Key Insights

The European bioplastics market is poised for significant expansion, driven by escalating environmental consciousness and stringent waste management regulations. The market, valued at approximately 0.67 million in the base year 2025, is projected to achieve a Compound Annual Growth Rate (CAGR) of 17.96% from 2025 to 2033. This growth trajectory is supported by increasing demand for sustainable packaging across diverse sectors, including flexible and rigid packaging, automotive, agriculture, construction, and textiles. The widespread adoption of bio-based biodegradable materials, offering eco-friendly alternatives to conventional plastics, is a primary growth catalyst. Additionally, technological advancements in bioplastics are enhancing material performance, broadening their applicability in demanding applications. Key European markets, such as Germany, France, Italy, and the United Kingdom, are leading this growth, bolstered by robust infrastructure and heightened consumer awareness of sustainable product choices.

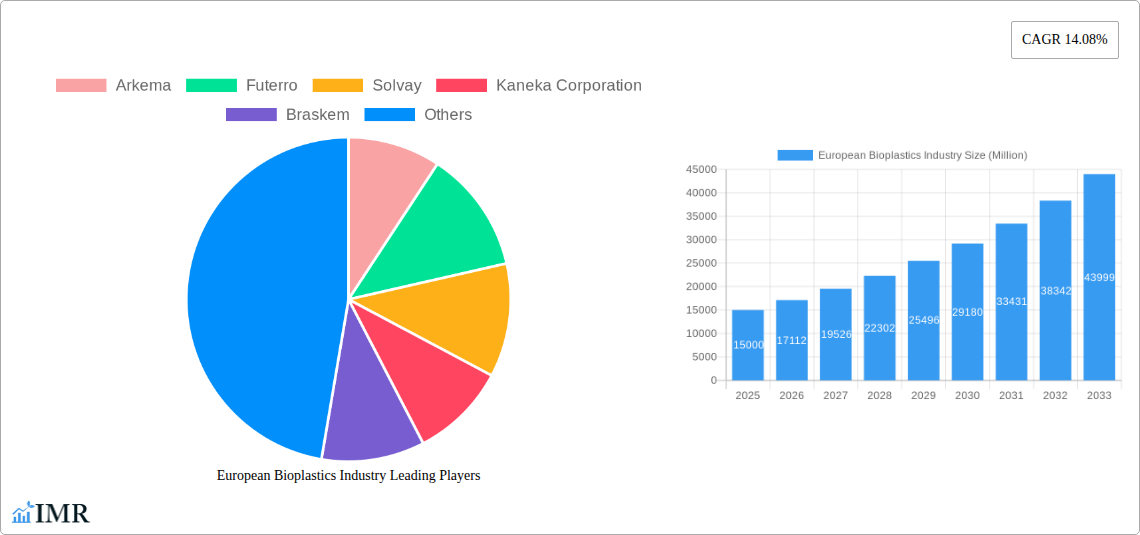

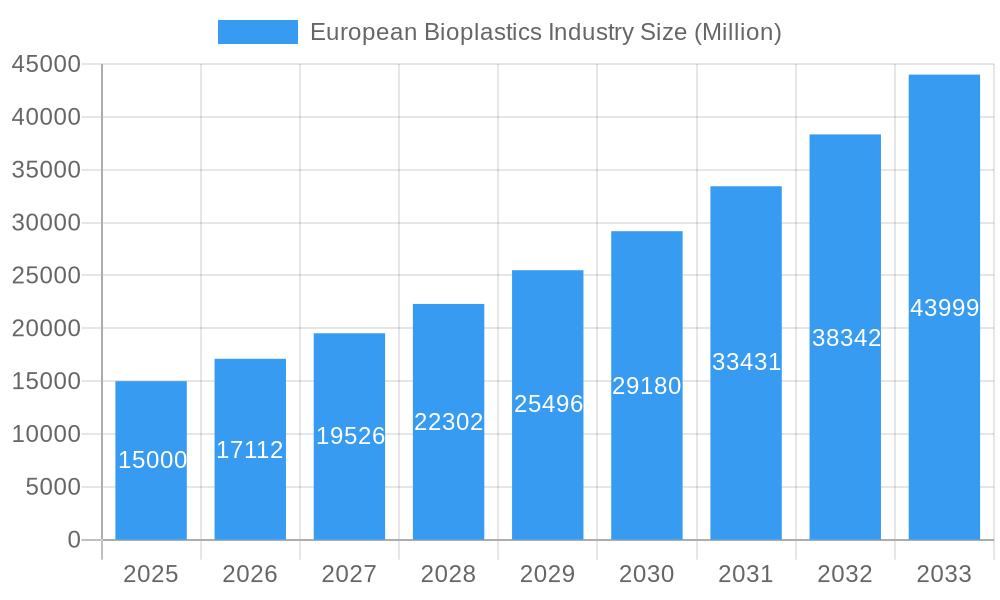

European Bioplastics Industry Market Size (In Million)

Despite the positive outlook, the market encounters obstacles. The comparatively higher production costs of bioplastics versus traditional plastics present a notable restraint to broad adoption. Furthermore, insufficient standardized infrastructure for the collection and composting of bioplastics impedes their full lifecycle sustainability. Nevertheless, the long-term prospects for the European bioplastics industry remain strong, propelled by supportive governmental policies promoting circular economy principles and a growing consumer preference for environmentally responsible products. Leading industry players, including Arkema, Futerro, and Solvay, are actively investing in research and development to enhance bioplastic performance and reduce costs, thereby accelerating market growth. Segments expected to experience the most rapid expansion include bio-based biodegradable materials for flexible packaging and applications within the agricultural sector, owing to their advantageous properties and suitability for these specific uses.

European Bioplastics Industry Company Market Share

European Bioplastics Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the European bioplastics industry, encompassing market dynamics, growth trends, dominant segments, and key players. It offers invaluable insights for industry professionals, investors, and strategic decision-makers seeking to navigate this rapidly evolving sector. The report covers the period 2019-2033, with a focus on the 2025 market, incorporating historical data, current market conditions, and future projections. The total market value for 2025 is estimated at €XX Million.

Study Period: 2019–2033 | Base Year: 2025 | Estimated Year: 2025 | Forecast Period: 2025–2033 | Historical Period: 2019–2024

European Bioplastics Industry Market Dynamics & Structure

The European bioplastics market is characterized by moderate concentration, with several major players holding significant market share. Technological innovation, driven by increasing demand for sustainable materials and stringent environmental regulations, is a key driver. The regulatory landscape, including the EU's Single-Use Plastics Directive, significantly influences market growth. Competitive pressures from traditional plastics and the availability of bio-based but non-biodegradable alternatives present challenges. M&A activity is expected to increase as companies consolidate their market positions and expand their product portfolios.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately xx% market share in 2025.

- Technological Innovation: Focus on enhanced biodegradability, compostability, and performance parity with conventional plastics.

- Regulatory Framework: Stringent regulations promoting bioplastics adoption and reducing reliance on fossil-fuel-based plastics.

- Competitive Substitutes: Traditional plastics, other bio-based polymers, and recycled plastics pose competition.

- End-User Demographics: Growing consumer awareness of sustainability is driving demand across various sectors.

- M&A Trends: Increased consolidation expected, driven by the need for scale and technological expertise (xx M&A deals projected in 2025-2033).

European Bioplastics Industry Growth Trends & Insights

The European bioplastics market is experiencing robust growth, driven by increasing consumer demand for sustainable products, supportive government policies, and technological advancements leading to improved performance characteristics and cost competitiveness. The market is projected to register a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), reaching an estimated value of €XX Million by 2033. This growth is fueled by the rising adoption of bioplastics in various applications, including packaging, agriculture, and automotive sectors. Technological disruptions, such as advancements in bio-based polymer synthesis and improved biodegradability techniques, are further accelerating market expansion. Consumer behavior shifts toward eco-friendly products and a growing awareness of environmental concerns are crucial factors underpinning this growth. Market penetration is expected to reach xx% by 2033.

Dominant Regions, Countries, or Segments in European Bioplastics Industry

Germany, France, and the UK are currently the leading markets for bioplastics in Europe, driven by strong environmental regulations, robust recycling infrastructure, and a significant presence of key industry players. Within product types, Bio-based Biodegradables holds the largest market share, fueled by increasing demand for compostable packaging and agricultural films. In terms of application, Flexible Packaging is currently the dominant segment, followed by Rigid Packaging and Agriculture & Horticulture. The growth in these segments is spurred by factors such as increased consumer preference for sustainable packaging solutions, supportive government policies promoting the use of biodegradable materials in packaging, and advancements in bioplastic technology to meet the stringent performance requirements of various applications.

- Key Drivers (Germany): Strong government support for renewable resources, established chemical industry, high consumer awareness of sustainability.

- Key Drivers (France): Significant investments in bio-based research and development, supportive regulatory environment, growing demand from the agricultural sector.

- Key Drivers (UK): Growing consumer demand for eco-friendly products, increasing focus on plastic waste reduction, supportive policy frameworks.

- Dominant Product Type: Bio-based Biodegradables (estimated xx% market share in 2025)

- Dominant Application: Flexible Packaging (estimated xx% market share in 2025)

European Bioplastics Industry Product Landscape

The European bioplastics market showcases a diverse range of products, including bio-based polylactic acid (PLA), polyhydroxyalkanoates (PHAs), and bio-based polyethylene (PE). Innovation is focused on enhancing biodegradability, compostability, and mechanical properties to match or surpass conventional plastics. Key selling propositions include sustainability credentials, reduced carbon footprint, and improved biodegradability compared to traditional plastics. Technological advancements focus on developing more cost-effective and efficient production methods, enhancing the barrier properties of bioplastics, and expanding their application range.

Key Drivers, Barriers & Challenges in European Bioplastics Industry

Key Drivers:

- Increasing consumer demand for sustainable products.

- Stringent environmental regulations promoting bioplastics adoption.

- Technological advancements enhancing the performance and cost-effectiveness of bioplastics.

- Government incentives and subsidies supporting bioplastics production and use.

Key Challenges:

- Higher production costs compared to conventional plastics, limiting market penetration (estimated xx% price premium in 2025).

- Limited availability of suitable feedstocks for bioplastic production, posing supply chain issues.

- Concerns regarding the biodegradability and compostability of certain bioplastics under various conditions.

- Competition from traditional plastics and other sustainable materials.

Emerging Opportunities in European Bioplastics Industry

Emerging opportunities lie in developing bioplastics for specialized applications, including medical devices, electronics, and advanced packaging solutions. Untapped markets exist in developing countries within Europe and expanding into new applications like construction materials and textiles. Evolving consumer preferences for sustainable and eco-friendly products present a strong growth driver.

Growth Accelerators in the European Bioplastics Industry

Technological breakthroughs in bio-based polymer synthesis, the development of highly efficient and scalable production processes, and strategic partnerships between bioplastic producers and downstream users are crucial catalysts for long-term market growth. Expanding into new applications and markets through innovation and strategic investments will drive accelerated growth in the years to come.

Key Players Shaping the European Bioplastics Industry Market

- Arkema

- Futerro

- Solvay

- Kaneka Corporation

- Braskem

- Mitsubishi Chemical Corporation

- Maccaferri Industrial Group

- Corbion

- BASF SE

- Toray International Inc

- Trinseo

- Dow

- Novamont SpA

- Natureworks LLC

- Danimer Scientific

Notable Milestones in European Bioplastics Industry Sector

- February 2022: Carbios and Indorama Ventures announced a partnership for bio-recycled PET in France with a processing capacity estimated at 50,000 tons. This signifies a major step towards scaling up the production of sustainable PET alternatives.

In-Depth European Bioplastics Industry Market Outlook

The European bioplastics market is poised for sustained growth, driven by strong tailwinds from increased consumer demand for sustainable products, supportive government policies, and continuous advancements in bioplastic technology. Strategic partnerships, investments in research and development, and expansion into new applications and markets will further fuel market expansion, presenting significant opportunities for industry players. The market is expected to witness substantial growth and innovation in the coming decade.

European Bioplastics Industry Segmentation

-

1. Product Type

-

1.1. Bio-based Biodegradables

- 1.1.1. Starch-based

- 1.1.2. Polylactic Acid (PLA)

- 1.1.3. Polyhydroxyalkanoates (PHA)

- 1.1.4. Polyester (PBS, PBAT, and PCL)

- 1.1.5. Other Bio-based Biodegradables

-

1.2. Bio-based Non-biodegradables

- 1.2.1. Bio-polyethylene Terephthalate

- 1.2.2. Bio-polyamides

- 1.2.3. Bio-polytrimethylene Terephthalate

- 1.2.4. Other Bio-based Non-biodegradables

-

1.1. Bio-based Biodegradables

-

2. Application

- 2.1. Flexible Packaging

- 2.2. Rigid Packaging

- 2.3. Automotive and Assembly Operations

- 2.4. Agriculture and Horticulture

- 2.5. Construction

- 2.6. Textiles

- 2.7. Electrical and Electronics

- 2.8. Other Applications

European Bioplastics Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. Italy

- 4. France

- 5. Spain

- 6. Russia

- 7. Nordic Countries

- 8. Rest of Europe

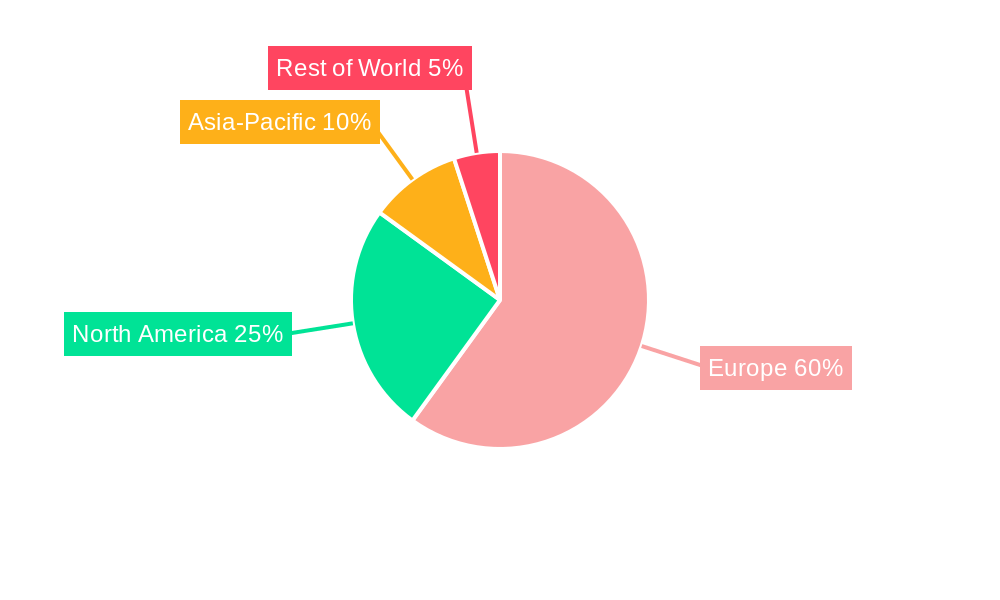

European Bioplastics Industry Regional Market Share

Geographic Coverage of European Bioplastics Industry

European Bioplastics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.98% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Bio-based Biodegradables

- 5.1.1.1. Starch-based

- 5.1.1.2. Polylactic Acid (PLA)

- 5.1.1.3. Polyhydroxyalkanoates (PHA)

- 5.1.1.4. Polyester (PBS, PBAT, and PCL)

- 5.1.1.5. Other Bio-based Biodegradables

- 5.1.2. Bio-based Non-biodegradables

- 5.1.2.1. Bio-polyethylene Terephthalate

- 5.1.2.2. Bio-polyamides

- 5.1.2.3. Bio-polytrimethylene Terephthalate

- 5.1.2.4. Other Bio-based Non-biodegradables

- 5.1.1. Bio-based Biodegradables

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Flexible Packaging

- 5.2.2. Rigid Packaging

- 5.2.3. Automotive and Assembly Operations

- 5.2.4. Agriculture and Horticulture

- 5.2.5. Construction

- 5.2.6. Textiles

- 5.2.7. Electrical and Electronics

- 5.2.8. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. Italy

- 5.3.4. France

- 5.3.5. Spain

- 5.3.6. Russia

- 5.3.7. Nordic Countries

- 5.3.8. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. European Bioplastics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Bio-based Biodegradables

- 6.1.1.1. Starch-based

- 6.1.1.2. Polylactic Acid (PLA)

- 6.1.1.3. Polyhydroxyalkanoates (PHA)

- 6.1.1.4. Polyester (PBS, PBAT, and PCL)

- 6.1.1.5. Other Bio-based Biodegradables

- 6.1.2. Bio-based Non-biodegradables

- 6.1.2.1. Bio-polyethylene Terephthalate

- 6.1.2.2. Bio-polyamides

- 6.1.2.3. Bio-polytrimethylene Terephthalate

- 6.1.2.4. Other Bio-based Non-biodegradables

- 6.1.1. Bio-based Biodegradables

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Flexible Packaging

- 6.2.2. Rigid Packaging

- 6.2.3. Automotive and Assembly Operations

- 6.2.4. Agriculture and Horticulture

- 6.2.5. Construction

- 6.2.6. Textiles

- 6.2.7. Electrical and Electronics

- 6.2.8. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Germany European Bioplastics Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Bio-based Biodegradables

- 7.1.1.1. Starch-based

- 7.1.1.2. Polylactic Acid (PLA)

- 7.1.1.3. Polyhydroxyalkanoates (PHA)

- 7.1.1.4. Polyester (PBS, PBAT, and PCL)

- 7.1.1.5. Other Bio-based Biodegradables

- 7.1.2. Bio-based Non-biodegradables

- 7.1.2.1. Bio-polyethylene Terephthalate

- 7.1.2.2. Bio-polyamides

- 7.1.2.3. Bio-polytrimethylene Terephthalate

- 7.1.2.4. Other Bio-based Non-biodegradables

- 7.1.1. Bio-based Biodegradables

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Flexible Packaging

- 7.2.2. Rigid Packaging

- 7.2.3. Automotive and Assembly Operations

- 7.2.4. Agriculture and Horticulture

- 7.2.5. Construction

- 7.2.6. Textiles

- 7.2.7. Electrical and Electronics

- 7.2.8. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. United Kingdom European Bioplastics Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Bio-based Biodegradables

- 8.1.1.1. Starch-based

- 8.1.1.2. Polylactic Acid (PLA)

- 8.1.1.3. Polyhydroxyalkanoates (PHA)

- 8.1.1.4. Polyester (PBS, PBAT, and PCL)

- 8.1.1.5. Other Bio-based Biodegradables

- 8.1.2. Bio-based Non-biodegradables

- 8.1.2.1. Bio-polyethylene Terephthalate

- 8.1.2.2. Bio-polyamides

- 8.1.2.3. Bio-polytrimethylene Terephthalate

- 8.1.2.4. Other Bio-based Non-biodegradables

- 8.1.1. Bio-based Biodegradables

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Flexible Packaging

- 8.2.2. Rigid Packaging

- 8.2.3. Automotive and Assembly Operations

- 8.2.4. Agriculture and Horticulture

- 8.2.5. Construction

- 8.2.6. Textiles

- 8.2.7. Electrical and Electronics

- 8.2.8. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Italy European Bioplastics Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Bio-based Biodegradables

- 9.1.1.1. Starch-based

- 9.1.1.2. Polylactic Acid (PLA)

- 9.1.1.3. Polyhydroxyalkanoates (PHA)

- 9.1.1.4. Polyester (PBS, PBAT, and PCL)

- 9.1.1.5. Other Bio-based Biodegradables

- 9.1.2. Bio-based Non-biodegradables

- 9.1.2.1. Bio-polyethylene Terephthalate

- 9.1.2.2. Bio-polyamides

- 9.1.2.3. Bio-polytrimethylene Terephthalate

- 9.1.2.4. Other Bio-based Non-biodegradables

- 9.1.1. Bio-based Biodegradables

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Flexible Packaging

- 9.2.2. Rigid Packaging

- 9.2.3. Automotive and Assembly Operations

- 9.2.4. Agriculture and Horticulture

- 9.2.5. Construction

- 9.2.6. Textiles

- 9.2.7. Electrical and Electronics

- 9.2.8. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. France European Bioplastics Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Bio-based Biodegradables

- 10.1.1.1. Starch-based

- 10.1.1.2. Polylactic Acid (PLA)

- 10.1.1.3. Polyhydroxyalkanoates (PHA)

- 10.1.1.4. Polyester (PBS, PBAT, and PCL)

- 10.1.1.5. Other Bio-based Biodegradables

- 10.1.2. Bio-based Non-biodegradables

- 10.1.2.1. Bio-polyethylene Terephthalate

- 10.1.2.2. Bio-polyamides

- 10.1.2.3. Bio-polytrimethylene Terephthalate

- 10.1.2.4. Other Bio-based Non-biodegradables

- 10.1.1. Bio-based Biodegradables

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Flexible Packaging

- 10.2.2. Rigid Packaging

- 10.2.3. Automotive and Assembly Operations

- 10.2.4. Agriculture and Horticulture

- 10.2.5. Construction

- 10.2.6. Textiles

- 10.2.7. Electrical and Electronics

- 10.2.8. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. Spain European Bioplastics Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 11.1.1. Bio-based Biodegradables

- 11.1.1.1. Starch-based

- 11.1.1.2. Polylactic Acid (PLA)

- 11.1.1.3. Polyhydroxyalkanoates (PHA)

- 11.1.1.4. Polyester (PBS, PBAT, and PCL)

- 11.1.1.5. Other Bio-based Biodegradables

- 11.1.2. Bio-based Non-biodegradables

- 11.1.2.1. Bio-polyethylene Terephthalate

- 11.1.2.2. Bio-polyamides

- 11.1.2.3. Bio-polytrimethylene Terephthalate

- 11.1.2.4. Other Bio-based Non-biodegradables

- 11.1.1. Bio-based Biodegradables

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Flexible Packaging

- 11.2.2. Rigid Packaging

- 11.2.3. Automotive and Assembly Operations

- 11.2.4. Agriculture and Horticulture

- 11.2.5. Construction

- 11.2.6. Textiles

- 11.2.7. Electrical and Electronics

- 11.2.8. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Product Type

- 12. Russia European Bioplastics Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 12.1.1. Bio-based Biodegradables

- 12.1.1.1. Starch-based

- 12.1.1.2. Polylactic Acid (PLA)

- 12.1.1.3. Polyhydroxyalkanoates (PHA)

- 12.1.1.4. Polyester (PBS, PBAT, and PCL)

- 12.1.1.5. Other Bio-based Biodegradables

- 12.1.2. Bio-based Non-biodegradables

- 12.1.2.1. Bio-polyethylene Terephthalate

- 12.1.2.2. Bio-polyamides

- 12.1.2.3. Bio-polytrimethylene Terephthalate

- 12.1.2.4. Other Bio-based Non-biodegradables

- 12.1.1. Bio-based Biodegradables

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Flexible Packaging

- 12.2.2. Rigid Packaging

- 12.2.3. Automotive and Assembly Operations

- 12.2.4. Agriculture and Horticulture

- 12.2.5. Construction

- 12.2.6. Textiles

- 12.2.7. Electrical and Electronics

- 12.2.8. Other Applications

- 12.1. Market Analysis, Insights and Forecast - by Product Type

- 13. Nordic Countries European Bioplastics Industry Analysis, Insights and Forecast, 2020-2032

- 13.1. Market Analysis, Insights and Forecast - by Product Type

- 13.1.1. Bio-based Biodegradables

- 13.1.1.1. Starch-based

- 13.1.1.2. Polylactic Acid (PLA)

- 13.1.1.3. Polyhydroxyalkanoates (PHA)

- 13.1.1.4. Polyester (PBS, PBAT, and PCL)

- 13.1.1.5. Other Bio-based Biodegradables

- 13.1.2. Bio-based Non-biodegradables

- 13.1.2.1. Bio-polyethylene Terephthalate

- 13.1.2.2. Bio-polyamides

- 13.1.2.3. Bio-polytrimethylene Terephthalate

- 13.1.2.4. Other Bio-based Non-biodegradables

- 13.1.1. Bio-based Biodegradables

- 13.2. Market Analysis, Insights and Forecast - by Application

- 13.2.1. Flexible Packaging

- 13.2.2. Rigid Packaging

- 13.2.3. Automotive and Assembly Operations

- 13.2.4. Agriculture and Horticulture

- 13.2.5. Construction

- 13.2.6. Textiles

- 13.2.7. Electrical and Electronics

- 13.2.8. Other Applications

- 13.1. Market Analysis, Insights and Forecast - by Product Type

- 14. Rest of Europe European Bioplastics Industry Analysis, Insights and Forecast, 2020-2032

- 14.1. Market Analysis, Insights and Forecast - by Product Type

- 14.1.1. Bio-based Biodegradables

- 14.1.1.1. Starch-based

- 14.1.1.2. Polylactic Acid (PLA)

- 14.1.1.3. Polyhydroxyalkanoates (PHA)

- 14.1.1.4. Polyester (PBS, PBAT, and PCL)

- 14.1.1.5. Other Bio-based Biodegradables

- 14.1.2. Bio-based Non-biodegradables

- 14.1.2.1. Bio-polyethylene Terephthalate

- 14.1.2.2. Bio-polyamides

- 14.1.2.3. Bio-polytrimethylene Terephthalate

- 14.1.2.4. Other Bio-based Non-biodegradables

- 14.1.1. Bio-based Biodegradables

- 14.2. Market Analysis, Insights and Forecast - by Application

- 14.2.1. Flexible Packaging

- 14.2.2. Rigid Packaging

- 14.2.3. Automotive and Assembly Operations

- 14.2.4. Agriculture and Horticulture

- 14.2.5. Construction

- 14.2.6. Textiles

- 14.2.7. Electrical and Electronics

- 14.2.8. Other Applications

- 14.1. Market Analysis, Insights and Forecast - by Product Type

- 15. Competitive Analysis

- 15.1. Company Profiles

- 15.1.1 Arkema

- 15.1.1.1. Company Overview

- 15.1.1.2. Products

- 15.1.1.3. Company Financials

- 15.1.1.4. SWOT Analysis

- 15.1.2 Futerro

- 15.1.2.1. Company Overview

- 15.1.2.2. Products

- 15.1.2.3. Company Financials

- 15.1.2.4. SWOT Analysis

- 15.1.3 Solvay

- 15.1.3.1. Company Overview

- 15.1.3.2. Products

- 15.1.3.3. Company Financials

- 15.1.3.4. SWOT Analysis

- 15.1.4 Kaneka Corporation

- 15.1.4.1. Company Overview

- 15.1.4.2. Products

- 15.1.4.3. Company Financials

- 15.1.4.4. SWOT Analysis

- 15.1.5 Braskem

- 15.1.5.1. Company Overview

- 15.1.5.2. Products

- 15.1.5.3. Company Financials

- 15.1.5.4. SWOT Analysis

- 15.1.6 Mitsubishi Chemical Corporation

- 15.1.6.1. Company Overview

- 15.1.6.2. Products

- 15.1.6.3. Company Financials

- 15.1.6.4. SWOT Analysis

- 15.1.7 Maccaferri Industrial Group

- 15.1.7.1. Company Overview

- 15.1.7.2. Products

- 15.1.7.3. Company Financials

- 15.1.7.4. SWOT Analysis

- 15.1.8 Corbion

- 15.1.8.1. Company Overview

- 15.1.8.2. Products

- 15.1.8.3. Company Financials

- 15.1.8.4. SWOT Analysis

- 15.1.9 BASF SE

- 15.1.9.1. Company Overview

- 15.1.9.2. Products

- 15.1.9.3. Company Financials

- 15.1.9.4. SWOT Analysis

- 15.1.10 Toray International Inc

- 15.1.10.1. Company Overview

- 15.1.10.2. Products

- 15.1.10.3. Company Financials

- 15.1.10.4. SWOT Analysis

- 15.1.11 Trinseo

- 15.1.11.1. Company Overview

- 15.1.11.2. Products

- 15.1.11.3. Company Financials

- 15.1.11.4. SWOT Analysis

- 15.1.12 Dow

- 15.1.12.1. Company Overview

- 15.1.12.2. Products

- 15.1.12.3. Company Financials

- 15.1.12.4. SWOT Analysis

- 15.1.13 Novamont SpA

- 15.1.13.1. Company Overview

- 15.1.13.2. Products

- 15.1.13.3. Company Financials

- 15.1.13.4. SWOT Analysis

- 15.1.14 Natureworks LLC

- 15.1.14.1. Company Overview

- 15.1.14.2. Products

- 15.1.14.3. Company Financials

- 15.1.14.4. SWOT Analysis

- 15.1.15 Danimer Scientific

- 15.1.15.1. Company Overview

- 15.1.15.2. Products

- 15.1.15.3. Company Financials

- 15.1.15.4. SWOT Analysis

- 15.1.1 Arkema

- 15.2. Market Entropy

- 15.2.1 Company's Key Areas Served

- 15.2.2 Recent Developments

- 15.3. Company Market Share Analysis 2025

- 15.3.1 Top 5 Companies Market Share Analysis

- 15.3.2 Top 3 Companies Market Share Analysis

- 15.4. List of Potential Customers

- 16. Research Methodology

List of Figures

- Figure 1: European Bioplastics Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: European Bioplastics Industry Share (%) by Company 2025

List of Tables

- Table 1: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 3: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 5: European Bioplastics Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: European Bioplastics Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 9: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 10: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 11: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 14: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 15: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 16: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 17: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 19: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 20: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 21: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 22: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 23: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 25: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 26: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 27: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 28: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 29: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 31: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 32: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 33: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 34: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 35: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 36: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 37: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 38: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 39: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 40: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 41: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 42: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 43: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 44: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 45: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 46: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 47: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 48: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 49: European Bioplastics Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 50: European Bioplastics Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 51: European Bioplastics Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 52: European Bioplastics Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 53: European Bioplastics Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 54: European Bioplastics Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Bioplastics Industry?

The projected CAGR is approximately 17.98%.

2. Which companies are prominent players in the European Bioplastics Industry?

Key companies in the market include Arkema, Futerro, Solvay, Kaneka Corporation, Braskem, Mitsubishi Chemical Corporation, Maccaferri Industrial Group, Corbion, BASF SE, Toray International Inc, Trinseo, Dow, Novamont SpA, Natureworks LLC, Danimer Scientific.

3. What are the main segments of the European Bioplastics Industry?

The market segments include Product Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 9.54 billion as of 2022.

5. What are some drivers contributing to market growth?

Environmental Factors Encouraging a Paradigm Shift; Growing Demand for Bioplastics in Flexible Packaging; Other Drivers.

6. What are the notable trends driving market growth?

Flexible Packaging Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

Availability of Cheaper Alternatives; Other Restraints.

8. Can you provide examples of recent developments in the market?

February 2022: Carbios and Indorama Ventures announced their partnership for bio-recycled PET in France with a processing capacity estimated at 50,000 tons.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Bioplastics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Bioplastics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Bioplastics Industry?

To stay informed about further developments, trends, and reports in the European Bioplastics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence