Key Insights

The Middle East and Africa (MEA) leather goods market, valued at approximately $XX million in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 7.06% from 2025 to 2033. This expansion is fueled by several key drivers. Rising disposable incomes across the region, particularly in the UAE, Saudi Arabia, and Turkey, are empowering a burgeoning middle class with increased purchasing power for luxury and premium leather goods. Furthermore, a growing trend towards personalized fashion and the increasing adoption of online retail channels are significantly contributing to market expansion. The preference for high-quality, durable leather products, coupled with the influence of global fashion trends and the increasing popularity of designer brands, further bolsters market growth. However, economic fluctuations in certain MEA countries and the potential impact of counterfeit products pose challenges to sustained growth.

Segmentation within the MEA leather goods market reveals a diverse landscape. Footwear constitutes a significant portion, driven by both athletic and formal wear demand. Luggage, catering to both business and leisure travel, is another sizable segment, with growing demand for stylish and functional travel accessories. Accessories, encompassing handbags, wallets, belts, and other leather items, contribute substantially to overall market value. The distribution channel is split between offline retail stores, which maintain a considerable share due to the importance of physical product examination and brand experience, and online retail stores, which are steadily gaining traction as e-commerce penetration increases across the region. Key players like Adidas AG, LVMH, Prada, Michael Kors, Hermes, Capri Holdings, Kering, Louis Vuitton, and Ralph Lauren Corporation, among others, fiercely compete for market share, contributing to innovation and product diversification.

This comprehensive report provides an in-depth analysis of the Middle East and Africa (MEA) leather goods industry, offering invaluable insights for businesses, investors, and industry professionals. The report covers the period from 2019 to 2033, with 2025 serving as the base year and 2025 as the estimated year. The forecast period spans from 2025 to 2033, while the historical period encompasses 2019-2024. The MEA leather goods market, segmented by type (Footwear, Luggage, Accessories) and distribution channel (Offline Retail Stores, Online Retail Stores), is expected to reach xx Million units by 2033. Key players analyzed include Adidas AG, LVMH, Prada S p A, Michael Kors Holdings Ltd, Hermes International S A, Capri Holdings Ltd, Kering S A, Louis Vuitton, and Ralph Lauren Corporation (list not exhaustive).

MEA Leather Goods Industry Market Dynamics & Structure

The Middle East and Africa (MEA) leather goods market presents a dynamic landscape characterized by a moderately concentrated structure. A few large multinational corporations coexist with a multitude of smaller, regional businesses, creating a diverse competitive environment. Technological innovation acts as a key driver, with advancements in sustainable leather alternatives, 3D printing techniques, and smart features significantly impacting product development and manufacturing processes. The regulatory environment plays a crucial role, with increasing emphasis on ethical sourcing, environmental standards, and fair labor practices shaping market dynamics. The sector faces ongoing competition from synthetic materials and other substitutes, necessitating continuous product differentiation and innovation to maintain market share. Furthermore, evolving end-user demographics, notably a burgeoning young and affluent population with a growing disposable income, are significantly driving demand for premium and fashion-forward leather goods. Mergers and acquisitions (M&A) activity has been moderate over the past five years, with [Insert Precise Number] deals recorded, valued at approximately [Insert Precise Value in Currency].

- Market Concentration: Moderately concentrated, with the top 5 players holding approximately [Insert Precise Percentage]% market share (2024).

- Technological Innovation: Focus on sustainable and ethically sourced materials, smart features (e.g., RFID tracking), and improved manufacturing efficiency through automation and advanced technologies.

- Regulatory Landscape: Stringent regulations promoting ethical sourcing, environmental sustainability (e.g., reduced carbon footprint), and fair labor practices are increasingly influencing market operations.

- Competitive Substitutes: Synthetic materials and plant-based alternatives pose a significant competitive challenge, requiring the leather industry to constantly innovate and highlight the unique qualities of genuine leather.

- End-User Demographics: A growing middle class and young, affluent population, particularly in urban centers, fuel demand for luxury, high-quality, and fashion-forward leather goods.

- M&A Activity: [Insert Precise Number] deals completed between 2019 and 2024, totaling approximately [Insert Precise Value in Currency] in value.

MEA Leather Goods Industry Growth Trends & Insights

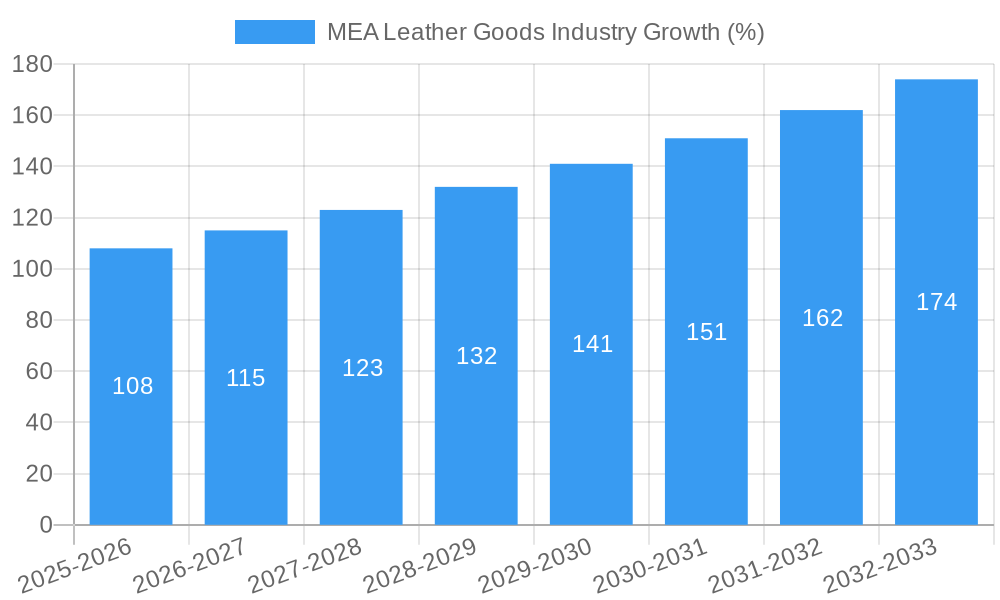

The MEA leather goods market experienced robust growth during the historical period (2019-2024), with a CAGR of xx%. This growth is primarily attributable to rising disposable incomes, increasing urbanization, and a shift towards aspirational consumerism. The adoption rate of online retail channels has been steadily increasing, contributing to the expansion of the market. Technological disruptions, including e-commerce platforms and personalized marketing strategies, significantly influence consumer behavior. Changes in consumer preferences towards sustainable and ethically sourced products present both opportunities and challenges. The forecast period (2025-2033) is projected to show a CAGR of xx%, driven by continued economic growth and evolving consumer demand. Market penetration in key segments is expected to increase, particularly within the online retail space.

Dominant Regions, Countries, or Segments in MEA Leather Goods Industry

The United Arab Emirates (UAE) and Saudi Arabia currently hold leading positions within the MEA leather goods market, fueled by robust economic growth, high levels of consumer spending, and well-established retail infrastructure. Within the product segments, footwear commands the largest market share, followed by accessories (handbags, wallets, belts) and luggage. While offline retail stores still constitute a major sales channel, online platforms are experiencing rapid expansion and increased market penetration, driven by the growing adoption of e-commerce among consumers.

- Key Drivers:

- Strong Economic Growth: High GDP growth in key markets directly translates into increased consumer spending and disposable income.

- Robust Retail Infrastructure: Well-developed retail networks, both physical and online, ensure efficient product distribution and accessibility for consumers.

- Favorable Demographics: A young and expanding population with rising disposable income levels creates a strong consumer base for leather goods.

- Dominant Segments:

- Footwear: The largest segment, driven by high demand for both casual and formal footwear across various styles and price points.

- Accessories: Handbags, wallets, and belts represent a significant and growing segment, particularly within the luxury and fashion markets.

- Online Retail: While offline channels remain significant, online sales are rapidly expanding, offering increased convenience and reach to a broader consumer base.

MEA Leather Goods Industry Product Landscape

The MEA leather goods market showcases a diverse and evolving product range, with ongoing innovation focused on enhancing functionality, durability, aesthetics, and sustainability. Products are carefully tailored to meet diverse lifestyles and preferences, spanning from high-end luxury handbags and travel luggage to athletic footwear and everyday accessories. Key unique selling propositions (USPs) include the use of superior quality leather, ethically sourced materials, sustainable manufacturing practices, and cutting-edge designs. The integration of technological advancements, such as smart features (e.g., GPS tracking in luggage, RFID technology in wallets), is gaining significant traction, adding value and convenience for consumers.

Key Drivers, Barriers & Challenges in MEA Leather Goods Industry

Key Drivers: Rising disposable incomes, rapid urbanization leading to increased consumer spending, growing demand for luxury and branded goods, and the continuous expansion of e-commerce platforms are all key catalysts for market growth. Government support initiatives aimed at boosting the leather industry and favorable demographic trends further contribute to positive market momentum.

Key Challenges: Volatility in raw material prices, particularly hides and skins, poses a significant challenge. Intense competition from synthetic alternatives requires continuous differentiation and innovation. Addressing concerns surrounding ethical sourcing, sustainability, and environmental impact is crucial for long-term market success. Supply chain disruptions, as experienced during the pandemic, continue to impact production and distribution efficiency, highlighting the need for resilient and diversified supply chains. Regulatory hurdles related to environmental compliance and labor standards can also affect profitability and market access.

Emerging Opportunities in MEA Leather Goods Industry

Untapped markets in smaller MEA countries present significant growth potential. The increasing demand for personalized and customized products creates opportunities for niche players. Evolving consumer preferences toward sustainable and ethically sourced leather goods open doors for companies adopting eco-friendly practices.

Growth Accelerators in the MEA Leather Goods Industry

Technological breakthroughs in materials science, sustainable leather alternatives, and advanced manufacturing processes (e.g., automation, 3D printing) are poised to further accelerate market expansion. Strategic partnerships between international brands and local manufacturers can facilitate smoother market penetration, create innovative distribution channels, and leverage local expertise. Expansion into emerging markets within the MEA region, focusing on untapped consumer segments, presents significant opportunities for substantial growth and market diversification. Furthermore, a strong emphasis on sustainability and ethical practices will be crucial for attracting environmentally conscious consumers and building a positive brand reputation.

Key Players Shaping the MEA Leather Goods Industry Market

- Adidas AG

- LVMH

- Prada S p A

- Michael Kors Holdings Ltd

- Hermes International S A

- Capri Holdings Ltd

- Kering S A

- Louis Vuitton

- Ralph Lauren Corporation

Notable Milestones in MEA Leather Goods Industry Sector

- 2020: Increased adoption of online retail channels due to the pandemic.

- 2021: Launch of several sustainable leather collections by major brands.

- 2022: Several key M&A deals involving regional players.

- 2023: Government initiatives to promote the local leather industry in some MEA countries.

In-Depth MEA Leather Goods Industry Market Outlook

The MEA leather goods market is poised for continued growth, driven by favorable demographic trends, rising disposable incomes, and increased adoption of online retail channels. Strategic partnerships, investments in technological innovation, and a focus on sustainability will be crucial for long-term success. The market is expected to witness robust growth in the coming decade, presenting lucrative opportunities for both established players and new entrants.

MEA Leather Goods Industry Segmentation

-

1. Type

- 1.1. Footwear

- 1.2. Luggage

- 1.3. Accessories

-

2. Distribution Channel

- 2.1. Offline Retail Stores

- 2.2. Online Retail Stores

-

3. Geography

-

3.1. Middle East & Africa

- 3.1.1. United Arab Emirates

- 3.1.2. Saudi Arabia

- 3.1.3. Egypt

- 3.1.4. Turkey

- 3.1.5. South Africa

- 3.1.6. Rest of Middle East & Africa

-

3.1. Middle East & Africa

MEA Leather Goods Industry Segmentation By Geography

- 1. Middle East

-

2. United Arab Emirates

- 2.1. Saudi Arabia

- 2.2. Egypt

- 2.3. Turkey

- 2.4. South Africa

- 2.5. Rest of Middle East

MEA Leather Goods Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.06% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increase in Sports Participation; Trend of Athleisure

- 3.3. Market Restrains

- 3.3.1. Availability of Fake and Counterfeit Products

- 3.4. Market Trends

- 3.4.1. Specialized Leather Processing Hub leading to an Increase in Production and Exports

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. MEA Leather Goods Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Footwear

- 5.1.2. Luggage

- 5.1.3. Accessories

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Offline Retail Stores

- 5.2.2. Online Retail Stores

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Middle East & Africa

- 5.3.1.1. United Arab Emirates

- 5.3.1.2. Saudi Arabia

- 5.3.1.3. Egypt

- 5.3.1.4. Turkey

- 5.3.1.5. South Africa

- 5.3.1.6. Rest of Middle East & Africa

- 5.3.1. Middle East & Africa

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Middle East

- 5.4.2. United Arab Emirates

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Middle East MEA Leather Goods Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Footwear

- 6.1.2. Luggage

- 6.1.3. Accessories

- 6.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.2.1. Offline Retail Stores

- 6.2.2. Online Retail Stores

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Middle East & Africa

- 6.3.1.1. United Arab Emirates

- 6.3.1.2. Saudi Arabia

- 6.3.1.3. Egypt

- 6.3.1.4. Turkey

- 6.3.1.5. South Africa

- 6.3.1.6. Rest of Middle East & Africa

- 6.3.1. Middle East & Africa

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. United Arab Emirates MEA Leather Goods Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Footwear

- 7.1.2. Luggage

- 7.1.3. Accessories

- 7.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.2.1. Offline Retail Stores

- 7.2.2. Online Retail Stores

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Middle East & Africa

- 7.3.1.1. United Arab Emirates

- 7.3.1.2. Saudi Arabia

- 7.3.1.3. Egypt

- 7.3.1.4. Turkey

- 7.3.1.5. South Africa

- 7.3.1.6. Rest of Middle East & Africa

- 7.3.1. Middle East & Africa

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Middle East MEA Leather Goods Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 8.1.1.

- 9. United Arab Emirates MEA Leather Goods Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 9.1.1 Saudi Arabia

- 9.1.2 Egypt

- 9.1.3 Turkey

- 9.1.4 South Africa

- 9.1.5 Rest of Middle East

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Adidas AG

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 LVMH

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Prada S p A

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Michael Kors Holdings Ltd

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Hermes International S A

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Capri Holdings Ltd

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Kering S A *List Not Exhaustive

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Louis Vuitton

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Ralph Lauren Corporation

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.1 Adidas AG

List of Figures

- Figure 1: MEA Leather Goods Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: MEA Leather Goods Industry Share (%) by Company 2024

List of Tables

- Table 1: MEA Leather Goods Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: MEA Leather Goods Industry Volume K Units Forecast, by Region 2019 & 2032

- Table 3: MEA Leather Goods Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 4: MEA Leather Goods Industry Volume K Units Forecast, by Type 2019 & 2032

- Table 5: MEA Leather Goods Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 6: MEA Leather Goods Industry Volume K Units Forecast, by Distribution Channel 2019 & 2032

- Table 7: MEA Leather Goods Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 8: MEA Leather Goods Industry Volume K Units Forecast, by Geography 2019 & 2032

- Table 9: MEA Leather Goods Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: MEA Leather Goods Industry Volume K Units Forecast, by Region 2019 & 2032

- Table 11: MEA Leather Goods Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: MEA Leather Goods Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 13: MEA Leather Goods Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: MEA Leather Goods Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 15: MEA Leather Goods Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: MEA Leather Goods Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 17: Saudi Arabia MEA Leather Goods Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Saudi Arabia MEA Leather Goods Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 19: Egypt MEA Leather Goods Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Egypt MEA Leather Goods Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 21: Turkey MEA Leather Goods Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Turkey MEA Leather Goods Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 23: South Africa MEA Leather Goods Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: South Africa MEA Leather Goods Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 25: Rest of Middle East MEA Leather Goods Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Rest of Middle East MEA Leather Goods Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 27: MEA Leather Goods Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 28: MEA Leather Goods Industry Volume K Units Forecast, by Type 2019 & 2032

- Table 29: MEA Leather Goods Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 30: MEA Leather Goods Industry Volume K Units Forecast, by Distribution Channel 2019 & 2032

- Table 31: MEA Leather Goods Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 32: MEA Leather Goods Industry Volume K Units Forecast, by Geography 2019 & 2032

- Table 33: MEA Leather Goods Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: MEA Leather Goods Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 35: MEA Leather Goods Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 36: MEA Leather Goods Industry Volume K Units Forecast, by Type 2019 & 2032

- Table 37: MEA Leather Goods Industry Revenue Million Forecast, by Distribution Channel 2019 & 2032

- Table 38: MEA Leather Goods Industry Volume K Units Forecast, by Distribution Channel 2019 & 2032

- Table 39: MEA Leather Goods Industry Revenue Million Forecast, by Geography 2019 & 2032

- Table 40: MEA Leather Goods Industry Volume K Units Forecast, by Geography 2019 & 2032

- Table 41: MEA Leather Goods Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 42: MEA Leather Goods Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 43: Saudi Arabia MEA Leather Goods Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Saudi Arabia MEA Leather Goods Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 45: Egypt MEA Leather Goods Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Egypt MEA Leather Goods Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 47: Turkey MEA Leather Goods Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Turkey MEA Leather Goods Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 49: South Africa MEA Leather Goods Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: South Africa MEA Leather Goods Industry Volume (K Units) Forecast, by Application 2019 & 2032

- Table 51: Rest of Middle East MEA Leather Goods Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 52: Rest of Middle East MEA Leather Goods Industry Volume (K Units) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the MEA Leather Goods Industry?

The projected CAGR is approximately 7.06%.

2. Which companies are prominent players in the MEA Leather Goods Industry?

Key companies in the market include Adidas AG, LVMH, Prada S p A, Michael Kors Holdings Ltd, Hermes International S A, Capri Holdings Ltd, Kering S A *List Not Exhaustive, Louis Vuitton, Ralph Lauren Corporation.

3. What are the main segments of the MEA Leather Goods Industry?

The market segments include Type, Distribution Channel, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Sports Participation; Trend of Athleisure.

6. What are the notable trends driving market growth?

Specialized Leather Processing Hub leading to an Increase in Production and Exports.

7. Are there any restraints impacting market growth?

Availability of Fake and Counterfeit Products.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "MEA Leather Goods Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the MEA Leather Goods Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the MEA Leather Goods Industry?

To stay informed about further developments, trends, and reports in the MEA Leather Goods Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence