Key Insights

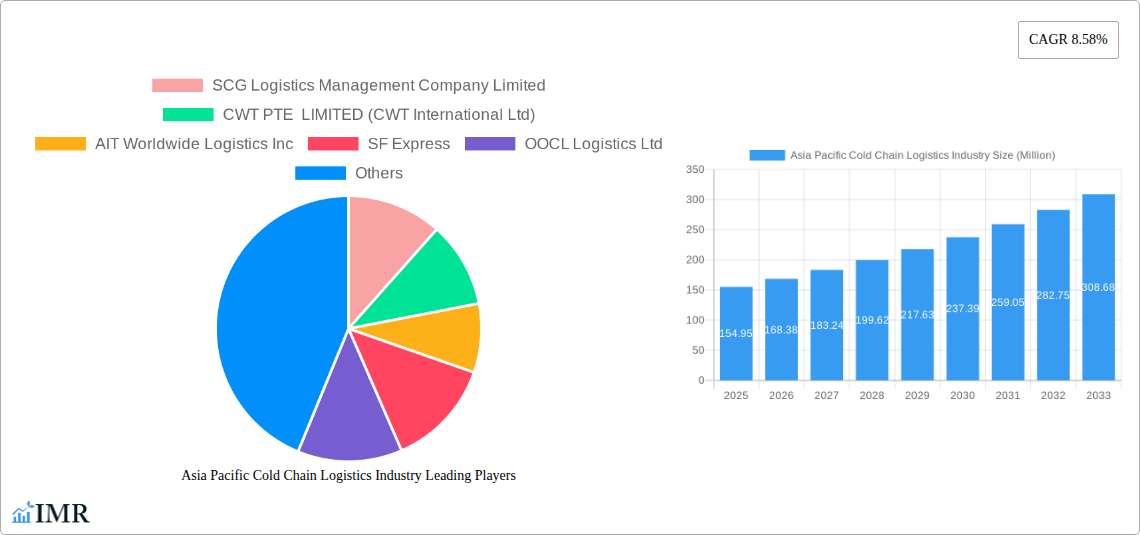

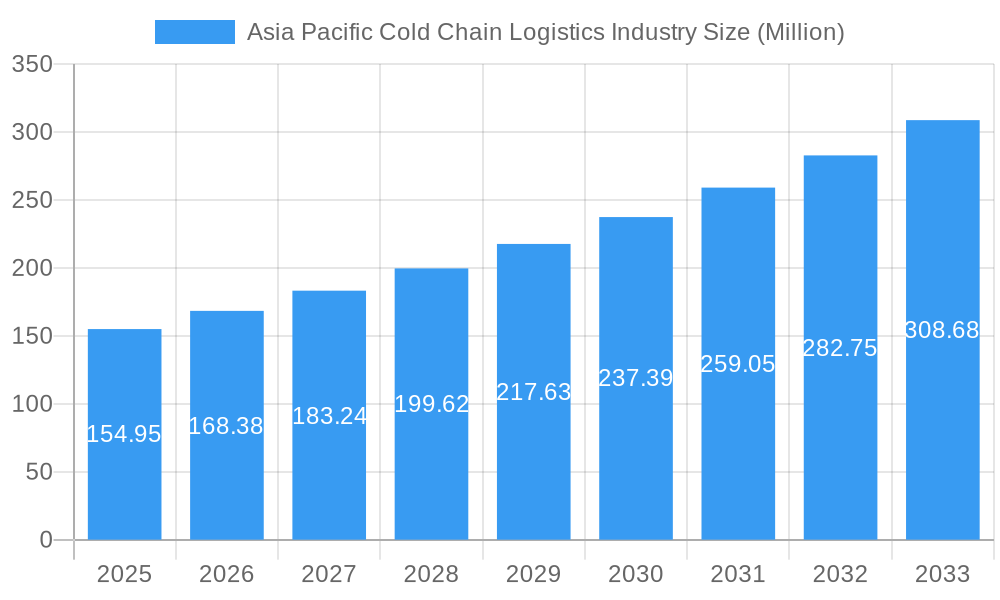

The Asia-Pacific cold chain logistics market, valued at $154.95 million in 2025, is experiencing robust growth, projected to expand at a compound annual growth rate (CAGR) of 8.58% from 2025 to 2033. This significant expansion is driven by several key factors. The rising demand for fresh produce, processed foods, pharmaceuticals, and other temperature-sensitive goods across rapidly developing economies fuels the need for efficient and reliable cold chain solutions. Increased consumer disposable incomes, coupled with a shift towards convenient and healthier lifestyles, are driving consumption of perishable goods, further bolstering market growth. Technological advancements, including the adoption of sophisticated temperature monitoring systems, real-time tracking, and improved logistics management software, are enhancing efficiency and reducing losses within the cold chain. Furthermore, increasing investments in cold storage infrastructure, particularly in emerging markets like India and Southeast Asia, are creating opportunities for market expansion. Government initiatives promoting food safety and reducing post-harvest losses are also contributing positively to market growth.

Asia Pacific Cold Chain Logistics Industry Market Size (In Million)

However, the market faces certain challenges. Maintaining consistent cold chain integrity across diverse geographical regions with varying infrastructure can be complex and costly. Fluctuations in fuel prices and the stringent regulatory requirements for handling temperature-sensitive goods add to the operational complexities. Moreover, ensuring skilled labor and specialized equipment across the entire cold chain network remains a crucial consideration. Despite these hurdles, the long-term outlook for the Asia-Pacific cold chain logistics market remains positive, fueled by sustained economic growth, evolving consumer preferences, and continuous technological innovation. Key players in the market, including SCG Logistics, CWT, and others are strategically positioning themselves to capitalize on these emerging opportunities. The expanding middle class in countries like China and India presents a particularly significant growth driver for the sector in the coming years.

Asia Pacific Cold Chain Logistics Industry Company Market Share

Asia Pacific Cold Chain Logistics Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the Asia Pacific cold chain logistics industry, covering market dynamics, growth trends, key players, and future outlook. The study period spans from 2019 to 2033, with 2025 serving as the base and estimated year. This report is crucial for businesses, investors, and policymakers seeking a comprehensive understanding of this dynamic sector. The report analyzes the market across various segments, including services (storage, transportation, value-added services), temperature types (chilled, frozen), applications (horticulture, dairy, meats, pharmaceuticals, etc.), and countries across the Asia-Pacific region.

Keywords: Asia Pacific cold chain logistics, cold chain market, refrigerated transportation, temperature-controlled logistics, food logistics, pharmaceutical logistics, China cold chain, India cold chain, Japan cold chain, South Korea cold chain, cold storage, value-added services, SCG Logistics, CWT, AIT Worldwide Logistics, SF Express, OOCL Logistics, CJ Rokin Logistics, Nichirei Logistics Group, UPS, X2 Logistics, JWD Infologistics.

Asia Pacific Cold Chain Logistics Industry Market Dynamics & Structure

The Asia-Pacific cold chain logistics industry is a dynamic and evolving sector, characterized by increasing demand, technological innovation, and a complex regulatory landscape. The market exhibits a moderately concentrated structure, with established large players holding significant market share, alongside a growing number of agile companies catering to specific niche segments and emerging markets. This dynamic interplay influences pricing, service offerings, and the pace of technological adoption.

Market Concentration: In 2025, the top 5 players, including SCG Logistics, CWT, AIT Worldwide Logistics, SF Express, and OOCL Logistics, are projected to collectively command approximately [Insert % Here] of the market share. The remaining portion is fragmented among a multitude of smaller, specialized providers and regional operators.

Technological Innovation: The industry is witnessing a rapid integration of cutting-edge technologies. IoT-enabled monitoring systems provide real-time visibility and control over temperature and humidity, while AI-powered route optimization enhances delivery efficiency and reduces transit times. Automated warehousing solutions are streamlining operations, minimizing human error, and increasing throughput. However, the substantial initial investment and the complexities of integrating these advanced systems continue to present challenges, particularly for smaller enterprises seeking to scale their operations.

Regulatory Frameworks: Stringent and evolving regulations governing food safety, pharmaceutical handling, and biosecurity are significant drivers in the cold chain sector. These regulations, while increasing operational complexity and costs for compliance, also create substantial opportunities for specialized cold chain providers with the expertise and infrastructure to meet these demanding standards. Adherence to these guidelines is paramount for market entry and sustained success.

Competitive Product Substitutes: While direct substitutes for dedicated cold chain logistics are limited, advancements in traditional transportation methods, such as improved refrigeration units in standard trucks, and the development of innovative thermal packaging technologies can offer some competitive pressure. However, these are generally not suitable for the stringent temperature control required for high-value perishables and pharmaceuticals.

End-User Demographics: The burgeoning middle class in Asia-Pacific, characterized by increasing urbanization and rising disposable incomes, is significantly influencing demand. Changing consumer preferences towards convenience, fresh produce, processed foods, and ready-to-eat meals are directly fueling the need for robust and efficient cold chain solutions to maintain product quality and safety from farm to table.

M&A Trends: The period between 2019 and 2024 saw a notable surge in Mergers & Acquisitions within the Asia-Pacific cold chain logistics sector, with deal volume increasing by approximately [Insert % Here]. This consolidation activity is largely attributed to strategic efforts by major players to expand their geographic reach, enhance their service portfolios, and achieve economies of scale. The average deal value during this period hovered around [Insert Value Here] million, reflecting the growing strategic importance and investment in this sector.

Asia Pacific Cold Chain Logistics Industry Growth Trends & Insights

The Asia Pacific cold chain logistics market is experiencing robust growth, driven by rising demand for temperature-sensitive goods across various sectors. The market size was valued at xx million in 2024 and is projected to reach xx million in 2033, exhibiting a CAGR of xx% during the forecast period (2025-2033).

This expansion is fueled by several factors, including rising disposable incomes, expanding middle-class populations, increased consumer preference for fresh and processed foods, and stringent regulations related to food safety and pharmaceutical handling. Technological disruptions, particularly the implementation of IoT-enabled monitoring and automation solutions, are significantly enhancing efficiency and reducing operational costs. The adoption rate of advanced technologies is gradually increasing, with higher penetration expected in developed economies compared to developing ones.

Dominant Regions, Countries, or Segments in Asia Pacific Cold Chain Logistics Industry

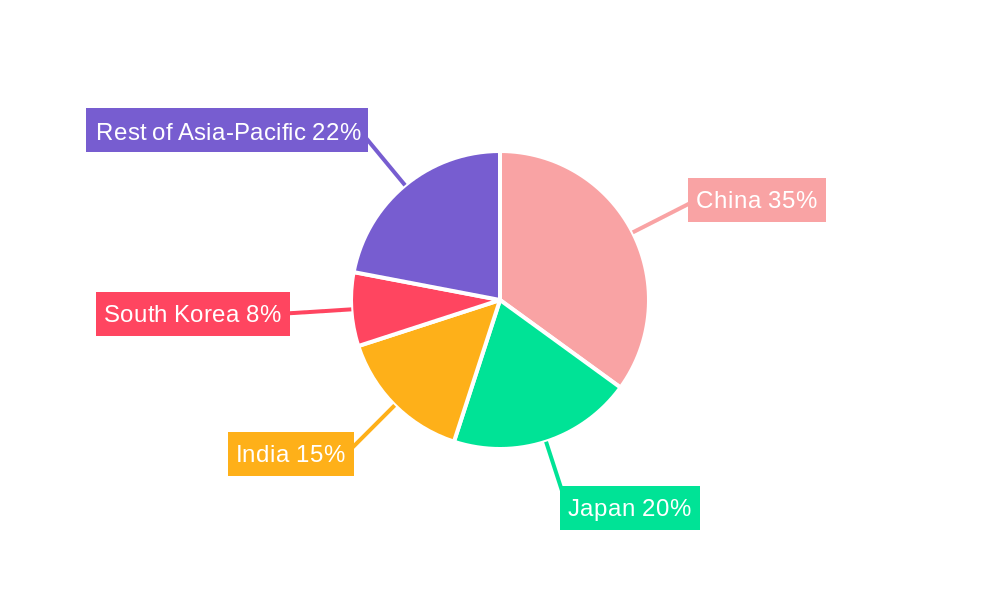

China, India, and Japan dominate the Asia-Pacific cold chain logistics market, driven by substantial growth in their respective food and pharmaceutical sectors. However, other countries, such as South Korea, Indonesia, and Thailand, are exhibiting rapid growth potential.

By Services: Transportation currently holds the largest market share, followed by storage and value-added services. The value-added services segment is experiencing the fastest growth due to the increasing demand for specialized handling and processing of temperature-sensitive products.

By Temperature Type: The frozen segment holds the larger market share, driven by the high demand for frozen food products. The chilled segment is also witnessing significant growth due to increased consumption of fresh produce and dairy products.

By Application: The food and beverage segment holds the major market share. However, the pharmaceutical and life sciences segment is experiencing the fastest growth rate, driven by the increasing demand for temperature-sensitive drugs and vaccines.

- Key Drivers (China): Rapid economic growth, expanding middle class, rising urbanization, and significant investments in cold chain infrastructure.

- Key Drivers (India): Increasing per capita income, improving cold chain infrastructure, and the government's initiatives to promote food processing and export.

- Key Drivers (Japan): High consumer demand for fresh and processed food, advanced cold chain technologies, and efficient logistics networks.

- Key Drivers (South Korea): High disposable income, strong regulatory framework for food safety, and technological innovations in cold chain management.

Asia Pacific Cold Chain Logistics Industry Product Landscape

Product innovations in the Asia-Pacific cold chain logistics industry primarily focus on improving temperature control, tracking, and monitoring capabilities. Advancements include smart containers with IoT sensors, GPS tracking, and automated temperature control systems, leading to enhanced efficiency, reduced spoilage, and improved supply chain visibility. Unique selling propositions include tailored solutions for specific product types (e.g., pharmaceuticals), real-time monitoring dashboards, and comprehensive data analytics for supply chain optimization.

Key Drivers, Barriers & Challenges in Asia Pacific Cold Chain Logistics Industry

Key Drivers: Growing demand for fresh and processed foods, rising disposable incomes, stringent regulatory requirements, and advancements in cold chain technologies are the primary drivers. Specific examples include the expansion of e-commerce platforms for grocery delivery and government initiatives to enhance food security.

Key Challenges: Inadequate cold chain infrastructure in certain regions, particularly in rural areas, creates significant challenges, impacting transportation costs and product quality. Regulatory complexities and variations across different countries increase compliance costs and operational difficulties. Intense competition and fluctuating fuel prices are also considerable challenges. For instance, inadequate reefer container availability contributes to delays and increased costs. The lack of skilled labor further hampers industry growth.

Emerging Opportunities in Asia Pacific Cold Chain Logistics Industry

The burgeoning e-commerce landscape, particularly the significant growth in online grocery shopping and same-day delivery services, presents a wealth of opportunities for cold chain logistics providers. Developing bespoke, end-to-end solutions tailored for last-mile delivery in urban and suburban areas, ensuring the integrity of temperature-sensitive goods throughout the entire journey, is a key area for growth. Furthermore, the escalating demand for specialized cold chain services, especially for the secure and compliant transportation of pharmaceuticals, including vaccines and biologics, represents a largely untapped market potential. The increasing global emphasis on sustainability is also creating significant opportunities for innovation. The adoption of eco-friendly refrigerants, energy-efficient storage facilities, and optimized transportation networks powered by renewable energy sources are not only responding to regulatory pressures but also opening avenues for differentiation and enhanced brand value.

Growth Accelerators in the Asia Pacific Cold Chain Logistics Industry Industry

The relentless pace of technological advancement is a primary catalyst for growth. The integration of Artificial Intelligence (AI) and Machine Learning (ML) is revolutionizing operations through predictive maintenance of refrigeration equipment, real-time demand forecasting, and dynamic route optimization that accounts for traffic, weather, and delivery windows. Strategic alliances between established cold chain logistics providers and innovative technology companies are fostering rapid advancements in sophisticated monitoring and tracking systems, providing unprecedented visibility and control. Moreover, aggressive expansion into underserved emerging markets within the Asia-Pacific region, coupled with the development of highly specialized solutions for niche applications like the critical transportation of organs for transplantation and temperature-sensitive vaccines, will significantly accelerate industry growth.

Key Players Shaping the Asia Pacific Cold Chain Logistics Industry Market

- SCG Logistics Management Company Limited

- CWT PTE LIMITED (CWT International Ltd)

- AIT Worldwide Logistics Inc

- SF Express

- OOCL Logistics Ltd

- CJ Rokin Logistics

- Nichirei Logistics Group Inc

- United Parcel Service of America

- X2 Logistics Network (X2 GROUP)

- JWD Infologistics Public Company Ltd

Notable Milestones in Asia Pacific Cold Chain Logistics Industry Sector

- October 2022: UPS significantly enhanced its global cold chain capabilities by expanding its Premier service, specifically designed for time- and temperature-sensitive shipments, to include key markets in Thailand and Singapore, bolstering its presence in the critical Asia-Pacific region.

- September 2022: A pivotal collaboration was formed between SCG Logistics, DENSO Sales (Thailand), and Toyota Tsusho Thailand. This strategic partnership aims to elevate Thailand's refrigeration ecosystem and significantly improve national food safety standards through shared expertise and integrated solutions.

In-Depth Asia Pacific Cold Chain Logistics Industry Market Outlook

The Asia-Pacific cold chain logistics market is poised for continued growth, driven by evolving consumer preferences, technological advancements, and supportive government policies. Strategic investments in infrastructure development, particularly in emerging economies, will further unlock market potential. Companies focusing on innovation, sustainability, and customer-centric solutions will be best positioned to capture significant market share. The increasing adoption of digital technologies and data analytics will enhance operational efficiency and supply chain visibility, leading to improved cost management and enhanced customer service.

Asia Pacific Cold Chain Logistics Industry Segmentation

-

1. Services

- 1.1. Storage

- 1.2. Transportation

- 1.3. Value-ad

-

2. Temperature Type

- 2.1. Chilled

- 2.2. Frozen

-

3. Application

- 3.1. Horticulture (Fresh Fruits and Vegetables)

- 3.2. Dairy Products (Milk, Ice-cream, Butter, Etc.)

- 3.3. Meats, Fish, Poultry

- 3.4. Processed Food Products

- 3.5. Pharma, Life Sciences, and Chemicals

- 3.6. Other Applications

Asia Pacific Cold Chain Logistics Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. Japan

- 1.3. South Korea

- 1.4. India

- 1.5. Australia

- 1.6. New Zealand

- 1.7. Indonesia

- 1.8. Malaysia

- 1.9. Singapore

- 1.10. Thailand

- 1.11. Vietnam

- 1.12. Philippines

Asia Pacific Cold Chain Logistics Industry Regional Market Share

Geographic Coverage of Asia Pacific Cold Chain Logistics Industry

Asia Pacific Cold Chain Logistics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.58% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Services

- 5.1.1. Storage

- 5.1.2. Transportation

- 5.1.3. Value-ad

- 5.2. Market Analysis, Insights and Forecast - by Temperature Type

- 5.2.1. Chilled

- 5.2.2. Frozen

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Horticulture (Fresh Fruits and Vegetables)

- 5.3.2. Dairy Products (Milk, Ice-cream, Butter, Etc.)

- 5.3.3. Meats, Fish, Poultry

- 5.3.4. Processed Food Products

- 5.3.5. Pharma, Life Sciences, and Chemicals

- 5.3.6. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Services

- 6. Asia Pacific Cold Chain Logistics Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Services

- 6.1.1. Storage

- 6.1.2. Transportation

- 6.1.3. Value-ad

- 6.2. Market Analysis, Insights and Forecast - by Temperature Type

- 6.2.1. Chilled

- 6.2.2. Frozen

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Horticulture (Fresh Fruits and Vegetables)

- 6.3.2. Dairy Products (Milk, Ice-cream, Butter, Etc.)

- 6.3.3. Meats, Fish, Poultry

- 6.3.4. Processed Food Products

- 6.3.5. Pharma, Life Sciences, and Chemicals

- 6.3.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Services

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 SCG Logistics Management Company Limited

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 CWT PTE LIMITED (CWT International Ltd)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 AIT Worldwide Logistics Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 SF Express

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 OOCL Logistics Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 CJ Rokin Logistics**List Not Exhaustive

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Nichirei Logistics Group Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 United Parcel Service of America

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 X2 Logistics Network (X2 GROUP)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 JWD Infologistics Public Company Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 SCG Logistics Management Company Limited

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Asia Pacific Cold Chain Logistics Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia Pacific Cold Chain Logistics Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Services 2020 & 2033

- Table 2: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Temperature Type 2020 & 2033

- Table 3: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Services 2020 & 2033

- Table 6: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Temperature Type 2020 & 2033

- Table 7: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Asia Pacific Cold Chain Logistics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: China Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Japan Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: South Korea Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: India Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Australia Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: New Zealand Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Indonesia Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Malaysia Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Singapore Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Thailand Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Vietnam Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Philippines Asia Pacific Cold Chain Logistics Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia Pacific Cold Chain Logistics Industry?

The projected CAGR is approximately 8.58%.

2. Which companies are prominent players in the Asia Pacific Cold Chain Logistics Industry?

Key companies in the market include SCG Logistics Management Company Limited, CWT PTE LIMITED (CWT International Ltd), AIT Worldwide Logistics Inc, SF Express, OOCL Logistics Ltd, CJ Rokin Logistics**List Not Exhaustive, Nichirei Logistics Group Inc, United Parcel Service of America, X2 Logistics Network (X2 GROUP), JWD Infologistics Public Company Ltd.

3. What are the main segments of the Asia Pacific Cold Chain Logistics Industry?

The market segments include Services, Temperature Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 154.95 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing international trade; Advancements in technology.

6. What are the notable trends driving market growth?

Decreasing Volume of Domestic Water Freight Transport in Japan.

7. Are there any restraints impacting market growth?

Geopolitical uncertainities; Changing trade policies.

8. Can you provide examples of recent developments in the market?

October 2022: Express giant UPS expanded its Premier service for time and temperature-sensitive shipments to Thailand and Singapore. The service offers to track and prioritize loads and has three tiers, with Premier Gold service available in two locations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia Pacific Cold Chain Logistics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia Pacific Cold Chain Logistics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia Pacific Cold Chain Logistics Industry?

To stay informed about further developments, trends, and reports in the Asia Pacific Cold Chain Logistics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence