Key Insights

The United Kingdom white cement market, a segment of the broader global industry valued at $798.55 million in 2025, is experiencing steady growth fueled by several key factors. The 4.41% Compound Annual Growth Rate (CAGR) suggests a positive outlook, primarily driven by increasing infrastructure development projects, particularly within the residential and non-residential construction sectors. Government initiatives promoting sustainable building practices and the rising demand for high-performance cement in specialized applications are further contributing to market expansion. While precise UK market size data is unavailable, considering the global market value and the UK’s significant construction industry, a reasonable estimate for the UK white cement market size in 2025 would be in the range of £50- £100 million (assuming a market share proportional to the UK's contribution to European construction). Major players like Aggregate Industries (Holcim Group), CRH, Breedon Group plc, and Hanson are actively shaping the market dynamics through strategic investments in production capacity and innovative product offerings. However, potential restraints include fluctuating raw material prices, environmental regulations impacting production processes, and economic uncertainties affecting construction activity. The market segmentation reveals a substantial demand across residential and non-residential applications, with Type I and Type III white cements likely dominating market share due to their specific properties. Future growth will likely be influenced by technological advancements, focusing on sustainable and high-performance cement varieties, along with effective supply chain management to mitigate potential disruptions.

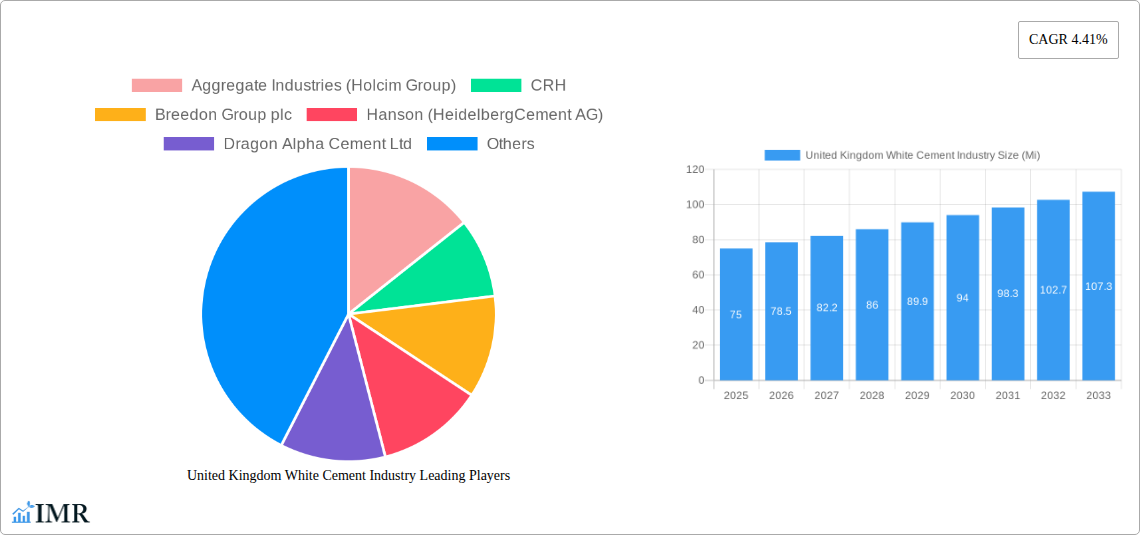

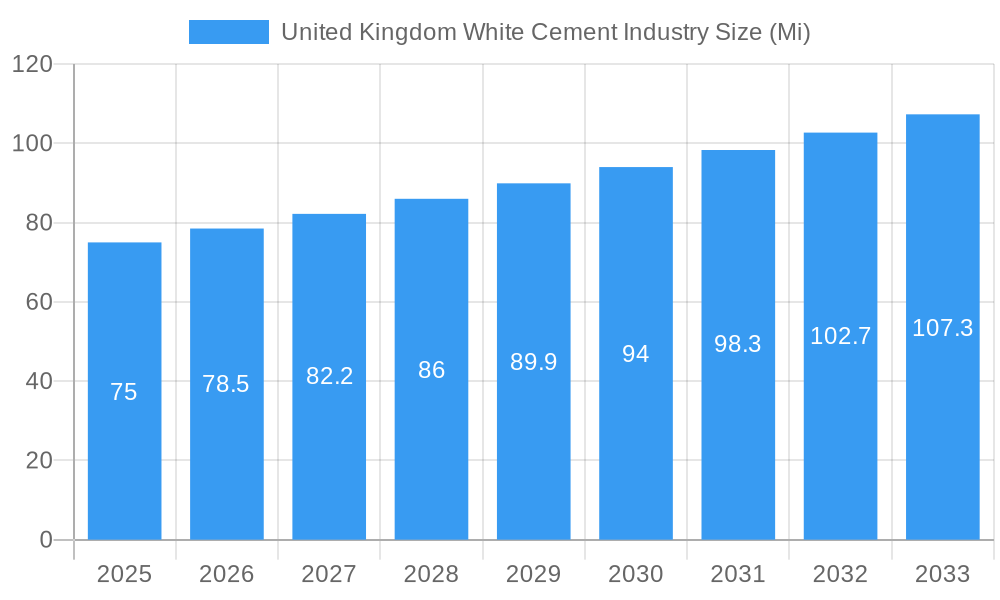

United Kingdom White Cement Industry Market Size (In Million)

The competitive landscape is characterized by both established multinational corporations and regional players. This leads to a dynamic market with varying pricing strategies, product portfolios, and geographical reach. The geographic distribution of the market within the UK will reflect the distribution of construction projects, with regions experiencing significant infrastructure developments showing higher demand. Furthermore, the industry's future trajectory is intricately linked to national construction policies and the broader economic climate. Understanding these interdependencies will be crucial for stakeholders in strategic planning and informed decision-making. While specific regional breakdowns within the UK are not provided, regional variations likely exist, reflecting variations in construction activity and infrastructure investments across the country.

United Kingdom White Cement Industry Company Market Share

United Kingdom White Cement Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the United Kingdom white cement industry, offering invaluable insights for industry professionals, investors, and strategic decision-makers. Covering the period 2019-2033, with a focus on 2025, this report meticulously examines market dynamics, growth trends, key players, and future opportunities within the UK white cement sector. The report segments the market by type (Type I, Type III, Other Types) and application (Residential, Non-Residential), providing a granular view of market performance across various segments. The Mi unit is used for all value representation throughout the report.

United Kingdom White Cement Industry Market Dynamics & Structure

This section analyzes the competitive landscape, technological advancements, regulatory environment, and market trends within the UK white cement industry. The market exhibits a moderately concentrated structure, with key players holding significant market share. Technological innovation is driven by the need for sustainable and high-performance products. Stringent environmental regulations are shaping industry practices, prompting companies to adopt eco-friendly manufacturing processes.

- Market Concentration: xx% market share held by the top 5 players (Aggregate Industries, CRH, Breedon Group, Hanson, Cemex).

- Technological Innovation: Focus on reducing carbon footprint, improving durability, and developing specialized white cements for niche applications.

- Regulatory Framework: Compliance with EU and UK environmental standards is crucial, influencing production methods and product specifications.

- Competitive Substitutes: Other cementitious materials and alternative construction solutions present competitive pressure.

- M&A Trends: The acquisition of Tarmac by CRH in 2019 exemplifies significant consolidation within the industry. xx M&A deals recorded between 2019-2024.

- End-User Demographics: Growth is driven by both residential and non-residential construction activities, with infrastructure projects playing a significant role.

United Kingdom White Cement Industry Growth Trends & Insights

The UK white cement market demonstrates consistent growth, driven by robust construction activity and increasing demand for aesthetically pleasing building materials. The market size experienced a CAGR of xx% during the historical period (2019-2024) and is projected to maintain a CAGR of xx% during the forecast period (2025-2033). Market penetration for white cement in specific applications (e.g., architectural facades) is increasing steadily. Technological disruptions, such as the introduction of eco-friendly white cement variants, are reshaping market dynamics. Consumer preference for sustainable and high-quality materials further fuels growth. By 2033, the market size is estimated to reach xx Mi units.

Dominant Regions, Countries, or Segments in United Kingdom White Cement Industry

The South East of England demonstrates the highest market share for white cement consumption, followed by the North West and London. This is primarily due to higher construction activity and a greater concentration of large-scale projects in these regions. Within the product segments, Type I white cement holds the largest market share due to its versatility and wide range of applications. The non-residential segment shows higher growth potential due to ongoing infrastructure development.

- Key Drivers for South East England: High construction activity, significant infrastructure development, and a concentration of large-scale projects.

- Key Drivers for Type I Cement: Versatility and suitability for diverse applications.

- Key Drivers for Non-Residential Segment: Infrastructure projects, commercial building construction, and industrial development.

United Kingdom White Cement Industry Product Landscape

The UK white cement market offers a range of products catering to diverse applications. Innovations focus on enhancing durability, strength, and aesthetic appeal. Eco-friendly options, utilizing recycled materials and reducing carbon emissions, are gaining traction. Key performance indicators include compressive strength, water demand, and setting time. Unique selling propositions often focus on superior whiteness, fineness, and ease of use. The launch of eco-friendly white cement by Hanson in 2021 showcases the ongoing innovation within the sector.

Key Drivers, Barriers & Challenges in United Kingdom White Cement Industry

Key Drivers: Increasing construction activity, particularly in infrastructure and residential sectors; growing demand for aesthetically superior building materials; technological advancements leading to improved product performance; government initiatives promoting sustainable construction practices.

Key Barriers & Challenges: Fluctuations in raw material prices; environmental regulations impacting production costs; competition from alternative building materials; supply chain disruptions; potential economic downturns affecting construction activity. xx% increase in raw material costs between 2021 and 2024 negatively impacted profit margins.

Emerging Opportunities in United Kingdom White Cement Industry

Emerging opportunities lie in the growing demand for sustainable and high-performance white cement. There is potential for expansion into niche applications, such as precast concrete elements and specialized architectural designs. The development of new product formulations with enhanced properties and reduced environmental impact offers significant growth potential. Tapping into the rising demand for green building materials presents a major opportunity for market expansion.

Growth Accelerators in the United Kingdom White Cement Industry Industry

Long-term growth will be driven by technological innovations leading to more sustainable and higher-performing white cements. Strategic partnerships between cement producers and construction companies can unlock new market segments. Government policies promoting sustainable infrastructure development will further stimulate market growth. Expansion into export markets presents additional opportunities for growth.

Key Players Shaping the United Kingdom White Cement Industry Market

- Aggregate Industries (Holcim Group) [www.aggregate.com]

- CRH [www.crh.com]

- Breedon Group plc [www.breedongroup.com]

- Hanson (HeidelbergCement AG) [www.heidelbergcement.com]

- Dragon Alpha Cement Ltd

- Cemex S A B de C V [www.cemex.com]

- Southern Cement Limited (CRH Company)

- Cementir Holding N V [www.cemtir.com]

- Saint-Gobain [www.saint-gobain.com]

- Holcim Group [www.holcim.com]

- Tarmac [www.tarmac.com]

Notable Milestones in United Kingdom White Cement Industry Sector

- 2019: Acquisition of Tarmac by CRH.

- 2021: Launch of eco-friendly white cement products by Hanson.

In-Depth United Kingdom White Cement Industry Market Outlook

The UK white cement industry is poised for continued growth, driven by sustained demand from construction and infrastructure projects. Strategic investments in sustainable technologies and innovative product development will be crucial for maintaining competitiveness. Opportunities exist in expanding into niche applications and exploring export markets. The market is projected to exhibit robust growth, with significant potential for industry players who successfully adapt to evolving market dynamics and consumer preferences.

United Kingdom White Cement Industry Segmentation

-

1. Type

- 1.1. Type I

- 1.2. Type III

- 1.3. Other Types

-

2. Application

- 2.1. Residential

-

2.2. Non-residential

- 2.2.1. Commercial

- 2.2.2. Infrastructure

- 2.2.3. Industrial/Institutional

United Kingdom White Cement Industry Segmentation By Geography

- 1. United Kingdom

United Kingdom White Cement Industry Regional Market Share

Geographic Coverage of United Kingdom White Cement Industry

United Kingdom White Cement Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.41% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Type I

- 5.1.2. Type III

- 5.1.3. Other Types

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Residential

- 5.2.2. Non-residential

- 5.2.2.1. Commercial

- 5.2.2.2. Infrastructure

- 5.2.2.3. Industrial/Institutional

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United Kingdom

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United Kingdom White Cement Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Type I

- 6.1.2. Type III

- 6.1.3. Other Types

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Residential

- 6.2.2. Non-residential

- 6.2.2.1. Commercial

- 6.2.2.2. Infrastructure

- 6.2.2.3. Industrial/Institutional

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Aggregate Industries (Holcim Group)

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 CRH

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Breedon Group plc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hanson (HeidelbergCement AG)

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Dragon Alpha Cement Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Cemex S A B de C V

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Southern Cement Limited (CRH Company)*List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Cementir Holding N V

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Saint-Gobain

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Holcim Group

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Tarmac

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 Aggregate Industries (Holcim Group)

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United Kingdom White Cement Industry Revenue Breakdown (Mi, %) by Product 2025 & 2033

- Figure 2: United Kingdom White Cement Industry Share (%) by Company 2025

List of Tables

- Table 1: United Kingdom White Cement Industry Revenue Mi Forecast, by Type 2020 & 2033

- Table 2: United Kingdom White Cement Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 3: United Kingdom White Cement Industry Revenue Mi Forecast, by Application 2020 & 2033

- Table 4: United Kingdom White Cement Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 5: United Kingdom White Cement Industry Revenue Mi Forecast, by Region 2020 & 2033

- Table 6: United Kingdom White Cement Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: United Kingdom White Cement Industry Revenue Mi Forecast, by Type 2020 & 2033

- Table 8: United Kingdom White Cement Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 9: United Kingdom White Cement Industry Revenue Mi Forecast, by Application 2020 & 2033

- Table 10: United Kingdom White Cement Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 11: United Kingdom White Cement Industry Revenue Mi Forecast, by Country 2020 & 2033

- Table 12: United Kingdom White Cement Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United Kingdom White Cement Industry?

The projected CAGR is approximately 4.41%.

2. Which companies are prominent players in the United Kingdom White Cement Industry?

Key companies in the market include Aggregate Industries (Holcim Group), CRH, Breedon Group plc, Hanson (HeidelbergCement AG), Dragon Alpha Cement Ltd, Cemex S A B de C V, Southern Cement Limited (CRH Company)*List Not Exhaustive, Cementir Holding N V, Saint-Gobain , Holcim Group , Tarmac.

3. What are the main segments of the United Kingdom White Cement Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 798.55 Mi as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand from the Construction Industry; Substitution of Grey Cement due to White Cement's Superior Properties; Other Drivers.

6. What are the notable trends driving market growth?

Type I Cement to Dominate.

7. Are there any restraints impacting market growth?

High Production Cost; Other Restraints.

8. Can you provide examples of recent developments in the market?

Acquisition of Tarmac by CRH in 2019

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Mi and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United Kingdom White Cement Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United Kingdom White Cement Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United Kingdom White Cement Industry?

To stay informed about further developments, trends, and reports in the United Kingdom White Cement Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence