Key Insights

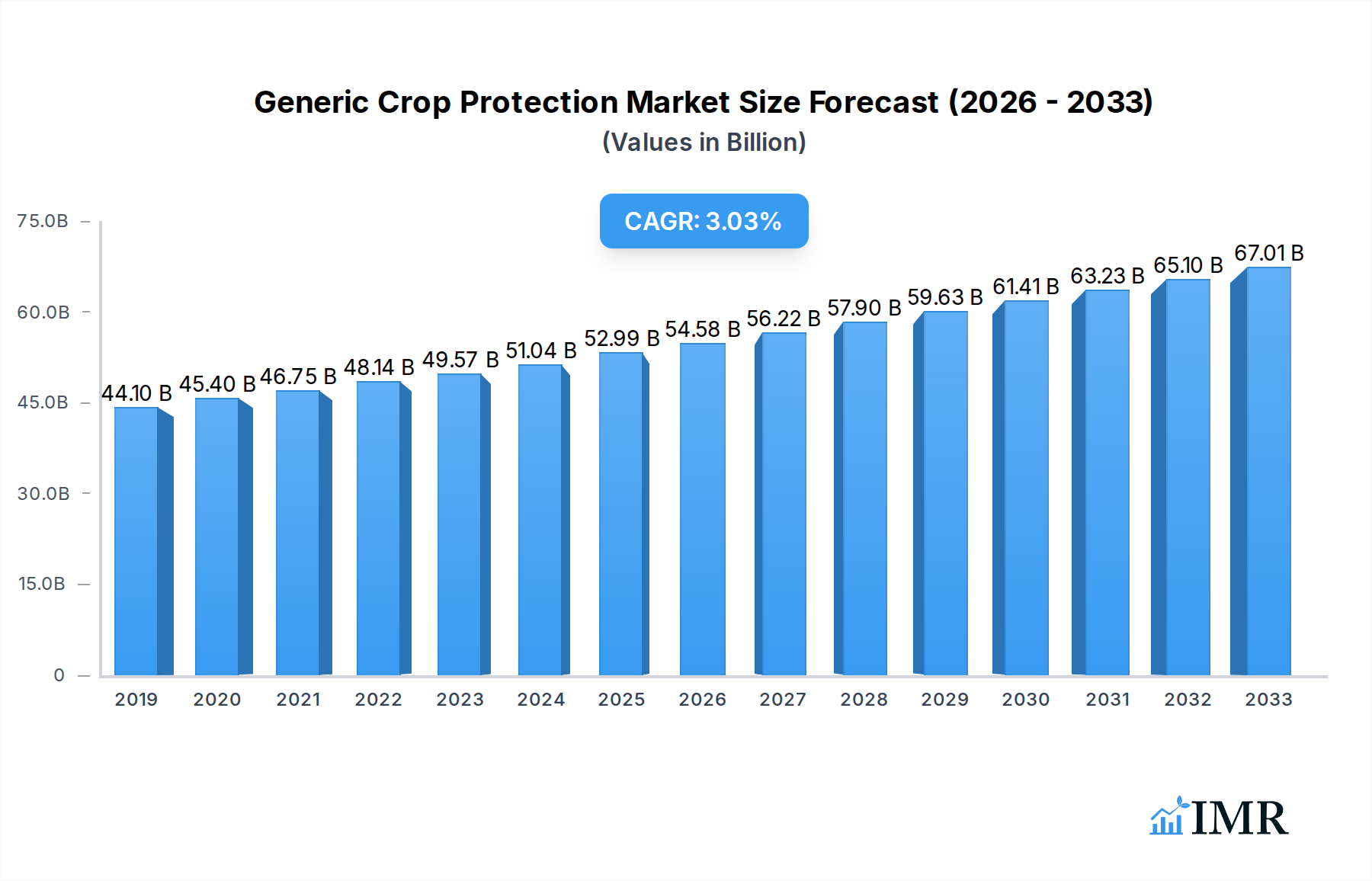

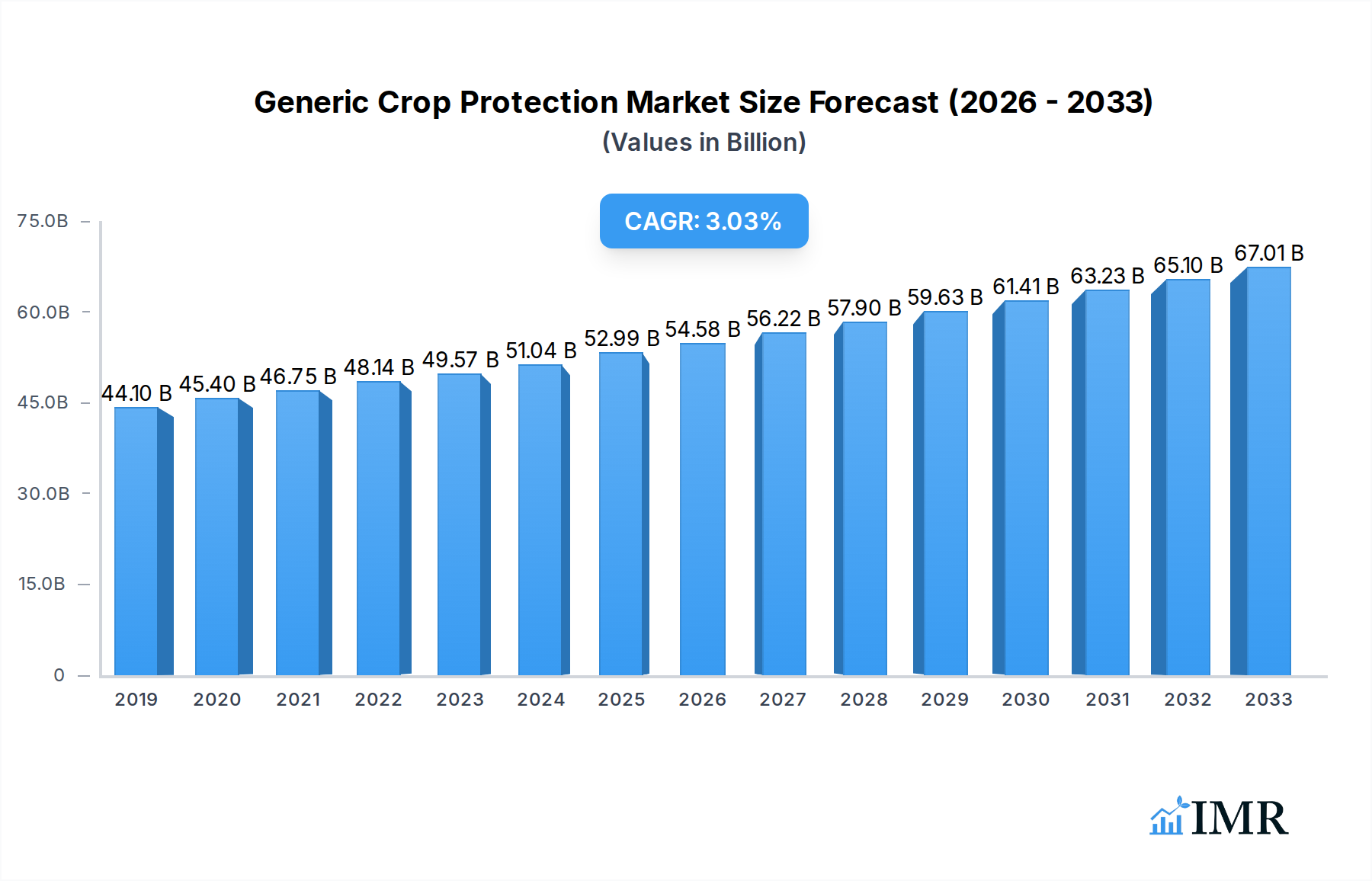

The global Generic Crop Protection market is poised for significant expansion, projected to reach an estimated $52,990 million by 2025, driven by a robust compound annual growth rate (CAGR) of 3.1% throughout the forecast period of 2025-2033. This growth is underpinned by the increasing demand for cost-effective agricultural solutions to enhance crop yields and ensure food security for a burgeoning global population. The market's trajectory is further bolstered by rising awareness among farmers regarding the benefits of generic crop protection products, which offer a competitive alternative to branded counterparts without compromising efficacy. Innovations in formulation technologies, leading to more targeted and environmentally friendly agrochemicals, will also play a crucial role in driving adoption. Furthermore, government initiatives promoting sustainable agriculture and the development of robust distribution networks across key agricultural regions are expected to create a favorable environment for market participants.

Generic Crop Protection Market Size (In Billion)

The market is segmented across diverse applications, with Cereals & Grains and Fruits & Vegetables anticipated to be major demand drivers, reflecting their substantial contribution to global food production. The "Others" category, potentially encompassing specialty crops and emerging agricultural sectors, is also expected to witness considerable growth. From a product type perspective, Herbicides are likely to maintain their dominant position due to the pervasive challenge of weed infestation in various cropping systems. Fungicides and Insecticides will also see consistent demand, driven by the need to mitigate losses from plant diseases and insect pests, respectively. The emergence of Plant Growth Regulators as a segment will gain traction as farmers increasingly focus on optimizing crop development for higher quality and yield. Key industry players like Syngenta, Bayer Crop Science, and BASF are actively investing in research and development to introduce advanced generic formulations, further solidifying their market presence and contributing to the overall dynamism of the generic crop protection landscape.

Generic Crop Protection Company Market Share

Generic Crop Protection Market Dynamics & Structure

The global generic crop protection market is characterized by a dynamic and evolving landscape, shaped by intense competition, technological advancements, and evolving regulatory frameworks. Market concentration is moderate, with a mix of large multinational corporations and a growing number of regional and specialized manufacturers. Key players like Syngenta, Bayer Crop Science, BASF, DuPont, and Monsanto are dominant forces, but their market share is steadily being challenged by agile and cost-effective generic producers such as Adama, FMC, and UPL. Technological innovation is a critical driver, focusing on developing new formulations, improving application efficiencies, and enhancing product efficacy against resistant pests and diseases. The adoption of precision agriculture and digital farming solutions also influences demand for specific generic crop protection products.

- Market Concentration: Moderate, with significant presence of both global giants and emerging generic players.

- Technological Innovation: Driven by formulation advancements, resistance management solutions, and integration with digital agriculture.

- Regulatory Frameworks: Stringent but also creating opportunities for off-patent active ingredient generics, especially in developing economies.

- Competitive Product Substitutes: Increasing availability of bio-pesticides and integrated pest management (IPM) strategies pose a long-term substitute threat.

- End-User Demographics: Farmers globally, with a growing segment of smallholder farmers in emerging markets increasingly adopting generic solutions for cost-effectiveness.

- M&A Trends: Strategic acquisitions by larger players to gain market access and expand product portfolios, alongside consolidation among smaller generic manufacturers.

- Parent Market: Global Crop Protection Market (estimated $78,000 million in 2025), with generic crop protection representing a significant and growing portion.

- Child Market: Specific generic active ingredient formulations and branded generic products.

Generic Crop Protection Growth Trends & Insights

The generic crop protection market is poised for robust expansion, driven by a confluence of factors including increasing global food demand, the expiry of patents on major active ingredients, and the persistent need for cost-effective agricultural inputs. The market size for generic crop protection is projected to grow substantially, reflecting a significant shift towards these more affordable alternatives. Adoption rates are on an upward trajectory, particularly in developing regions where farmers are highly sensitive to input costs but require effective solutions to protect their yields. Technological disruptions, such as the development of novel delivery systems for generic active ingredients and the integration with smart farming technologies, are enhancing their attractiveness and efficacy.

Consumer behavior shifts are also playing a crucial role. With rising awareness about sustainable agriculture and the economic benefits, more farmers are actively seeking out generic crop protection products that offer comparable performance to branded counterparts at a reduced price point. This trend is further amplified by government initiatives in various countries to promote the use of generics, thereby supporting agricultural productivity and food security. The CAGR for the generic crop protection market is estimated to be robust, indicating a sustained period of growth driven by these fundamental market forces. Market penetration is expected to deepen across diverse crop types and geographical regions as the value proposition of generic solutions becomes increasingly undeniable. The interplay of these factors creates a fertile ground for sustained growth and innovation within the generic crop protection sector.

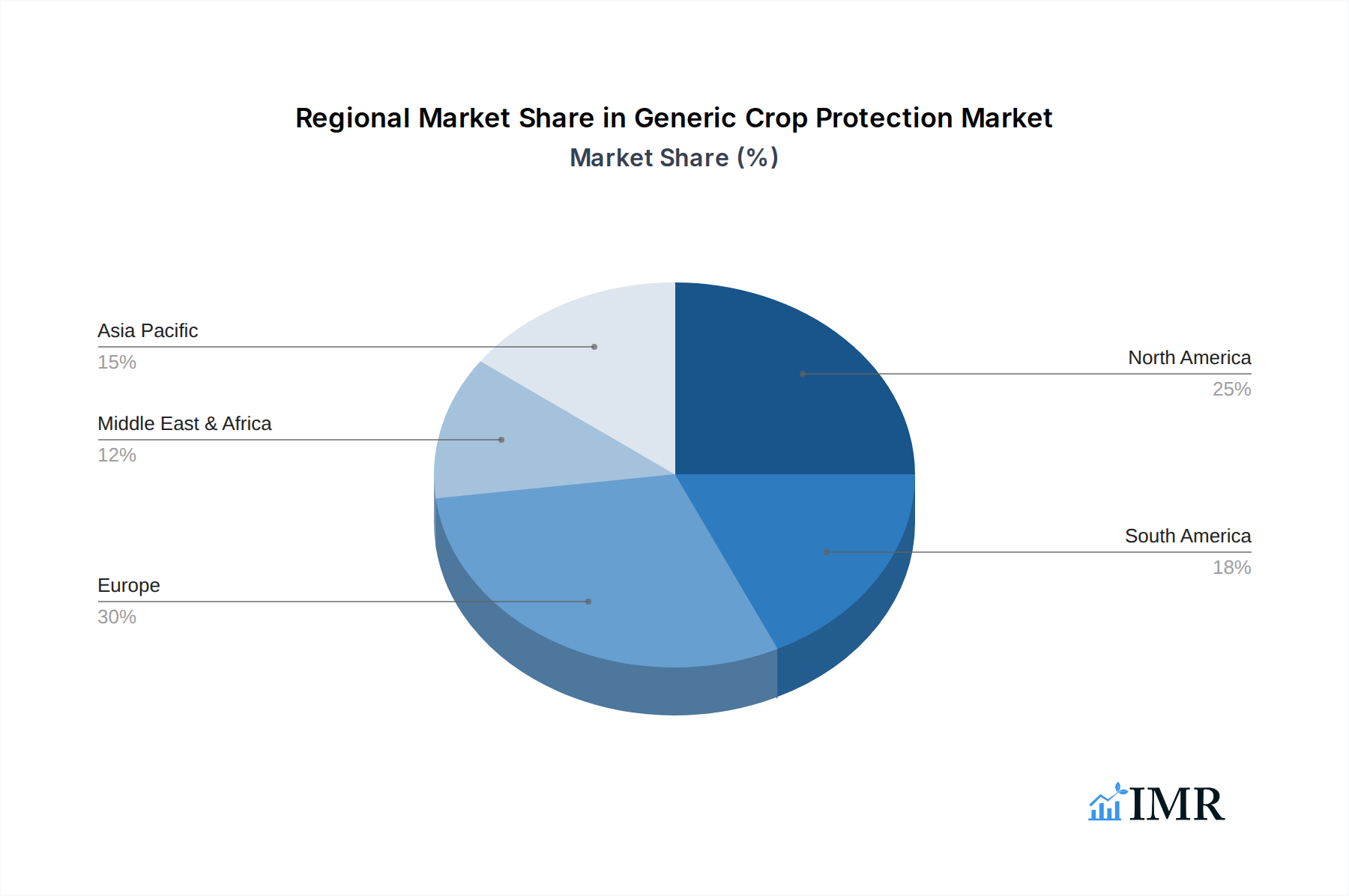

Dominant Regions, Countries, or Segments in Generic Crop Protection

The generic crop protection market's dominance is largely dictated by agricultural output, regulatory environments, and the economic capacity of farmers. Asia-Pacific consistently emerges as a leading region, driven by its vast agricultural land, substantial population, and a burgeoning demand for food. Countries like China and India, with their massive farming populations and significant production of cereals and grains, oilseeds, and vegetables, are primary consumers of generic crop protection solutions. The economic imperative for farmers in these regions to maximize yield while minimizing input costs makes generic alternatives highly attractive.

Dominant Application Segment: Cereals & Grains stand out as the most dominant application segment within the generic crop protection market. This is due to the sheer scale of cultivation for staples like rice, wheat, and corn globally, requiring extensive and cost-effective pest and disease management.

- Market Share: Estimated to hold over 40% of the generic crop protection market share in the forecast period.

- Key Drivers: High volume production, susceptibility to a wide range of pests and diseases, and the direct impact on food security.

- Economic Policies: Government subsidies and support for staple crop production indirectly boost the demand for generic inputs.

- Infrastructure: Well-established distribution networks for agricultural inputs to reach vast cereal-growing regions.

Dominant Type Segment: Herbicides are the leading product type within the generic crop protection market. Their widespread use across all major crop segments for weed control, a critical factor in maximizing crop yields, solidifies their dominance.

- Market Share: Estimated to account for approximately 50-55% of the total generic crop protection market.

- Growth Potential: Continued development of new generic herbicide formulations, including those targeting herbicide-resistant weeds, will fuel growth.

- Technological Integration: Application in conjunction with GPS-guided sprayers and precision agriculture technologies enhances their effectiveness and adoption.

Dominant Country: China is a powerhouse in the generic crop protection market. Its extensive agricultural sector, robust manufacturing capabilities for active ingredients and formulations, and significant domestic demand contribute to its leading position.

- Market Share: Holds a substantial share of the global generic crop protection market, estimated at over 25%.

- Manufacturing Hub: China is a major global supplier of generic crop protection active ingredients and finished products.

- Regulatory Environment: Evolving regulations are pushing for more sustainable and safer generic options, fostering innovation.

Generic Crop Protection Product Landscape

The generic crop protection product landscape is characterized by its focus on providing cost-effective alternatives to branded agrochemicals, leveraging off-patent active ingredients. Innovations primarily revolve around advanced formulation technologies that improve efficacy, extend residual activity, and enhance user safety. These include microencapsulation, suspension concentrates, and water-dispersible granules, which optimize the delivery of generic herbicides, fungicides, and insecticides. Performance metrics are benchmarked against originator products, with a strong emphasis on achieving comparable pest and disease control levels at a significantly lower price point. Unique selling propositions lie in the accessible price, wide availability across diverse crop applications, and increasingly, the development of combination products offering broader spectrum control.

Key Drivers, Barriers & Challenges in Generic Crop Protection

Key Drivers:

The generic crop protection market is propelled by several key drivers. The expiry of patents on numerous blockbuster active ingredients is a primary catalyst, opening the door for generic manufacturers. Increasing global food demand necessitates higher agricultural productivity, which, coupled with the price sensitivity of farmers, fuels the adoption of cost-effective generic solutions. Favorable regulatory environments in many developing nations also encourage the use of generics. Technological advancements in formulation and manufacturing processes enable generic companies to produce high-quality, effective products that rival branded counterparts.

Barriers & Challenges:

Despite the strong drivers, the market faces significant barriers and challenges. Intense price competition among generic players can erode profit margins. Navigating complex and varying regulatory approval processes in different countries requires substantial investment and time. Perceptions of lower quality or efficacy compared to branded products can hinder adoption in certain markets, despite scientific evidence to the contrary. Supply chain disruptions, raw material price volatility, and the emergence of herbicide and pesticide resistance in target organisms pose ongoing challenges.

Emerging Opportunities in Generic Crop Protection

Emerging opportunities in the generic crop protection industry are centered on expanding into untapped markets, developing innovative application methods, and catering to evolving consumer preferences. The growing demand for bio-based and integrated pest management (IPM) solutions presents an opportunity for generic manufacturers to develop complementary or even bio-rational generic products. Furthermore, the integration of digital farming technologies, such as drone-based applications and sensor-driven pest detection, creates a demand for precisely formulated generic products. Developing specialized generic formulations for niche crops or specific regional pest challenges also offers significant growth potential.

Growth Accelerators in the Generic Crop Protection Industry

Several catalysts are accelerating growth in the generic crop protection industry. The continuous pipeline of patent expiries for established active ingredients remains a fundamental growth accelerator, ensuring a steady supply of new market opportunities. Strategic partnerships and collaborations between generic manufacturers and distributors are crucial for expanding market reach and enhancing brand visibility. Furthermore, the increasing adoption of precision agriculture technologies by farmers is creating a demand for optimized generic formulations that can be applied more efficiently and effectively, leading to improved yield outcomes. The rising trend of contract manufacturing of generic active ingredients also supports the industry's growth by providing flexible production capabilities.

Key Players Shaping the Generic Crop Protection Market

- Syngenta

- Bayer Crop Science

- BASF

- DuPont

- Monsanto (now part of Bayer)

- Adama

- FMC

- UPL

- Nufarm

- Sumitomo Chemical

- Arysta LifeScience (now part of UPL)

- Albaugh

- Sipcam Oxon

- Wynca Chemical

- Zhejiang Jinfanda Biochemical

- Huapont

- Fuhua Tongda Agro-Chemical Technology

Notable Milestones in Generic Crop Protection Sector

- 2019: Significant patent expiries of key fungicide and insecticide active ingredients, opening avenues for generic product launches.

- 2020: Increased adoption of online platforms for agrochemical sales, benefiting generic manufacturers with wider reach.

- 2021: Growing focus on sustainable agriculture and biopesticides, prompting generic companies to invest in research and development for eco-friendlier solutions.

- 2022: Mergers and acquisitions among smaller generic players to achieve economies of scale and strengthen market position.

- 2023: Advancements in formulation technologies leading to enhanced efficacy and reduced environmental impact for generic crop protection products.

- 2024: Strengthened regulatory scrutiny and demand for dossier sharing, influencing the pace of generic product registrations globally.

In-Depth Generic Crop Protection Market Outlook

The future outlook for the generic crop protection market is exceptionally promising, fueled by sustained global food demand and the ongoing expiry of patents on branded agrochemicals. Growth accelerators such as technological breakthroughs in formulation science, strategic partnerships for market expansion, and the increasing adoption of precision agriculture will continue to drive market expansion. The market is expected to witness significant penetration in emerging economies as cost-effective crop protection solutions become more accessible. Strategic opportunities lie in developing integrated pest management solutions that combine generic chemical inputs with biological and digital tools, catering to the evolving needs of modern agriculture for both productivity and sustainability.

Generic Crop Protection Segmentation

-

1. Application

- 1.1. Cereals & Grains

- 1.2. Fruits & Vegetables

- 1.3. Oilseeds & Pulses

- 1.4. Others

-

2. Types

- 2.1. Herbicide

- 2.2. Fungicide

- 2.3. Insecticide

- 2.4. Plant Growth Regulator

Generic Crop Protection Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Generic Crop Protection Regional Market Share

Geographic Coverage of Generic Crop Protection

Generic Crop Protection REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Generic Crop Protection Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Cereals & Grains

- 5.1.2. Fruits & Vegetables

- 5.1.3. Oilseeds & Pulses

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Herbicide

- 5.2.2. Fungicide

- 5.2.3. Insecticide

- 5.2.4. Plant Growth Regulator

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Generic Crop Protection Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Cereals & Grains

- 6.1.2. Fruits & Vegetables

- 6.1.3. Oilseeds & Pulses

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Herbicide

- 6.2.2. Fungicide

- 6.2.3. Insecticide

- 6.2.4. Plant Growth Regulator

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Generic Crop Protection Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Cereals & Grains

- 7.1.2. Fruits & Vegetables

- 7.1.3. Oilseeds & Pulses

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Herbicide

- 7.2.2. Fungicide

- 7.2.3. Insecticide

- 7.2.4. Plant Growth Regulator

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Generic Crop Protection Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Cereals & Grains

- 8.1.2. Fruits & Vegetables

- 8.1.3. Oilseeds & Pulses

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Herbicide

- 8.2.2. Fungicide

- 8.2.3. Insecticide

- 8.2.4. Plant Growth Regulator

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Generic Crop Protection Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Cereals & Grains

- 9.1.2. Fruits & Vegetables

- 9.1.3. Oilseeds & Pulses

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Herbicide

- 9.2.2. Fungicide

- 9.2.3. Insecticide

- 9.2.4. Plant Growth Regulator

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Generic Crop Protection Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Cereals & Grains

- 10.1.2. Fruits & Vegetables

- 10.1.3. Oilseeds & Pulses

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Herbicide

- 10.2.2. Fungicide

- 10.2.3. Insecticide

- 10.2.4. Plant Growth Regulator

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Syngenta

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Bayer Crop Science

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 BASF

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 DuPont

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Monsanto

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Adama

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 FMC

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 UPL

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Nufarm

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Sumitomo Chemical

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Arysta LifeScience

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Albaugh

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Sipcam-oxon

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Wynca Chemical

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Zhejiang Jinfanda Biochemical

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Huapont

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Fuhua Tongda Agro-Chemical Technology

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Syngenta

List of Figures

- Figure 1: Global Generic Crop Protection Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Generic Crop Protection Revenue (million), by Application 2025 & 2033

- Figure 3: North America Generic Crop Protection Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Generic Crop Protection Revenue (million), by Types 2025 & 2033

- Figure 5: North America Generic Crop Protection Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Generic Crop Protection Revenue (million), by Country 2025 & 2033

- Figure 7: North America Generic Crop Protection Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Generic Crop Protection Revenue (million), by Application 2025 & 2033

- Figure 9: South America Generic Crop Protection Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Generic Crop Protection Revenue (million), by Types 2025 & 2033

- Figure 11: South America Generic Crop Protection Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Generic Crop Protection Revenue (million), by Country 2025 & 2033

- Figure 13: South America Generic Crop Protection Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Generic Crop Protection Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Generic Crop Protection Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Generic Crop Protection Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Generic Crop Protection Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Generic Crop Protection Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Generic Crop Protection Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Generic Crop Protection Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Generic Crop Protection Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Generic Crop Protection Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Generic Crop Protection Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Generic Crop Protection Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Generic Crop Protection Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Generic Crop Protection Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Generic Crop Protection Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Generic Crop Protection Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Generic Crop Protection Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Generic Crop Protection Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Generic Crop Protection Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Generic Crop Protection Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Generic Crop Protection Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Generic Crop Protection Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Generic Crop Protection Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Generic Crop Protection Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Generic Crop Protection Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Generic Crop Protection Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Generic Crop Protection Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Generic Crop Protection Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Generic Crop Protection Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Generic Crop Protection Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Generic Crop Protection Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Generic Crop Protection Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Generic Crop Protection Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Generic Crop Protection Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Generic Crop Protection Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Generic Crop Protection Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Generic Crop Protection Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Generic Crop Protection Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Generic Crop Protection?

The projected CAGR is approximately 3.1%.

2. Which companies are prominent players in the Generic Crop Protection?

Key companies in the market include Syngenta, Bayer Crop Science, BASF, DuPont, Monsanto, Adama, FMC, UPL, Nufarm, Sumitomo Chemical, Arysta LifeScience, Albaugh, Sipcam-oxon, Wynca Chemical, Zhejiang Jinfanda Biochemical, Huapont, Fuhua Tongda Agro-Chemical Technology.

3. What are the main segments of the Generic Crop Protection?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 52990 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5600.00, USD 8400.00, and USD 11200.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Generic Crop Protection," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Generic Crop Protection report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Generic Crop Protection?

To stay informed about further developments, trends, and reports in the Generic Crop Protection, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence