Key Insights

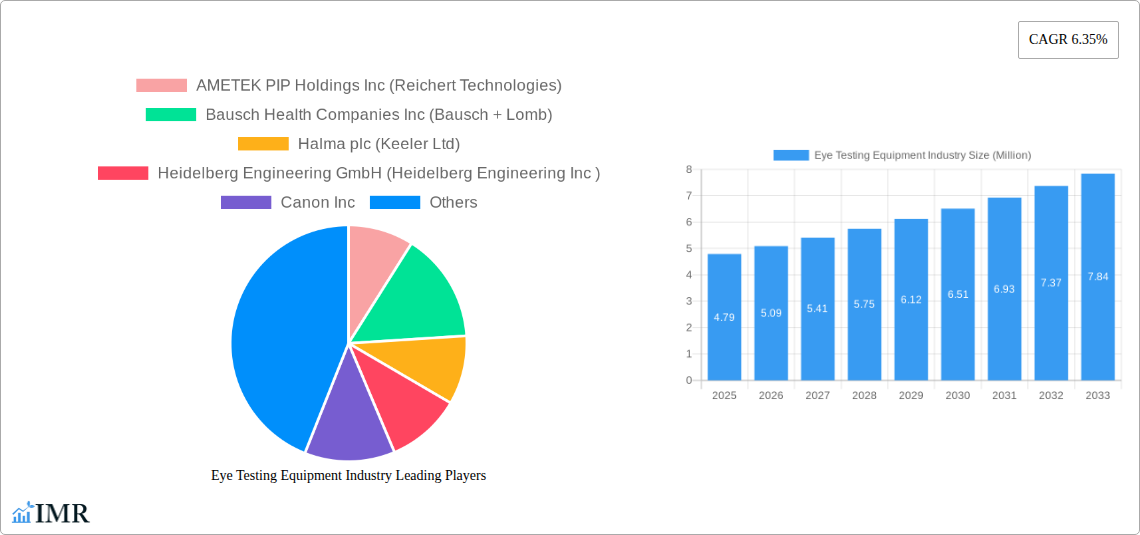

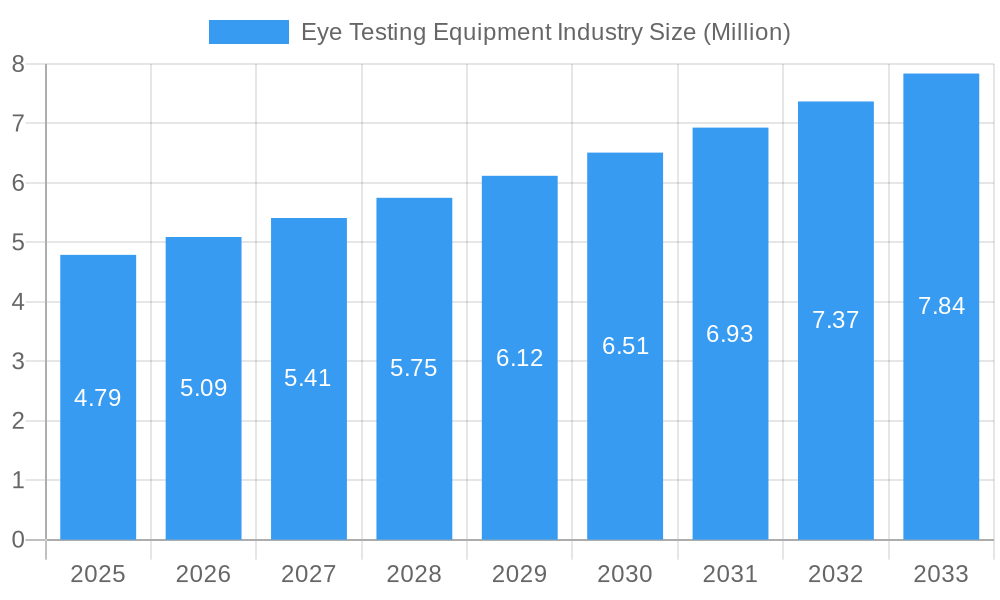

The global Eye Testing Equipment market is poised for substantial growth, projected to reach approximately USD 4.79 million by 2025, with a robust Compound Annual Growth Rate (CAGR) of 6.35% anticipated through 2033. This upward trajectory is significantly fueled by an increasing prevalence of eye disorders, driven by factors such as an aging global population, rising digital screen usage leading to eye strain, and the growing incidence of chronic conditions like diabetes and hypertension, which have ocular implications. Furthermore, advancements in diagnostic technologies, leading to more accurate and non-invasive examination methods, are also acting as key growth drivers. The demand for sophisticated equipment like OCT scanners, visual field analyzers, and wavefront aberrometers is on the rise as eye care professionals strive for earlier and more precise disease detection and management. This technological evolution directly contributes to the market's expansion as healthcare providers invest in state-of-the-art diagnostic tools to improve patient outcomes.

Eye Testing Equipment Industry Market Size (In Million)

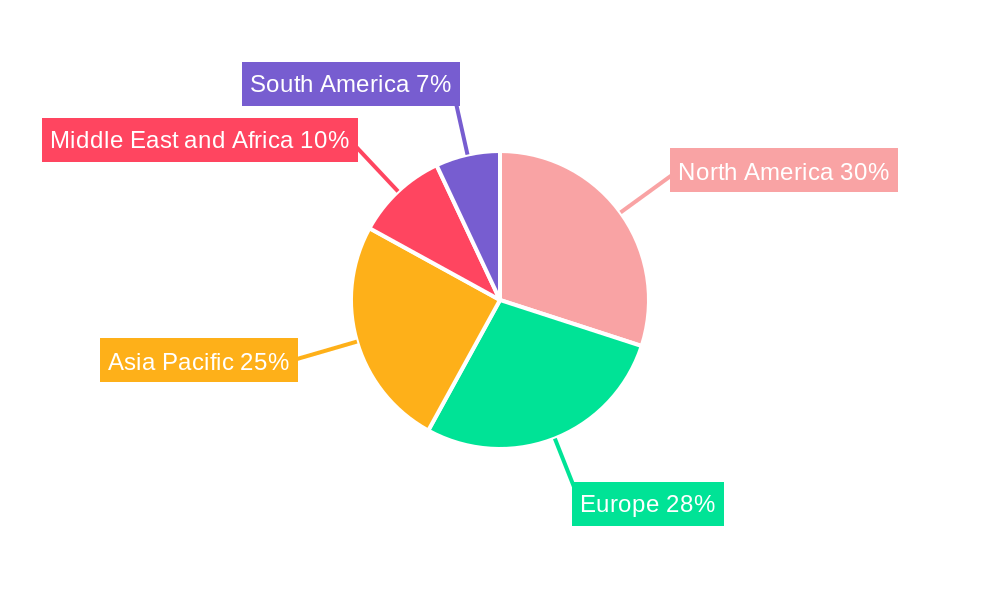

The market segmentation reveals a dynamic landscape with distinct growth potentials across various examination types and end-user segments. Retina examinations, encompassing critical technologies such as OCT scanners and fundus cameras, are expected to witness considerable demand due to the rising burden of retinal diseases like macular degeneration and diabetic retinopathy. Similarly, advancements in cornea examination technologies, including wavefront aberrometers for refractive error correction and specular microscopes for endothelial health assessment, are crucial. General examinations, utilizing autorefractors, tonometers, and phoropters, remain foundational to routine eye care and will continue to constitute a significant market share. Eye clinics and hospitals are the primary end-users, with eye clinics likely to drive early adoption of new technologies, while hospitals will cater to a broader spectrum of complex cases. Geographically, North America and Europe currently dominate the market, driven by advanced healthcare infrastructure and high awareness of eye health. However, the Asia Pacific region is emerging as a significant growth hub, fueled by a large and growing population, increasing healthcare expenditure, and a rising awareness of eye care. Restrains such as the high cost of advanced equipment and the need for specialized training could temper growth in certain developing regions, but the overall outlook remains strongly positive due to the indispensable nature of eye testing for maintaining vision and quality of life.

Eye Testing Equipment Industry Company Market Share

Eye Testing Equipment Industry: Comprehensive Market Analysis & Forecast (2019–2033)

This in-depth report provides a definitive analysis of the global Eye Testing Equipment market, projecting significant growth from 2019 to 2033. It delves into the intricate dynamics, current trends, and future outlook for ophthalmic diagnostic tools, crucial for early detection and management of vision impairments. The study meticulously examines parent and child markets, offering a holistic view of market segmentation by examination type, end-user, and regional dominance. With a base year of 2025 and a forecast period spanning 2025–2033, this report equips industry stakeholders with actionable insights into market size evolution, technological advancements, competitive landscapes, and emerging opportunities.

Eye Testing Equipment Industry Market Dynamics & Structure

The Eye Testing Equipment market is characterized by a moderate level of concentration, with key players like Canon Inc., Carl Zeiss Meditec AG, and Essilor Luxottica holding significant market share. Technological innovation serves as a primary driver, fueled by advancements in imaging technologies, AI-powered diagnostics, and miniaturization of equipment. Regulatory frameworks, particularly those from bodies like the FDA and EMA, play a crucial role in ensuring product safety and efficacy, influencing market entry and product development timelines. Competitive product substitutes, such as advanced smartphone-based diagnostic apps, present an emerging challenge, though they currently complement rather than fully replace traditional equipment. End-user demographics are shifting towards an aging global population, increasing the demand for ophthalmic diagnostics. Mergers and acquisitions (M&A) are a consistent feature, with companies seeking to expand their product portfolios and market reach. For instance, the acquisition of Oculus Inc. by Halma plc (Keeler Ltd) in 2023 highlights consolidation trends. Key market dynamics include:

- Technological Innovation: Continuous development in OCT scanners, fundus cameras, and wavefront aberrometers.

- Regulatory Compliance: Stringent approval processes impacting product launches.

- Aging Population: Growing demand for diagnostic equipment to manage age-related eye conditions.

- M&A Activities: Strategic partnerships and acquisitions for market expansion.

- Emerging Substitutes: Increasing competition from portable and app-based diagnostic tools.

Eye Testing Equipment Industry Growth Trends & Insights

The global Eye Testing Equipment market is poised for robust expansion, driven by a confluence of escalating eye health concerns, technological breakthroughs, and increasing healthcare infrastructure development worldwide. The market size evolution is a testament to the growing awareness of visual health and the critical role of early diagnosis in preventing irreversible vision loss. Adoption rates of advanced diagnostic technologies like Optical Coherence Tomography (OCT) scanners and high-resolution fundus cameras are steadily rising, particularly in developed and rapidly developing economies. These technologies enable earlier and more precise detection of conditions such as diabetic retinopathy, glaucoma, and age-related macular degeneration (AMD).

Technological disruptions are continuously reshaping the market. The integration of artificial intelligence (AI) into ophthalmic imaging analysis is a significant trend, promising to enhance diagnostic accuracy and efficiency. AI algorithms are being developed to automate the detection of abnormalities in retinal images, assisting ophthalmologists in making faster and more informed decisions. Furthermore, the increasing demand for non-invasive and patient-friendly diagnostic procedures is pushing manufacturers to develop more portable and user-friendly equipment. Handheld fundus cameras and compact autorefractor devices are gaining traction, facilitating eye examinations in primary care settings and remote locations.

Consumer behavior shifts are also playing a pivotal role. There is a growing proactive approach towards eye health, with individuals increasingly seeking regular eye check-ups, not just when experiencing symptoms. This heightened awareness, coupled with rising disposable incomes in emerging markets, is fueling the demand for sophisticated eye testing equipment. Teleophthalmology, enabled by advanced imaging and communication technologies, is also emerging as a significant growth avenue, expanding access to specialized eye care services, especially in underserved regions. The projected Compound Annual Growth Rate (CAGR) for the Eye Testing Equipment market is approximately 6.5% during the forecast period, with an estimated market size of $7.2 billion in 2025, projected to reach $11.6 billion by 2033. Market penetration for advanced diagnostic tools is expected to increase from 45% in 2025 to over 60% by 2033.

Dominant Regions, Countries, or Segments in Eye Testing Equipment Industry

The North America region is a dominant force in the global Eye Testing Equipment market, driven by its advanced healthcare infrastructure, high prevalence of eye diseases, and significant investment in research and development. The United States, in particular, represents a major market due to its well-established healthcare system, high disposable incomes, and proactive patient engagement in preventive healthcare. The region's dominance is further amplified by the presence of leading eye care institutions and a strong regulatory framework that encourages the adoption of cutting-edge technologies.

Within the Type of Examination segment, Retina Examination equipment consistently commands a substantial market share. This is largely attributable to the rising incidence of conditions like diabetic retinopathy, glaucoma, and age-related macular degeneration (AMD), which require sophisticated diagnostic tools such as OCT Scanners and Fundus Cameras for early detection and management. The increasing adoption of these advanced imaging modalities in both specialized eye clinics and general hospitals contributes significantly to this segment's growth. The General Examination segment, encompassing devices like Autorefractor and Tonometer, also holds a considerable share due to their widespread use in routine eye screenings and primary care settings.

In terms of End Users, Eye Clinics represent the largest segment, as they are specialized centers for ophthalmic care and are thus early adopters of advanced eye testing equipment. Hospitals, with their comprehensive diagnostic capabilities and patient volume, also contribute significantly to the market's growth. The increasing integration of eye care services within general hospitals further bolsters this segment. The Other End Users category, including optometry practices, research institutions, and mobile eye care units, is also experiencing steady growth, driven by the decentralization of eye care services and innovative delivery models.

Key drivers of dominance in North America include:

- High Prevalence of Eye Diseases: Significant incidence of diabetes-related eye conditions and an aging population prone to vision impairment.

- Advanced Healthcare Infrastructure: Well-equipped hospitals and clinics with a high adoption rate of advanced diagnostic technologies.

- Strong R&D Investment: Continuous innovation and development of next-generation eye testing equipment.

- Favorable Reimbursement Policies: Supportive insurance coverage for diagnostic procedures.

- Patient Awareness and Demand: High consumer awareness regarding eye health and proactive seeking of regular check-ups.

The market share for Retina Examination equipment is estimated at 40% in 2025, while the General Examination segment holds approximately 35%. Eye clinics account for 55% of the end-user market.

Eye Testing Equipment Industry Product Landscape

The product landscape of the Eye Testing Equipment industry is defined by continuous innovation and a focus on enhanced diagnostic accuracy, portability, and patient comfort. Key product categories include sophisticated OCT scanners capable of high-resolution cross-sectional imaging of the retina, advanced fundus cameras for detailed visualization of the posterior segment, and non-mydriatic fundus cameras that eliminate the need for pupil dilation. Wavefront aberrometers are increasingly sophisticated, offering precise measurements for refractive surgery planning and custom lens design. The development of AI-powered diagnostic software integrated with these devices is a major technological advancement, enabling automated detection of anomalies. Furthermore, the trend towards miniaturization has led to the introduction of portable and handheld devices, such as handheld fundus cameras and compact tonometers, expanding the reach of eye care services. These innovations are crucial for early disease detection, personalized treatment, and improved patient outcomes.

Key Drivers, Barriers & Challenges in Eye Testing Equipment Industry

Key Drivers:

The Eye Testing Equipment industry is propelled by several significant drivers. The escalating global prevalence of age-related eye conditions like cataracts and macular degeneration, coupled with the rise in lifestyle-related disorders such as diabetes and hypertension, which significantly impact ocular health, are major demand catalysts. Technological advancements, including the integration of AI and advanced imaging techniques (e.g., OCT, high-resolution fundus photography), are enabling more accurate and early diagnosis, driving market growth. The growing awareness among the general population regarding the importance of regular eye check-ups for preventive care also plays a crucial role. Furthermore, expanding healthcare infrastructure in emerging economies and supportive government initiatives promoting eye care are creating new market opportunities.

Barriers & Challenges:

Despite the positive growth trajectory, the industry faces notable barriers and challenges. High initial investment costs for advanced diagnostic equipment can be a significant deterrent for smaller clinics and healthcare facilities, especially in cost-sensitive markets. Stringent regulatory approvals required for medical devices, though essential for patient safety, can prolong time-to-market for new products. The limited availability of skilled ophthalmologists and trained technicians in certain regions can hinder the optimal utilization of sophisticated equipment. Moreover, the emergence of lower-cost alternatives and the ongoing debate around reimbursement policies for new technologies present competitive pressures and financial uncertainties. Supply chain disruptions, as witnessed during recent global events, can also impact manufacturing and availability. The market size for ophthalmic ultrasound systems is projected to face a CAGR of 5.2% due to cost sensitivities.

Emerging Opportunities in Eye Testing Equipment Industry

Emerging opportunities in the Eye Testing Equipment industry are centered around underserved markets, innovative applications, and evolving consumer preferences. The increasing demand for accessible and affordable eye care in rural and remote areas presents a significant opportunity for portable and handheld diagnostic devices, as well as teleophthalmology solutions. The growing application of AI in image analysis and diagnostic prediction holds immense potential for improving diagnostic accuracy and efficiency, creating demand for AI-integrated equipment. Furthermore, the focus on personalized medicine is driving innovation in diagnostic tools that can provide highly detailed patient-specific data for tailored treatment plans. The expanding geriatric population globally will continue to fuel the demand for equipment catering to age-related vision impairments. The market for wavefront aberrometers is expected to see a CAGR of 7.1%, driven by advancements in refractive surgery and personalized vision correction.

Growth Accelerators in the Eye Testing Equipment Industry Industry

Several factors are acting as growth accelerators for the Eye Testing Equipment industry. The rapid technological advancements, particularly in areas like artificial intelligence, machine learning, and digital imaging, are continuously enhancing the capabilities and accuracy of diagnostic tools. The increasing investment in eye care research and development by both established players and innovative startups is fostering a pipeline of next-generation products. Strategic partnerships and collaborations between technology companies, healthcare providers, and research institutions are accelerating the development and adoption of new solutions. Furthermore, the expanding healthcare expenditure, especially in emerging economies, and the increasing government focus on public health initiatives related to vision care are creating a more conducive market environment. The global adoption of integrated diagnostic platforms, which combine multiple testing modalities, is also a key growth accelerator.

Key Players Shaping the Eye Testing Equipment Industry Market

- AMETEK PIP Holdings Inc (Reichert Technologies)

- Bausch Health Companies Inc (Bausch + Lomb)

- Halma plc (Keeler Ltd)

- Heidelberg Engineering GmbH (Heidelberg Engineering Inc )

- Canon Inc

- Carl Zeiss Meditec AG

- Revenio Group PLC (iCare Finland OY)

- Oculus Inc

- Nidek Co Ltd

- Johnson & Johnson

- Alcon

- Essilor Luxottica (Essilor International SA)

- HEINE Optotechnik

Notable Milestones in Eye Testing Equipment Industry Sector

- July 2022: Sightsavers launched a mobile van under its National Truckers Eye Health Programme in Delhi-NCR, equipped with essential eye testing tools like an ophthalmoscope, retinoscope, lensometer, and vision charts, to provide eye care services to truckers.

- March 2022: Epipole launched its new epiCam fundus camera at Vision Expo East 2022 in New York City. The epiCam is a high-powered, ultra-portable, wireless fundus camera that captures high-resolution live video footage of the retina using its VDO platform.

In-Depth Eye Testing Equipment Industry Market Outlook

The future outlook for the Eye Testing Equipment industry is exceptionally promising, driven by a sustained demand for advanced diagnostic solutions and a growing emphasis on preventive eye care globally. The integration of AI and machine learning into diagnostic workflows will revolutionize disease detection and management, leading to improved patient outcomes. The increasing adoption of teleophthalmology will expand access to specialized eye care services, particularly in underserved regions, further accelerating market growth. Strategic collaborations and the continuous pursuit of technological innovation by key players will introduce novel functionalities and enhance the performance of existing equipment. The industry is well-positioned to capitalize on the expanding healthcare infrastructure in emerging markets and the rising global incidence of vision-impairing conditions, ensuring a robust growth trajectory in the coming years.

Eye Testing Equipment Industry Segmentation

-

1. Type of Examination

-

1.1. Retina Examination

- 1.1.1. OCT Scanner

- 1.1.2. Fundus Camera

- 1.1.3. Visual Field Analyzer

- 1.1.4. Ophthalmoscope

- 1.1.5. Retinoscope

-

1.2. Cornea Examination

- 1.2.1. Wavefront Aberrometer

- 1.2.2. Specular Microscope

- 1.2.3. Other Cornea Examinations

-

1.3. General Examination

- 1.3.1. Autorefractor

- 1.3.2. Ophthalmic Ultrasound System

- 1.3.3. Tonometer

- 1.3.4. Phoropter

- 1.3.5. Keratometer

- 1.3.6. Lensometer

- 1.3.7. Other General Examinations

-

1.1. Retina Examination

-

2. End User

- 2.1. Eye Clinic

- 2.2. Hospital

- 2.3. Other End Users

Eye Testing Equipment Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Eye Testing Equipment Industry Regional Market Share

Geographic Coverage of Eye Testing Equipment Industry

Eye Testing Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.35% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type of Examination

- 5.1.1. Retina Examination

- 5.1.1.1. OCT Scanner

- 5.1.1.2. Fundus Camera

- 5.1.1.3. Visual Field Analyzer

- 5.1.1.4. Ophthalmoscope

- 5.1.1.5. Retinoscope

- 5.1.2. Cornea Examination

- 5.1.2.1. Wavefront Aberrometer

- 5.1.2.2. Specular Microscope

- 5.1.2.3. Other Cornea Examinations

- 5.1.3. General Examination

- 5.1.3.1. Autorefractor

- 5.1.3.2. Ophthalmic Ultrasound System

- 5.1.3.3. Tonometer

- 5.1.3.4. Phoropter

- 5.1.3.5. Keratometer

- 5.1.3.6. Lensometer

- 5.1.3.7. Other General Examinations

- 5.1.1. Retina Examination

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Eye Clinic

- 5.2.2. Hospital

- 5.2.3. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Type of Examination

- 6. Global Eye Testing Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type of Examination

- 6.1.1. Retina Examination

- 6.1.1.1. OCT Scanner

- 6.1.1.2. Fundus Camera

- 6.1.1.3. Visual Field Analyzer

- 6.1.1.4. Ophthalmoscope

- 6.1.1.5. Retinoscope

- 6.1.2. Cornea Examination

- 6.1.2.1. Wavefront Aberrometer

- 6.1.2.2. Specular Microscope

- 6.1.2.3. Other Cornea Examinations

- 6.1.3. General Examination

- 6.1.3.1. Autorefractor

- 6.1.3.2. Ophthalmic Ultrasound System

- 6.1.3.3. Tonometer

- 6.1.3.4. Phoropter

- 6.1.3.5. Keratometer

- 6.1.3.6. Lensometer

- 6.1.3.7. Other General Examinations

- 6.1.1. Retina Examination

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Eye Clinic

- 6.2.2. Hospital

- 6.2.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Type of Examination

- 7. North America Eye Testing Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type of Examination

- 7.1.1. Retina Examination

- 7.1.1.1. OCT Scanner

- 7.1.1.2. Fundus Camera

- 7.1.1.3. Visual Field Analyzer

- 7.1.1.4. Ophthalmoscope

- 7.1.1.5. Retinoscope

- 7.1.2. Cornea Examination

- 7.1.2.1. Wavefront Aberrometer

- 7.1.2.2. Specular Microscope

- 7.1.2.3. Other Cornea Examinations

- 7.1.3. General Examination

- 7.1.3.1. Autorefractor

- 7.1.3.2. Ophthalmic Ultrasound System

- 7.1.3.3. Tonometer

- 7.1.3.4. Phoropter

- 7.1.3.5. Keratometer

- 7.1.3.6. Lensometer

- 7.1.3.7. Other General Examinations

- 7.1.1. Retina Examination

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Eye Clinic

- 7.2.2. Hospital

- 7.2.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Type of Examination

- 8. Europe Eye Testing Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type of Examination

- 8.1.1. Retina Examination

- 8.1.1.1. OCT Scanner

- 8.1.1.2. Fundus Camera

- 8.1.1.3. Visual Field Analyzer

- 8.1.1.4. Ophthalmoscope

- 8.1.1.5. Retinoscope

- 8.1.2. Cornea Examination

- 8.1.2.1. Wavefront Aberrometer

- 8.1.2.2. Specular Microscope

- 8.1.2.3. Other Cornea Examinations

- 8.1.3. General Examination

- 8.1.3.1. Autorefractor

- 8.1.3.2. Ophthalmic Ultrasound System

- 8.1.3.3. Tonometer

- 8.1.3.4. Phoropter

- 8.1.3.5. Keratometer

- 8.1.3.6. Lensometer

- 8.1.3.7. Other General Examinations

- 8.1.1. Retina Examination

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Eye Clinic

- 8.2.2. Hospital

- 8.2.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Type of Examination

- 9. Asia Pacific Eye Testing Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type of Examination

- 9.1.1. Retina Examination

- 9.1.1.1. OCT Scanner

- 9.1.1.2. Fundus Camera

- 9.1.1.3. Visual Field Analyzer

- 9.1.1.4. Ophthalmoscope

- 9.1.1.5. Retinoscope

- 9.1.2. Cornea Examination

- 9.1.2.1. Wavefront Aberrometer

- 9.1.2.2. Specular Microscope

- 9.1.2.3. Other Cornea Examinations

- 9.1.3. General Examination

- 9.1.3.1. Autorefractor

- 9.1.3.2. Ophthalmic Ultrasound System

- 9.1.3.3. Tonometer

- 9.1.3.4. Phoropter

- 9.1.3.5. Keratometer

- 9.1.3.6. Lensometer

- 9.1.3.7. Other General Examinations

- 9.1.1. Retina Examination

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Eye Clinic

- 9.2.2. Hospital

- 9.2.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Type of Examination

- 10. Middle East and Africa Eye Testing Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type of Examination

- 10.1.1. Retina Examination

- 10.1.1.1. OCT Scanner

- 10.1.1.2. Fundus Camera

- 10.1.1.3. Visual Field Analyzer

- 10.1.1.4. Ophthalmoscope

- 10.1.1.5. Retinoscope

- 10.1.2. Cornea Examination

- 10.1.2.1. Wavefront Aberrometer

- 10.1.2.2. Specular Microscope

- 10.1.2.3. Other Cornea Examinations

- 10.1.3. General Examination

- 10.1.3.1. Autorefractor

- 10.1.3.2. Ophthalmic Ultrasound System

- 10.1.3.3. Tonometer

- 10.1.3.4. Phoropter

- 10.1.3.5. Keratometer

- 10.1.3.6. Lensometer

- 10.1.3.7. Other General Examinations

- 10.1.1. Retina Examination

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Eye Clinic

- 10.2.2. Hospital

- 10.2.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Type of Examination

- 11. South America Eye Testing Equipment Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type of Examination

- 11.1.1. Retina Examination

- 11.1.1.1. OCT Scanner

- 11.1.1.2. Fundus Camera

- 11.1.1.3. Visual Field Analyzer

- 11.1.1.4. Ophthalmoscope

- 11.1.1.5. Retinoscope

- 11.1.2. Cornea Examination

- 11.1.2.1. Wavefront Aberrometer

- 11.1.2.2. Specular Microscope

- 11.1.2.3. Other Cornea Examinations

- 11.1.3. General Examination

- 11.1.3.1. Autorefractor

- 11.1.3.2. Ophthalmic Ultrasound System

- 11.1.3.3. Tonometer

- 11.1.3.4. Phoropter

- 11.1.3.5. Keratometer

- 11.1.3.6. Lensometer

- 11.1.3.7. Other General Examinations

- 11.1.1. Retina Examination

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Eye Clinic

- 11.2.2. Hospital

- 11.2.3. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Type of Examination

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 AMETEK PIP Holdings Inc (Reichert Technologies)

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Bausch Health Companies Inc (Bausch + Lomb)

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Halma plc (Keeler Ltd)

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Heidelberg Engineering GmbH (Heidelberg Engineering Inc )

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Canon Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Carl Zeiss Meditec AG

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Revenio Group PLC (iCare Finland OY)

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Oculus Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nidek Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Johnson & Johnson

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Alcon

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Essilor Luxottica (Essilor International SA)

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 HEINE Optotechnik

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 AMETEK PIP Holdings Inc (Reichert Technologies)

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Eye Testing Equipment Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Eye Testing Equipment Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Eye Testing Equipment Industry Revenue (Million), by Type of Examination 2025 & 2033

- Figure 4: North America Eye Testing Equipment Industry Volume (K Unit), by Type of Examination 2025 & 2033

- Figure 5: North America Eye Testing Equipment Industry Revenue Share (%), by Type of Examination 2025 & 2033

- Figure 6: North America Eye Testing Equipment Industry Volume Share (%), by Type of Examination 2025 & 2033

- Figure 7: North America Eye Testing Equipment Industry Revenue (Million), by End User 2025 & 2033

- Figure 8: North America Eye Testing Equipment Industry Volume (K Unit), by End User 2025 & 2033

- Figure 9: North America Eye Testing Equipment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 10: North America Eye Testing Equipment Industry Volume Share (%), by End User 2025 & 2033

- Figure 11: North America Eye Testing Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: North America Eye Testing Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 13: North America Eye Testing Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Eye Testing Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: Europe Eye Testing Equipment Industry Revenue (Million), by Type of Examination 2025 & 2033

- Figure 16: Europe Eye Testing Equipment Industry Volume (K Unit), by Type of Examination 2025 & 2033

- Figure 17: Europe Eye Testing Equipment Industry Revenue Share (%), by Type of Examination 2025 & 2033

- Figure 18: Europe Eye Testing Equipment Industry Volume Share (%), by Type of Examination 2025 & 2033

- Figure 19: Europe Eye Testing Equipment Industry Revenue (Million), by End User 2025 & 2033

- Figure 20: Europe Eye Testing Equipment Industry Volume (K Unit), by End User 2025 & 2033

- Figure 21: Europe Eye Testing Equipment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 22: Europe Eye Testing Equipment Industry Volume Share (%), by End User 2025 & 2033

- Figure 23: Europe Eye Testing Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: Europe Eye Testing Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 25: Europe Eye Testing Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Europe Eye Testing Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Asia Pacific Eye Testing Equipment Industry Revenue (Million), by Type of Examination 2025 & 2033

- Figure 28: Asia Pacific Eye Testing Equipment Industry Volume (K Unit), by Type of Examination 2025 & 2033

- Figure 29: Asia Pacific Eye Testing Equipment Industry Revenue Share (%), by Type of Examination 2025 & 2033

- Figure 30: Asia Pacific Eye Testing Equipment Industry Volume Share (%), by Type of Examination 2025 & 2033

- Figure 31: Asia Pacific Eye Testing Equipment Industry Revenue (Million), by End User 2025 & 2033

- Figure 32: Asia Pacific Eye Testing Equipment Industry Volume (K Unit), by End User 2025 & 2033

- Figure 33: Asia Pacific Eye Testing Equipment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 34: Asia Pacific Eye Testing Equipment Industry Volume Share (%), by End User 2025 & 2033

- Figure 35: Asia Pacific Eye Testing Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Asia Pacific Eye Testing Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 37: Asia Pacific Eye Testing Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Asia Pacific Eye Testing Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East and Africa Eye Testing Equipment Industry Revenue (Million), by Type of Examination 2025 & 2033

- Figure 40: Middle East and Africa Eye Testing Equipment Industry Volume (K Unit), by Type of Examination 2025 & 2033

- Figure 41: Middle East and Africa Eye Testing Equipment Industry Revenue Share (%), by Type of Examination 2025 & 2033

- Figure 42: Middle East and Africa Eye Testing Equipment Industry Volume Share (%), by Type of Examination 2025 & 2033

- Figure 43: Middle East and Africa Eye Testing Equipment Industry Revenue (Million), by End User 2025 & 2033

- Figure 44: Middle East and Africa Eye Testing Equipment Industry Volume (K Unit), by End User 2025 & 2033

- Figure 45: Middle East and Africa Eye Testing Equipment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 46: Middle East and Africa Eye Testing Equipment Industry Volume Share (%), by End User 2025 & 2033

- Figure 47: Middle East and Africa Eye Testing Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: Middle East and Africa Eye Testing Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Middle East and Africa Eye Testing Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East and Africa Eye Testing Equipment Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: South America Eye Testing Equipment Industry Revenue (Million), by Type of Examination 2025 & 2033

- Figure 52: South America Eye Testing Equipment Industry Volume (K Unit), by Type of Examination 2025 & 2033

- Figure 53: South America Eye Testing Equipment Industry Revenue Share (%), by Type of Examination 2025 & 2033

- Figure 54: South America Eye Testing Equipment Industry Volume Share (%), by Type of Examination 2025 & 2033

- Figure 55: South America Eye Testing Equipment Industry Revenue (Million), by End User 2025 & 2033

- Figure 56: South America Eye Testing Equipment Industry Volume (K Unit), by End User 2025 & 2033

- Figure 57: South America Eye Testing Equipment Industry Revenue Share (%), by End User 2025 & 2033

- Figure 58: South America Eye Testing Equipment Industry Volume Share (%), by End User 2025 & 2033

- Figure 59: South America Eye Testing Equipment Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: South America Eye Testing Equipment Industry Volume (K Unit), by Country 2025 & 2033

- Figure 61: South America Eye Testing Equipment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: South America Eye Testing Equipment Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Eye Testing Equipment Industry Revenue Million Forecast, by Type of Examination 2020 & 2033

- Table 2: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Type of Examination 2020 & 2033

- Table 3: Global Eye Testing Equipment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: Global Eye Testing Equipment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 5: Global Eye Testing Equipment Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 7: Global Eye Testing Equipment Industry Revenue Million Forecast, by Type of Examination 2020 & 2033

- Table 8: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Type of Examination 2020 & 2033

- Table 9: Global Eye Testing Equipment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 10: Global Eye Testing Equipment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 11: Global Eye Testing Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 13: United States Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United States Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 15: Canada Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Canada Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 17: Mexico Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Global Eye Testing Equipment Industry Revenue Million Forecast, by Type of Examination 2020 & 2033

- Table 20: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Type of Examination 2020 & 2033

- Table 21: Global Eye Testing Equipment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 22: Global Eye Testing Equipment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 23: Global Eye Testing Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 24: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: Germany Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: Germany Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 27: United Kingdom Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: United Kingdom Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 29: France Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: France Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 31: Italy Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Italy Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Spain Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Spain Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Europe Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Global Eye Testing Equipment Industry Revenue Million Forecast, by Type of Examination 2020 & 2033

- Table 38: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Type of Examination 2020 & 2033

- Table 39: Global Eye Testing Equipment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 40: Global Eye Testing Equipment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 41: Global Eye Testing Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 42: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 43: China Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: China Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 45: Japan Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: Japan Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: India Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: India Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: Australia Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Australia Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 51: South Korea Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: South Korea Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Rest of Asia Pacific Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Asia Pacific Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Global Eye Testing Equipment Industry Revenue Million Forecast, by Type of Examination 2020 & 2033

- Table 56: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Type of Examination 2020 & 2033

- Table 57: Global Eye Testing Equipment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 58: Global Eye Testing Equipment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 59: Global Eye Testing Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: GCC Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: GCC Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: South Africa Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 64: South Africa Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 65: Rest of Middle East and Africa Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 66: Rest of Middle East and Africa Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 67: Global Eye Testing Equipment Industry Revenue Million Forecast, by Type of Examination 2020 & 2033

- Table 68: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Type of Examination 2020 & 2033

- Table 69: Global Eye Testing Equipment Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 70: Global Eye Testing Equipment Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 71: Global Eye Testing Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 72: Global Eye Testing Equipment Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 73: Brazil Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: Brazil Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Argentina Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: Argentina Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Rest of South America Eye Testing Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 78: Rest of South America Eye Testing Equipment Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Eye Testing Equipment Industry?

The projected CAGR is approximately 6.35%.

2. Which companies are prominent players in the Eye Testing Equipment Industry?

Key companies in the market include AMETEK PIP Holdings Inc (Reichert Technologies), Bausch Health Companies Inc (Bausch + Lomb), Halma plc (Keeler Ltd), Heidelberg Engineering GmbH (Heidelberg Engineering Inc ), Canon Inc, Carl Zeiss Meditec AG, Revenio Group PLC (iCare Finland OY), Oculus Inc , Nidek Co Ltd, Johnson & Johnson, Alcon, Essilor Luxottica (Essilor International SA), HEINE Optotechnik.

3. What are the main segments of the Eye Testing Equipment Industry?

The market segments include Type of Examination, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.79 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Prevalence of Eye Diseases; Technological Advancements in Ophthalmic Devices; Increasing Government Initiatives to Control Visual Impairment.

6. What are the notable trends driving market growth?

OCT Scanner Segment is Expected to Hold Significant Market Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Cost of Eye Examination Equipment; Lack of Awareness and Low Accessibility to Eye Care in Low-income Economies.

8. Can you provide examples of recent developments in the market?

In July 2022, a mobile van was launched by Sightsavers under its National Truckers Eye Health Programme with the support of Cholamandalam Investment and Finance Company Limited (Chola) in Delhi-NCR to provide eye care services to the truckers' community. The van is equipped with the necessary tools and supplies, specifically an ophthalmoscope, a retinoscope, trial lenses, trial frames, a lensometer, vision charts, an occluder, and a drum for vision testing.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Eye Testing Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Eye Testing Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Eye Testing Equipment Industry?

To stay informed about further developments, trends, and reports in the Eye Testing Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence