Key Insights

The global sleep industry is poised for substantial growth, projected to reach an estimated market size of $XX million with a Compound Annual Growth Rate (CAGR) of 7.10% between 2025 and 2033. This robust expansion is fueled by a confluence of critical drivers, including the escalating prevalence of sleep disorders such as insomnia and sleep apnea, a growing awareness among consumers about the profound impact of quality sleep on overall health and well-being, and significant advancements in sleep technology and therapeutic solutions. The industry encompasses a diverse range of segments, from essential products like mattresses and pillows to advanced sleep laboratory services, and pharmaceuticals. The increasing demand for innovative sleep aids and diagnostic tools, coupled with a rising disposable income globally, further underpins this optimistic growth trajectory.

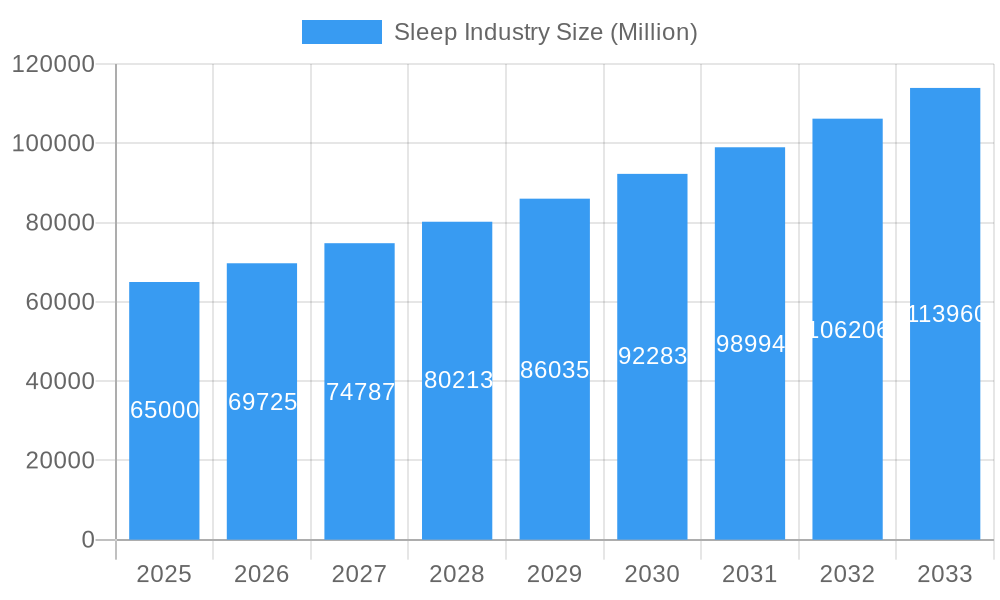

Sleep Industry Market Size (In Billion)

Key trends shaping the sleep industry include the rapid development and adoption of wearable sleep trackers, smart beds, and advanced sleep apnea treatment devices, all offering more personalized and effective sleep management solutions. Furthermore, there's a growing emphasis on the integration of sleep health into broader wellness and corporate wellness programs, recognizing sleep as a foundational pillar of health. However, the industry faces certain restraints, such as the high cost of some advanced sleep diagnostic and treatment technologies, which can limit accessibility for a segment of the population. Regulatory hurdles and the need for extensive clinical validation for new sleep therapies can also present challenges. Despite these constraints, the overwhelming societal recognition of sleep's importance, particularly in the wake of global health events that have highlighted the need for robust immune systems and mental resilience, ensures continued market expansion and innovation across all segments.

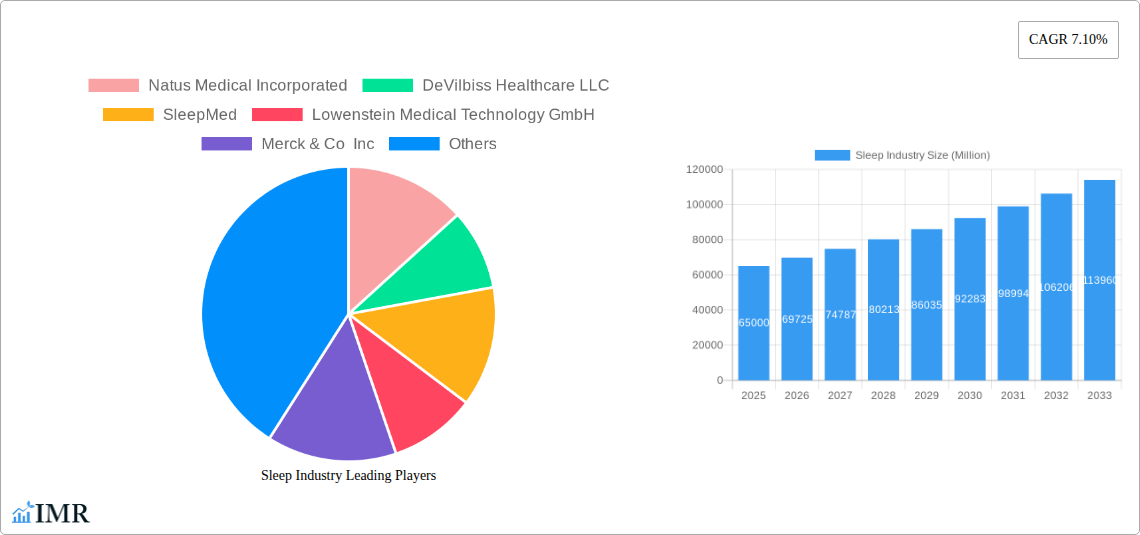

Sleep Industry Company Market Share

Unlocking the Global Sleep Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a strategic analysis of the global sleep industry, offering unparalleled insights into its intricate dynamics, growth trajectory, and competitive landscape. Designed for industry leaders, investors, and market strategists, this research delves into key segments, regional dominance, and emerging trends that are shaping the future of sleep health. From groundbreaking product innovations to evolving consumer behaviors and robust regulatory frameworks, understand the forces driving this multi-billion dollar market.

Sleep Industry Market Dynamics & Structure

The global sleep industry is characterized by a dynamic interplay of market concentration, rapid technological innovation, and evolving regulatory landscapes. High market concentration is observed in segments like Continuous Positive Airway Pressure (CPAP) devices, where established players hold significant sway. Conversely, newer segments like digital therapeutics and personalized sleep solutions exhibit more fragmented structures, fostering innovation. Technological innovation is primarily driven by advancements in AI-powered sleep tracking, wearable technology, and non-invasive diagnostic tools, aiming to provide more accurate and personalized sleep solutions. Regulatory frameworks, while crucial for ensuring patient safety and product efficacy, can also present barriers to entry, particularly for novel treatments and devices. Competitive product substitutes are increasingly prevalent, ranging from over-the-counter sleep aids and natural remedies to advanced medical devices and behavioral therapy programs. End-user demographics are diverse, encompassing a growing aging population, individuals with chronic sleep disorders, and a broader consumer base seeking to optimize sleep quality for general well-being. Mergers and acquisitions (M&A) trends are robust, with larger corporations acquiring innovative startups to expand their product portfolios and market reach. For instance, there were an estimated 15 M&A deals in the sleep tech sector during the historical period 2019-2024, indicating a strong consolidation drive. The market share of dominant players in the CPAP segment is estimated to be around 60% collectively. Innovation barriers include high R&D costs, stringent clinical trial requirements, and the need for extensive consumer education to drive adoption of new technologies.

- Market Concentration: High in established device segments, fragmented in emerging digital health solutions.

- Technological Drivers: AI in sleep tracking, wearables, non-invasive diagnostics, digital therapeutics.

- Regulatory Impact: Essential for safety, but can create market entry barriers.

- Competitive Landscape: Diverse, from OTC remedies to advanced medical devices.

- End-User Focus: Aging population, sleep disorder patients, general wellness consumers.

- M&A Activity: Significant, indicating consolidation and strategic expansion. Estimated 15 deals from 2019-2024.

Sleep Industry Growth Trends & Insights

The global sleep industry is poised for significant growth, driven by a confluence of escalating health awareness, technological advancements, and an increasing prevalence of sleep disorders. The market size is projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period of 2025–2033, reaching an estimated value of over $120,000 million units by 2033. This robust expansion is fueled by a growing understanding of sleep’s critical role in overall health and well-being, leading to increased demand for effective sleep solutions. Adoption rates for advanced sleep tracking devices and wearable technology are soaring, with an estimated market penetration of over 40% among health-conscious consumers in developed regions by 2025. Technological disruptions, such as the integration of artificial intelligence in diagnostic tools and the development of personalized sleep interventions, are revolutionizing how sleep disorders are managed. These innovations are not only improving diagnostic accuracy but also offering more tailored and effective treatment options, thereby enhancing patient outcomes. Consumer behavior shifts are also a major catalyst. There is a discernible move from simply treating sleep disorders to proactively optimizing sleep for enhanced cognitive function, physical performance, and mental health. This shift is evident in the rising popularity of sleep-related apps, smart bedding, and wellness programs focused on sleep hygiene. The increasing focus on preventative healthcare further bolsters the demand for solutions that promote healthy sleep habits. The Medication segment, while important, is increasingly being complemented by non-pharmacological approaches, reflecting a holistic approach to sleep health. The estimated market size for the sleep industry in the base year of 2025 is approximately $65,000 million units.

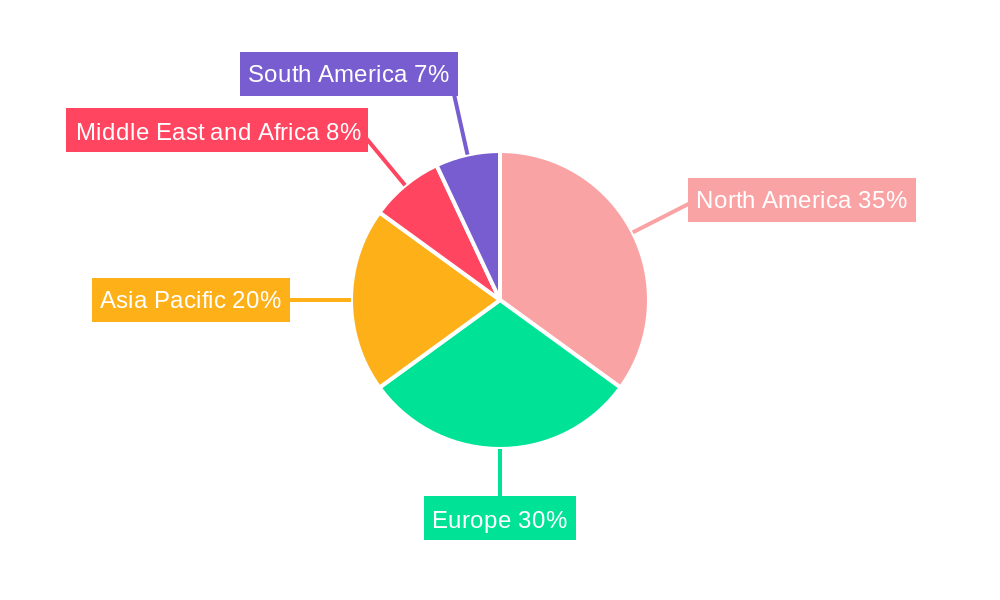

Dominant Regions, Countries, or Segments in Sleep Industry

The global sleep industry's growth is propelled by distinct regional strengths and segment dominance, with North America emerging as a leading market due to high disposable incomes, robust healthcare infrastructure, and a strong emphasis on personal well-being. The United States, in particular, accounts for a significant share of the global market, driven by high awareness of sleep disorders, particularly sleep apnea and insomnia, and substantial investment in sleep research and technology. The prevalence of sleep disorders in this region, estimated at over 70,000 million individuals suffering from at least one sleep-related issue, significantly fuels the demand for mattresses and pillows, sleep laboratory services, and pharmaceutical interventions.

The Mattresses and Pillows segment is consistently a top performer within the product landscape, driven by continuous innovation in materials, ergonomics, and smart technology, projected to capture over 35% of the total market value by 2025. This segment’s dominance is further amplified by the growing consumer interest in achieving optimal sleep comfort and support for general health benefits.

In terms of sleep disorders, Sleep Apnea remains a critical driver of market growth, accounting for an estimated 40% of the total sleep disorder market value. The increasing diagnosis rates, coupled with the availability of advanced CPAP devices and related accessories, contribute to this segment's robust performance. The global market for Sleep Apnea diagnosis and treatment solutions is expected to reach approximately $30,000 million units by 2025.

Key drivers for North America's dominance include government initiatives promoting sleep health awareness, favorable reimbursement policies for sleep disorder treatments, and the presence of leading sleep technology manufacturers and research institutions. Economic policies that support healthcare innovation and consumer spending on health and wellness products further solidify its leading position. The country's advanced healthcare infrastructure supports the widespread availability of specialized sleep clinics and diagnostic services, enhancing accessibility for a broader patient population. The estimated market share of North America in the global sleep industry is approximately 38% in 2025.

- Dominant Region: North America (primarily the USA).

- Key Product Segment: Mattresses and Pillows (projected 35% market share by 2025).

- Dominant Sleep Disorder Segment: Sleep Apnea (estimated 40% market value contribution).

- Drivers for Dominance: High disposable income, advanced healthcare, sleep health awareness, supportive policies, technological innovation.

Sleep Industry Product Landscape

The sleep industry's product landscape is characterized by continuous innovation, ranging from foundational essentials to cutting-edge technological solutions. Mattresses and pillows are undergoing a transformation with the integration of advanced materials like memory foam, cooling gels, and adjustable firmness options, catering to personalized comfort and therapeutic needs. Sleep laboratory services are evolving with the advent of home sleep apnea testing (HSAT) devices and AI-powered polysomnography (PSG) analysis, offering greater convenience and accuracy. The medication segment continues to see development in pharmaceutical treatments for insomnia and narcolepsy, with a growing emphasis on targeted therapies with fewer side effects. Other products encompass a wide array of wearables for sleep tracking, smart bedding, light therapy devices, and white noise machines, all designed to enhance sleep quality. Unique selling propositions often revolve around data-driven personalization, evidence-based efficacy, and user-friendly interfaces. Technological advancements are pivotal, with companies like Koninklijke Philips N.V. and Fisher & Paykel Healthcare Limited leading in the development of sophisticated CPAP machines and respiratory support systems. The overall product performance is measured by patient adherence, diagnostic accuracy, and measurable improvements in sleep quality and overall health outcomes.

Key Drivers, Barriers & Challenges in Sleep Industry

The sleep industry is propelled by several key drivers, including the escalating global prevalence of sleep disorders like insomnia and sleep apnea, a growing awareness of sleep's impact on overall health and cognitive function, and significant advancements in sleep technology and diagnostics. The aging population also contributes to increased demand for sleep solutions. Technological breakthroughs in wearables and AI-driven analysis are further accelerating market growth by providing personalized and accessible insights.

- Technological Advancements: AI in sleep tracking, wearables, non-invasive diagnostics.

- Health Awareness: Increased understanding of sleep’s importance for well-being.

- Prevalence of Sleep Disorders: Growing numbers of insomnia and sleep apnea diagnoses.

- Aging Population: Demographic shift increasing demand for sleep solutions.

However, the industry faces notable barriers and challenges. High development costs for new medical devices and pharmaceuticals, coupled with stringent regulatory approval processes, can hinder market entry and product innovation. Supply chain disruptions, as witnessed in recent global events, can impact the availability of essential components and finished goods. Competitive pressures from both established players and new entrants, along with potential reimbursement issues for new technologies, also pose significant challenges. Furthermore, consumer education regarding the efficacy and proper use of advanced sleep solutions remains crucial.

- High R&D and Regulatory Costs: Significant investment required for innovation and approval.

- Supply Chain Vulnerabilities: Potential disruptions affecting product availability.

- Reimbursement Complexities: Navigating insurance policies for new technologies.

- Intense Competition: Market saturation and the need for differentiation.

Emerging Opportunities in Sleep Industry

Emerging opportunities in the sleep industry are centered around personalized sleep solutions, the integration of sleep technology into broader wellness ecosystems, and the expansion of digital therapeutics. The growing demand for at-home diagnostic tools and remote patient monitoring presents a significant untapped market. The development of AI-powered platforms that offer personalized sleep coaching and behavioral interventions, such as digital sleep clinics, is gaining traction. Furthermore, the intersection of sleep and mental health is opening avenues for integrated solutions that address anxiety, depression, and sleep disturbances concurrently. The focus on preventative health and performance optimization is also creating demand for sleep solutions that cater to athletes, high-achieving professionals, and individuals seeking to enhance their daily functioning.

Growth Accelerators in the Sleep Industry Industry

The long-term growth of the sleep industry is significantly accelerated by ongoing technological breakthroughs, particularly in artificial intelligence and machine learning, which are enhancing the accuracy of sleep monitoring and the personalization of treatments. Strategic partnerships between technology companies, healthcare providers, and pharmaceutical firms are creating synergistic opportunities for comprehensive sleep health solutions. Market expansion strategies, including entering nascent markets and developing products tailored to diverse demographic needs, are crucial growth catalysts. The increasing consumer adoption of wearable devices and the growing recognition of sleep as a vital component of overall health and wellness are fundamentally reshaping the market and driving sustained expansion.

Key Players Shaping the Sleep Industry Market

- Natus Medical Incorporated

- DeVilbiss Healthcare LLC

- SleepMed

- Lowenstein Medical Technology GmbH

- Merck & Co Inc

- Compumedics Limited

- Koninklijke Philips N V

- Eisai Inc

- Fisher & Paykel Healthcare Limited

- BMC Medical Co Ltd

- Cadwell

- Takeda Pharmaceutical Company Limited

Notable Milestones in Sleep Industry Sector

- June 2022: Sleep Habit launched Sleep Reset, a digital, personalized sleep clinic accessible via iPhone and Android apps, utilizing clinically proven methods to address the root cause of sleep issues.

- May 2022: StimScience launched Somnee, the first electronic sleep aid headband using personalized non-invasive brain stimulation to improve sleep quality.

In-Depth Sleep Industry Market Outlook

The future outlook for the sleep industry is exceptionally promising, driven by continuous innovation and an escalating global focus on holistic health. Growth accelerators such as advancements in AI-powered diagnostics, personalized digital therapeutics, and smart wearable technology will continue to shape the market. Strategic opportunities lie in addressing the unmet needs of underserved populations and expanding into emerging economies where awareness of sleep health is growing. The increasing integration of sleep solutions within broader wellness platforms signifies a shift towards a more proactive and preventative approach to healthcare, ensuring sustained market expansion and a significant positive impact on global public health.

Sleep Industry Segmentation

-

1. Product

- 1.1. Mattresses and Pillows

- 1.2. Sleep Laboratory Services

- 1.3. Medication

- 1.4. Other Products

-

2. Sleep Disorder

- 2.1. Insomnia

- 2.2. Sleep Apnea

- 2.3. Other Sleep Disorders

Sleep Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Sleep Industry Regional Market Share

Geographic Coverage of Sleep Industry

Sleep Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.10% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Prevalence of Insomnia and Other Disorders; Increasing Adoption of Wearable Monitors and Sensors

- 3.3. Market Restrains

- 3.3.1. Side Effects Associated With Sleep Medications

- 3.4. Market Trends

- 3.4.1. Insomnia Segment is Expected to Hold a Significant Market Share Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Sleep Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. Mattresses and Pillows

- 5.1.2. Sleep Laboratory Services

- 5.1.3. Medication

- 5.1.4. Other Products

- 5.2. Market Analysis, Insights and Forecast - by Sleep Disorder

- 5.2.1. Insomnia

- 5.2.2. Sleep Apnea

- 5.2.3. Other Sleep Disorders

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. North America Sleep Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Product

- 6.1.1. Mattresses and Pillows

- 6.1.2. Sleep Laboratory Services

- 6.1.3. Medication

- 6.1.4. Other Products

- 6.2. Market Analysis, Insights and Forecast - by Sleep Disorder

- 6.2.1. Insomnia

- 6.2.2. Sleep Apnea

- 6.2.3. Other Sleep Disorders

- 6.1. Market Analysis, Insights and Forecast - by Product

- 7. Europe Sleep Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product

- 7.1.1. Mattresses and Pillows

- 7.1.2. Sleep Laboratory Services

- 7.1.3. Medication

- 7.1.4. Other Products

- 7.2. Market Analysis, Insights and Forecast - by Sleep Disorder

- 7.2.1. Insomnia

- 7.2.2. Sleep Apnea

- 7.2.3. Other Sleep Disorders

- 7.1. Market Analysis, Insights and Forecast - by Product

- 8. Asia Pacific Sleep Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product

- 8.1.1. Mattresses and Pillows

- 8.1.2. Sleep Laboratory Services

- 8.1.3. Medication

- 8.1.4. Other Products

- 8.2. Market Analysis, Insights and Forecast - by Sleep Disorder

- 8.2.1. Insomnia

- 8.2.2. Sleep Apnea

- 8.2.3. Other Sleep Disorders

- 8.1. Market Analysis, Insights and Forecast - by Product

- 9. Middle East and Africa Sleep Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product

- 9.1.1. Mattresses and Pillows

- 9.1.2. Sleep Laboratory Services

- 9.1.3. Medication

- 9.1.4. Other Products

- 9.2. Market Analysis, Insights and Forecast - by Sleep Disorder

- 9.2.1. Insomnia

- 9.2.2. Sleep Apnea

- 9.2.3. Other Sleep Disorders

- 9.1. Market Analysis, Insights and Forecast - by Product

- 10. South America Sleep Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Product

- 10.1.1. Mattresses and Pillows

- 10.1.2. Sleep Laboratory Services

- 10.1.3. Medication

- 10.1.4. Other Products

- 10.2. Market Analysis, Insights and Forecast - by Sleep Disorder

- 10.2.1. Insomnia

- 10.2.2. Sleep Apnea

- 10.2.3. Other Sleep Disorders

- 10.1. Market Analysis, Insights and Forecast - by Product

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Natus Medical Incorporated

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 DeVilbiss Healthcare LLC

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 SleepMed

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Lowenstein Medical Technology GmbH

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Merck & Co Inc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Compumedics Limited

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Koninklijke Philips N V

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Eisai Inc

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Fisher & Paykel Healthcare Limited

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 BMC Medical Co Ltd

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Cadwell

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Takeda Pharmaceutical Company Limited*List Not Exhaustive

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Natus Medical Incorporated

List of Figures

- Figure 1: Global Sleep Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Sleep Industry Revenue (Million), by Product 2025 & 2033

- Figure 3: North America Sleep Industry Revenue Share (%), by Product 2025 & 2033

- Figure 4: North America Sleep Industry Revenue (Million), by Sleep Disorder 2025 & 2033

- Figure 5: North America Sleep Industry Revenue Share (%), by Sleep Disorder 2025 & 2033

- Figure 6: North America Sleep Industry Revenue (Million), by Country 2025 & 2033

- Figure 7: North America Sleep Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Sleep Industry Revenue (Million), by Product 2025 & 2033

- Figure 9: Europe Sleep Industry Revenue Share (%), by Product 2025 & 2033

- Figure 10: Europe Sleep Industry Revenue (Million), by Sleep Disorder 2025 & 2033

- Figure 11: Europe Sleep Industry Revenue Share (%), by Sleep Disorder 2025 & 2033

- Figure 12: Europe Sleep Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Europe Sleep Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Sleep Industry Revenue (Million), by Product 2025 & 2033

- Figure 15: Asia Pacific Sleep Industry Revenue Share (%), by Product 2025 & 2033

- Figure 16: Asia Pacific Sleep Industry Revenue (Million), by Sleep Disorder 2025 & 2033

- Figure 17: Asia Pacific Sleep Industry Revenue Share (%), by Sleep Disorder 2025 & 2033

- Figure 18: Asia Pacific Sleep Industry Revenue (Million), by Country 2025 & 2033

- Figure 19: Asia Pacific Sleep Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Sleep Industry Revenue (Million), by Product 2025 & 2033

- Figure 21: Middle East and Africa Sleep Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Middle East and Africa Sleep Industry Revenue (Million), by Sleep Disorder 2025 & 2033

- Figure 23: Middle East and Africa Sleep Industry Revenue Share (%), by Sleep Disorder 2025 & 2033

- Figure 24: Middle East and Africa Sleep Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Middle East and Africa Sleep Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Sleep Industry Revenue (Million), by Product 2025 & 2033

- Figure 27: South America Sleep Industry Revenue Share (%), by Product 2025 & 2033

- Figure 28: South America Sleep Industry Revenue (Million), by Sleep Disorder 2025 & 2033

- Figure 29: South America Sleep Industry Revenue Share (%), by Sleep Disorder 2025 & 2033

- Figure 30: South America Sleep Industry Revenue (Million), by Country 2025 & 2033

- Figure 31: South America Sleep Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Sleep Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 2: Global Sleep Industry Revenue Million Forecast, by Sleep Disorder 2020 & 2033

- Table 3: Global Sleep Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Global Sleep Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 5: Global Sleep Industry Revenue Million Forecast, by Sleep Disorder 2020 & 2033

- Table 6: Global Sleep Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Global Sleep Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 11: Global Sleep Industry Revenue Million Forecast, by Sleep Disorder 2020 & 2033

- Table 12: Global Sleep Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Germany Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Global Sleep Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 20: Global Sleep Industry Revenue Million Forecast, by Sleep Disorder 2020 & 2033

- Table 21: Global Sleep Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 22: China Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Japan Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 24: India Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 25: Australia Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: South Korea Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Global Sleep Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 29: Global Sleep Industry Revenue Million Forecast, by Sleep Disorder 2020 & 2033

- Table 30: Global Sleep Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 31: GCC Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: South Africa Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Global Sleep Industry Revenue Million Forecast, by Product 2020 & 2033

- Table 35: Global Sleep Industry Revenue Million Forecast, by Sleep Disorder 2020 & 2033

- Table 36: Global Sleep Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 37: Brazil Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Argentina Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Sleep Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Sleep Industry?

The projected CAGR is approximately 7.10%.

2. Which companies are prominent players in the Sleep Industry?

Key companies in the market include Natus Medical Incorporated, DeVilbiss Healthcare LLC, SleepMed, Lowenstein Medical Technology GmbH, Merck & Co Inc, Compumedics Limited, Koninklijke Philips N V, Eisai Inc, Fisher & Paykel Healthcare Limited, BMC Medical Co Ltd, Cadwell, Takeda Pharmaceutical Company Limited*List Not Exhaustive.

3. What are the main segments of the Sleep Industry?

The market segments include Product, Sleep Disorder.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Prevalence of Insomnia and Other Disorders; Increasing Adoption of Wearable Monitors and Sensors.

6. What are the notable trends driving market growth?

Insomnia Segment is Expected to Hold a Significant Market Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

Side Effects Associated With Sleep Medications.

8. Can you provide examples of recent developments in the market?

In June 2022, Sleep Habit launched a product, Sleep Reset, a digital, personalized sleep clinic. Sleep Reset utilizes clinically proven methods to uncover and address the root cause of one's sleep issues through its iPhone and Android apps.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Sleep Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Sleep Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Sleep Industry?

To stay informed about further developments, trends, and reports in the Sleep Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence