Key Insights

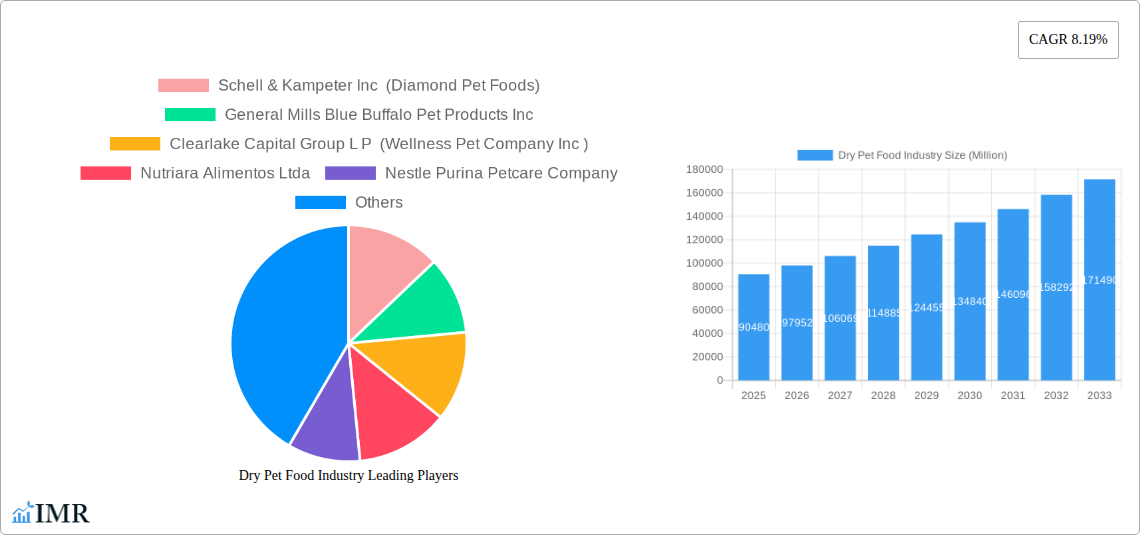

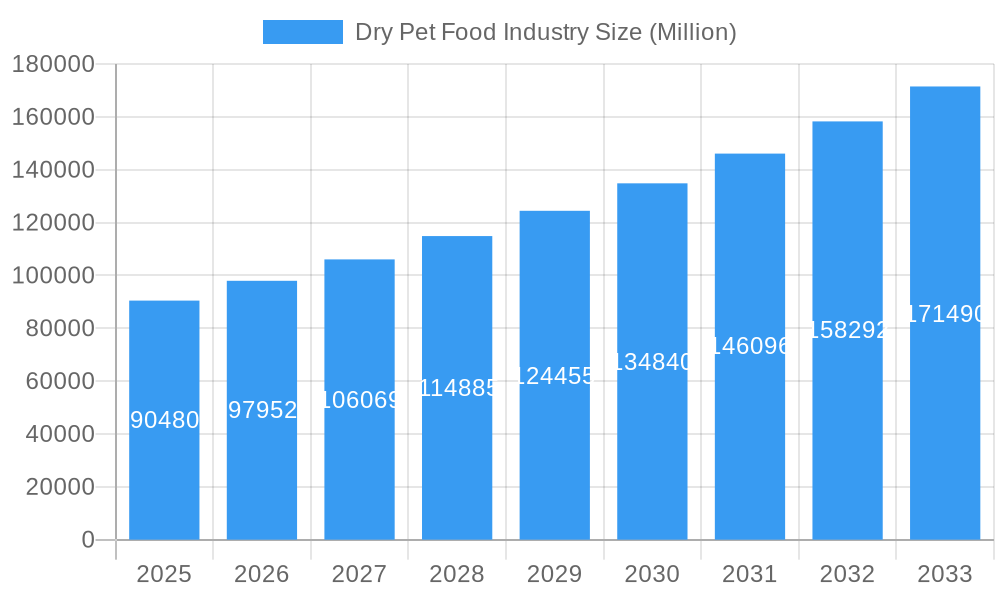

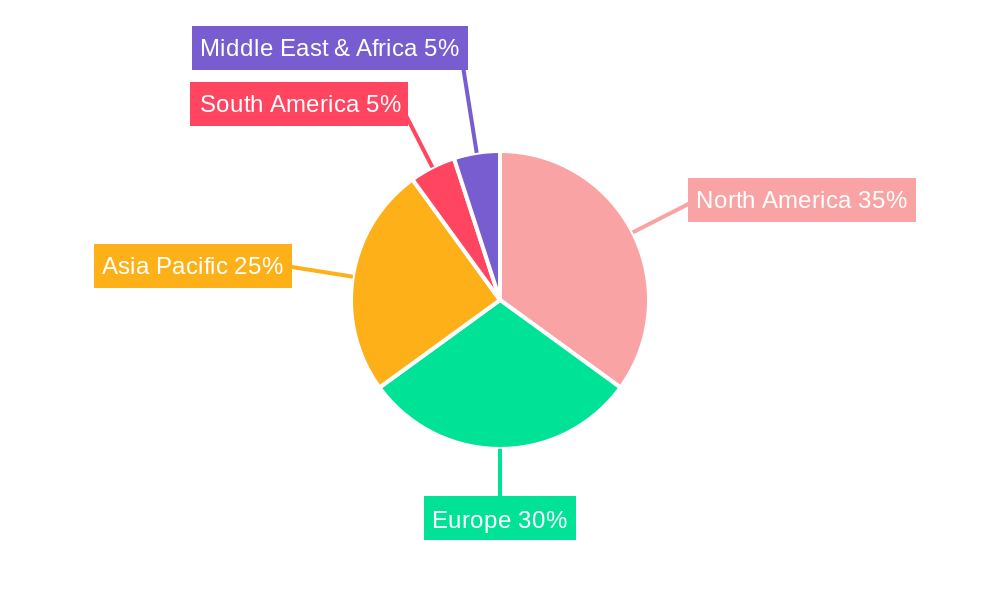

The global dry pet food market, valued at $90.48 billion in 2025, is poised for robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 8.19% from 2025 to 2033. This expansion is driven by several key factors. The increasing humanization of pets fuels higher spending on premium dry food options, reflecting a growing awareness of pet health and nutrition. Convenience, a crucial factor for busy pet owners, also contributes significantly to the market's growth. The rise of e-commerce platforms provides easy access to a wider variety of products, further boosting sales. Furthermore, innovation in ingredient sourcing, with a focus on natural and functional ingredients such as high-protein options and specific dietary needs catering to allergies or sensitivities, is shaping consumer preferences and driving market segmentation. The market's regional distribution reflects developed economies' higher pet ownership rates and disposable incomes, with North America and Europe holding substantial market share. However, developing economies in Asia-Pacific are also experiencing significant growth, fueled by rising middle-class incomes and increased pet adoption.

Dry Pet Food Industry Market Size (In Billion)

The market is segmented by animal type (dogs, cats, others), product type (kibble, others), ingredient type (protein, plant-derived, others), and distribution channel (specialized pet shops, online channels, supermarkets/hypermarkets, others). The dog food segment currently dominates, but the cat food segment is experiencing strong growth. Kibble remains the leading product type due to cost-effectiveness and convenience. However, the demand for specialized dry pet food catering to specific dietary requirements and life stages is steadily increasing. Online channels are experiencing rapid growth as a distribution channel, challenging traditional retail outlets. While established players like Nestlé Purina PetCare, Mars Inc., and Hill's Pet Nutrition hold significant market share, smaller niche players focusing on specialized ingredients and dietary needs are gaining traction. Regulatory changes focusing on pet food safety and labeling will continue to influence market dynamics in the coming years.

Dry Pet Food Industry Company Market Share

Dry Pet Food Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the global dry pet food industry, encompassing market dynamics, growth trends, regional performance, product landscapes, and key players. With a focus on the period 2019-2033 (Base Year: 2025, Forecast Period: 2025-2033), this report is an essential resource for industry professionals, investors, and anyone seeking to understand this dynamic sector. Market values are presented in million units.

Dry Pet Food Industry Market Dynamics & Structure

The global dry pet food market is characterized by a moderately consolidated structure, with key players holding significant market share. Technological innovation, particularly in ingredient formulation and manufacturing processes, is a major driver. Stringent regulatory frameworks concerning pet food safety and labeling influence market operations. Competitive pressures arise from substitutes like wet food and homemade diets. The growing pet-owning population, especially in developing economies, fuels demand. Mergers and acquisitions (M&A) activity is relatively frequent, with larger players seeking to expand their product portfolios and geographic reach. In 2024, approximately xx M&A deals were recorded, representing a xx% increase from the previous year. Larger players hold approximately 60% of the market share collectively.

- Market Concentration: Moderately consolidated, with top 10 players accounting for approximately 60% market share in 2024.

- Technological Innovation: Focus on novel protein sources, functional ingredients, and sustainable packaging.

- Regulatory Landscape: Stringent regulations regarding food safety, labeling, and ingredient sourcing.

- Competitive Substitutes: Wet pet food, raw food diets, and homemade pet food.

- End-User Demographics: Increasing pet ownership, particularly in emerging markets, drives market growth.

- M&A Activity: Significant M&A activity observed in recent years, consolidating market share. Innovation barriers include high R&D costs and stringent regulations.

Dry Pet Food Industry Growth Trends & Insights

The global dry pet food market experienced robust growth during the historical period (2019-2024). The market size reached xx million units in 2024, exhibiting a CAGR of xx% during this period. This growth is attributed to increasing pet ownership, rising disposable incomes, and shifting consumer preferences towards convenient and nutritionally balanced pet food options. Technological advancements, such as the introduction of novel protein sources and customized formulations, further fueled market expansion. Consumer behavior shifts towards premiumization and functional pet food are also impacting market growth. The forecast period (2025-2033) is projected to witness continued growth, driven by similar factors. Market penetration is expected to reach xx% by 2033, with a forecasted CAGR of xx%.

Dominant Regions, Countries, or Segments in Dry Pet Food Industry

North America and Europe currently dominate the dry pet food market, driven by high pet ownership rates and strong consumer spending on pet care. Within these regions, the United States and Germany, respectively, are leading national markets. In terms of segments, the Dog segment commands the largest market share due to higher pet ownership compared to cats and other animals. Kibble remains the dominant product type, while protein-based ingredients are highly sought after. Supermarkets/hypermarkets constitute the primary distribution channel, followed by specialized pet shops and online channels.

- Key Drivers (North America): High pet ownership, strong consumer spending on pet care, and established pet food industry infrastructure.

- Key Drivers (Europe): Increasing humanization of pets, growing awareness of pet health and nutrition, and strong regulatory frameworks.

- Segment Dominance: Dogs (Market Share: xx%), Kibble (Market Share: xx%), Protein-based ingredients (Market Share: xx%), Supermarkets/Hypermarkets (Market Share: xx%).

Dry Pet Food Industry Product Landscape

The dry pet food industry is witnessing robust product innovation driven by a deep understanding of pet well-being and owner expectations. Current formulations are meticulously crafted to enhance nutritional value, maximize palatability, and optimize digestibility. A significant trend involves the incorporation of novel protein sources, such as fish, lamb, and venison, alongside the integration of cutting-edge functional ingredients like probiotics, prebiotics, and Omega-3 fatty acids for gut health and a lustrous coat. Tailored nutritional profiles designed for specific life stages (puppy, adult, senior), breed sizes, and common health conditions (e.g., weight management, sensitive stomachs) are increasingly popular. Beyond the kibble itself, manufacturers are placing a strong emphasis on sustainability, with a growing commitment to eco-friendly packaging solutions and environmentally responsible production processes. The core selling propositions continue to revolve around demonstrable benefits such as improved digestive health, enhanced coat and skin condition, and precisely formulated diets that address individual pet needs. Advancements in extrusion technology and other sophisticated processing techniques are instrumental in creating superior textures, preserving nutrient integrity, and developing advanced nutritional profiles that cater to the evolving demands of discerning pet owners.

Key Drivers, Barriers & Challenges in Dry Pet Food Industry

Key Drivers: Rising pet ownership, increasing disposable incomes in emerging markets, growing awareness of pet health and nutrition, and technological advancements in pet food formulations and manufacturing.

Challenges: Fluctuations in raw material prices, stringent regulatory requirements, intense competition, and supply chain disruptions due to geopolitical events. These factors can lead to increased production costs and potential price increases, impacting market dynamics. Supply chain disruptions during the period 2020-2022 caused a xx% increase in production costs.

Emerging Opportunities in Dry Pet Food Industry

The dry pet food industry is ripe with emerging opportunities, primarily fueled by the escalating demand for highly specialized pet food products. This includes a burgeoning segment catering to pets with specific dietary requirements, such as grain-free options, limited-ingredient diets for pets with allergies or sensitivities, and veterinary-prescribed therapeutic foods. The market for organically certified and sustainably sourced pet food continues its significant growth trajectory, reflecting a broader consumer shift towards ethical and environmentally conscious purchasing decisions. Furthermore, the pervasive rise of e-commerce has democratized access and distribution, opening up new and lucrative channels for both established manufacturers and agile startups to reach consumers directly. The increasing adoption of personalized nutrition strategies, where diets are customized based on a pet's unique DNA, lifestyle, and health data, presents a transformative frontier. Additionally, the development and integration of innovative, alternative protein sources, such as insect-based proteins and cultivated meat, are poised to address sustainability concerns and offer novel nutritional benefits.

Growth Accelerators in the Dry Pet Food Industry

Several potent forces are accelerating growth within the dry pet food industry. Technological breakthroughs across the entire value chain, from sophisticated ingredient sourcing and development to advanced processing techniques like freeze-drying and precision extrusion, are continually enhancing product quality and appeal. The burgeoning field of personalized nutrition, leveraging data analytics and veterinary insights, is creating a new paradigm for tailored pet diets. Strategic collaborations and partnerships between pet food manufacturers, innovative ingredient suppliers, and research institutions are crucial for fostering a dynamic ecosystem that drives product development and market penetration. Expansion into emerging economies, characterized by rising disposable incomes and increasing pet ownership rates, represents a significant avenue for market growth. The ongoing evolution and widespread adoption of e-commerce platforms and direct-to-consumer (DTC) sales models are further amplifying reach, facilitating customer engagement, and driving sales volume by offering convenience and personalized shopping experiences.

Key Players Shaping the Dry Pet Food Industry Market

- Schell & Kampeter Inc (Diamond Pet Foods) - Website

- General Mills Blue Buffalo Pet Products Inc - Website

- Clearlake Capital Group L P (Wellness Pet Company Inc) - Website

- Nutriara Alimentos Ltda

- Nestle Purina Petcare Company - Website

- Alltech Inc

- Archer Daniels Midland - Website

- Colgate-Palmolive Company (Hill's Pet Nutrition Inc) - Website

- Mars Inc - Website

- The JM Smucker Company - Website

Notable Milestones in Dry Pet Food Industry Sector

- 2020-Q3: A significant surge in pet food demand was observed globally, largely attributed to pandemic-related lockdowns, increased time spent at home, and a heightened focus on pet well-being. This period also saw a rise in e-commerce purchases for pet supplies.

- 2021-Q1: A wave of new product launches focused on sustainability and organic ingredients emerged from several key industry players, signaling a growing commitment to environmentally conscious and healthier pet food options.

- 2022-Q4: The dry pet food industry experienced a notable uptick in merger and acquisition (M&A) activity, with larger corporations acquiring innovative startups and established brands to expand their portfolios and market reach.

- 2023-Q2: The sector witnessed the introduction of several groundbreaking pet food products that incorporated novel protein sources, such as insect protein and plant-based alternatives, alongside advanced functional ingredients designed to support specific health benefits.

In-Depth Dry Pet Food Industry Market Outlook

The future of the dry pet food market looks promising, with continued growth driven by factors such as increasing pet ownership, rising disposable incomes, and ongoing product innovation. Strategic opportunities exist in expanding into emerging markets, developing sustainable and personalized pet food products, and leveraging digital channels to enhance customer reach and engagement. The focus on premiumization and the incorporation of functional ingredients are expected to drive further market growth in the years to come.

Dry Pet Food Industry Segmentation

-

1. Animal Type

- 1.1. Dogs

- 1.2. Cats

- 1.3. Other Animals

-

2. Product Type

- 2.1. Kibble

- 2.2. Other Product Types

-

3. Ingredient Type

-

3.1. Protien

- 3.1.1. Animal-derived

- 3.1.2. Plant-derived

- 3.2. Cereals and Cereal Derivatives

- 3.3. Other Ingredient Types

-

3.1. Protien

-

4. Distribution Channel

- 4.1. Specialized Pet Shops

- 4.2. Online Channels

- 4.3. Supermarkets/Hypermarkets

- 4.4. Other Distribution Channels

Dry Pet Food Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Russia

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. India

- 3.2. China

- 3.3. Japan

- 3.4. Australia

- 3.5. Rest of Asia Pacific

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

- 5. Middle East

-

6. South Africa

- 6.1. United Arab Emirates

- 6.2. Saudi Arabia

- 6.3. Rest of Middle East

Dry Pet Food Industry Regional Market Share

Geographic Coverage of Dry Pet Food Industry

Dry Pet Food Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.19% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Animal Type

- 5.1.1. Dogs

- 5.1.2. Cats

- 5.1.3. Other Animals

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Kibble

- 5.2.2. Other Product Types

- 5.3. Market Analysis, Insights and Forecast - by Ingredient Type

- 5.3.1. Protien

- 5.3.1.1. Animal-derived

- 5.3.1.2. Plant-derived

- 5.3.2. Cereals and Cereal Derivatives

- 5.3.3. Other Ingredient Types

- 5.3.1. Protien

- 5.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.4.1. Specialized Pet Shops

- 5.4.2. Online Channels

- 5.4.3. Supermarkets/Hypermarkets

- 5.4.4. Other Distribution Channels

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia Pacific

- 5.5.4. South America

- 5.5.5. Middle East

- 5.5.6. South Africa

- 5.1. Market Analysis, Insights and Forecast - by Animal Type

- 6. Global Dry Pet Food Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Animal Type

- 6.1.1. Dogs

- 6.1.2. Cats

- 6.1.3. Other Animals

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Kibble

- 6.2.2. Other Product Types

- 6.3. Market Analysis, Insights and Forecast - by Ingredient Type

- 6.3.1. Protien

- 6.3.1.1. Animal-derived

- 6.3.1.2. Plant-derived

- 6.3.2. Cereals and Cereal Derivatives

- 6.3.3. Other Ingredient Types

- 6.3.1. Protien

- 6.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.4.1. Specialized Pet Shops

- 6.4.2. Online Channels

- 6.4.3. Supermarkets/Hypermarkets

- 6.4.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Animal Type

- 7. North America Dry Pet Food Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Animal Type

- 7.1.1. Dogs

- 7.1.2. Cats

- 7.1.3. Other Animals

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Kibble

- 7.2.2. Other Product Types

- 7.3. Market Analysis, Insights and Forecast - by Ingredient Type

- 7.3.1. Protien

- 7.3.1.1. Animal-derived

- 7.3.1.2. Plant-derived

- 7.3.2. Cereals and Cereal Derivatives

- 7.3.3. Other Ingredient Types

- 7.3.1. Protien

- 7.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.4.1. Specialized Pet Shops

- 7.4.2. Online Channels

- 7.4.3. Supermarkets/Hypermarkets

- 7.4.4. Other Distribution Channels

- 7.1. Market Analysis, Insights and Forecast - by Animal Type

- 8. Europe Dry Pet Food Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Animal Type

- 8.1.1. Dogs

- 8.1.2. Cats

- 8.1.3. Other Animals

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Kibble

- 8.2.2. Other Product Types

- 8.3. Market Analysis, Insights and Forecast - by Ingredient Type

- 8.3.1. Protien

- 8.3.1.1. Animal-derived

- 8.3.1.2. Plant-derived

- 8.3.2. Cereals and Cereal Derivatives

- 8.3.3. Other Ingredient Types

- 8.3.1. Protien

- 8.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.4.1. Specialized Pet Shops

- 8.4.2. Online Channels

- 8.4.3. Supermarkets/Hypermarkets

- 8.4.4. Other Distribution Channels

- 8.1. Market Analysis, Insights and Forecast - by Animal Type

- 9. Asia Pacific Dry Pet Food Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Animal Type

- 9.1.1. Dogs

- 9.1.2. Cats

- 9.1.3. Other Animals

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Kibble

- 9.2.2. Other Product Types

- 9.3. Market Analysis, Insights and Forecast - by Ingredient Type

- 9.3.1. Protien

- 9.3.1.1. Animal-derived

- 9.3.1.2. Plant-derived

- 9.3.2. Cereals and Cereal Derivatives

- 9.3.3. Other Ingredient Types

- 9.3.1. Protien

- 9.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.4.1. Specialized Pet Shops

- 9.4.2. Online Channels

- 9.4.3. Supermarkets/Hypermarkets

- 9.4.4. Other Distribution Channels

- 9.1. Market Analysis, Insights and Forecast - by Animal Type

- 10. South America Dry Pet Food Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Animal Type

- 10.1.1. Dogs

- 10.1.2. Cats

- 10.1.3. Other Animals

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Kibble

- 10.2.2. Other Product Types

- 10.3. Market Analysis, Insights and Forecast - by Ingredient Type

- 10.3.1. Protien

- 10.3.1.1. Animal-derived

- 10.3.1.2. Plant-derived

- 10.3.2. Cereals and Cereal Derivatives

- 10.3.3. Other Ingredient Types

- 10.3.1. Protien

- 10.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.4.1. Specialized Pet Shops

- 10.4.2. Online Channels

- 10.4.3. Supermarkets/Hypermarkets

- 10.4.4. Other Distribution Channels

- 10.1. Market Analysis, Insights and Forecast - by Animal Type

- 11. Middle East Dry Pet Food Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Animal Type

- 11.1.1. Dogs

- 11.1.2. Cats

- 11.1.3. Other Animals

- 11.2. Market Analysis, Insights and Forecast - by Product Type

- 11.2.1. Kibble

- 11.2.2. Other Product Types

- 11.3. Market Analysis, Insights and Forecast - by Ingredient Type

- 11.3.1. Protien

- 11.3.1.1. Animal-derived

- 11.3.1.2. Plant-derived

- 11.3.2. Cereals and Cereal Derivatives

- 11.3.3. Other Ingredient Types

- 11.3.1. Protien

- 11.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.4.1. Specialized Pet Shops

- 11.4.2. Online Channels

- 11.4.3. Supermarkets/Hypermarkets

- 11.4.4. Other Distribution Channels

- 11.1. Market Analysis, Insights and Forecast - by Animal Type

- 12. South Africa Dry Pet Food Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Animal Type

- 12.1.1. Dogs

- 12.1.2. Cats

- 12.1.3. Other Animals

- 12.2. Market Analysis, Insights and Forecast - by Product Type

- 12.2.1. Kibble

- 12.2.2. Other Product Types

- 12.3. Market Analysis, Insights and Forecast - by Ingredient Type

- 12.3.1. Protien

- 12.3.1.1. Animal-derived

- 12.3.1.2. Plant-derived

- 12.3.2. Cereals and Cereal Derivatives

- 12.3.3. Other Ingredient Types

- 12.3.1. Protien

- 12.4. Market Analysis, Insights and Forecast - by Distribution Channel

- 12.4.1. Specialized Pet Shops

- 12.4.2. Online Channels

- 12.4.3. Supermarkets/Hypermarkets

- 12.4.4. Other Distribution Channels

- 12.1. Market Analysis, Insights and Forecast - by Animal Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Schell & Kampeter Inc (Diamond Pet Foods)

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 General Mills Blue Buffalo Pet Products Inc

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Clearlake Capital Group L P (Wellness Pet Company Inc )

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Nutriara Alimentos Ltda

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Nestle Purina Petcare Company

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Alltech Inc

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Archer Daniels Midland

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Colgate-Palmolive Company (Hill's Pet Nutrition Inc )

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Mars Inc

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 The JM Smucker Company

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Schell & Kampeter Inc (Diamond Pet Foods)

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Dry Pet Food Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Dry Pet Food Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 3: North America Dry Pet Food Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 4: North America Dry Pet Food Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 5: North America Dry Pet Food Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Dry Pet Food Industry Revenue (Million), by Ingredient Type 2025 & 2033

- Figure 7: North America Dry Pet Food Industry Revenue Share (%), by Ingredient Type 2025 & 2033

- Figure 8: North America Dry Pet Food Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 9: North America Dry Pet Food Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 10: North America Dry Pet Food Industry Revenue (Million), by Country 2025 & 2033

- Figure 11: North America Dry Pet Food Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: Europe Dry Pet Food Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 13: Europe Dry Pet Food Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 14: Europe Dry Pet Food Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 15: Europe Dry Pet Food Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: Europe Dry Pet Food Industry Revenue (Million), by Ingredient Type 2025 & 2033

- Figure 17: Europe Dry Pet Food Industry Revenue Share (%), by Ingredient Type 2025 & 2033

- Figure 18: Europe Dry Pet Food Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 19: Europe Dry Pet Food Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 20: Europe Dry Pet Food Industry Revenue (Million), by Country 2025 & 2033

- Figure 21: Europe Dry Pet Food Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Asia Pacific Dry Pet Food Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 23: Asia Pacific Dry Pet Food Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 24: Asia Pacific Dry Pet Food Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 25: Asia Pacific Dry Pet Food Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 26: Asia Pacific Dry Pet Food Industry Revenue (Million), by Ingredient Type 2025 & 2033

- Figure 27: Asia Pacific Dry Pet Food Industry Revenue Share (%), by Ingredient Type 2025 & 2033

- Figure 28: Asia Pacific Dry Pet Food Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 29: Asia Pacific Dry Pet Food Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Asia Pacific Dry Pet Food Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: Asia Pacific Dry Pet Food Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: South America Dry Pet Food Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 33: South America Dry Pet Food Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 34: South America Dry Pet Food Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 35: South America Dry Pet Food Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 36: South America Dry Pet Food Industry Revenue (Million), by Ingredient Type 2025 & 2033

- Figure 37: South America Dry Pet Food Industry Revenue Share (%), by Ingredient Type 2025 & 2033

- Figure 38: South America Dry Pet Food Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 39: South America Dry Pet Food Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 40: South America Dry Pet Food Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: South America Dry Pet Food Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East Dry Pet Food Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 43: Middle East Dry Pet Food Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 44: Middle East Dry Pet Food Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 45: Middle East Dry Pet Food Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 46: Middle East Dry Pet Food Industry Revenue (Million), by Ingredient Type 2025 & 2033

- Figure 47: Middle East Dry Pet Food Industry Revenue Share (%), by Ingredient Type 2025 & 2033

- Figure 48: Middle East Dry Pet Food Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 49: Middle East Dry Pet Food Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 50: Middle East Dry Pet Food Industry Revenue (Million), by Country 2025 & 2033

- Figure 51: Middle East Dry Pet Food Industry Revenue Share (%), by Country 2025 & 2033

- Figure 52: South Africa Dry Pet Food Industry Revenue (Million), by Animal Type 2025 & 2033

- Figure 53: South Africa Dry Pet Food Industry Revenue Share (%), by Animal Type 2025 & 2033

- Figure 54: South Africa Dry Pet Food Industry Revenue (Million), by Product Type 2025 & 2033

- Figure 55: South Africa Dry Pet Food Industry Revenue Share (%), by Product Type 2025 & 2033

- Figure 56: South Africa Dry Pet Food Industry Revenue (Million), by Ingredient Type 2025 & 2033

- Figure 57: South Africa Dry Pet Food Industry Revenue Share (%), by Ingredient Type 2025 & 2033

- Figure 58: South Africa Dry Pet Food Industry Revenue (Million), by Distribution Channel 2025 & 2033

- Figure 59: South Africa Dry Pet Food Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 60: South Africa Dry Pet Food Industry Revenue (Million), by Country 2025 & 2033

- Figure 61: South Africa Dry Pet Food Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Dry Pet Food Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 2: Global Dry Pet Food Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 3: Global Dry Pet Food Industry Revenue Million Forecast, by Ingredient Type 2020 & 2033

- Table 4: Global Dry Pet Food Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 5: Global Dry Pet Food Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Dry Pet Food Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 7: Global Dry Pet Food Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 8: Global Dry Pet Food Industry Revenue Million Forecast, by Ingredient Type 2020 & 2033

- Table 9: Global Dry Pet Food Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 10: Global Dry Pet Food Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: United States Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Canada Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Mexico Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Rest of North America Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Global Dry Pet Food Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 16: Global Dry Pet Food Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 17: Global Dry Pet Food Industry Revenue Million Forecast, by Ingredient Type 2020 & 2033

- Table 18: Global Dry Pet Food Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 19: Global Dry Pet Food Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 20: Germany Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: United Kingdom Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: France Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Russia Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: Spain Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Global Dry Pet Food Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 27: Global Dry Pet Food Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 28: Global Dry Pet Food Industry Revenue Million Forecast, by Ingredient Type 2020 & 2033

- Table 29: Global Dry Pet Food Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 30: Global Dry Pet Food Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: India Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: China Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Japan Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Australia Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Rest of Asia Pacific Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Global Dry Pet Food Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 37: Global Dry Pet Food Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 38: Global Dry Pet Food Industry Revenue Million Forecast, by Ingredient Type 2020 & 2033

- Table 39: Global Dry Pet Food Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 40: Global Dry Pet Food Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 41: Brazil Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Argentina Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: Rest of South America Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Global Dry Pet Food Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 45: Global Dry Pet Food Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 46: Global Dry Pet Food Industry Revenue Million Forecast, by Ingredient Type 2020 & 2033

- Table 47: Global Dry Pet Food Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 48: Global Dry Pet Food Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 49: Global Dry Pet Food Industry Revenue Million Forecast, by Animal Type 2020 & 2033

- Table 50: Global Dry Pet Food Industry Revenue Million Forecast, by Product Type 2020 & 2033

- Table 51: Global Dry Pet Food Industry Revenue Million Forecast, by Ingredient Type 2020 & 2033

- Table 52: Global Dry Pet Food Industry Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 53: Global Dry Pet Food Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 54: United Arab Emirates Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 55: Saudi Arabia Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: Rest of Middle East Dry Pet Food Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Dry Pet Food Industry?

The projected CAGR is approximately 8.19%.

2. Which companies are prominent players in the Dry Pet Food Industry?

Key companies in the market include Schell & Kampeter Inc (Diamond Pet Foods), General Mills Blue Buffalo Pet Products Inc, Clearlake Capital Group L P (Wellness Pet Company Inc ), Nutriara Alimentos Ltda, Nestle Purina Petcare Company, Alltech Inc, Archer Daniels Midland, Colgate-Palmolive Company (Hill's Pet Nutrition Inc ), Mars Inc, The JM Smucker Company.

3. What are the main segments of the Dry Pet Food Industry?

The market segments include Animal Type, Product Type, Ingredient Type , Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 90.48 Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in the Fish Meal and Fish Oil Production; Demand for Quality Animal Feed.

6. What are the notable trends driving market growth?

Growing Trend of Pet Humanization in All Regions.

7. Are there any restraints impacting market growth?

High Prices of Fish Meal and Fish Oil Products; Threat to Fish Reserves.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Dry Pet Food Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Dry Pet Food Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Dry Pet Food Industry?

To stay informed about further developments, trends, and reports in the Dry Pet Food Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence