Key Insights

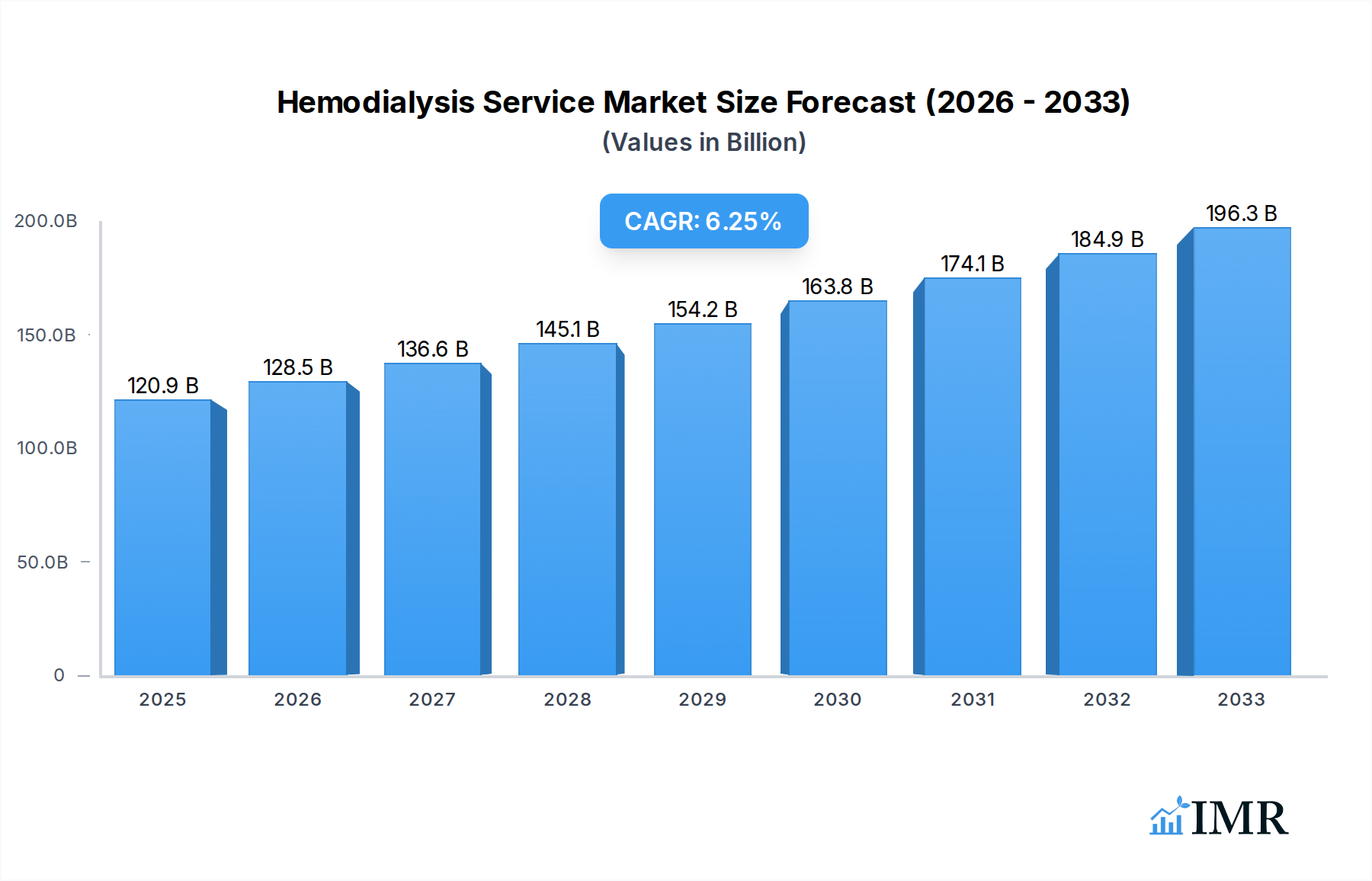

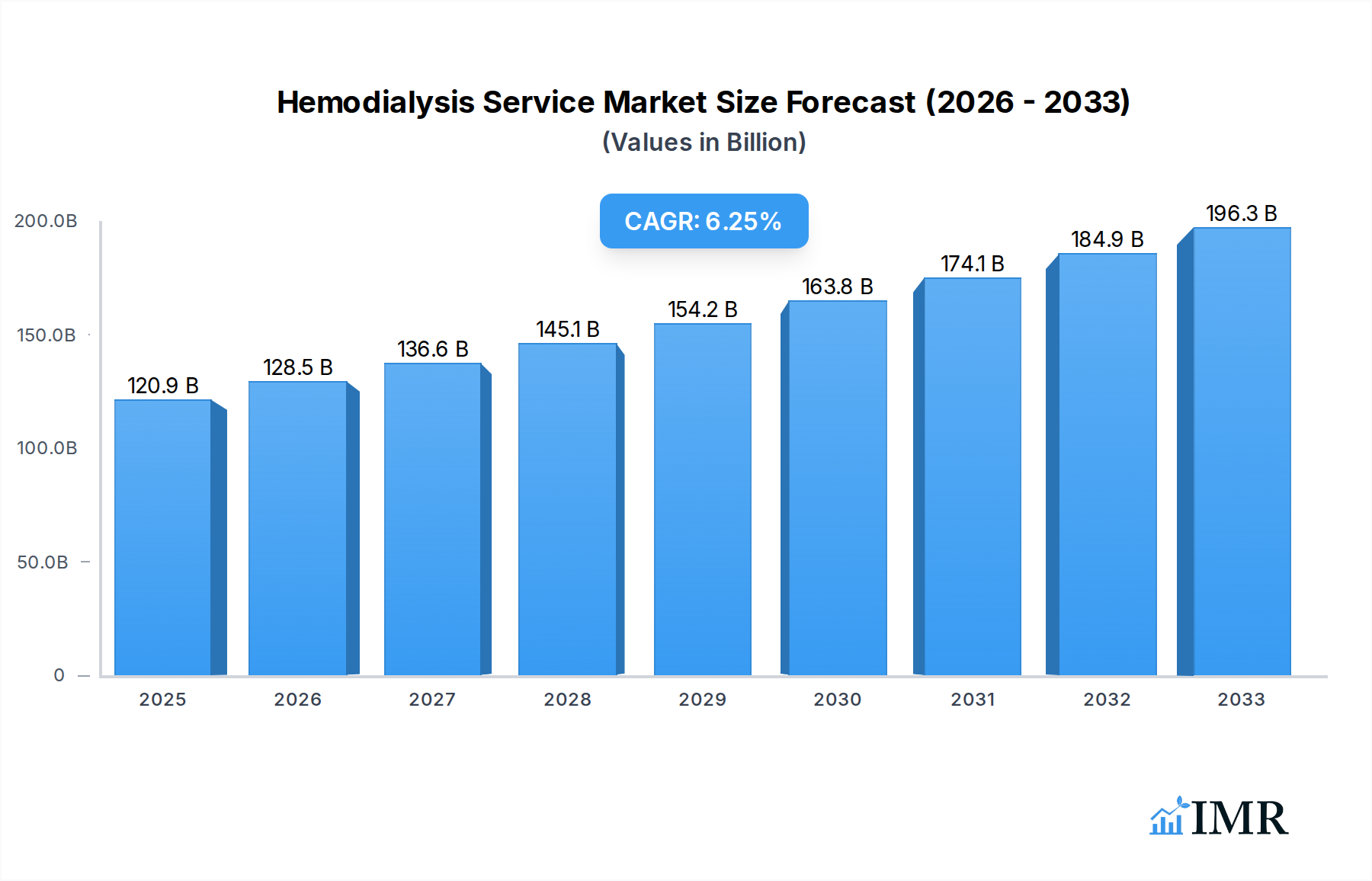

The global hemodialysis service market is poised for substantial expansion, projected to reach USD 120.93 billion by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 6.25% through 2033. This robust growth is primarily fueled by the escalating prevalence of chronic kidney disease (CKD) and end-stage renal disease (ESRD) globally, driven by factors such as the rising incidence of diabetes, hypertension, and an aging population. The increasing demand for convenient and accessible dialysis treatments, particularly in outpatient settings like dialysis centers, is a significant market driver. Furthermore, advancements in dialysis technology, including the development of more efficient and patient-friendly machines, coupled with a growing awareness of kidney health, are contributing to market expansion. Geographically, the Asia Pacific region is expected to witness the fastest growth due to a large and growing patient pool, improving healthcare infrastructure, and increasing disposable incomes, which allow for greater healthcare spending.

Hemodialysis Service Market Size (In Billion)

While the market is propelled by strong demand and technological innovation, certain factors present challenges. The high cost of dialysis treatment and the associated healthcare expenses can be a restraining factor for a segment of the population. Moreover, the shortage of skilled healthcare professionals specializing in nephrology and dialysis care could impede the seamless delivery of services, particularly in underserved regions. Despite these restraints, the continuous efforts by healthcare providers and manufacturers to enhance treatment accessibility, improve patient outcomes, and develop innovative solutions are expected to mitigate these challenges. The market segmentation by application, including hospitals and standalone dialysis centers, along with the distinction between acute and chronic hemodialysis, highlights the diverse needs and service offerings within this vital healthcare sector, all contributing to the overall positive market trajectory.

Hemodialysis Service Company Market Share

Here's a comprehensive, SEO-optimized report description for the Hemodialysis Service Market, designed for maximum visibility and industry engagement.

Hemodialysis Service Market Dynamics & Structure

The global hemodialysis service market is a complex and dynamic ecosystem, characterized by a moderate to high concentration of key players. Leading companies like Fresenius, Baxter, US Renal Care, and DaVita command significant market share, driven by extensive clinical networks and robust technological investments. Technological innovation remains a paramount driver, with advancements in dialysis machine efficiency, water purification systems, and patient monitoring technologies constantly pushing the boundaries of care. Regulatory frameworks, established by bodies such as the FDA and EMA, play a crucial role in ensuring patient safety and service quality, influencing market entry and operational standards. Competitive product substitutes, while nascent, include peritoneal dialysis and emerging home-based dialysis solutions, necessitating continuous innovation in hemodialysis services to maintain their competitive edge. End-user demographics are predominantly driven by the rising incidence of chronic kidney disease (CKD) and end-stage renal disease (ESRD) globally, particularly among aging populations and individuals with co-morbidities like diabetes and hypertension. Mergers and acquisitions (M&A) trends continue to shape the landscape, with larger entities acquiring smaller providers to expand geographical reach and service offerings. For instance, the historical period (2019-2024) saw several strategic consolidations aimed at optimizing operational efficiencies and increasing patient access.

- Market Concentration: Dominated by a few major global players, with increasing consolidation through M&A activities.

- Technological Innovation: Driven by advancements in dialysis machinery, AI-powered monitoring, and remote patient care solutions.

- Regulatory Frameworks: Strict oversight from health authorities ensures quality and safety, impacting operational costs and service delivery.

- Competitive Product Substitutes: Peritoneal dialysis and emerging home dialysis technologies present challenges and opportunities for innovation.

- End-User Demographics: Aging global population and increasing prevalence of chronic diseases like diabetes and hypertension are key growth drivers.

- M&A Trends: Strategic acquisitions and partnerships are prevalent, aiming for market expansion and service portfolio enhancement.

Hemodialysis Service Growth Trends & Insights

The global hemodialysis service market is poised for substantial growth, driven by an aging global population, a rising prevalence of chronic kidney disease (CKD) and end-stage renal disease (ESRD), and continuous advancements in medical technology. The study period from 2019 to 2033, with a base year of 2025, projects a significant market size evolution. In the historical period (2019-2024), the market demonstrated a steady upward trajectory, fueled by increased awareness of kidney health and improved access to diagnostic tools. The base year of 2025 is estimated to represent a market value of approximately $55.7 billion. Looking ahead to the forecast period of 2025-2033, a projected Compound Annual Growth Rate (CAGR) of around 5.2% is anticipated. This growth is underpinned by several key trends. Firstly, the increasing incidence of co-morbidities such as diabetes and hypertension, which are primary risk factors for CKD, is a major catalyst. As these conditions become more prevalent, the demand for kidney replacement therapies, including hemodialysis, naturally escalates. Secondly, technological disruptions are revolutionizing dialysis delivery. Innovations in hemodialysis machines, such as portable and user-friendly devices, are enabling more in-home treatments, thereby enhancing patient convenience and potentially reducing healthcare system burdens. The integration of artificial intelligence (AI) and machine learning (ML) for real-time patient monitoring and predictive analytics is further optimizing treatment protocols and improving patient outcomes. Consumer behavior shifts are also contributing to market expansion. Patients are increasingly seeking personalized treatment plans and greater autonomy in managing their health. This has led to a surge in demand for outpatient dialysis centers and home dialysis services, which offer greater flexibility and comfort compared to traditional in-center treatments. The expansion of healthcare infrastructure in emerging economies is also playing a pivotal role, extending access to essential dialysis services to previously underserved populations. Market penetration is expected to deepen as healthcare systems in developing nations continue to invest in chronic disease management and renal care. The estimated market size for 2033 is projected to reach approximately $83.5 billion.

- Market Size Evolution: The global hemodialysis service market is projected to grow from an estimated $55.7 billion in 2025 to $83.5 billion by 2033.

- Adoption Rates: Increasing adoption of home hemodialysis and advanced in-center services driven by patient preference and technological advancements.

- Technological Disruptions: Integration of AI, IoT, and portable dialysis machines are reshaping service delivery and patient experience.

- Consumer Behavior Shifts: Growing demand for personalized care, convenience, and greater patient autonomy in treatment management.

- Market Penetration: Expansion into emerging economies and increased focus on managing chronic diseases are driving deeper market penetration.

- CAGR: A projected Compound Annual Growth Rate (CAGR) of approximately 5.2% from 2025 to 2033.

Dominant Regions, Countries, or Segments in Hemodialysis Service

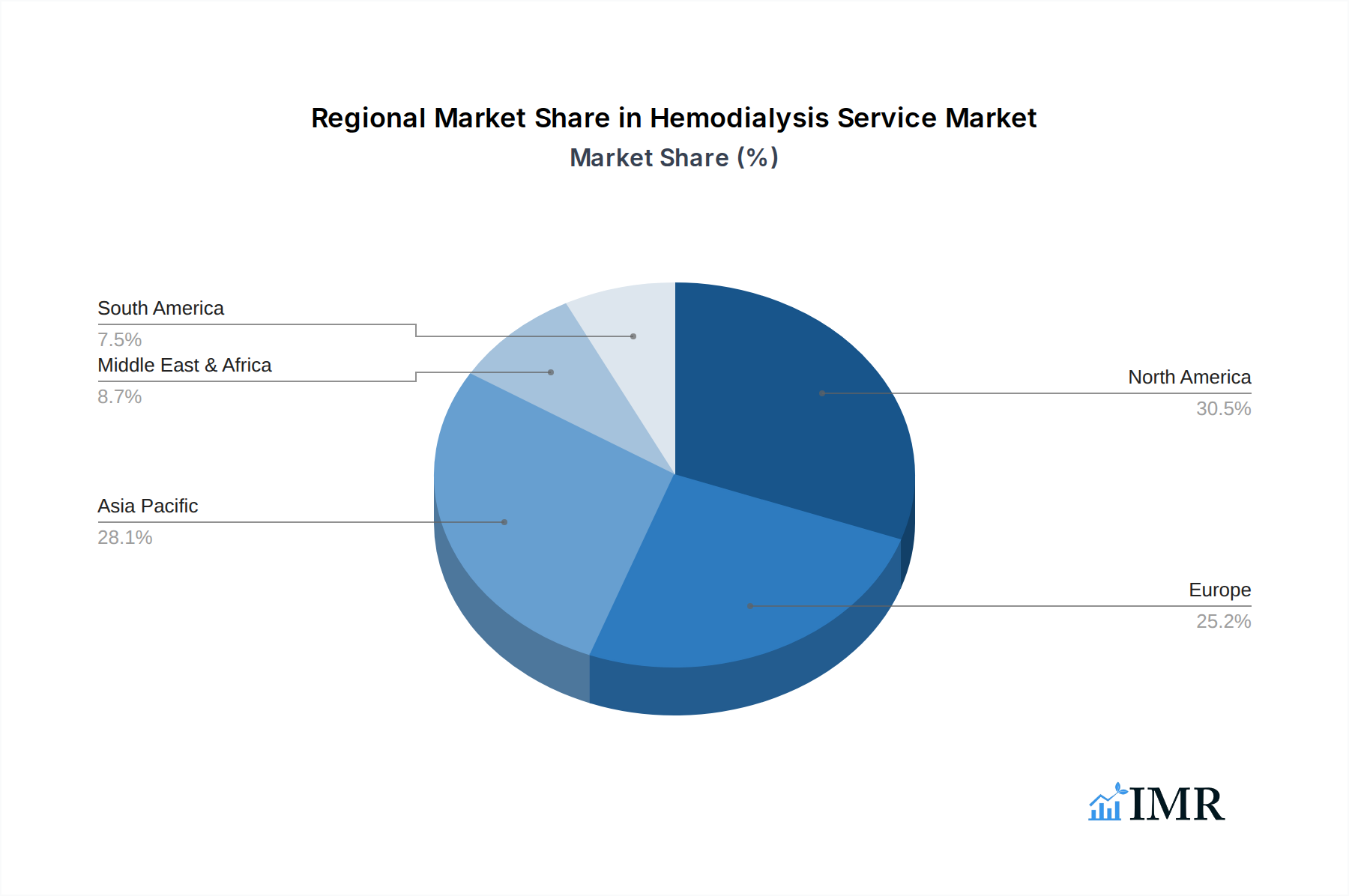

The hemodialysis service market exhibits significant regional variations in growth and adoption, with North America and Europe currently leading the charge. However, the Asia-Pacific region, particularly countries like China and India, is emerging as a rapid growth engine. Within the segmentation of Applications, Dialysis Centers represent the most dominant segment, accounting for approximately 65% of the global market share in 2025. This dominance stems from their specialized infrastructure, dedicated staff, and established protocols for delivering consistent and high-quality hemodialysis treatments. Hospitals, while crucial for acute hemodialysis and complex cases, constitute the second-largest segment at around 28%, with "Others" (including home dialysis setups and specialized clinics) making up the remaining 7%. In terms of Types of Hemodialysis, Chronic Hemodialysis overwhelmingly leads, driven by the rising global burden of chronic kidney disease (CKD). Chronic hemodialysis services are projected to hold over 90% of the market share in 2025, reflecting the long-term nature of treatment for most renal patients. Acute Hemodialysis, primarily used for temporary kidney support in critical care settings, accounts for the remaining portion. The dominance of North America is attributed to a strong healthcare infrastructure, high disposable incomes, advanced technological adoption, and a robust reimbursement system. The United States, in particular, is a powerhouse, with a high prevalence of ESRD and a well-established network of dialysis providers. European countries like Germany, the UK, and France also contribute significantly due to their universal healthcare systems and proactive management of chronic diseases. The Asia-Pacific region's ascendancy is propelled by a burgeoning middle class, increasing healthcare expenditure, a rapidly growing elderly population, and a substantial unmet need for renal care. Countries such as China, with its vast population and rising CKD rates, are experiencing exponential growth in demand for hemodialysis services. The strategic investments by global players like Fresenius and Baxter in this region, coupled with local manufacturing capabilities, are further accelerating market expansion. The development of localized dialysis centers and the increasing acceptance of home dialysis solutions in these regions are key drivers of this growth. Economic policies that prioritize public health and the expansion of healthcare insurance coverage are instrumental in facilitating access to these life-sustaining treatments.

- Dominant Application Segment: Dialysis Centers, holding approximately 65% of the market share in 2025, are the primary providers of hemodialysis services.

- Secondary Application Segment: Hospitals, crucial for acute care, represent about 28% of the market.

- Dominant Type Segment: Chronic Hemodialysis accounts for over 90% of the market share in 2025, reflecting the prevalence of long-term kidney disease.

- Leading Region: North America, particularly the United States, leads in market share due to advanced infrastructure and high prevalence of ESRD.

- Rapid Growth Region: Asia-Pacific, especially China and India, is experiencing significant growth due to rising healthcare expenditure and increasing CKD incidence.

- Key Drivers in Dominant Regions: Strong healthcare infrastructure, advanced technology adoption, favorable reimbursement policies, and a growing aging population.

Hemodialysis Service Product Landscape

The product landscape within hemodialysis services is characterized by continuous innovation focused on enhancing patient outcomes, improving treatment efficiency, and increasing patient comfort. Key product innovations include next-generation hemodialysis machines offering more compact designs, improved user interfaces, and advanced monitoring capabilities. Water purification systems are also seeing advancements, with more sophisticated technologies ensuring ultra-pure water essential for dialysis. Wearable and portable dialysis devices are emerging as significant disruptors, promising greater patient mobility and the potential for home-based dialysis. These innovations aim to reduce the burden of disease and improve the quality of life for individuals with kidney failure. Performance metrics are increasingly focused on dialyzer efficiency, biocompatibility of membranes, and the ability of machines to adapt to individual patient needs. Unique selling propositions of leading providers often revolve around integrated care models, advanced technological integration, and patient-centric service delivery.

Key Drivers, Barriers & Challenges in Hemodialysis Service

Key Drivers: The hemodialysis service market is propelled by several key drivers. The escalating global prevalence of chronic kidney disease (CKD) and end-stage renal disease (ESRD), largely driven by an aging population and the rise of diabetes and hypertension, is the most significant factor. Technological advancements in dialysis machines, water purification systems, and remote patient monitoring enhance treatment efficacy and patient convenience. Government initiatives and increasing healthcare expenditure, particularly in emerging economies, are expanding access to renal care. Furthermore, growing patient awareness and demand for better quality of life are encouraging the adoption of more advanced and convenient dialysis solutions, including home hemodialysis.

Barriers & Challenges: Despite its growth potential, the market faces several challenges. High operational costs associated with dialysis centers, including staffing, equipment maintenance, and consumables, pose a significant barrier. Reimbursement policies and pricing pressures from healthcare payers can impact profitability. Stringent regulatory requirements for dialysis equipment and services add to compliance costs and complexities. The shortage of skilled healthcare professionals, including nephrologists and dialysis technicians, remains a critical concern. Moreover, the risk of infections and complications associated with dialysis treatments necessitates continuous vigilance and investment in safety protocols. Supply chain disruptions for essential components and consumables can also impact service delivery.

Emerging Opportunities in Hemodialysis Service

Emerging opportunities in the hemodialysis service market are largely centered around technological innovation and expanding access to care. The development and wider adoption of home hemodialysis technologies present a significant opportunity to improve patient convenience and reduce healthcare system costs. Advancements in wearable or portable dialysis devices could revolutionize treatment delivery, offering unprecedented mobility to patients. Telehealth and remote patient monitoring solutions are poised to enhance care management, allowing for more proactive interventions and personalized treatment adjustments. Furthermore, the untapped market potential in developing countries, where the burden of kidney disease is rising but access to advanced care is limited, offers substantial growth prospects for providers and manufacturers willing to invest in these regions. Personalized medicine approaches, leveraging AI and data analytics to tailor dialysis treatments to individual patient profiles, represent another promising avenue for innovation and improved patient outcomes.

Growth Accelerators in the Hemodialysis Service Industry

Several catalysts are accelerating long-term growth in the hemodialysis service industry. Technological breakthroughs, such as the development of more efficient and user-friendly dialysis machines, alongside advancements in artificial kidney technologies, are poised to redefine treatment modalities. Strategic partnerships between dialysis providers, medical device manufacturers, and pharmaceutical companies are fostering innovation and expanding service offerings. Market expansion strategies, particularly focusing on underserved regions and the growing demand for home-based dialysis solutions, are crucial growth accelerators. The increasing global focus on preventative healthcare and early detection of kidney disease, coupled with supportive government policies and improved insurance coverage for renal care, will further fuel market expansion. The growing trend towards value-based care models is also encouraging providers to focus on optimizing patient outcomes and operational efficiency, thereby driving innovation and service enhancement.

Key Players Shaping the Hemodialysis Service Market

- Fresenius Medical Care

- Baxter International Inc.

- US Renal Care

- DaVita Inc.

- Mayo Clinic

- American Renal Associates

- Bangkok Hospital

- Halton Healthcare

- Dialysis Clinic, Inc.

- WEGO

- 3SBio Group

- Dakang Medical

- Shinva Medical

Notable Milestones in Hemodialysis Service Sector

- 2019: Fresenius Medical Care launches the 6008 CARE system, enhancing efficiency and patient comfort in hemodialysis.

- 2020: Baxter International receives FDA clearance for its VIVIDAS Hemodialysis System, introducing advanced monitoring capabilities.

- 2021: US Renal Care expands its network through strategic acquisitions, increasing its patient reach in key U.S. regions.

- 2022: DaVita Inc. invests heavily in telehealth and remote patient monitoring technologies to improve chronic care management.

- 2023: The Mayo Clinic reports significant progress in research for wearable artificial kidney devices, signaling future treatment possibilities.

- 2024: American Renal Associates announces expansion into new international markets, broadening its global footprint.

In-Depth Hemodialysis Service Market Outlook

The future of the hemodialysis service market is exceptionally promising, driven by a confluence of demographic shifts, technological advancements, and evolving healthcare paradigms. Growth accelerators such as the increasing global prevalence of kidney disease, coupled with supportive government policies and expanding healthcare infrastructure in emerging economies, will continue to fuel market expansion. The anticipated market size of $83.5 billion by 2033 underscores this robust growth trajectory. Strategic opportunities lie in the widespread adoption of home hemodialysis, the development of more sophisticated AI-driven diagnostic and monitoring tools, and the exploration of personalized treatment approaches. Companies that can effectively navigate regulatory landscapes, foster innovation, and prioritize patient-centric care will be well-positioned to capitalize on the significant growth potential in this vital sector of healthcare.

Hemodialysis Service Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Dialysis Center

- 1.3. Others

-

2. Types

- 2.1. Acute Hemodialysis

- 2.2. Chronic Hemodialysis

Hemodialysis Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Hemodialysis Service Regional Market Share

Geographic Coverage of Hemodialysis Service

Hemodialysis Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.25% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Hemodialysis Service Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Dialysis Center

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Acute Hemodialysis

- 5.2.2. Chronic Hemodialysis

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Hemodialysis Service Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Dialysis Center

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Acute Hemodialysis

- 6.2.2. Chronic Hemodialysis

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Hemodialysis Service Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Dialysis Center

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Acute Hemodialysis

- 7.2.2. Chronic Hemodialysis

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Hemodialysis Service Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Dialysis Center

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Acute Hemodialysis

- 8.2.2. Chronic Hemodialysis

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Hemodialysis Service Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Dialysis Center

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Acute Hemodialysis

- 9.2.2. Chronic Hemodialysis

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Hemodialysis Service Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Dialysis Center

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Acute Hemodialysis

- 10.2.2. Chronic Hemodialysis

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Fresenius

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Baxter

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 US Renal Care

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 DaVita

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Mayo Clinic

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 American Renal Associates

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Bangkok Hospital

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Halton Healthcare

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Dialysis Clinic

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 WEGO

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 3SBio Group

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Dakang Medical

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Shinva Medical

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Fresenius

List of Figures

- Figure 1: Global Hemodialysis Service Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Hemodialysis Service Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Hemodialysis Service Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Hemodialysis Service Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Hemodialysis Service Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Hemodialysis Service Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Hemodialysis Service Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Hemodialysis Service Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Hemodialysis Service Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Hemodialysis Service Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Hemodialysis Service Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Hemodialysis Service Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Hemodialysis Service Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Hemodialysis Service Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Hemodialysis Service Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Hemodialysis Service Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Hemodialysis Service Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Hemodialysis Service Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Hemodialysis Service Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Hemodialysis Service Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Hemodialysis Service Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Hemodialysis Service Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Hemodialysis Service Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Hemodialysis Service Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Hemodialysis Service Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Hemodialysis Service Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Hemodialysis Service Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Hemodialysis Service Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Hemodialysis Service Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Hemodialysis Service Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Hemodialysis Service Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Hemodialysis Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Hemodialysis Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Hemodialysis Service Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Hemodialysis Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Hemodialysis Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Hemodialysis Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Hemodialysis Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Hemodialysis Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Hemodialysis Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Hemodialysis Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Hemodialysis Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Hemodialysis Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Hemodialysis Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Hemodialysis Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Hemodialysis Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Hemodialysis Service Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Hemodialysis Service Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Hemodialysis Service Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Hemodialysis Service Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Hemodialysis Service?

The projected CAGR is approximately 6.25%.

2. Which companies are prominent players in the Hemodialysis Service?

Key companies in the market include Fresenius, Baxter, US Renal Care, DaVita, Mayo Clinic, American Renal Associates, Bangkok Hospital, Halton Healthcare, Dialysis Clinic, WEGO, 3SBio Group, Dakang Medical, Shinva Medical.

3. What are the main segments of the Hemodialysis Service?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Hemodialysis Service," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Hemodialysis Service report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Hemodialysis Service?

To stay informed about further developments, trends, and reports in the Hemodialysis Service, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence