Key Insights

The titanium alloys market is experiencing robust growth, projected to maintain a Compound Annual Growth Rate (CAGR) exceeding 7% from 2025 to 2033. This expansion is fueled by increasing demand across diverse end-user industries. The aerospace sector, a significant driver, utilizes titanium alloys for lightweight yet strong aircraft components, benefiting from fuel efficiency improvements and extended aircraft lifespans. Similarly, the automotive and shipbuilding industries are adopting titanium alloys for enhanced durability and corrosion resistance in specialized applications. The chemical and power generation sectors also contribute to market growth, leveraging titanium's exceptional resistance to harsh chemicals and high temperatures. Emerging trends, such as additive manufacturing (3D printing) for titanium alloys, are further accelerating market expansion by enabling complex part designs and reducing production lead times. While the high cost of titanium and its processing remains a restraint, technological advancements and increasing demand for high-performance materials are mitigating this challenge. Market segmentation by microstructure (alpha, alpha-beta, and beta alloys) reflects the diverse properties tailored to specific applications, further influencing market dynamics. The geographical distribution shows a strong presence in North America and Europe, driven by established aerospace and industrial bases. However, Asia Pacific is expected to witness significant growth due to increasing industrialization and investments in infrastructure projects.

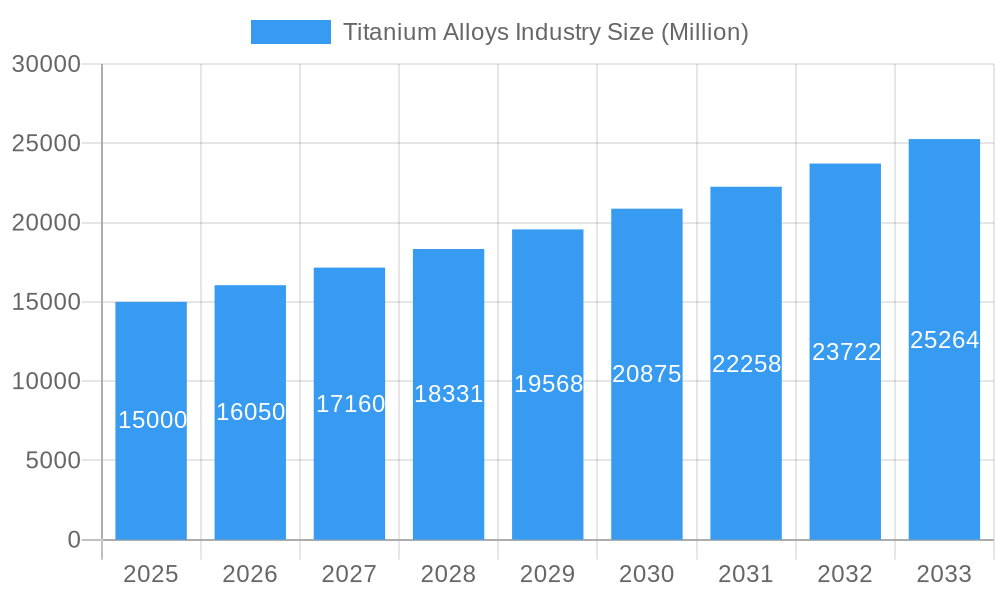

Titanium Alloys Industry Market Size (In Billion)

The competitive landscape features a mix of established global players and regional manufacturers. Major companies like VSMPO-AVISMA, ATI, and Howmet Aerospace hold significant market shares, driven by their extensive production capabilities and technological expertise. However, smaller, specialized manufacturers are also gaining traction, particularly those focusing on niche applications or advanced processing techniques. The market's future trajectory will likely depend on the continued innovation in titanium alloy production, the adoption of advanced manufacturing processes, and the growth of key end-user industries globally. Continued research and development in improving alloy properties and reducing manufacturing costs will be crucial for sustained market growth. Furthermore, sustainable manufacturing practices and the exploration of eco-friendly titanium alloy production methods are gaining importance, shaping future market dynamics.

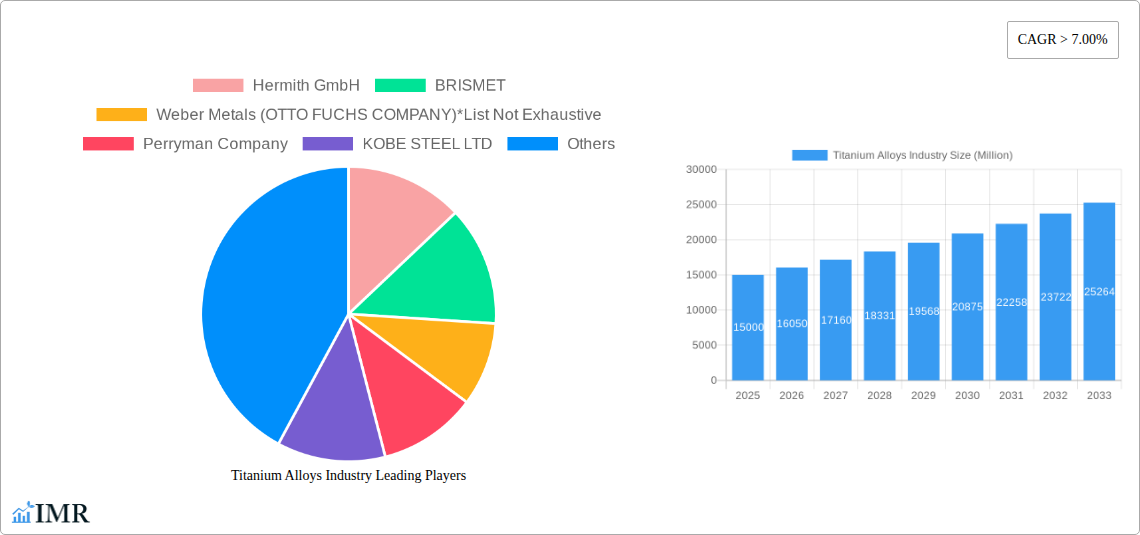

Titanium Alloys Industry Company Market Share

Titanium Alloys Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Titanium Alloys Industry, covering market dynamics, growth trends, regional dominance, product landscape, key players, and future outlook. The study period spans 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. This report is crucial for industry professionals, investors, and strategic decision-makers seeking to understand and capitalize on the opportunities within this dynamic market. The parent market is the Metals industry and the child market is the Specialty Metals market.

Titanium Alloys Industry Market Dynamics & Structure

The titanium alloys market is characterized by moderate concentration, with several key players holding significant market share. Technological innovation, particularly in materials science and manufacturing processes, is a major driver. Stringent regulatory frameworks, especially concerning aerospace and defense applications, significantly influence market dynamics. Competitive substitutes, such as aluminum alloys and composites, exert pressure on market growth. End-user demographics, primarily driven by aerospace and defense sectors, heavily impact demand. Mergers and acquisitions (M&A) activity reflects industry consolidation and efforts to expand market reach.

- Market Concentration: Moderately concentrated, with top 5 players holding xx% market share in 2024.

- Technological Innovation: Focus on lightweighting, high-strength alloys, and improved manufacturing techniques (e.g., additive manufacturing).

- Regulatory Frameworks: Stringent safety and quality standards, particularly for aerospace and medical applications.

- Competitive Substitutes: Aluminum alloys, composites, and high-strength steels pose competitive challenges.

- End-User Demographics: Aerospace remains the dominant end-user, followed by automotive and medical.

- M&A Activity: xx M&A deals recorded between 2019 and 2024, driven by market consolidation and technological access.

Titanium Alloys Industry Growth Trends & Insights

The titanium alloys market experienced steady growth between 2019 and 2024, with a CAGR of xx%. This growth is primarily attributed to increasing demand from the aerospace industry, driven by the adoption of lightweight materials for fuel efficiency and enhanced performance. Technological advancements, such as the development of advanced alloys with improved strength-to-weight ratios, have further fueled market expansion. Shifts in consumer preferences towards fuel-efficient vehicles and sustainable solutions are also impacting market adoption. Disruptions due to supply chain bottlenecks and raw material price fluctuations have created challenges, but technological innovations in recycling and alternative material sourcing are expected to mitigate these issues in the coming years. The market is predicted to grow at a CAGR of xx% from 2025 to 2033, reaching a market size of xx Million units by 2033. Market penetration in key sectors like aerospace remains high, but new applications in other sectors are expected to drive further growth.

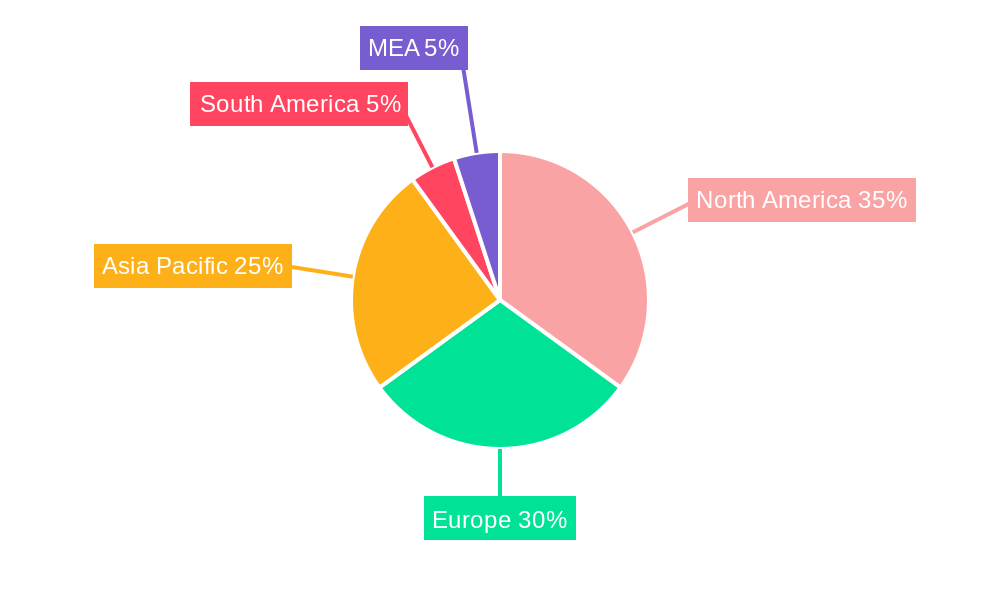

Dominant Regions, Countries, or Segments in Titanium Alloys Industry

The Aerospace segment dominates the Titanium Alloys market, accounting for approximately xx% of the total market value in 2024. North America and Europe are the leading regions, driven by robust aerospace and defense industries. Asia-Pacific is experiencing rapid growth, fueled by increasing investments in infrastructure and manufacturing.

- By End-user Industry: Aerospace (dominant, driven by lightweighting needs and high-performance requirements), followed by Automotive and Shipbuilding, Chemical, Power and Desalination, and Other End-user Industries.

- By Microstructure: Alpha and Near-alpha alloys dominate due to their excellent corrosion resistance and high strength-to-weight ratio. Alpha-beta and Beta alloys cater to niche applications requiring specific properties.

- Key Drivers: Government investments in aerospace and defense, rising demand for fuel-efficient vehicles, growing chemical processing industry, and expansion of power and desalination infrastructure are key growth drivers.

Titanium Alloys Industry Product Landscape

Titanium alloys are available in a wide range of grades and compositions, each tailored for specific applications. Product innovation focuses on enhancing mechanical properties (strength, ductility, and fatigue resistance), improving corrosion resistance, and expanding applications into new sectors. Advanced manufacturing techniques, such as additive manufacturing and precision casting, are driving the development of complex and high-performance components. Unique selling propositions include high strength-to-weight ratios, superior corrosion resistance, and biocompatibility.

Key Drivers, Barriers & Challenges in Titanium Alloys Industry

Key Drivers:

- Increasing demand from the aerospace industry for lightweight materials.

- Growing adoption of titanium alloys in the automotive and medical sectors.

- Technological advancements leading to improved material properties and manufacturing processes.

- Government investments in research and development of new titanium alloys.

Challenges:

- High production costs and limited availability of raw materials.

- Volatility in raw material prices impacting profitability.

- Stringent regulatory requirements for specific applications.

- Competition from alternative materials such as aluminum alloys and composites.

Emerging Opportunities in Titanium Alloys Industry

Emerging opportunities include:

- Expanding applications in the biomedical industry (implants and prosthetics).

- Growth in the additive manufacturing sector for customized components.

- Development of advanced alloys with enhanced properties.

- Exploration of new applications in the energy and infrastructure sectors.

Growth Accelerators in the Titanium Alloys Industry

Long-term growth will be fueled by continued advancements in materials science, leading to lighter, stronger, and more corrosion-resistant alloys. Strategic partnerships between manufacturers and end-users will accelerate the adoption of titanium alloys in new applications. Market expansion into developing economies will also contribute to sustained growth.

Key Players Shaping the Titanium Alloys Industry Market

- Hermith GmbH

- BRISMET

- Weber Metals (OTTO FUCHS COMPANY)

- Perryman Company

- KOBE STEEL LTD

- ATI

- Daido Steel Co Ltd

- Toho Titanium Co Ltd

- VSMPO-AVISMA Corporation

- Howmet Aerospace

- CRS Holdings LLC

- Eramet

- M/s Bansal Brothers

- AMG Advanced Metallurgical Group N V

- Mishra Dhatu Nigam Limited

- TIMET (Precision Castparts Corp )

Notable Milestones in Titanium Alloys Industry Sector

- November 2022: PTC Industries and Mishra Dhatu Nigam (MIDHANI) signed an MOU for technological collaboration in titanium alloy manufacturing for defense and aerospace.

- July 2022: Perryman Company announced plans to significantly expand its titanium melting capacity by 16 million pounds, strengthening its position in the global market.

In-Depth Titanium Alloys Industry Market Outlook

The titanium alloys market is poised for robust growth, driven by ongoing technological advancements, increasing demand from key sectors, and expansion into new applications. Strategic investments in research and development, along with collaborations across the value chain, will unlock significant opportunities for market participants. The market is expected to witness a substantial increase in market size, driven by the expansion of the aerospace and defense sectors, particularly in regions like Asia-Pacific. Companies focusing on innovation, sustainable manufacturing practices, and supply chain resilience will be best positioned to capitalize on future growth prospects.

Titanium Alloys Industry Segmentation

-

1. Microstructure

- 1.1. Alpha and Near-alpha Alloy

- 1.2. Alpha-beta Alloy

- 1.3. Beta Alloy

-

2. End-user Industry

- 2.1. Aerospace

- 2.2. Automotive and Shipbuilding

- 2.3. Chemical

- 2.4. Power and Desalination

- 2.5. Other End-user Industries

Titanium Alloys Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. Italy

- 3.4. France

- 3.5. Rest of Europe

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Titanium Alloys Industry Regional Market Share

Geographic Coverage of Titanium Alloys Industry

Titanium Alloys Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Microstructure

- 5.1.1. Alpha and Near-alpha Alloy

- 5.1.2. Alpha-beta Alloy

- 5.1.3. Beta Alloy

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Aerospace

- 5.2.2. Automotive and Shipbuilding

- 5.2.3. Chemical

- 5.2.4. Power and Desalination

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Microstructure

- 6. Global Titanium Alloys Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Microstructure

- 6.1.1. Alpha and Near-alpha Alloy

- 6.1.2. Alpha-beta Alloy

- 6.1.3. Beta Alloy

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. Aerospace

- 6.2.2. Automotive and Shipbuilding

- 6.2.3. Chemical

- 6.2.4. Power and Desalination

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Microstructure

- 7. Asia Pacific Titanium Alloys Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Microstructure

- 7.1.1. Alpha and Near-alpha Alloy

- 7.1.2. Alpha-beta Alloy

- 7.1.3. Beta Alloy

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. Aerospace

- 7.2.2. Automotive and Shipbuilding

- 7.2.3. Chemical

- 7.2.4. Power and Desalination

- 7.2.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Microstructure

- 8. North America Titanium Alloys Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Microstructure

- 8.1.1. Alpha and Near-alpha Alloy

- 8.1.2. Alpha-beta Alloy

- 8.1.3. Beta Alloy

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. Aerospace

- 8.2.2. Automotive and Shipbuilding

- 8.2.3. Chemical

- 8.2.4. Power and Desalination

- 8.2.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Microstructure

- 9. Europe Titanium Alloys Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Microstructure

- 9.1.1. Alpha and Near-alpha Alloy

- 9.1.2. Alpha-beta Alloy

- 9.1.3. Beta Alloy

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. Aerospace

- 9.2.2. Automotive and Shipbuilding

- 9.2.3. Chemical

- 9.2.4. Power and Desalination

- 9.2.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Microstructure

- 10. Rest of the World Titanium Alloys Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Microstructure

- 10.1.1. Alpha and Near-alpha Alloy

- 10.1.2. Alpha-beta Alloy

- 10.1.3. Beta Alloy

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. Aerospace

- 10.2.2. Automotive and Shipbuilding

- 10.2.3. Chemical

- 10.2.4. Power and Desalination

- 10.2.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Microstructure

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Hermith GmbH

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 BRISMET

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Weber Metals (OTTO FUCHS COMPANY)*List Not Exhaustive

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Perryman Company

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 KOBE STEEL LTD

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 ATI

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Daido Steel Co Ltd

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Toho Titanium Co Ltd

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 VSMPO-AVISMA Corporation

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Howmet Aerospace

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 CRS Holdings LLC

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Eramet

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.13 M/s Bansal Brothers

- 11.1.13.1. Company Overview

- 11.1.13.2. Products

- 11.1.13.3. Company Financials

- 11.1.13.4. SWOT Analysis

- 11.1.14 AMG Advanced Metallurgical Group N V

- 11.1.14.1. Company Overview

- 11.1.14.2. Products

- 11.1.14.3. Company Financials

- 11.1.14.4. SWOT Analysis

- 11.1.15 Mishra Dhatu Nigam Limited

- 11.1.15.1. Company Overview

- 11.1.15.2. Products

- 11.1.15.3. Company Financials

- 11.1.15.4. SWOT Analysis

- 11.1.16 TIMET (Precision Castparts Corp )

- 11.1.16.1. Company Overview

- 11.1.16.2. Products

- 11.1.16.3. Company Financials

- 11.1.16.4. SWOT Analysis

- 11.1.1 Hermith GmbH

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Titanium Alloys Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Titanium Alloys Industry Revenue (billion), by Microstructure 2025 & 2033

- Figure 3: Asia Pacific Titanium Alloys Industry Revenue Share (%), by Microstructure 2025 & 2033

- Figure 4: Asia Pacific Titanium Alloys Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 5: Asia Pacific Titanium Alloys Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 6: Asia Pacific Titanium Alloys Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific Titanium Alloys Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Titanium Alloys Industry Revenue (billion), by Microstructure 2025 & 2033

- Figure 9: North America Titanium Alloys Industry Revenue Share (%), by Microstructure 2025 & 2033

- Figure 10: North America Titanium Alloys Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: North America Titanium Alloys Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: North America Titanium Alloys Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: North America Titanium Alloys Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Titanium Alloys Industry Revenue (billion), by Microstructure 2025 & 2033

- Figure 15: Europe Titanium Alloys Industry Revenue Share (%), by Microstructure 2025 & 2033

- Figure 16: Europe Titanium Alloys Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 17: Europe Titanium Alloys Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 18: Europe Titanium Alloys Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Titanium Alloys Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Titanium Alloys Industry Revenue (billion), by Microstructure 2025 & 2033

- Figure 21: Rest of the World Titanium Alloys Industry Revenue Share (%), by Microstructure 2025 & 2033

- Figure 22: Rest of the World Titanium Alloys Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 23: Rest of the World Titanium Alloys Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 24: Rest of the World Titanium Alloys Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the World Titanium Alloys Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Titanium Alloys Industry Revenue billion Forecast, by Microstructure 2020 & 2033

- Table 2: Global Titanium Alloys Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 3: Global Titanium Alloys Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Titanium Alloys Industry Revenue billion Forecast, by Microstructure 2020 & 2033

- Table 5: Global Titanium Alloys Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 6: Global Titanium Alloys Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: China Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: India Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Japan Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: South Korea Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Global Titanium Alloys Industry Revenue billion Forecast, by Microstructure 2020 & 2033

- Table 13: Global Titanium Alloys Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 14: Global Titanium Alloys Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United States Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Mexico Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Global Titanium Alloys Industry Revenue billion Forecast, by Microstructure 2020 & 2033

- Table 19: Global Titanium Alloys Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 20: Global Titanium Alloys Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 21: Germany Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Italy Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: France Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Rest of Europe Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Global Titanium Alloys Industry Revenue billion Forecast, by Microstructure 2020 & 2033

- Table 27: Global Titanium Alloys Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 28: Global Titanium Alloys Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: South America Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Middle East and Africa Titanium Alloys Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Titanium Alloys Industry?

The projected CAGR is approximately 7.1%.

2. Which companies are prominent players in the Titanium Alloys Industry?

Key companies in the market include Hermith GmbH, BRISMET, Weber Metals (OTTO FUCHS COMPANY)*List Not Exhaustive, Perryman Company, KOBE STEEL LTD, ATI, Daido Steel Co Ltd, Toho Titanium Co Ltd, VSMPO-AVISMA Corporation, Howmet Aerospace, CRS Holdings LLC, Eramet, M/s Bansal Brothers, AMG Advanced Metallurgical Group N V, Mishra Dhatu Nigam Limited, TIMET (Precision Castparts Corp ).

3. What are the main segments of the Titanium Alloys Industry?

The market segments include Microstructure, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 30.34 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Usage of Titanium Alloys in the Aerospace Sector; Increasing Demand for Titanium Alloys for Combat Vehicles to Replace Steel and Aluminum.

6. What are the notable trends driving market growth?

Increasing Demand of Titanium Alloys in the Aerospace Industry.

7. Are there any restraints impacting market growth?

High Reactivity of Alloy Demands Specialized Care During Production; Other Restraints.

8. Can you provide examples of recent developments in the market?

In November 2022, PTC Industries and Defence PSU Mishra Dhatu Nigam (MIDHANI) signed a memorandum of understanding (MOU) for a technological partnership. In accordance with their MOU, PTC Industries and Midhani will make use of each other's technological resources to manufacture titanium alloy pipes and tubes using locally processed raw materials; manufacture titanium alloy plates and sheets; and fabricate critical parts and LRUs for the defense and aerospace industries using PTC's advanced machining facility and Midhani's forged and rolled products.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Titanium Alloys Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Titanium Alloys Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Titanium Alloys Industry?

To stay informed about further developments, trends, and reports in the Titanium Alloys Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence