Key Insights

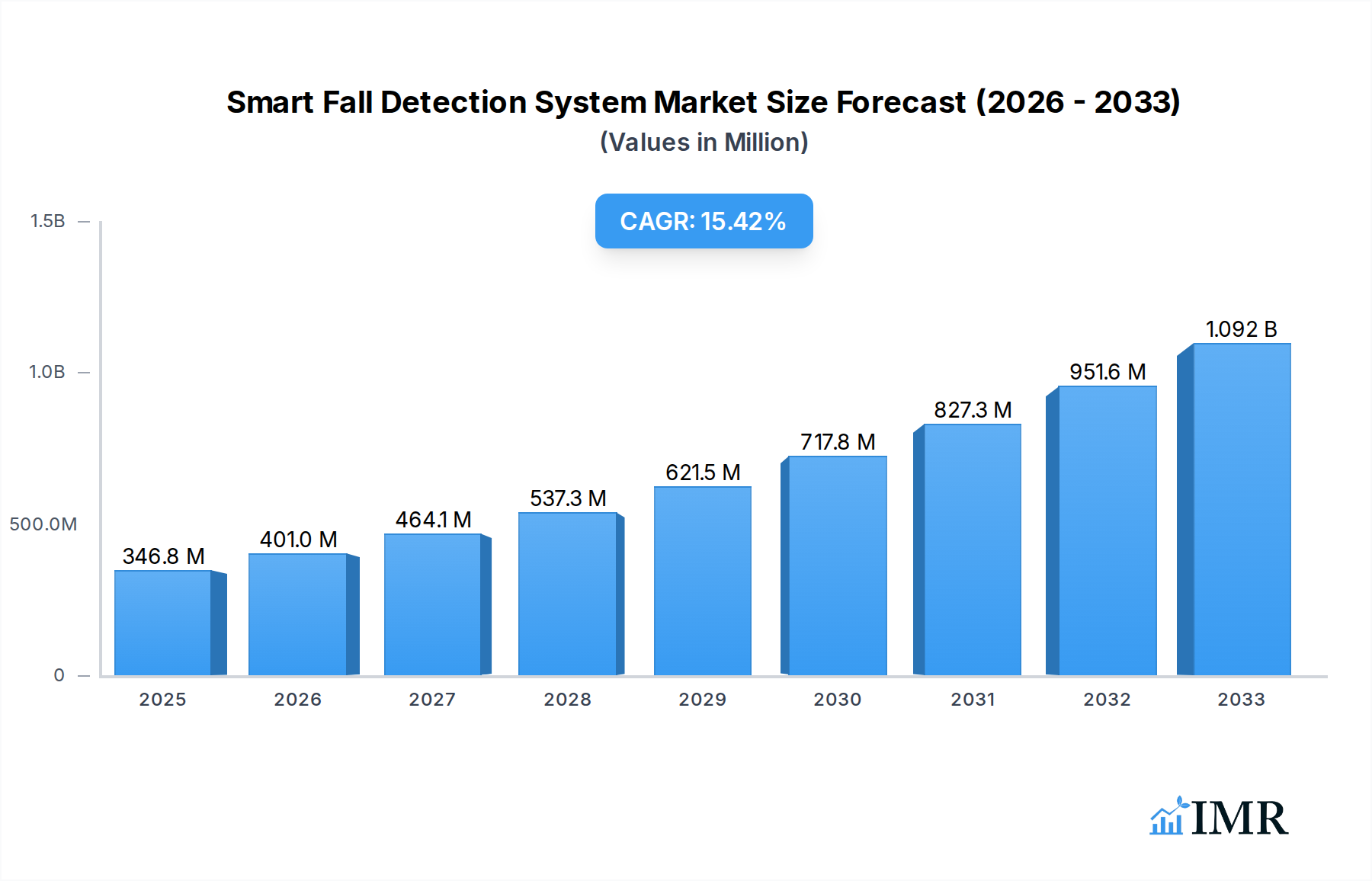

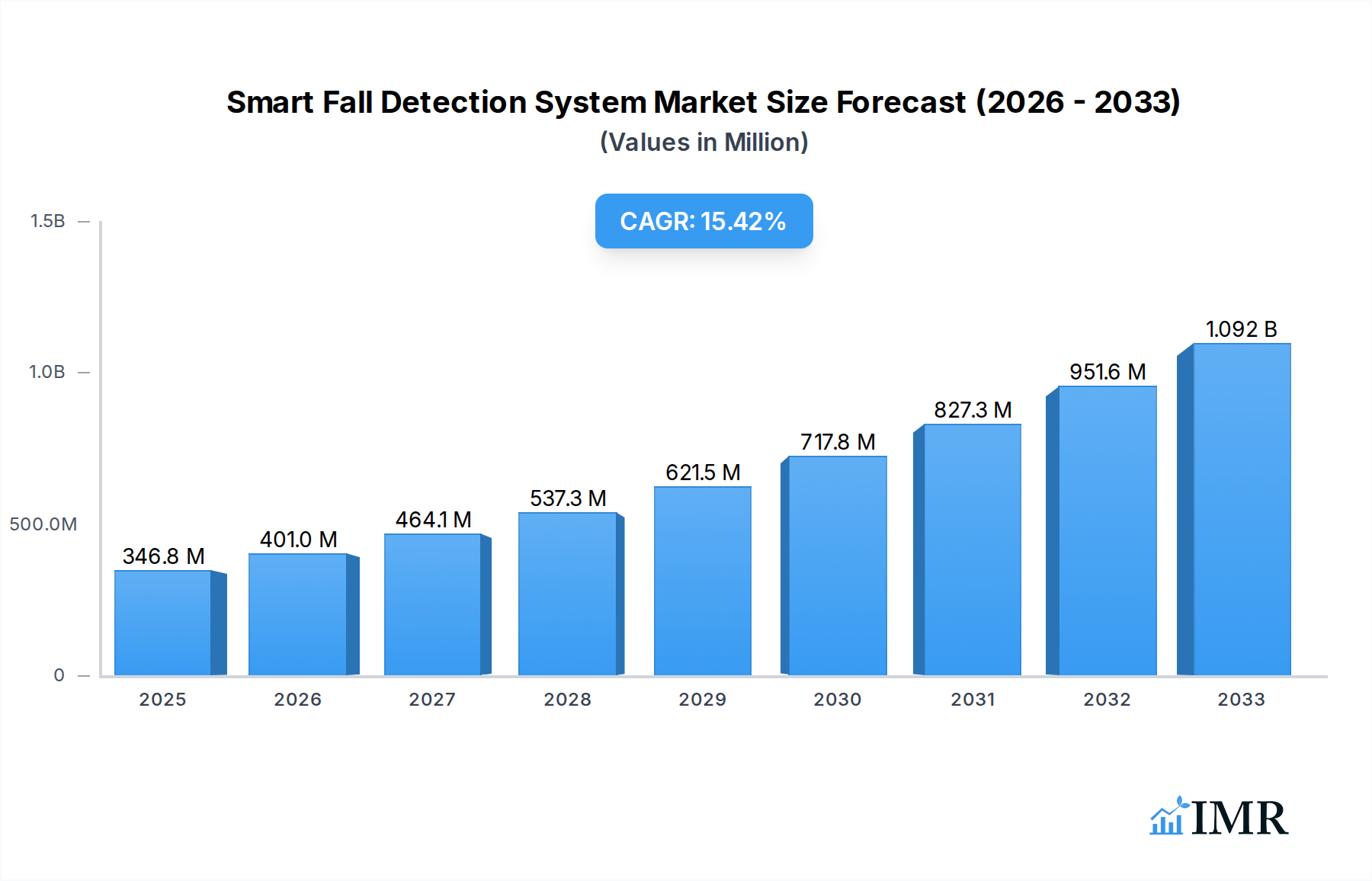

The Smart Fall Detection System market is poised for significant expansion, with an estimated market size of $346.83 million in 2025, projected to grow at a robust Compound Annual Growth Rate (CAGR) of 15.53% through 2033. This impressive growth trajectory is fueled by a confluence of factors, primarily the increasing prevalence of aging populations worldwide and the heightened awareness of fall prevention solutions among both individuals and healthcare providers. The inherent desire for independent living, particularly among seniors, coupled with the increasing concern for their safety and well-being, acts as a primary market driver. Furthermore, advancements in sensor technology, artificial intelligence, and connectivity are leading to the development of more sophisticated and accurate fall detection systems, thereby enhancing user confidence and adoption rates. The integration of these systems into medical alert devices and wearable technology is further expanding their reach and applicability.

Smart Fall Detection System Market Size (In Million)

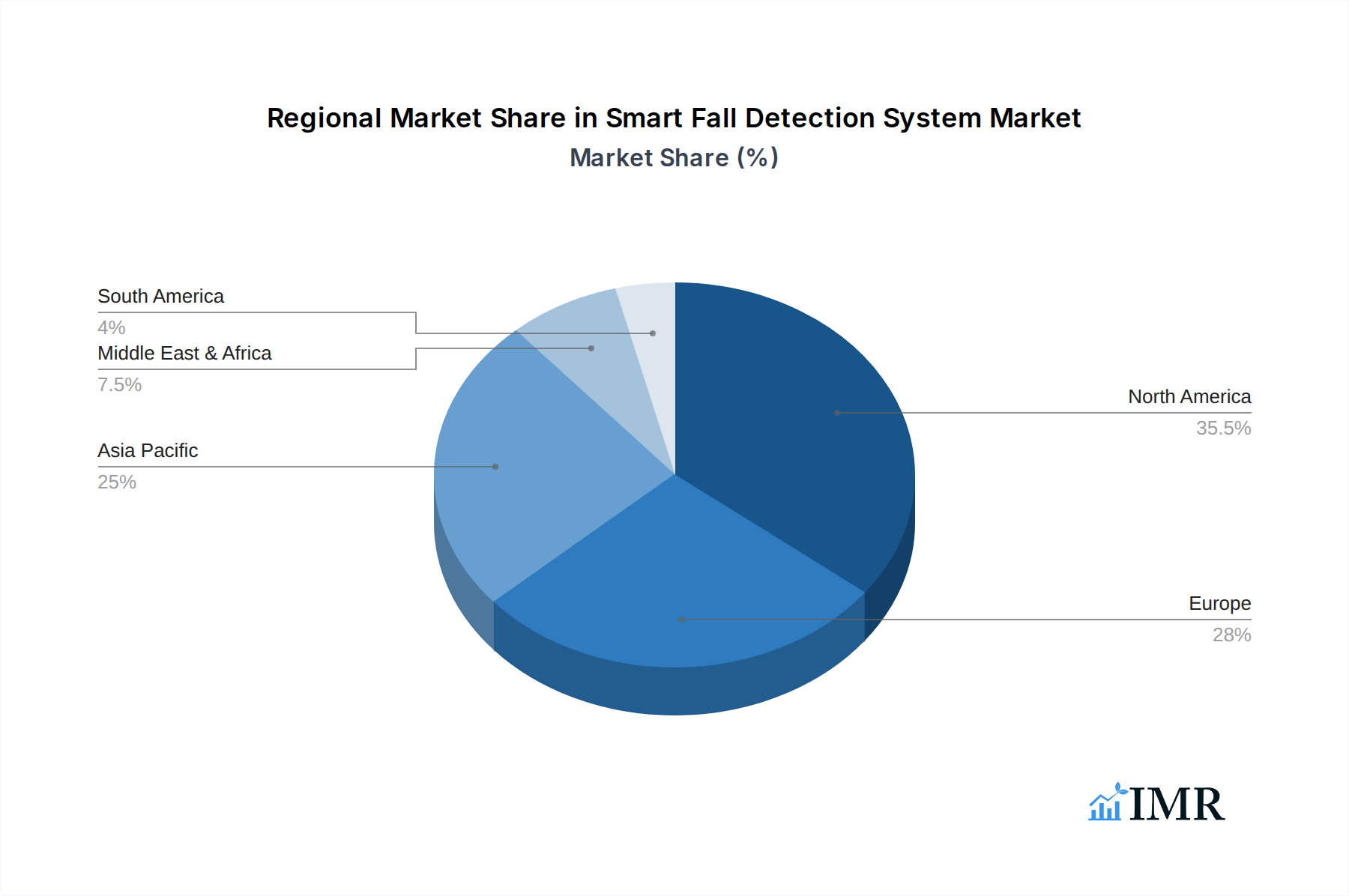

The market is segmented into Household and Medical applications, with further classification based on Type: Sensor Based and Camera Recognition Based systems. Sensor-based solutions, leveraging accelerometers, gyroscopes, and other biometric sensors, currently dominate due to their privacy-preserving nature and widespread adoption in personal emergency response systems (PERS). However, camera recognition-based systems are gaining traction, offering potentially richer contextual data for fall analysis and prevention, though privacy concerns remain a consideration. Geographically, North America, led by the United States, is anticipated to hold a significant market share, driven by a mature healthcare infrastructure and a large elderly demographic. Asia Pacific is expected to witness the fastest growth, propelled by rapid urbanization, increasing disposable incomes, and a growing elderly population in countries like China and India. Restraints may include the initial cost of advanced systems, user acceptance challenges, and the need for robust data privacy and security measures. However, the overwhelming benefits of enhanced safety, prompt emergency response, and the promotion of independent living are expected to outweigh these limitations, paving the way for sustained market growth.

Smart Fall Detection System Company Market Share

Here is a compelling, SEO-optimized report description for the Smart Fall Detection System market, designed for maximum visibility and engagement with industry professionals.

Smart Fall Detection System Market Dynamics & Structure

The Smart Fall Detection System market is characterized by a moderate level of concentration, with key players like Philips Lifeline, Tunstall Healthcare Group, and Medical Guardian holding significant market shares. Technological innovation is the primary driver, fueled by advancements in sensor technology, AI-powered video analytics, and miniaturization of wearable devices. Regulatory frameworks, particularly those surrounding healthcare data privacy and medical device certifications, play a crucial role in market entry and product development. Competitive product substitutes include traditional personal emergency response systems (PERS) and informal caregiving arrangements, though the enhanced accuracy and proactive nature of smart fall detection systems are diminishing their appeal. End-user demographics are rapidly expanding beyond the elderly to include individuals with mobility issues, chronic health conditions, and those living alone, driven by a growing awareness of safety and independence. Mergers and acquisitions (M&A) trends are on the rise as larger companies seek to consolidate their market position and acquire innovative technologies. For instance, several strategic acquisitions have occurred in the past two years, totaling an estimated xx million units in deal volume, aimed at expanding product portfolios and geographical reach.

- Market Concentration: Moderate, with key players focusing on innovation and market penetration.

- Technological Innovation Drivers: Miniaturized sensors, AI for video analysis, cloud-based platforms.

- Regulatory Frameworks: HIPAA, GDPR compliance, FDA approvals for medical-grade devices.

- Competitive Substitutes: Traditional PERS, human caregivers, assisted living facilities.

- End-User Demographics: Elderly population, individuals with chronic conditions, post-operative recovery patients.

- M&A Trends: Active consolidation for technology acquisition and market expansion.

Smart Fall Detection System Growth Trends & Insights

The global Smart Fall Detection System market is poised for robust expansion, driven by an aging global population and increasing awareness of the critical need for senior safety and independent living solutions. Market size evolution is projected to witness a compound annual growth rate (CAGR) of approximately 12.5% from 2025 to 2033, reaching an estimated market value of $32.5 billion by the end of the forecast period. Adoption rates are steadily increasing, particularly in developed economies where healthcare infrastructure and disposable income are higher. This growth is propelled by technological disruptions that have made systems more accurate, less intrusive, and more user-friendly. For example, the integration of AI and machine learning algorithms in sensor-based systems has significantly reduced false alarms, a historical barrier to adoption. Consumer behavior shifts are also instrumental; individuals are increasingly proactive about their health and safety, and families are seeking advanced solutions to monitor and protect their loved ones. The market penetration is expected to rise from 15% in 2025 to over 30% by 2033. This shift is further amplified by a growing preference for non-intrusive monitoring solutions that respect privacy while ensuring immediate assistance. The transition from reactive alert systems to proactive health monitoring, incorporating features like activity tracking and sleep analysis, is a significant trend shaping consumer demand and product development. The impact of the COVID-19 pandemic also played a role, highlighting the importance of remote monitoring and emergency preparedness.

- Market Size Evolution: Expected to reach $32.5 billion by 2033.

- CAGR: Projected at 12.5% during the forecast period (2025-2033).

- Adoption Rates: Increasing, especially in North America and Europe.

- Technological Disruptions: AI integration, wearable sensors, cloud connectivity, ambient sensing.

- Consumer Behavior Shifts: Growing demand for independence, proactive health monitoring, and peace of mind.

- Market Penetration: Anticipated to grow from 15% in 2025 to over 30% by 2033.

Dominant Regions, Countries, or Segments in Smart Fall Detection System

North America currently dominates the Smart Fall Detection System market, driven by a confluence of factors including a high elderly population demographic, advanced healthcare infrastructure, significant disposable income, and strong government initiatives promoting independent living for seniors. The United States, in particular, accounts for a substantial portion of this regional dominance, estimated at 45% of the global market share in 2025. Key drivers in this region include robust reimbursement policies from healthcare providers and insurance companies, a mature technological adoption landscape, and a proactive approach to elder care. Countries like Canada also contribute significantly to this leadership.

The Household application segment is the primary growth engine within the North American market, representing an estimated 60% of the total market revenue in 2025. This segment's dominance is attributed to the growing trend of aging in place, where individuals prefer to maintain their independence and live in their own homes for as long as possible. Sensor-based systems are the most prevalent type, accounting for approximately 75% of the market in this region, owing to their established reliability, cost-effectiveness, and diverse form factors, including wearables and environmental sensors.

Europe, particularly Western European countries like Germany, the UK, and France, represents the second-largest market, exhibiting strong growth potential due to its rapidly aging population and well-developed social welfare systems. Economic policies in these regions are increasingly focused on supporting the elderly population to live independently, fostering demand for smart fall detection solutions.

- Dominant Region: North America, led by the United States.

- Key Drivers in North America: High elderly population, advanced healthcare, favorable reimbursement, aging-in-place trend.

- Dominant Segment (Application): Household, driven by independent living preferences.

- Dominant Segment (Type): Sensor Based, due to reliability and variety.

- Emerging Regional Strength: Europe, with a focus on social welfare and elder care policies.

- Market Share (US): Estimated at 45% of the global market in 2025.

- Market Share (Household Application): Estimated at 60% in North America in 2025.

- Market Share (Sensor Based Type): Estimated at 75% in North America in 2025.

Smart Fall Detection System Product Landscape

The product landscape for Smart Fall Detection Systems is rapidly evolving, marked by continuous innovation in form factor, functionality, and integration capabilities. Companies are developing highly discreet wearable devices, such as pendants, wristbands, and even clothing-integrated sensors, that offer advanced motion detection and AI-powered algorithms to distinguish falls from normal activity. Alongside these, ambient sensor systems that monitor movement and activity within the home without requiring user interaction are gaining traction. Product performance metrics are improving with enhanced accuracy in fall detection, reduced false alarms, and extended battery life for wearable devices. Furthermore, the integration of smart home ecosystems and telehealth platforms is creating a more connected and comprehensive safety net for users. Unique selling propositions often lie in the seamless user experience, the ability to provide context-aware alerts, and the discreet integration into daily life.

Key Drivers, Barriers & Challenges in Smart Fall Detection System

Key Drivers:

- Technological Advancements: AI-powered algorithms, miniaturized sensors, and improved connectivity enhance accuracy and user experience.

- Aging Global Population: A significant and growing demographic requiring proactive safety solutions.

- Government Initiatives & Healthcare Policies: Increased focus on elder care, independent living, and remote patient monitoring.

- Rising Healthcare Costs: Smart fall detection offers a cost-effective alternative to institutional care.

- Growing Consumer Awareness: Increased understanding of fall risks and the benefits of proactive detection.

Barriers & Challenges:

- High Initial Cost: For advanced systems, the upfront investment can be a deterrent for some consumers.

- Privacy Concerns: Data collection and potential for misuse of personal information.

- Technological Literacy: Some elderly users may struggle with setup and daily operation.

- False Alarm Fatigue: While improving, persistent false alarms can erode user trust.

- Regulatory Hurdles: Obtaining necessary certifications and ensuring compliance with healthcare standards.

- Market Saturation & Competition: Intense competition can lead to price wars and pressure on margins. Supply chain disruptions have also impacted production and delivery timelines, adding to operational challenges.

Emerging Opportunities in Smart Fall Detection System

Emerging opportunities in the Smart Fall Detection System market lie in the expansion of the technology beyond traditional elder care. Integration with telehealth platforms for remote patient monitoring of conditions like Parkinson's or epilepsy presents a significant growth avenue. The development of more sophisticated AI that can predict fall risks based on gait analysis and activity patterns offers a proactive approach. Furthermore, opportunities exist in catering to niche markets, such as individuals with specific disabilities or those recovering from surgery. The growing trend of "smart aging" and the demand for integrated home care solutions also create a fertile ground for innovative product development and service offerings. The parent market, personal emergency response systems, is undergoing a transformation, with smart fall detection systems poised to capture a substantial share.

Growth Accelerators in the Smart Fall Detection System Industry

Long-term growth in the Smart Fall Detection System industry will be propelled by several key catalysts. Continuous breakthroughs in sensor technology, leading to smaller, more comfortable, and more accurate devices, will be crucial. Strategic partnerships between technology providers, healthcare organizations, and insurance companies will accelerate adoption through bundled services and improved reimbursement models. The expansion of the smart home ecosystem, integrating fall detection seamlessly with other connected devices, will also drive demand. Furthermore, the increasing global focus on preventative healthcare and the desire to reduce hospital readmissions will create sustained market momentum. The child market, encompassing specialized solutions for pediatric care and rehabilitation, is also expected to see significant development and investment.

Key Players Shaping the Smart Fall Detection System Market

- GIGABYTE Global

- Philips Lifeline

- Tunstall Healthcare Group

- LifeFone

- ADT Corporation

- MobileHelp

- Nihon Kohden

- Medical Guardian

- Bay Alarm Medical

- LifeStation

- Edan

- Tsingray Technology

Notable Milestones in Smart Fall Detection System Sector

- 2019: Philips Lifeline launches its GoSafe 2 mobile help button with improved GPS and fall detection accuracy.

- 2020: Tunstall Healthcare Group enhances its Telecare portfolio with advanced sensor integration for discreet fall monitoring.

- 2021: Medical Guardian introduces its Mobile LTE device, offering enhanced connectivity and fall detection capabilities for active seniors.

- 2022: LifeFone expands its service offerings to include advanced fall detection with automatic alerts to caregivers.

- 2022: ADT Corporation acquires Life Alert, consolidating its position in the personal emergency response market.

- 2023: GIGABYTE Global announces advancements in AI-powered video analytics for non-wearable fall detection in smart home devices.

- 2023: MobileHelp rolls out its new generation of wearable fall detection devices with longer battery life and enhanced reliability.

- 2024: Nihon Kohden introduces a new line of medical alert systems with integrated fall detection, focusing on clinical applications.

- 2024: Bay Alarm Medical launches a new subscription service model for its fall detection systems, making them more accessible.

- 2024: Tsingray Technology showcases its latest ambient sensing technology for proactive fall risk assessment in smart homes.

In-Depth Smart Fall Detection System Market Outlook

The Smart Fall Detection System market is characterized by a highly promising future, driven by the confluence of demographic shifts, technological innovation, and a growing societal emphasis on proactive health and safety solutions. The continued aging of the global population ensures a sustained and expanding customer base, while advancements in AI, IoT, and wearable technology are continuously improving the accuracy, usability, and affordability of these systems. Strategic partnerships and the integration of fall detection into broader telehealth and smart home ecosystems are poised to accelerate market penetration and unlock new revenue streams. The market's trajectory points towards a future where smart fall detection is an indispensable component of independent living, offering peace of mind to individuals and their loved ones, and significantly contributing to the efficiency and effectiveness of healthcare delivery. The child market for these technologies, focused on specialized monitoring, is also expected to flourish.

Smart Fall Detection System Segmentation

-

1. Application

- 1.1. Household

- 1.2. Medical

-

2. Type

- 2.1. Sensor Based

- 2.2. Camera Recognition Based

Smart Fall Detection System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Smart Fall Detection System Regional Market Share

Geographic Coverage of Smart Fall Detection System

Smart Fall Detection System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.53% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Smart Fall Detection System Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Household

- 5.1.2. Medical

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Sensor Based

- 5.2.2. Camera Recognition Based

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Smart Fall Detection System Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Household

- 6.1.2. Medical

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Sensor Based

- 6.2.2. Camera Recognition Based

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Smart Fall Detection System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Household

- 7.1.2. Medical

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Sensor Based

- 7.2.2. Camera Recognition Based

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Smart Fall Detection System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Household

- 8.1.2. Medical

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Sensor Based

- 8.2.2. Camera Recognition Based

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Smart Fall Detection System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Household

- 9.1.2. Medical

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Sensor Based

- 9.2.2. Camera Recognition Based

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Smart Fall Detection System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Household

- 10.1.2. Medical

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Sensor Based

- 10.2.2. Camera Recognition Based

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 GIGABYTE Global

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Philips Lifeline

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Tunstall Healthcare Group

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 LifeFone

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 ADT Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 MobileHelp

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Nihon Kohden

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Medical Guardian

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Bay Alarm Medical

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 LifeStation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Edan

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Tsingray Technology

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 GIGABYTE Global

List of Figures

- Figure 1: Global Smart Fall Detection System Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Smart Fall Detection System Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Smart Fall Detection System Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Smart Fall Detection System Volume (K), by Application 2025 & 2033

- Figure 5: North America Smart Fall Detection System Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Smart Fall Detection System Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Smart Fall Detection System Revenue (undefined), by Type 2025 & 2033

- Figure 8: North America Smart Fall Detection System Volume (K), by Type 2025 & 2033

- Figure 9: North America Smart Fall Detection System Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Smart Fall Detection System Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Smart Fall Detection System Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Smart Fall Detection System Volume (K), by Country 2025 & 2033

- Figure 13: North America Smart Fall Detection System Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Smart Fall Detection System Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Smart Fall Detection System Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Smart Fall Detection System Volume (K), by Application 2025 & 2033

- Figure 17: South America Smart Fall Detection System Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Smart Fall Detection System Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Smart Fall Detection System Revenue (undefined), by Type 2025 & 2033

- Figure 20: South America Smart Fall Detection System Volume (K), by Type 2025 & 2033

- Figure 21: South America Smart Fall Detection System Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Smart Fall Detection System Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Smart Fall Detection System Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Smart Fall Detection System Volume (K), by Country 2025 & 2033

- Figure 25: South America Smart Fall Detection System Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Smart Fall Detection System Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Smart Fall Detection System Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Smart Fall Detection System Volume (K), by Application 2025 & 2033

- Figure 29: Europe Smart Fall Detection System Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Smart Fall Detection System Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Smart Fall Detection System Revenue (undefined), by Type 2025 & 2033

- Figure 32: Europe Smart Fall Detection System Volume (K), by Type 2025 & 2033

- Figure 33: Europe Smart Fall Detection System Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Smart Fall Detection System Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Smart Fall Detection System Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Smart Fall Detection System Volume (K), by Country 2025 & 2033

- Figure 37: Europe Smart Fall Detection System Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Smart Fall Detection System Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Smart Fall Detection System Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Smart Fall Detection System Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Smart Fall Detection System Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Smart Fall Detection System Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Smart Fall Detection System Revenue (undefined), by Type 2025 & 2033

- Figure 44: Middle East & Africa Smart Fall Detection System Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Smart Fall Detection System Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Smart Fall Detection System Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Smart Fall Detection System Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Smart Fall Detection System Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Smart Fall Detection System Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Smart Fall Detection System Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Smart Fall Detection System Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Smart Fall Detection System Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Smart Fall Detection System Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Smart Fall Detection System Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Smart Fall Detection System Revenue (undefined), by Type 2025 & 2033

- Figure 56: Asia Pacific Smart Fall Detection System Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Smart Fall Detection System Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Smart Fall Detection System Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Smart Fall Detection System Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Smart Fall Detection System Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Smart Fall Detection System Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Smart Fall Detection System Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Smart Fall Detection System Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Smart Fall Detection System Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Smart Fall Detection System Revenue undefined Forecast, by Type 2020 & 2033

- Table 4: Global Smart Fall Detection System Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Smart Fall Detection System Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Smart Fall Detection System Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Smart Fall Detection System Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Smart Fall Detection System Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Smart Fall Detection System Revenue undefined Forecast, by Type 2020 & 2033

- Table 10: Global Smart Fall Detection System Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Smart Fall Detection System Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Smart Fall Detection System Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Smart Fall Detection System Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Smart Fall Detection System Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Smart Fall Detection System Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: Global Smart Fall Detection System Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Smart Fall Detection System Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Smart Fall Detection System Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Smart Fall Detection System Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Smart Fall Detection System Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Smart Fall Detection System Revenue undefined Forecast, by Type 2020 & 2033

- Table 34: Global Smart Fall Detection System Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Smart Fall Detection System Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Smart Fall Detection System Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Smart Fall Detection System Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Smart Fall Detection System Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Smart Fall Detection System Revenue undefined Forecast, by Type 2020 & 2033

- Table 58: Global Smart Fall Detection System Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Smart Fall Detection System Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Smart Fall Detection System Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Smart Fall Detection System Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Smart Fall Detection System Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Smart Fall Detection System Revenue undefined Forecast, by Type 2020 & 2033

- Table 76: Global Smart Fall Detection System Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Smart Fall Detection System Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Smart Fall Detection System Volume K Forecast, by Country 2020 & 2033

- Table 79: China Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Smart Fall Detection System Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Smart Fall Detection System Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Smart Fall Detection System?

The projected CAGR is approximately 15.53%.

2. Which companies are prominent players in the Smart Fall Detection System?

Key companies in the market include GIGABYTE Global, Philips Lifeline, Tunstall Healthcare Group, LifeFone, ADT Corporation, MobileHelp, Nihon Kohden, Medical Guardian, Bay Alarm Medical, LifeStation, Edan, Tsingray Technology.

3. What are the main segments of the Smart Fall Detection System?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Smart Fall Detection System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Smart Fall Detection System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Smart Fall Detection System?

To stay informed about further developments, trends, and reports in the Smart Fall Detection System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence