financial Services, and Insurance 2020 & 2033

- Table 71: Poland Data Center Construction Market Revenue billion Forecast, by IT and Telecommunications 2020 & 2033

- Table 72: Poland Data Center Construction Market Volume K Unit Forecast, by IT and Telecommunications 2020 & 2033

- Table 73: Poland Data Center Construction Market Revenue billion Forecast, by Government and Defense 2020 & 2033

- Table 74: Poland Data Center Construction Market Volume K Unit Forecast, by Government and Defense 2020 & 2033

- Table 75: Poland Data Center Construction Market Revenue billion Forecast, by Healthcare 2020 & 2033

- Table 76: Poland Data Center Construction Market Volume K Unit Forecast, by Healthcare 2020 & 2033

- Table 77: Poland Data Center Construction Market Revenue billion Forecast, by Other End Users 2020 & 2033

- Table 78: Poland Data Center Construction Market Volume K Unit Forecast, by Other End Users 2020 & 2033

- Table 79: Poland Data Center Construction Market Revenue billion Forecast, by Country 2020 & 2033

- Table 80: Poland Data Center Construction Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Poland Data Center Construction Market?

The projected CAGR is approximately 21%.

2. Which companies are prominent players in the Poland Data Center Construction Market?

Key companies in the market include Per Aarsleff A/S, Turner & Townsend Limited, Coolair Equipment Limited, Johnson Controls International PLC, IBM Corporation, Legrand SA, Bouygues Construction SA, ALFA LAVAL AB, Schneider Electric SE, STULZ GmbH, DPR CONSTRUCTION INC, Arup Group Limited, Kirby Group Engineering, AECOM, Coromatic AB Sweden.

3. What are the main segments of the Poland Data Center Construction Market?

The market segments include Infrastructure, Electrical Infrastructure, Power Distribution Solution, Power Backup Solutions, Service , Mechanical Infrastructure, Cooling Systems, Racks, Other Mechanical Infrastructures, Tier Type, Tier-I and-II, Tier-III, Tier-IV, End User, Banking, Financial Services, and Insurance, IT and Telecommunications, Government and Defense, Healthcare, Other End Users.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.16 billion as of 2022.

5. What are some drivers contributing to market growth?

5G Developments Fuelling Data Center Investments; Growing Cloud Servce adoption; Green Data Centers rising awarness of Carbon-Neutrality leading to Infrastructure upgrades.

6. What are the notable trends driving market growth?

IT and Telecom to have significant market share.

7. Are there any restraints impacting market growth?

Security Challenges Impacting Growth of Data Centers.

8. Can you provide examples of recent developments in the market?

December 2022: Atman purchased land, the 5.5-hectare site in Duchnice near Ożarów Mazowiecki, to build another data center. The Atman Data Center Warsaw-3 campus was scheduled to open in Q4 2024 with a target IT capacity of 43 MW.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Poland Data Center Construction Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Poland Data Center Construction Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Poland Data Center Construction Market?

To stay informed about further developments, trends, and reports in the Poland Data Center Construction Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence