Key Insights

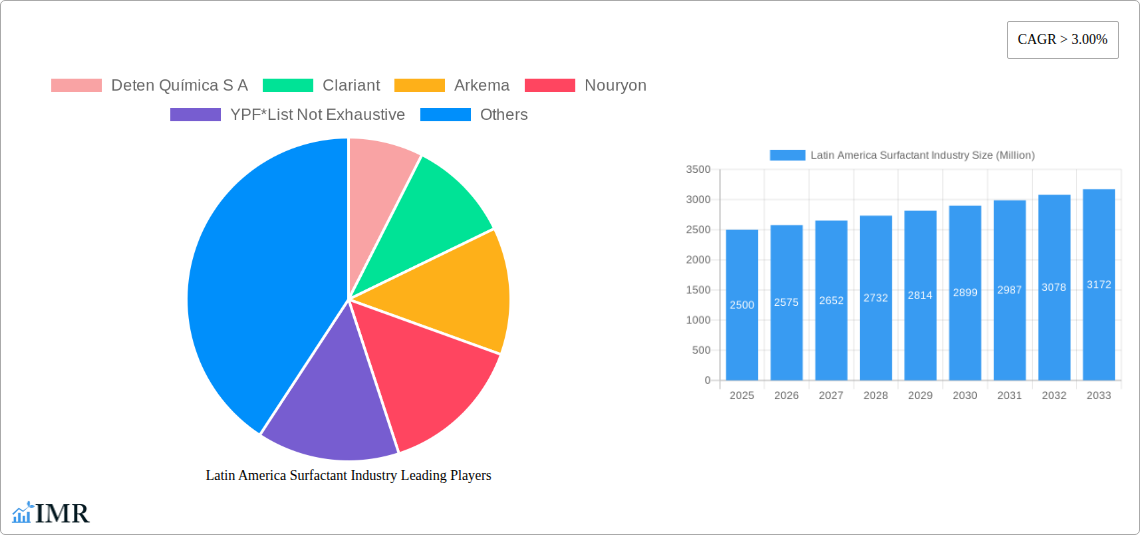

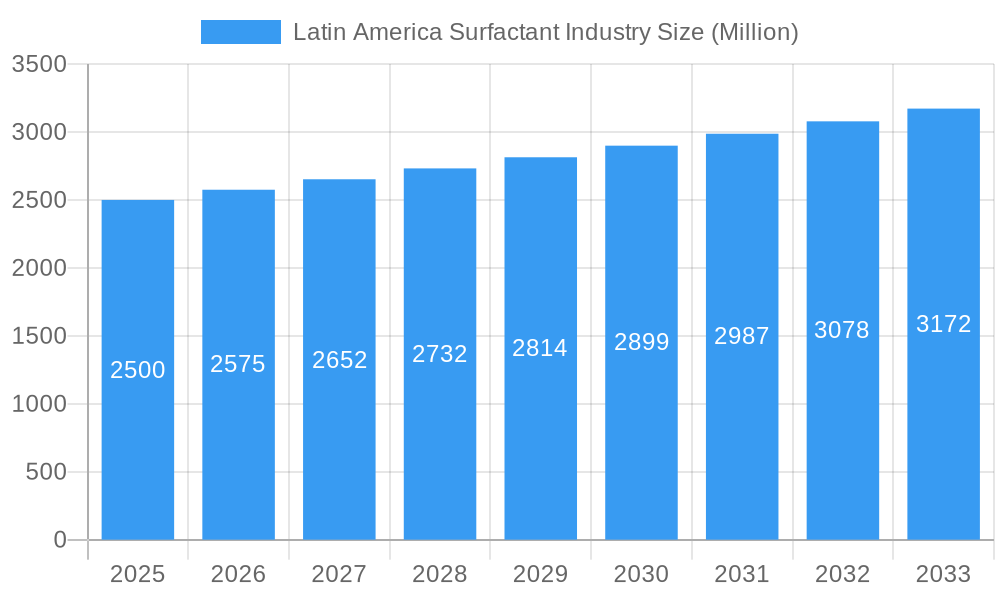

The Latin America Surfactant Industry is poised for robust expansion, with an estimated market size of 4139.4 million in 2025, projected to grow at a Compound Annual Growth Rate (CAGR) of 5.1% through 2033. This significant growth is primarily fueled by increasing demand across key application sectors such as household detergents, personal care products, and industrial cleaners. The region's expanding population, rapid urbanization, and rising disposable incomes are directly translating into higher consumption of consumer goods, thereby bolstering the need for surfactants as essential components. Furthermore, the burgeoning oil & gas industry, agricultural sector, and textile manufacturing in Latin America are critical drivers, utilizing surfactants as emulsifiers, wetting agents, and dispersing agents to enhance operational efficiency and product performance. The versatility of surfactants, spanning amphoteric, anionic, cationic, and non-ionic types, ensures their indispensable role across a wide array of end-user industries.

Latin America Surfactant Industry Market Size (In Billion)

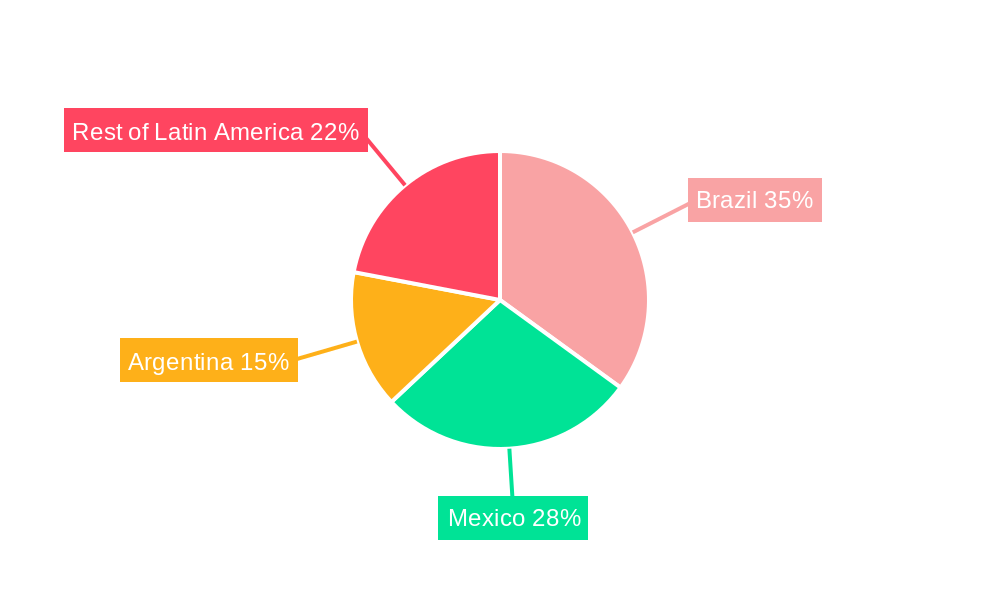

Market trends indicate a pronounced shift towards bio-based and sustainable surfactants, driven by growing environmental awareness and consumer preference for eco-friendly products. Innovations in specialty surfactants, offering enhanced performance characteristics for specific industrial applications, are also shaping market dynamics. While the industry benefits from robust demand, it navigates challenges such as the volatility of raw material prices and evolving regulatory landscapes. The competitive arena sees a blend of global giants like BASF SE, Dow, and Solvay, alongside prominent regional players such as Deten Química S A and Stepan Company, all vying for market share through product innovation and strategic expansions. Countries like Brazil, Mexico, and Argentina remain pivotal markets within the region, driving significant demand through both direct sales and an extensive distributor network, solidifying Latin America's position as a dynamic hub for surfactant industry growth.

Latin America Surfactant Industry Company Market Share

This comprehensive report delves into the intricate dynamics of the Latin America Surfactant Industry, a vital component of the broader chemical sector experiencing robust expansion. Valued at approximately USD 6,500 million in 2025, the market is strategically positioned for significant growth, projected to reach USD 10,500 million by 2033, exhibiting a compelling Compound Annual Growth Rate (CAGR) of 6.2% during the forecast period of 2025-2033. This in-depth analysis provides unparalleled insights into the forces shaping the Latin American surfactants market, from technological advancements and regulatory shifts to evolving consumer preferences and the escalating demand for sustainable chemical solutions. The report meticulously examines the surfactant market trends across key parent markets like household and industrial chemicals, and child markets including specific surfactant types (Anionic, Non-ionic, Amphoteric, Cationic), diverse applications (Detergents, Emulsifiers, Wetting Agents), and critical end-user industries (Household Chemicals, Food, Oil & Gas, Agriculture, Textile, Pharmaceutical). Discover how sustainability initiatives, coupled with rapid industrialization and urbanization across Brazil, Mexico, Argentina, and other Latin American nations, are driving the adoption of high-performance and bio-based surfactants. This report is an essential resource for industry professionals seeking to understand market size, growth drivers, competitive landscapes, and emerging opportunities within this dynamic and rapidly evolving industry.

Latin America Surfactant Industry Market Dynamics & Structure

The Latin America Surfactant Industry is characterized by a moderately concentrated market structure, with a few global giants holding substantial shares alongside a growing number of regional players. Market concentration is influenced by the high capital intensity required for R&D and manufacturing, yet technological innovation continues to be a primary driver for market differentiation. Regulatory frameworks across countries like Brazil, Mexico, and Argentina are increasingly focusing on environmental sustainability, driving the demand for biodegradable and bio-based surfactants. For instance, stringent regulations regarding phosphate content in detergents have spurred innovation in alternative surfactant formulations, impacting market share distribution among key players. Competitive product substitutes, particularly in niche applications, exist but generally face challenges in matching the versatility and cost-effectiveness of traditional surfactants. However, the rise of enzyme-based cleaning agents presents a long-term potential substitute, pushing surfactant manufacturers to enhance product performance and environmental profiles.

End-user demographics play a crucial role, with a burgeoning middle class and increasing disposable incomes driving demand for household and personal care products, which are major consumers of surfactants. Urbanization rates, particularly in Brazil and Mexico, are boosting the market for detergents, cleaners, and other consumer chemicals. Furthermore, the growth in the agricultural and oil & gas sectors in countries like Argentina and Colombia fuels the demand for specialty surfactants used as emulsifying agents, wetting agents, and demulsifying agents. Mergers and acquisitions (M&A) trends indicate a strategic consolidation aimed at expanding product portfolios, gaining market access, and acquiring specialized technologies. For example, the historical period (2019-2024) saw approximately xx M&A deals, with a total deal volume of around USD xx million, predominantly focused on integrating sustainable chemical technologies or expanding regional manufacturing footprints. Innovation barriers often include high R&D costs, complex regulatory approval processes for novel chemistries, and the need for significant investment in production scale-up. However, the push for green chemistry and circular economy principles is incentivizing companies to overcome these barriers, leading to a new wave of product development.

Latin America Surfactant Industry Growth Trends & Insights

Leverage comprehensive analysis to understand the Latin America Surfactant Industry's evolution, where robust growth is underpinned by shifting consumer behaviors, rapid technological advancements, and increasing industrial output. The market, estimated at USD 6,500 million in 2025, is poised for substantial expansion, projected to reach USD 10,500 million by 2033, exhibiting a CAGR of 6.2% during the forecast period. This trajectory is influenced by several critical factors, including heightened awareness regarding hygiene, particularly in the post-pandemic era, which has fueled a consistent demand for household and personal care products, the primary end-users of surfactants. Adoption rates for advanced and specialty surfactants are accelerating across industrial applications, driven by the need for enhanced performance and efficiency in processes such as oil & gas extraction, agriculture, and textiles.

Technological disruptions, especially in the realm of biosurfactants and green chemistry, are reshaping the product landscape. Innovations focusing on reduced environmental footprints, biodegradability, and derivation from renewable resources are gaining significant traction. For instance, the market penetration of bio-based surfactants, while still in its nascent stages, is growing steadily, projected to increase from xx% in 2025 to xx% by 2033, driven by regulatory support and consumer preference for eco-friendly products. Companies are investing heavily in R&D to develop novel chemistries that offer superior performance while adhering to sustainability mandates. This includes the development of APE-free polymerizable surfactants and glycolipid biosurfactants, as evidenced by recent industry developments.

Consumer behavior shifts are profoundly impacting product formulation. There's a noticeable trend towards premiumization in personal care and home care segments, where consumers are willing to pay more for products offering enhanced efficacy, safety, and environmental responsibility. This translates into increased demand for high-quality, mild, and dermatologically tested surfactants. Furthermore, the rising adoption of concentrated detergents and cleaning products also influences surfactant demand by requiring more efficient and potent formulations. The expansion of the organized retail sector and the growing reach of e-commerce platforms across Latin America are making a wider range of surfactant-containing products accessible to consumers, further stimulating market growth. Industrial growth in sectors like mining, construction, and food processing across the region also contributes significantly, requiring tailored surfactant solutions for processes like emulsification, dispersion, and wetting. The overall market dynamics suggest a vibrant future, characterized by continuous innovation and adaptation to evolving environmental standards and consumer expectations.

Dominant Regions, Countries, or Segments in Latin America Surfactant Industry

Within the Latin America Surfactant Industry, the Anionic Surfactants segment, by type, currently holds a dominant position, commanding an estimated market share of approximately 45% in 2025, and is projected to maintain its leadership throughout the forecast period. This dominance is primarily driven by their versatility, cost-effectiveness, and widespread application across various end-user industries, particularly in household chemicals and personal care. Anionic surfactants are highly effective foaming, cleaning, and emulsifying agents, making them indispensable in the formulation of detergents, shampoos, and soaps. Their robust performance characteristics and broad compatibility with other ingredients contribute significantly to their enduring market presence.

- Key Drivers for Anionic Surfactant Dominance:

- Cost-Effectiveness: Generally more economical to produce compared to other surfactant types, making them attractive for mass-market consumer products.

- High Performance: Excellent cleaning, foaming, and emulsifying properties are crucial for detergents and personal care products.

- Established Production Infrastructure: A mature supply chain and established manufacturing processes in Latin America ensure consistent availability and competitive pricing.

- Broad Application Spectrum: Essential ingredients in laundry detergents, dishwashing liquids, shampoos, and various industrial cleaners, which are high-volume markets.

- Consumer Familiarity: Products containing anionic surfactants are widely accepted and used by consumers across all socio-economic strata.

Following Anionic Surfactants, the Household Chemicals end-user industry emerges as the leading segment, capturing an estimated xx% of the total market share in 2025. This segment's preeminence is fueled by the region's demographic growth, increasing urbanization, and a growing emphasis on hygiene and cleanliness. Countries like Brazil, Mexico, and Argentina, with their large populations and developing economies, represent substantial markets for laundry detergents, surface cleaners, dishwashing liquids, and personal care products, all heavily reliant on surfactants. The rising disposable incomes and changing lifestyles further boost the demand for premium and specialized household cleaning solutions.

Geographically, Brazil stands out as the largest country market within Latin America, accounting for an estimated xx% of the regional surfactant market in 2025. Brazil's extensive consumer base, significant industrial output, and robust agricultural sector drive its demand for surfactants across all applications. The country's strong domestic manufacturing capabilities and its role as a regional economic powerhouse contribute to its market leadership. Mexico and Argentina also represent significant markets, driven by their respective industrial growth and consumer spending. The growth potential for these dominant segments and regions remains high, especially with the continuous innovation in sustainable and high-performance surfactant formulations catering to evolving market needs and environmental regulations. The continuous investment in research and development for new applications and more eco-friendly products within these segments will further cement their leading positions in the Latin American Surfactant Industry.

Latin America Surfactant Industry Product Landscape

The Latin America Surfactant Industry is undergoing a significant transformation, driven by innovations focused on sustainability and enhanced performance. The product landscape is increasingly characterized by the introduction of bio-based surfactants, designed to meet stringent environmental standards and cater to growing consumer demand for eco-friendly products. Notable advancements include the development of APE-free polymerizable surfactants like Solvay's Reactsurf 2490, which offers superior functional and aesthetic benefits in coatings and adhesives, even under high temperatures. Furthermore, the introduction of glycolipid biosurfactants such as Solvay's Mirasoft SL L60 and Mirasoft SL A60 exemplifies a shift towards minimal environmental and carbon footprints, expanding applications in sustainable beauty care products like shampoos and face washes. Clariant's Vita line of 100% bio-based surfactants and polyethylene glycols (PEGs) further underscores this commitment to removing fossil carbon from the value chain, offering unique selling propositions centered on sustainability and biodegradability, alongside maintaining high performance across various applications. These innovations are not just incremental improvements but represent a strategic pivot towards a greener chemical industry.

Key Drivers, Barriers & Challenges in Latin America Surfactant Industry

The Latin America Surfactant Industry is primarily propelled by several powerful forces. Technological advancements in sustainable chemistry, particularly the development of bio-based and biodegradable surfactants, are major drivers, responding to escalating environmental concerns and regulatory pressures. The robust growth of the household and personal care industries, fueled by urbanization and increasing disposable incomes, consistently boosts demand for detergents, shampoos, and cleaning agents. Furthermore, the expansion of key end-user sectors like agriculture and oil & gas necessitates specialized surfactant formulations for enhanced efficiency and processing. Economic growth in major Latin American economies like Brazil and Mexico, coupled with government initiatives promoting local manufacturing and sustainable practices, further accelerates market expansion by increasing industrial output and consumer purchasing power.

Despite significant growth potential, the market faces several challenges. Volatility in raw material prices, particularly for petrochemical-derived feedstocks, poses a continuous supply chain issue, impacting production costs and profit margins. Stringent and diverse regulatory frameworks across different Latin American countries create compliance complexities for manufacturers, potentially slowing down market entry for new products. Intense competitive pressures from both global giants and local players, often leading to price wars, can erode profitability, especially for commodity surfactants. The need for substantial R&D investments to develop novel, high-performance, and sustainable surfactant chemistries represents a significant financial hurdle, while consumer preferences for natural ingredients, though an opportunity, also demand continuous innovation and adaptation from traditional manufacturers.

Emerging Opportunities in Latin America Surfactant Industry

The Latin America Surfactant Industry is ripe with emerging opportunities, particularly in the realm of specialty surfactants and sustainable chemistry. Untapped markets exist in rural areas and rapidly developing smaller economies within Latin America, where demand for basic and advanced cleaning solutions is on the rise. Innovative applications in niche sectors such as enhanced oil recovery (EOR), bio-pesticides, and sophisticated pharmaceutical formulations present significant growth avenues for specialized surfactant types. Moreover, the increasing consumer preference for natural, organic, and hypoallergenic products is driving demand for mild surfactants derived from renewable resources, opening doors for companies investing in research and development of these eco-friendly alternatives. The growing e-commerce penetration and direct-to-consumer sales channels also create new pathways for market reach and brand building, especially for companies offering specialized or sustainable product lines.

Growth Accelerators in the Latin America Surfactant Industry

Catalysts driving long-term growth in the Latin America Surfactant Industry are deeply rooted in technological advancements, strategic market expansion, and evolving consumer and regulatory landscapes. Significant technological breakthroughs in biosurfactant production and the development of high-performance, eco-friendly surfactant chemistries are paramount, enabling formulators to meet both efficacy and sustainability targets. Strategic partnerships between chemical manufacturers and end-user industries (e.g., consumer goods, agriculture) facilitate co-creation of specialized solutions and quicker market penetration. Furthermore, market expansion strategies focusing on underserved regions and capitalizing on the burgeoning middle class in Latin America are critical. The continuous investment in robust R&D infrastructure and the adoption of advanced manufacturing processes will ensure the region remains at the forefront of surfactant innovation, driving sustained growth and competitive advantage.

Key Players Shaping the Latin America Surfactant Industry Market

- 3M

- Arkema

- Ashland

- BASF SE

- Bayer AG

- Clariant

- Croda International Plc

- Deten Química S A

- Dow

- Evonik Industries AG

- Godrej Industries

- Innospec

- Kao Corporation

- Lonza

- Nouryon

- Indorama Ventures Public Company Limited

- P&G Chemicals

- Reliance Industries Ltd

- Solvay

- Stepan Company

- TENSAC

- YPF

- Others

Notable Milestones in Latin America Surfactant Industry Sector

- November 2022: Solvay introduced Reactsurf 2490, a novel APE-free polymerizable surfactant. This innovation significantly enhances emulsion performance in acrylic, vinyl-acrylic, and styrene-acrylic latex systems, offering improved functional and aesthetic benefits for exterior coatings and pressure-sensitive adhesives (PSAs), even at high temperatures. This development marks a move towards high-performance, environmentally conscious formulations in industrial applications.

- June 2022: Solvay launched Mirasoft SL L60 and Mirasoft SL A60, two novel high-performance biosurfactants. These glycolipid biosurfactants, derived from rapeseed oil and sugar, boast minimal environmental and carbon footprints, enabling the production of sustainable beauty care products. Their suitability for a variety of uses in beauty care, including shampoos, conditioners, shower gels, face washes, and creams, significantly impacts the personal care segment by promoting green formulations.

- February 2022: Clariant introduced their new Vita line of 100% bio-based surfactants and polyethylene glycols (PEGs). This initiative directly addresses climate change by actively removing fossil carbon from the value chain. The expansion of Clariant's Vita-designated components with 100% bio-based surfactants and PEGs represents a major step towards fully sustainable chemical solutions, influencing the entire value chain towards bio-economy principles.

In-Depth Latin America Surfactant Industry Market Outlook

The outlook for the Latin America Surfactant Industry is overwhelmingly positive, driven by a confluence of growth accelerators that promise sustained expansion and strategic opportunities. The increasing emphasis on sustainability and bio-based solutions will continue to catalyze market transformation, with innovation in green chemistry leading to new product categories and applications. The expanding consumer base, coupled with rising disposable incomes across key Latin American countries, will ensure robust demand for household and personal care products, which remain the largest end-users. Furthermore, industrial growth in sectors like agriculture, oil & gas, and textiles will drive the need for specialized, high-performance surfactants. Companies that strategically invest in research and development of sustainable and efficient surfactant technologies, forge strong partnerships, and adapt to evolving regulatory landscapes will be best positioned to capitalize on the vast future market potential, securing leadership in this dynamic and essential industry.

Latin America Surfactant Industry Segmentation

-

1. Type

- 1.1. Amphoteric Surfactants

- 1.2. Anionic Surfactants

- 1.3. Cationic Surfactants

- 1.4. Non-ionic Surfactants

-

2. Application

- 2.1. Detergents

- 2.2. Emulsify Agents

- 2.3. Foaming Agents

- 2.4. Dispersing Agents

- 2.5. Wetting Agents

- 2.6. Demulsifying Agents

- 2.7. Antifoaming Agents

- 2.8. Antistatic Agents

- 2.9. Others

-

3. End User Industry

- 3.1. Household Chemicals

- 3.2. Food Industry

- 3.3. Oil & Gas

- 3.4. Agriculture

- 3.5. Textile

- 3.6. Pharmaceutical

- 3.7. Others

-

4. Sales Channel

- 4.1. Direct Sales

- 4.2. Distributors

- 4.3. Online

- 4.4. Others

Latin America Surfactant Industry Segmentation By Geography

- 1. Mexico

- 2. Brazil

- 3. Argentina

- 4. Chile

- 5. Colombia

- 6. Rest of Latin America

Latin America Surfactant Industry Regional Market Share

Geographic Coverage of Latin America Surfactant Industry

Latin America Surfactant Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Amphoteric Surfactants

- 5.1.2. Anionic Surfactants

- 5.1.3. Cationic Surfactants

- 5.1.4. Non-ionic Surfactants

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Detergents

- 5.2.2. Emulsify Agents

- 5.2.3. Foaming Agents

- 5.2.4. Dispersing Agents

- 5.2.5. Wetting Agents

- 5.2.6. Demulsifying Agents

- 5.2.7. Antifoaming Agents

- 5.2.8. Antistatic Agents

- 5.2.9. Others

- 5.3. Market Analysis, Insights and Forecast - by End User Industry

- 5.3.1. Household Chemicals

- 5.3.2. Food Industry

- 5.3.3. Oil & Gas

- 5.3.4. Agriculture

- 5.3.5. Textile

- 5.3.6. Pharmaceutical

- 5.3.7. Others

- 5.4. Market Analysis, Insights and Forecast - by Sales Channel

- 5.4.1. Direct Sales

- 5.4.2. Distributors

- 5.4.3. Online

- 5.4.4. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Mexico

- 5.5.2. Brazil

- 5.5.3. Argentina

- 5.5.4. Chile

- 5.5.5. Colombia

- 5.5.6. Rest of Latin America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Latin America Surfactant Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Amphoteric Surfactants

- 6.1.2. Anionic Surfactants

- 6.1.3. Cationic Surfactants

- 6.1.4. Non-ionic Surfactants

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Detergents

- 6.2.2. Emulsify Agents

- 6.2.3. Foaming Agents

- 6.2.4. Dispersing Agents

- 6.2.5. Wetting Agents

- 6.2.6. Demulsifying Agents

- 6.2.7. Antifoaming Agents

- 6.2.8. Antistatic Agents

- 6.2.9. Others

- 6.3. Market Analysis, Insights and Forecast - by End User Industry

- 6.3.1. Household Chemicals

- 6.3.2. Food Industry

- 6.3.3. Oil & Gas

- 6.3.4. Agriculture

- 6.3.5. Textile

- 6.3.6. Pharmaceutical

- 6.3.7. Others

- 6.4. Market Analysis, Insights and Forecast - by Sales Channel

- 6.4.1. Direct Sales

- 6.4.2. Distributors

- 6.4.3. Online

- 6.4.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Mexico Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Amphoteric Surfactants

- 7.1.2. Anionic Surfactants

- 7.1.3. Cationic Surfactants

- 7.1.4. Non-ionic Surfactants

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Detergents

- 7.2.2. Emulsify Agents

- 7.2.3. Foaming Agents

- 7.2.4. Dispersing Agents

- 7.2.5. Wetting Agents

- 7.2.6. Demulsifying Agents

- 7.2.7. Antifoaming Agents

- 7.2.8. Antistatic Agents

- 7.2.9. Others

- 7.3. Market Analysis, Insights and Forecast - by End User Industry

- 7.3.1. Household Chemicals

- 7.3.2. Food Industry

- 7.3.3. Oil & Gas

- 7.3.4. Agriculture

- 7.3.5. Textile

- 7.3.6. Pharmaceutical

- 7.3.7. Others

- 7.4. Market Analysis, Insights and Forecast - by Sales Channel

- 7.4.1. Direct Sales

- 7.4.2. Distributors

- 7.4.3. Online

- 7.4.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Brazil Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Amphoteric Surfactants

- 8.1.2. Anionic Surfactants

- 8.1.3. Cationic Surfactants

- 8.1.4. Non-ionic Surfactants

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Detergents

- 8.2.2. Emulsify Agents

- 8.2.3. Foaming Agents

- 8.2.4. Dispersing Agents

- 8.2.5. Wetting Agents

- 8.2.6. Demulsifying Agents

- 8.2.7. Antifoaming Agents

- 8.2.8. Antistatic Agents

- 8.2.9. Others

- 8.3. Market Analysis, Insights and Forecast - by End User Industry

- 8.3.1. Household Chemicals

- 8.3.2. Food Industry

- 8.3.3. Oil & Gas

- 8.3.4. Agriculture

- 8.3.5. Textile

- 8.3.6. Pharmaceutical

- 8.3.7. Others

- 8.4. Market Analysis, Insights and Forecast - by Sales Channel

- 8.4.1. Direct Sales

- 8.4.2. Distributors

- 8.4.3. Online

- 8.4.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Argentina Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Amphoteric Surfactants

- 9.1.2. Anionic Surfactants

- 9.1.3. Cationic Surfactants

- 9.1.4. Non-ionic Surfactants

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Detergents

- 9.2.2. Emulsify Agents

- 9.2.3. Foaming Agents

- 9.2.4. Dispersing Agents

- 9.2.5. Wetting Agents

- 9.2.6. Demulsifying Agents

- 9.2.7. Antifoaming Agents

- 9.2.8. Antistatic Agents

- 9.2.9. Others

- 9.3. Market Analysis, Insights and Forecast - by End User Industry

- 9.3.1. Household Chemicals

- 9.3.2. Food Industry

- 9.3.3. Oil & Gas

- 9.3.4. Agriculture

- 9.3.5. Textile

- 9.3.6. Pharmaceutical

- 9.3.7. Others

- 9.4. Market Analysis, Insights and Forecast - by Sales Channel

- 9.4.1. Direct Sales

- 9.4.2. Distributors

- 9.4.3. Online

- 9.4.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Chile Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Amphoteric Surfactants

- 10.1.2. Anionic Surfactants

- 10.1.3. Cationic Surfactants

- 10.1.4. Non-ionic Surfactants

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Detergents

- 10.2.2. Emulsify Agents

- 10.2.3. Foaming Agents

- 10.2.4. Dispersing Agents

- 10.2.5. Wetting Agents

- 10.2.6. Demulsifying Agents

- 10.2.7. Antifoaming Agents

- 10.2.8. Antistatic Agents

- 10.2.9. Others

- 10.3. Market Analysis, Insights and Forecast - by End User Industry

- 10.3.1. Household Chemicals

- 10.3.2. Food Industry

- 10.3.3. Oil & Gas

- 10.3.4. Agriculture

- 10.3.5. Textile

- 10.3.6. Pharmaceutical

- 10.3.7. Others

- 10.4. Market Analysis, Insights and Forecast - by Sales Channel

- 10.4.1. Direct Sales

- 10.4.2. Distributors

- 10.4.3. Online

- 10.4.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Colombia Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Amphoteric Surfactants

- 11.1.2. Anionic Surfactants

- 11.1.3. Cationic Surfactants

- 11.1.4. Non-ionic Surfactants

- 11.2. Market Analysis, Insights and Forecast - by Application

- 11.2.1. Detergents

- 11.2.2. Emulsify Agents

- 11.2.3. Foaming Agents

- 11.2.4. Dispersing Agents

- 11.2.5. Wetting Agents

- 11.2.6. Demulsifying Agents

- 11.2.7. Antifoaming Agents

- 11.2.8. Antistatic Agents

- 11.2.9. Others

- 11.3. Market Analysis, Insights and Forecast - by End User Industry

- 11.3.1. Household Chemicals

- 11.3.2. Food Industry

- 11.3.3. Oil & Gas

- 11.3.4. Agriculture

- 11.3.5. Textile

- 11.3.6. Pharmaceutical

- 11.3.7. Others

- 11.4. Market Analysis, Insights and Forecast - by Sales Channel

- 11.4.1. Direct Sales

- 11.4.2. Distributors

- 11.4.3. Online

- 11.4.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Rest of Latin America Latin America Surfactant Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Type

- 12.1.1. Amphoteric Surfactants

- 12.1.2. Anionic Surfactants

- 12.1.3. Cationic Surfactants

- 12.1.4. Non-ionic Surfactants

- 12.2. Market Analysis, Insights and Forecast - by Application

- 12.2.1. Detergents

- 12.2.2. Emulsify Agents

- 12.2.3. Foaming Agents

- 12.2.4. Dispersing Agents

- 12.2.5. Wetting Agents

- 12.2.6. Demulsifying Agents

- 12.2.7. Antifoaming Agents

- 12.2.8. Antistatic Agents

- 12.2.9. Others

- 12.3. Market Analysis, Insights and Forecast - by End User Industry

- 12.3.1. Household Chemicals

- 12.3.2. Food Industry

- 12.3.3. Oil & Gas

- 12.3.4. Agriculture

- 12.3.5. Textile

- 12.3.6. Pharmaceutical

- 12.3.7. Others

- 12.4. Market Analysis, Insights and Forecast - by Sales Channel

- 12.4.1. Direct Sales

- 12.4.2. Distributors

- 12.4.3. Online

- 12.4.4. Others

- 12.1. Market Analysis, Insights and Forecast - by Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 3M

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Arkema

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Ashland

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 BASF SE

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Bayer AG

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Clariant

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Croda International Plc

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 Deten Química S A

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Dow

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Evonik Industries AG

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Godrej Industries

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Innospec

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.13 Kao Corporation

- 13.1.13.1. Company Overview

- 13.1.13.2. Products

- 13.1.13.3. Company Financials

- 13.1.13.4. SWOT Analysis

- 13.1.14 Lonza

- 13.1.14.1. Company Overview

- 13.1.14.2. Products

- 13.1.14.3. Company Financials

- 13.1.14.4. SWOT Analysis

- 13.1.15 Nouryon

- 13.1.15.1. Company Overview

- 13.1.15.2. Products

- 13.1.15.3. Company Financials

- 13.1.15.4. SWOT Analysis

- 13.1.16 Indorama Ventures Public Company Limited

- 13.1.16.1. Company Overview

- 13.1.16.2. Products

- 13.1.16.3. Company Financials

- 13.1.16.4. SWOT Analysis

- 13.1.17 P&G Chemicals

- 13.1.17.1. Company Overview

- 13.1.17.2. Products

- 13.1.17.3. Company Financials

- 13.1.17.4. SWOT Analysis

- 13.1.18 Reliance Industries Ltd

- 13.1.18.1. Company Overview

- 13.1.18.2. Products

- 13.1.18.3. Company Financials

- 13.1.18.4. SWOT Analysis

- 13.1.19 Solvay

- 13.1.19.1. Company Overview

- 13.1.19.2. Products

- 13.1.19.3. Company Financials

- 13.1.19.4. SWOT Analysis

- 13.1.20 Stepan Company

- 13.1.20.1. Company Overview

- 13.1.20.2. Products

- 13.1.20.3. Company Financials

- 13.1.20.4. SWOT Analysis

- 13.1.21 TENSAC

- 13.1.21.1. Company Overview

- 13.1.21.2. Products

- 13.1.21.3. Company Financials

- 13.1.21.4. SWOT Analysis

- 13.1.22 YPF

- 13.1.22.1. Company Overview

- 13.1.22.2. Products

- 13.1.22.3. Company Financials

- 13.1.22.4. SWOT Analysis

- 13.1.23 Others

- 13.1.23.1. Company Overview

- 13.1.23.2. Products

- 13.1.23.3. Company Financials

- 13.1.23.4. SWOT Analysis

- 13.1.1 3M

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Latin America Surfactant Industry Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: Latin America Surfactant Industry Share (%) by Company 2025

List of Tables

- Table 1: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 2: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 3: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 4: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 5: Latin America Surfactant Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 7: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 9: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 10: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 11: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 13: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 14: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 15: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 16: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 17: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 18: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 19: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 20: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 21: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 22: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 23: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 24: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 25: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 26: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 27: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 28: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 29: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 30: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Latin America Surfactant Industry Revenue undefined Forecast, by Type 2020 & 2033

- Table 32: Latin America Surfactant Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 33: Latin America Surfactant Industry Revenue undefined Forecast, by End User Industry 2020 & 2033

- Table 34: Latin America Surfactant Industry Revenue undefined Forecast, by Sales Channel 2020 & 2033

- Table 35: Latin America Surfactant Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Latin America Surfactant Industry?

The projected CAGR is approximately 5.1%.

2. Which companies are prominent players in the Latin America Surfactant Industry?

Key companies in the market include 3M, Arkema, Ashland, BASF SE, Bayer AG, Clariant, Croda International Plc, Deten Química S A, Dow, Evonik Industries AG, Godrej Industries, Innospec, Kao Corporation, Lonza, Nouryon, Indorama Ventures Public Company Limited, P&G Chemicals, Reliance Industries Ltd, Solvay, Stepan Company, TENSAC, YPF, Others.

3. What are the main segments of the Latin America Surfactant Industry?

The market segments include Type, Application, End User Industry, Sales Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Growing Personal Care and Home Care Industry in Latin America; The Growth of the Oleo Chemicals Market Driving Bio-based Surfactants.

6. What are the notable trends driving market growth?

Growing Demand from Household Soap and Detergent Application.

7. Are there any restraints impacting market growth?

Increasing Focus on Environmental Regulations; Other Restraints.

8. Can you provide examples of recent developments in the market?

November 2022: Solvay introduced Reactsurf 2490, a novel APE-free1 polymerizable surfactant developed as a major emulsifier for acrylic, vinyl-acrylic, and styrene-acrylic latex systems. In comparison to traditional surfactants, Reactsurf 2490 enhances emulsion performance to give improved functional and aesthetic benefits in exterior coatings and pressure-sensitive adhesives (PSAs), even at high temperatures.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Latin America Surfactant Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Latin America Surfactant Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Latin America Surfactant Industry?

To stay informed about further developments, trends, and reports in the Latin America Surfactant Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence