Key Insights

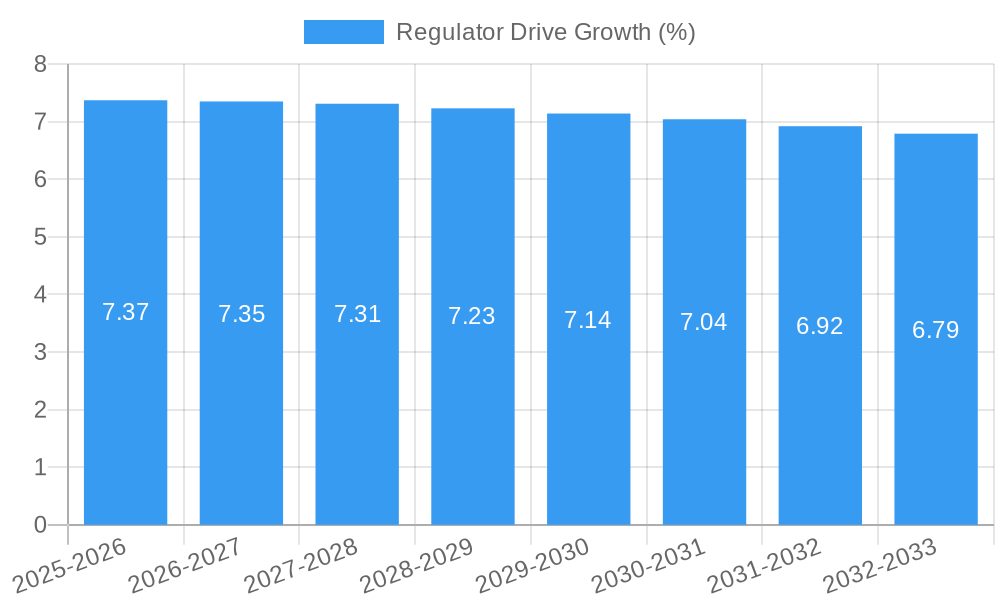

The global Regulator Drive market is poised for significant expansion, driven by the increasing demand for efficient power management solutions across a wide spectrum of electronic applications. With a projected market size of approximately $9.5 billion in 2025 and an anticipated Compound Annual Growth Rate (CAGR) of around 7.2%, the market is expected to reach an estimated $15.5 billion by 2033. This robust growth is underpinned by escalating adoption in key sectors such as vehicle electronics and communication devices, fueled by advancements in automotive electrification and the proliferation of high-performance mobile technology. The continuous evolution of consumer electronics, coupled with the growing need for precise voltage regulation in industrial automation and IoT devices, further accentuates the market's upward trajectory. Innovations in integrated circuit regulator drivers are particularly influential, offering enhanced efficiency and miniaturization, thereby appealing to manufacturers seeking to optimize power consumption and reduce the physical footprint of their products.

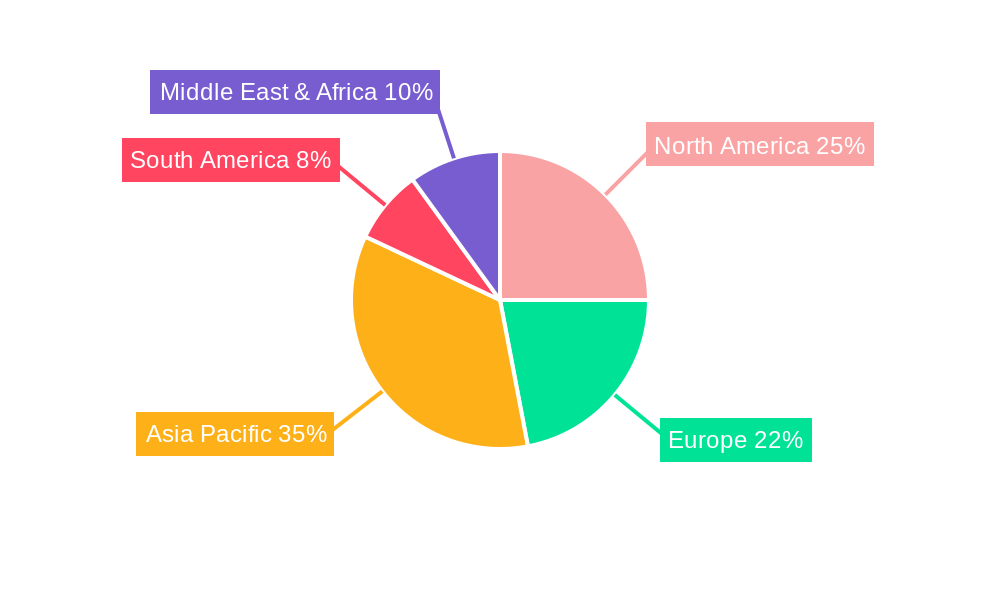

Key restraints, such as stringent regulatory compliance and the high initial cost of advanced regulator drive technologies, may present some headwinds. However, the market is expected to overcome these challenges through ongoing research and development, leading to more cost-effective solutions and broader accessibility. The competitive landscape features prominent players like Texas Instruments, ON Semiconductor, and Infineon Technologies, who are actively investing in product innovation and strategic partnerships to capture market share. Emerging trends indicate a growing preference for low-power and high-efficiency regulator drivers, alongside increasing demand for customized solutions tailored to specific application requirements. Geographically, Asia Pacific is anticipated to lead market growth due to its strong manufacturing base and rapid adoption of new technologies, particularly in China and India, while North America and Europe will remain significant markets driven by technological advancements and stringent energy efficiency standards in their respective automotive and electronics industries.

Regulator Drive Market Dynamics & Structure

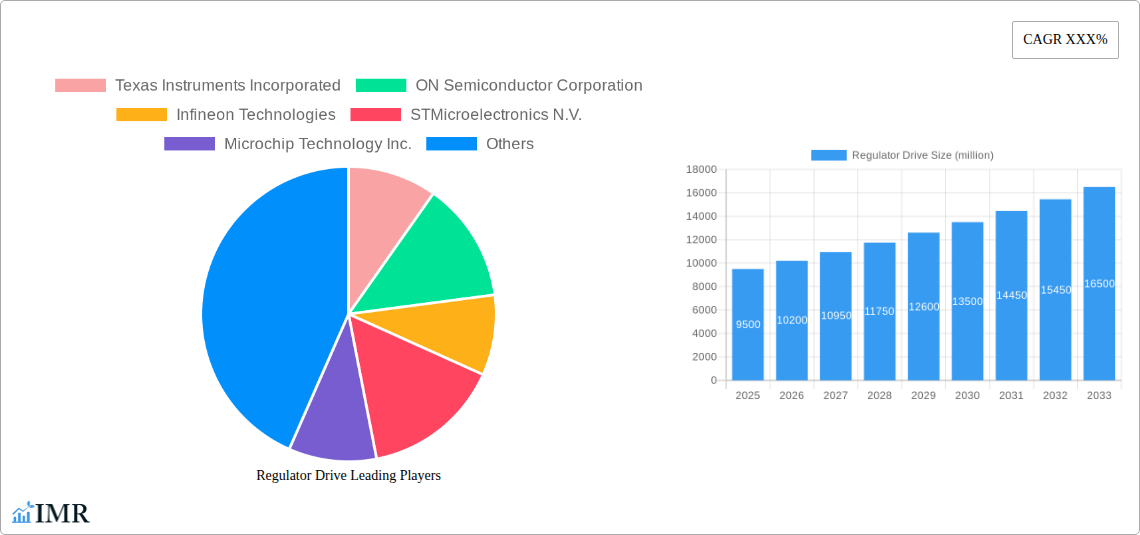

The global regulator drive market exhibits a moderate to high concentration, driven by a handful of dominant players like Texas Instruments Incorporated, ON Semiconductor Corporation, Infineon Technologies, STMicroelectronics N.V., and Microchip Technology Inc. These entities command significant market share, primarily due to their extensive product portfolios, strong R&D capabilities, and established global distribution networks. Technological innovation is a primary driver, with continuous advancements in power efficiency, miniaturization, and integration of advanced control features propelling market growth. Key innovations include the development of highly efficient and compact regulator drivers, smart power management ICs, and adaptive voltage control systems, crucial for applications in electric vehicles and advanced communication devices.

Regulatory frameworks, particularly those concerning energy efficiency and automotive safety standards, are also shaping market dynamics. Compliance with these regulations necessitates the adoption of advanced regulator drive solutions, creating opportunities for manufacturers offering energy-saving and high-performance products. Competitive product substitutes, such as discrete solutions and less efficient power management ICs, pose a challenge, but the superior performance and integration of specialized regulator drives increasingly make them the preferred choice. End-user demographics are shifting towards industries demanding higher power density and better thermal management, including the burgeoning electric vehicle sector and the ever-expanding Internet of Things (IoT) ecosystem. Mergers and acquisitions (M&A) activity, while not excessively high, is strategically focused on acquiring complementary technologies and expanding market reach. For instance, a recent acquisition might target a company specializing in wide-bandgap semiconductor technology for high-voltage applications.

- Market Share Concentration: Top 5 players estimated to hold over 60% of the global market.

- Technological Innovation Drivers: Focus on GaN and SiC based solutions for increased efficiency.

- Regulatory Influence: Stringent energy efficiency standards for consumer electronics and automotive applications.

- Competitive Landscape: Increasing demand for integrated solutions over discrete components.

- End-User Demand: Growth fueled by automotive electronics (especially EVs) and advanced communication devices.

- M&A Trends: Strategic acquisitions targeting niche technologies and regional market access.

Regulator Drive Growth Trends & Insights

The regulator drive market is poised for significant expansion over the forecast period of 2025-2033, driven by a confluence of technological advancements, evolving consumer preferences, and escalating demand across critical industries. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 7.5% to 8.5% during this period. This robust growth trajectory is underpinned by the increasing sophistication of electronic systems that demand precise and efficient voltage regulation. For instance, the automotive sector, particularly the electric vehicle (EV) segment, is a major catalyst. EVs require complex power management systems to efficiently regulate voltage for battery management, motor control, and various onboard electronics, directly boosting the demand for advanced regulator drives. The projected market size for 2025 is estimated to be around 18,500 million units, with an expected surge to over 35,000 million units by 2033.

Technological disruptions are playing a pivotal role in shaping market adoption rates. The transition from traditional silicon-based power devices to wide-bandgap semiconductors like Gallium Nitride (GaN) and Silicon Carbide (SiC) is a prime example. These materials offer superior efficiency, higher switching frequencies, and better thermal performance, enabling the development of smaller, lighter, and more powerful regulator drive solutions. This technological leap is crucial for meeting the stringent requirements of high-performance computing, advanced telecommunications, and next-generation power supplies. Consumer behavior shifts are also influencing the market. There's a growing demand for portable, energy-efficient, and feature-rich electronic devices, from smartphones and wearables to sophisticated industrial automation equipment. This trend necessitates compact, low-power consumption regulator drives that can deliver optimal performance without compromising battery life. Furthermore, the proliferation of the Internet of Things (IoT) and the increasing adoption of smart grids are creating new avenues for regulator drive applications, as each connected device requires reliable power management.

The integration of artificial intelligence (AI) and machine learning (ML) in power management systems, allowing for adaptive voltage regulation and predictive maintenance, represents another significant growth driver. This intelligent approach to power management not only enhances efficiency but also improves system reliability, making regulator drives with these capabilities highly sought after. The increasing complexity and miniaturization of electronic components across all segments, from communication devices to vehicle electronics, inherently drives the need for integrated circuit (IC) regulator drivers that can manage power effectively within confined spaces. The adoption rate of these specialized drivers is expected to accelerate as manufacturers strive to reduce component count and enhance overall system performance.

Dominant Regions, Countries, or Segments in Regulator Drive

The global regulator drive market demonstrates a clear dominance by Vehicle Electronics within the Application segment, driven by the exponential growth of the electric vehicle (EV) and advanced driver-assistance systems (ADAS) markets. The increasing sophistication of automotive electronics, coupled with stringent regulatory mandates for fuel efficiency and emissions reduction, has made robust and efficient power management systems a critical component in modern vehicles. By 2025, Vehicle Electronics is projected to account for an estimated 35% of the total regulator drive market share, translating to approximately 6,475 million units. The parent market for regulator drives is the broader power management IC market, which itself is experiencing substantial growth due to the pervasive nature of electronics in nearly every industry.

The Asia Pacific region stands out as the dominant geographical region, primarily due to its strong manufacturing base, significant automotive production, and rapid adoption of new technologies. Countries like China, Japan, and South Korea are at the forefront of EV production and consumer electronics manufacturing, creating a massive demand for regulator drives. China, in particular, is a powerhouse in both automotive and consumer electronics, with supportive government policies and a large domestic market, contributing significantly to the region's dominance. The estimated market share for Asia Pacific in 2025 is around 42%, representing approximately 7,770 million units.

Within the Type segment, the Integrated Circuit Regulator Driver category is expected to exhibit the strongest growth and command the largest market share. This is attributed to the trend towards higher integration, miniaturization, and the need for efficient power management in increasingly complex electronic devices. Integrated Circuit Regulator Drivers offer benefits such as reduced component count, lower power consumption, and improved performance compared to discrete solutions. By 2025, this segment is anticipated to capture approximately 55% of the market, equating to roughly 10,175 million units.

Key drivers fueling the dominance of Vehicle Electronics include:

- Electric Vehicle Penetration: The global surge in EV adoption necessitates advanced power management for batteries, drivetrains, and auxiliary systems.

- ADAS and Autonomous Driving: Sophisticated sensors, processors, and communication modules in ADAS require precise and reliable voltage regulation.

- Automotive Safety Standards: Increasingly stringent safety regulations mandate the use of highly reliable electronic components.

- Connectivity and Infotainment: The integration of advanced infotainment systems and vehicle-to-everything (V2X) communication increases the demand for efficient power solutions.

The dominance of Asia Pacific is bolstered by:

- Manufacturing Hub: Extensive manufacturing capabilities for automotive, consumer electronics, and communication devices.

- Government Initiatives: Favorable policies promoting electric vehicles and technological innovation.

- Strong Consumer Demand: Large and growing consumer base for advanced electronics and vehicles.

The ascendancy of Integrated Circuit Regulator Drivers is driven by:

- Miniaturization Trends: Need for smaller and more integrated power management solutions.

- Efficiency Demands: Growing emphasis on reducing power consumption in electronic devices.

- Performance Superiority: Higher integration leads to improved performance and reliability.

- Cost-Effectiveness: Reduced component count and assembly costs in the long run.

Regulator Drive Product Landscape

The regulator drive market is characterized by continuous product innovation, with manufacturers like Texas Instruments Incorporated, ON Semiconductor Corporation, and Infineon Technologies leading the charge. Key product advancements focus on enhancing power conversion efficiency, reducing footprint, and integrating smart control features. Innovations include the development of high-frequency switching regulator drivers capable of operating with GaN and SiC power devices, enabling smaller and more efficient power supplies. Applications span across demanding sectors such as electric vehicles (EVs), where regulator drives are critical for battery management systems and motor control; advanced communication devices, leveraging their efficiency for 5G infrastructure and mobile devices; and industrial automation, requiring precise power delivery for motor control and sensor systems. Performance metrics like ultra-low quiescent current, high switching frequencies (often exceeding 1 MHz), and improved thermal management are becoming standard benchmarks. Unique selling propositions include highly integrated solutions that combine multiple functions, such as gate drivers with built-in protection mechanisms and advanced communication interfaces for digital control.

Key Drivers, Barriers & Challenges in Regulator Drive

The regulator drive market is propelled by several key drivers. Technological advancements in wide-bandgap semiconductors (GaN and SiC) are enabling higher efficiency and smaller form factors. The growing adoption of electric vehicles (EVs) is a significant growth accelerator, demanding sophisticated power management solutions for batteries and powertrains. Furthermore, the proliferation of 5G networks and advanced communication devices requires efficient power solutions for increased data processing and connectivity. Supportive government policies promoting energy efficiency and electric mobility also act as crucial catalysts.

However, the market faces several barriers and challenges. Supply chain disruptions, particularly for critical raw materials and semiconductor components, can impact production and lead times. High R&D costs associated with developing next-generation technologies can be a significant hurdle for smaller players. Intense competition from established players and the constant need for price optimization exert downward pressure on margins. Stringent regulatory compliances in various regions, while also a driver, can pose challenges in terms of development and certification costs. For example, ensuring compliance with automotive-grade reliability standards for all new product lines requires substantial investment.

Emerging Opportunities in Regulator Drive

Emerging opportunities in the regulator drive industry are primarily centered around the increasing demand for ultra-high efficiency power solutions for data centers, renewable energy systems, and advanced computing. The ongoing expansion of the Internet of Things (IoT) ecosystem, with billions of connected devices requiring efficient and miniaturized power management, presents a vast untapped market. Innovations in wireless power transfer and the integration of AI-driven predictive power management within regulator drives offer new avenues for differentiation and market penetration. Furthermore, the growing trend towards smart grid technologies and energy harvesting solutions will create significant demand for highly specialized and efficient regulator drives.

Growth Accelerators in the Regulator Drive Industry

Several catalysts are driving long-term growth in the regulator drive industry. Continued advancements in semiconductor technology, particularly in materials like GaN and SiC, are enabling unprecedented levels of efficiency and power density, making regulator drives indispensable for next-generation electronics. Strategic partnerships and collaborations between semiconductor manufacturers, automotive OEMs, and consumer electronics giants are fostering innovation and accelerating product development cycles. Market expansion strategies focusing on emerging economies and the increasing demand for electrification in transportation and industrial sectors are opening up new growth frontiers. The ongoing transition to higher voltage systems in EVs and industrial equipment will also necessitate the development and adoption of advanced regulator drive solutions.

Key Players Shaping the Regulator Drive Market

- Texas Instruments Incorporated

- ON Semiconductor Corporation

- Infineon Technologies

- STMicroelectronics N.V.

- Microchip Technology Inc.

- Analog Devices, Inc.

- NXP Semiconductors N.V.

- Maxim Integrated

- Rohm Semiconductor

- Toshiba Electronic Devices & Storage Corporation

- Diodes Incorporated

- Monolithic Power Systems, Inc.

- Richtek Technology Corporation

- Semtech Corporation

- Zhejiang Zhengxi Electric Group Co., Ltd.

- Qingdao Kekai Electronics Research Institute Co., Ltd.

Notable Milestones in Regulator Drive Sector

- 2019: Launch of highly integrated GaN-based driver ICs enabling higher switching frequencies for power supplies.

- 2020: Significant increase in demand for power management solutions driven by the automotive industry's shift towards electrification.

- 2021: Major acquisition of a key power management IC company by a leading semiconductor manufacturer to strengthen its automotive portfolio.

- 2022: Introduction of SiC-based regulator drivers for high-voltage applications, improving efficiency in EVs and industrial systems.

- 2023: Announcement of new product lines focused on ultra-low power consumption for IoT devices.

- 2024 (Early): Increased investment in R&D for AI-enhanced power management solutions.

In-Depth Regulator Drive Market Outlook

The future outlook for the regulator drive market is exceptionally positive, driven by sustained innovation and increasing adoption across critical growth sectors. The ongoing electrification of vehicles, the expansion of 5G infrastructure, and the pervasive growth of the IoT will continue to fuel demand for advanced, efficient, and compact power management solutions. Strategic opportunities lie in the development of highly integrated regulator drives that incorporate intelligent power management features, such as adaptive voltage scaling and predictive diagnostics. Manufacturers focusing on emerging technologies like GaN and SiC, and those that can effectively navigate supply chain complexities and stringent regulatory environments, are well-positioned for substantial growth. The market's trajectory indicates a strong upward trend, supported by technological breakthroughs and the fundamental need for efficient power delivery in an increasingly electrified and connected world.

Regulator Drive Segmentation

-

1. Application

- 1.1. Power Management

- 1.2. Power Tools and Motors

- 1.3. Vehicle Electronics

- 1.4. Communication Device

- 1.5. Others

-

2. Type

- 2.1. Contact Regulator Driver

- 2.2. Transistor Regulator Driver

- 2.3. Integrated Circuit Regulator Driver

- 2.4. Computer Controlled Voltage Regulator Driver

Regulator Drive Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Regulator Drive REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XXX% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Regulator Drive Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Power Management

- 5.1.2. Power Tools and Motors

- 5.1.3. Vehicle Electronics

- 5.1.4. Communication Device

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Contact Regulator Driver

- 5.2.2. Transistor Regulator Driver

- 5.2.3. Integrated Circuit Regulator Driver

- 5.2.4. Computer Controlled Voltage Regulator Driver

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Regulator Drive Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Power Management

- 6.1.2. Power Tools and Motors

- 6.1.3. Vehicle Electronics

- 6.1.4. Communication Device

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Contact Regulator Driver

- 6.2.2. Transistor Regulator Driver

- 6.2.3. Integrated Circuit Regulator Driver

- 6.2.4. Computer Controlled Voltage Regulator Driver

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Regulator Drive Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Power Management

- 7.1.2. Power Tools and Motors

- 7.1.3. Vehicle Electronics

- 7.1.4. Communication Device

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Contact Regulator Driver

- 7.2.2. Transistor Regulator Driver

- 7.2.3. Integrated Circuit Regulator Driver

- 7.2.4. Computer Controlled Voltage Regulator Driver

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Regulator Drive Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Power Management

- 8.1.2. Power Tools and Motors

- 8.1.3. Vehicle Electronics

- 8.1.4. Communication Device

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Contact Regulator Driver

- 8.2.2. Transistor Regulator Driver

- 8.2.3. Integrated Circuit Regulator Driver

- 8.2.4. Computer Controlled Voltage Regulator Driver

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Regulator Drive Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Power Management

- 9.1.2. Power Tools and Motors

- 9.1.3. Vehicle Electronics

- 9.1.4. Communication Device

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Contact Regulator Driver

- 9.2.2. Transistor Regulator Driver

- 9.2.3. Integrated Circuit Regulator Driver

- 9.2.4. Computer Controlled Voltage Regulator Driver

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Regulator Drive Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Power Management

- 10.1.2. Power Tools and Motors

- 10.1.3. Vehicle Electronics

- 10.1.4. Communication Device

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Contact Regulator Driver

- 10.2.2. Transistor Regulator Driver

- 10.2.3. Integrated Circuit Regulator Driver

- 10.2.4. Computer Controlled Voltage Regulator Driver

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Texas Instruments Incorporated

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 ON Semiconductor Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Infineon Technologies

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 STMicroelectronics N.V.

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Microchip Technology Inc.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Analog Devices Inc.

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 NXP Semiconductors N.V.

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Maxim Integrated

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Rohm Semiconductor

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Toshiba Electronic Devices & Storage Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Diodes Incorporated

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Monolithic Power Systems Inc.

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Richtek Technology Corporation

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Semtech Corporation

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Zhejiang Zhengxi Electric Group Co. Ltd.

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Qingdao Kekai Electronics Research Institute Co. Ltd.

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Texas Instruments Incorporated

List of Figures

- Figure 1: Global Regulator Drive Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Regulator Drive Revenue (million), by Application 2024 & 2032

- Figure 3: North America Regulator Drive Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Regulator Drive Revenue (million), by Type 2024 & 2032

- Figure 5: North America Regulator Drive Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Regulator Drive Revenue (million), by Country 2024 & 2032

- Figure 7: North America Regulator Drive Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Regulator Drive Revenue (million), by Application 2024 & 2032

- Figure 9: South America Regulator Drive Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Regulator Drive Revenue (million), by Type 2024 & 2032

- Figure 11: South America Regulator Drive Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Regulator Drive Revenue (million), by Country 2024 & 2032

- Figure 13: South America Regulator Drive Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Regulator Drive Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Regulator Drive Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Regulator Drive Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Regulator Drive Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Regulator Drive Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Regulator Drive Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Regulator Drive Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Regulator Drive Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Regulator Drive Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Regulator Drive Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Regulator Drive Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Regulator Drive Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Regulator Drive Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Regulator Drive Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Regulator Drive Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Regulator Drive Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Regulator Drive Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Regulator Drive Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Regulator Drive Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Regulator Drive Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Regulator Drive Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Regulator Drive Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Regulator Drive Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Regulator Drive Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Regulator Drive Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Regulator Drive Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Regulator Drive Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Regulator Drive Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Regulator Drive Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Regulator Drive Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Regulator Drive Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Regulator Drive Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Regulator Drive Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Regulator Drive Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Regulator Drive Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Regulator Drive Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Regulator Drive Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Regulator Drive Revenue (million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Regulator Drive?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Regulator Drive?

Key companies in the market include Texas Instruments Incorporated, ON Semiconductor Corporation, Infineon Technologies, STMicroelectronics N.V., Microchip Technology Inc., Analog Devices, Inc., NXP Semiconductors N.V., Maxim Integrated, Rohm Semiconductor, Toshiba Electronic Devices & Storage Corporation, Diodes Incorporated, Monolithic Power Systems, Inc., Richtek Technology Corporation, Semtech Corporation, Zhejiang Zhengxi Electric Group Co., Ltd., Qingdao Kekai Electronics Research Institute Co., Ltd..

3. What are the main segments of the Regulator Drive?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Regulator Drive," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Regulator Drive report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Regulator Drive?

To stay informed about further developments, trends, and reports in the Regulator Drive, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence