Key Insights

The European wireless sensor market is experiencing robust growth, driven by increasing automation across diverse sectors and the burgeoning adoption of IoT technologies. The market, valued at approximately €X million in 2025 (assuming a logical estimation based on the provided CAGR of 23.10% and unspecified market size "XX"), is projected to expand significantly over the forecast period (2025-2033). Key growth drivers include the rising demand for real-time monitoring and data analytics in industries like automotive, healthcare, and energy, coupled with advancements in sensor technology leading to improved accuracy, reduced power consumption, and enhanced connectivity. The automotive sector is a major contributor, fueled by the proliferation of advanced driver-assistance systems (ADAS) and autonomous driving initiatives. Furthermore, the healthcare sector's increasing adoption of remote patient monitoring and the growth of smart homes are creating substantial opportunities for wireless sensor deployment. Germany, France, and the UK represent the largest national markets within Europe, benefiting from established industrial bases and technological infrastructure. However, regulatory compliance requirements and concerns related to data security pose potential challenges to market expansion.

The competitive landscape is characterized by a mix of established players like Honeywell, ABB, and Siemens, alongside specialized sensor manufacturers and smaller technology firms. These companies are continuously innovating to offer more sophisticated sensors with enhanced functionalities and improved integration capabilities. The market segmentation highlights the dominance of pressure and temperature sensors, reflecting widespread applications across various industries. Future growth will be heavily influenced by the maturation of 5G networks, enhancing connectivity and data transmission speeds, thereby unlocking new applications for wireless sensor technologies in smart cities, industrial automation, and precision agriculture. The continuous miniaturization and improved cost-effectiveness of wireless sensors will also play a crucial role in expanding market penetration across various industry verticals. Despite the restraints, the overall outlook for the European wireless sensors market remains positive, underpinned by technological advancements, increasing digitization, and strong demand from diverse end-user sectors.

European Wireless Sensors Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the European wireless sensors market, encompassing market dynamics, growth trends, dominant segments, and key players. The study period covers 2019-2033, with 2025 as the base and estimated year. The report offers invaluable insights for industry professionals, investors, and strategic decision-makers seeking to navigate this rapidly evolving landscape. The market is segmented by type (Pressure Sensor, Temperature Sensor, Chemical and Gas Sensor, Position and Proximity Sensor, Other Types), end-user industry (Automotive, Healthcare, Aerospace and Defense, Energy and Power, Food and Beverage, Other End-user Industries), and country (United Kingdom, Germany, Italy, France, Rest of Europe).

European Wireless Sensors Industry Market Dynamics & Structure

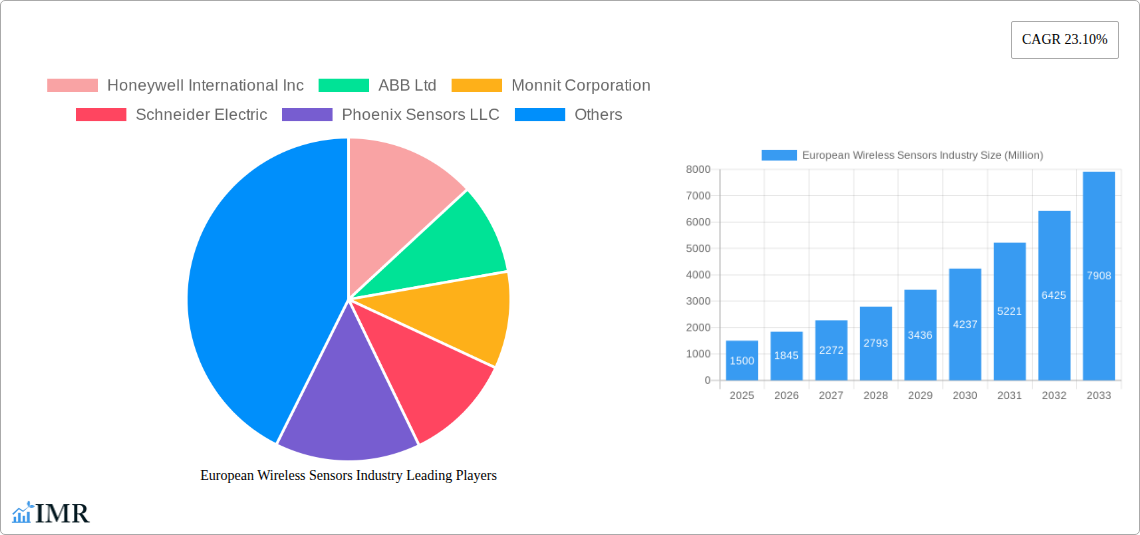

The European wireless sensors market is characterized by moderate concentration, with several key players holding significant market share, while numerous smaller companies cater to niche segments. The market size in 2025 is estimated at xx Million Units. Technological innovation is a crucial driver, spurred by advancements in low-power wide-area networks (LPWAN), miniaturization, and improved sensor accuracy. Stringent regulatory frameworks concerning data security and environmental compliance influence market developments. Competitive pressure from wired sensor alternatives remains, but the advantages of wireless sensors – such as ease of installation and remote monitoring – are driving adoption. The market also experiences frequent M&A activity, consolidating the market and fostering innovation. The overall market concentration is estimated at xx%, with the top 5 players holding approximately xx% of the market share.

- Market Concentration: xx% in 2025, projected to reach xx% by 2033.

- M&A Activity: An average of xx deals per year during the historical period (2019-2024).

- Innovation Barriers: High initial investment costs, interoperability challenges, and data security concerns.

- End-user Demographics: Growth is driven by increasing demand from industrial automation, smart cities, and IoT applications.

European Wireless Sensors Industry Growth Trends & Insights

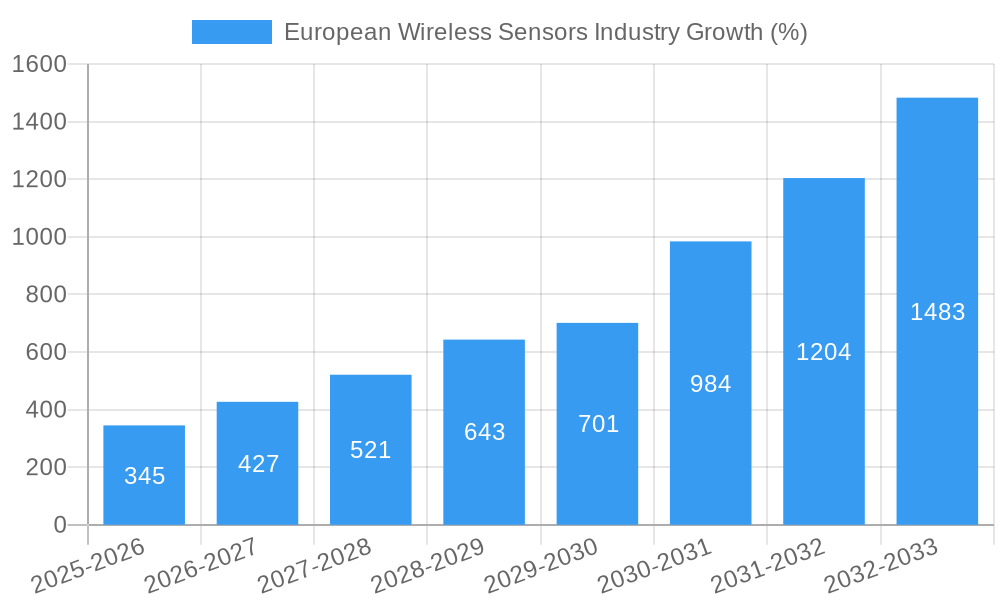

The European wireless sensors market witnessed significant growth during the historical period (2019-2024), fueled by the increasing adoption of IoT and Industry 4.0 initiatives. The market size expanded from xx Million Units in 2019 to xx Million Units in 2024, exhibiting a CAGR of xx%. This growth is projected to continue, reaching xx Million Units by 2033, with a projected CAGR of xx% during the forecast period (2025-2033). Technological advancements like LPWAN technologies and improved sensor capabilities are contributing to enhanced market penetration. Consumer behavior shifts towards remote monitoring and automated systems further propel adoption. Market penetration in key end-user industries, such as automotive and healthcare, is increasing steadily, with higher adoption rates observed in the industrial automation sector.

Dominant Regions, Countries, or Segments in European Wireless Sensors Industry

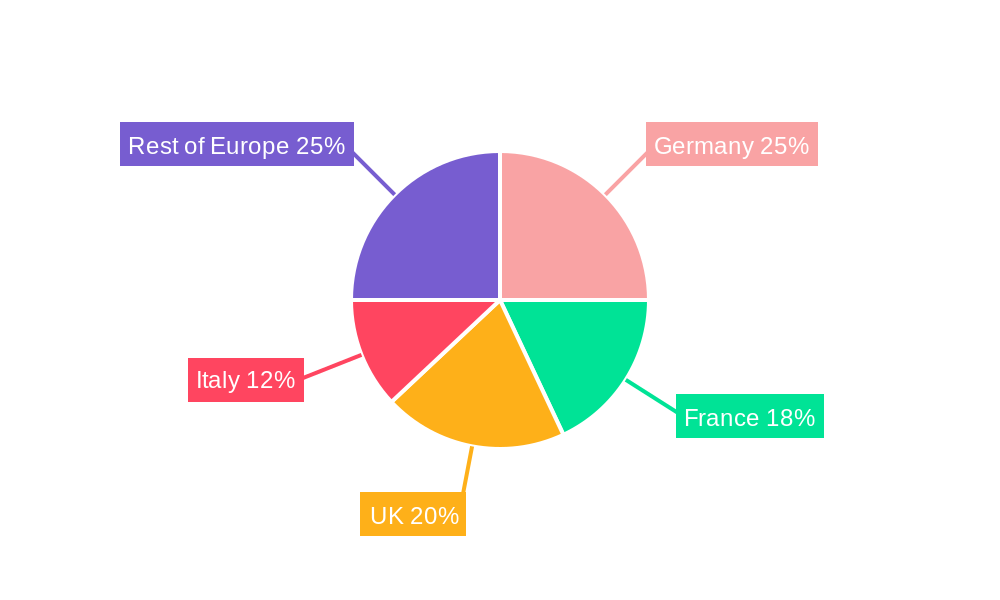

Germany and the United Kingdom represent the largest national markets within Europe, driven by robust industrial automation sectors and supportive government policies. The industrial automation sector drives demand for sensors across diverse types such as pressure sensors, chemical and gas sensors, and position and proximity sensors. The automotive and healthcare industries are also key growth drivers in specific countries and regions. Germany's strong manufacturing base and advanced technology sector contribute to its leading position, while the UK's substantial investments in smart city infrastructure support market growth. Italy and France show promising growth potential, driven by increasing investment in smart infrastructure and adoption of IoT solutions.

- Germany: Strong industrial base and focus on Industry 4.0.

- United Kingdom: Significant investments in smart city projects and IoT initiatives.

- Pressure Sensors: Largest segment by type, driven by high demand from industrial automation and automotive sectors.

- Automotive: Leading end-user industry due to increasing vehicle automation and safety features.

European Wireless Sensors Industry Product Landscape

The European wireless sensor market features a diverse range of products, characterized by continuous innovation in miniaturization, power efficiency, and communication protocols. New sensor designs incorporate advanced materials and manufacturing processes to achieve enhanced accuracy, reliability, and durability. Wireless sensors are now capable of measuring a wide range of parameters, including temperature, pressure, humidity, gas concentration, acceleration, and proximity, with improved capabilities for data transmission and analytics. Many sensors offer robust security features and can integrate with various cloud platforms for real-time monitoring and data analysis. Unique selling propositions frequently include long battery life, ease of installation, and enhanced data security.

Key Drivers, Barriers & Challenges in European Wireless Sensors Industry

Key Drivers: The increasing adoption of IoT and Industry 4.0 are primary drivers, along with rising demand for remote monitoring and predictive maintenance in various sectors. Government initiatives promoting smart cities and digitalization further stimulate market growth.

Challenges: High initial investment costs for infrastructure, interoperability issues among diverse sensor systems, and concerns regarding data security and privacy pose challenges to wider adoption. Supply chain disruptions and the availability of skilled labor also impact market expansion. Regulatory hurdles related to data privacy and environmental regulations are also potential bottlenecks. Competitive pressure from wired sensors and other technologies is a long-term challenge.

Emerging Opportunities in European Wireless Sensors Industry

Emerging opportunities lie in the expanding applications of wireless sensors in smart agriculture, environmental monitoring, and healthcare. The integration of AI and machine learning with sensor data analysis is opening new avenues for predictive maintenance and data-driven decision-making. The development of low-power, long-range wireless communication technologies and the rising demand for energy efficiency contribute to growth. Untapped markets in smaller European countries and specialized applications offer further potential.

Growth Accelerators in the European Wireless Sensors Industry

Technological advancements, particularly in LPWAN technologies and sensor miniaturization, are key growth accelerators. Strategic partnerships among sensor manufacturers, software providers, and system integrators are crucial for successful market expansion. Government policies and incentives promoting digital transformation and smart city initiatives boost market development. The increasing integration of wireless sensors into diverse applications across numerous sectors drives continuous growth.

Key Players Shaping the European Wireless Sensors Industry Market

- Honeywell International Inc

- ABB Ltd

- Monnit Corporation

- Schneider Electric

- Phoenix Sensors LLC

- Texas Instruments Incorporated

- Pasco Scientific

- Emerson Electric Co

- Siemens AG

Notable Milestones in European Wireless Sensors Industry Sector

- June 2020: ABB announced a wireless condition monitoring solution for rotating equipment, enhancing efficiency and reducing installation costs.

- January 2021: Disruptive Technologies collaborated with Ex-tech Group, launching IP68-rated wireless sensors for explosive environments, expanding application possibilities.

In-Depth European Wireless Sensors Industry Market Outlook

The European wireless sensors market is poised for sustained growth, driven by ongoing technological advancements, increasing adoption across diverse sectors, and supportive government policies. The integration of AI and machine learning will further enhance data analysis and create new opportunities for predictive maintenance and smart decision-making. Strategic partnerships and the expansion into new applications will be crucial for long-term success. The market's future potential is significant, with opportunities for innovation and expansion across various end-user industries.

European Wireless Sensors Industry Segmentation

-

1. Type

- 1.1. Pressure Sensor

- 1.2. Temperature Sensor

- 1.3. Chemical and Gas Sensor

- 1.4. Position and Proximity Sensor

- 1.5. Other Types

-

2. End-user Industry

- 2.1. Automotive

- 2.2. Healthcare

- 2.3. Aerospace and Defense

- 2.4. Energy and Power

- 2.5. Food and Beverage

- 2.6. Other End-user Industries

European Wireless Sensors Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

European Wireless Sensors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 23.10% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Adoption of Wireless Technologies (Especially in Harsh Environments); Emergence of Smart Factory Concepts (Industrial Automation)

- 3.3. Market Restrains

- 3.3.1. False Triggering of Switch and Inconsistency Issues Associated with Wireless Network Systems

- 3.4. Market Trends

- 3.4.1. Automotive is Expected to Hold Significant Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. European Wireless Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Pressure Sensor

- 5.1.2. Temperature Sensor

- 5.1.3. Chemical and Gas Sensor

- 5.1.4. Position and Proximity Sensor

- 5.1.5. Other Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Automotive

- 5.2.2. Healthcare

- 5.2.3. Aerospace and Defense

- 5.2.4. Energy and Power

- 5.2.5. Food and Beverage

- 5.2.6. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany European Wireless Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 7. France European Wireless Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy European Wireless Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom European Wireless Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands European Wireless Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden European Wireless Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe European Wireless Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Honeywell International Inc

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 ABB Ltd

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Monnit Corporation

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Schneider Electric

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Phoenix Sensors LLC

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Texas Instruments Incorporated*List Not Exhaustive

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Pasco Scientific

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 Emerson Electric Co

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 Siemens AG

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.1 Honeywell International Inc

List of Figures

- Figure 1: European Wireless Sensors Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: European Wireless Sensors Industry Share (%) by Company 2024

List of Tables

- Table 1: European Wireless Sensors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: European Wireless Sensors Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: European Wireless Sensors Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: European Wireless Sensors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: European Wireless Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Germany European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: France European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Italy European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: United Kingdom European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Netherlands European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Sweden European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: European Wireless Sensors Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 14: European Wireless Sensors Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 15: European Wireless Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: United Kingdom European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Germany European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: France European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Italy European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Spain European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Netherlands European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Belgium European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Sweden European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Norway European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Poland European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Denmark European Wireless Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Wireless Sensors Industry?

The projected CAGR is approximately 23.10%.

2. Which companies are prominent players in the European Wireless Sensors Industry?

Key companies in the market include Honeywell International Inc, ABB Ltd, Monnit Corporation, Schneider Electric, Phoenix Sensors LLC, Texas Instruments Incorporated*List Not Exhaustive, Pasco Scientific, Emerson Electric Co, Siemens AG.

3. What are the main segments of the European Wireless Sensors Industry?

The market segments include Type, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Wireless Technologies (Especially in Harsh Environments); Emergence of Smart Factory Concepts (Industrial Automation).

6. What are the notable trends driving market growth?

Automotive is Expected to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

False Triggering of Switch and Inconsistency Issues Associated with Wireless Network Systems.

8. Can you provide examples of recent developments in the market?

January 2021 - Disruptive Technologies (DT), a Norwegian developer smallest wireless sensors, collaborated with Ex-tech Group, an expert in the ex-area. Sensors from Disruptive Technologies have an IP68 rating and can withstand extremely high temperatures. Moreover, sensors can measure critical humidity, temperature, and proximity/presence in explosive atmospheres. Owing to the ex-protection, they can be deployed directly on/in other Ex-protected equipment. The sensor solution provides accurate monitoring and reporting of operational data continuously.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Wireless Sensors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Wireless Sensors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Wireless Sensors Industry?

To stay informed about further developments, trends, and reports in the European Wireless Sensors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence