Key Insights

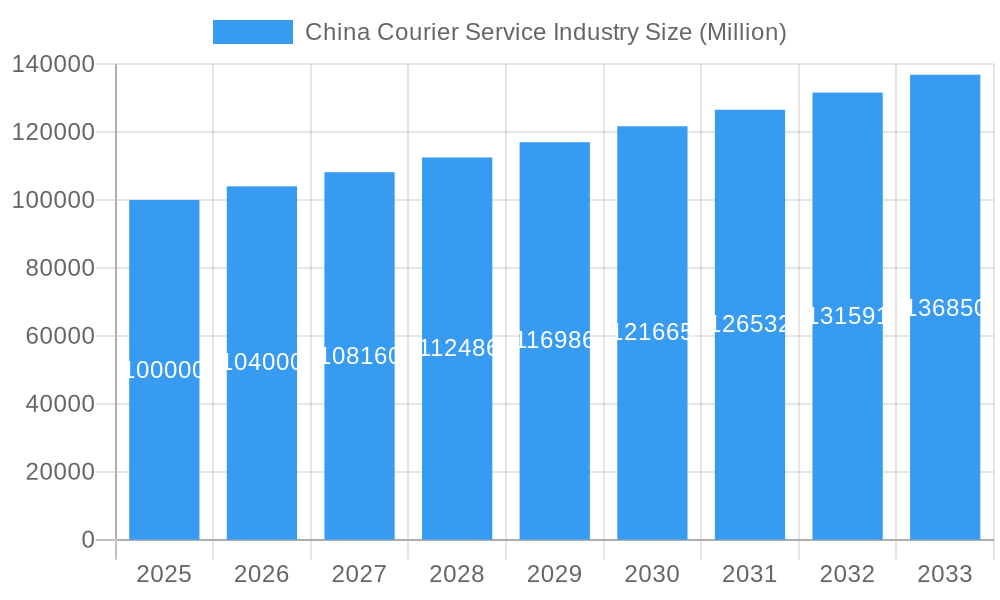

The China courier service market is projected to experience substantial growth, driven by the continued expansion of e-commerce, particularly in the B2C sector. With a projected Compound Annual Growth Rate (CAGR) of 7.21%, the market is estimated to reach $131.84 billion by 2025. Key growth catalysts include the increasing consumer adoption of online shopping, a growing middle class with enhanced purchasing power, and government initiatives to bolster logistics infrastructure. While domestic deliveries dominate, the international segment is also expanding due to rising cross-border e-commerce. Express delivery remains a primary growth driver, segmented by delivery speed. The industry is highly competitive, with major players like China Post, DHL, and SF Express innovating to differentiate their services. Challenges include escalating labor costs, evolving regulatory frameworks, and the imperative for technological upgrades to ensure efficiency and robust tracking systems. Shipment weight segmentation (light, medium, heavy) reflects the industry's diverse capabilities in handling various goods, mirroring the breadth of e-commerce operations. Air transport plays a significant role, complemented by road transport's foundational importance for domestic logistics. E-commerce, BFSI, and healthcare are key end-user industries contributing to the market's overall size.

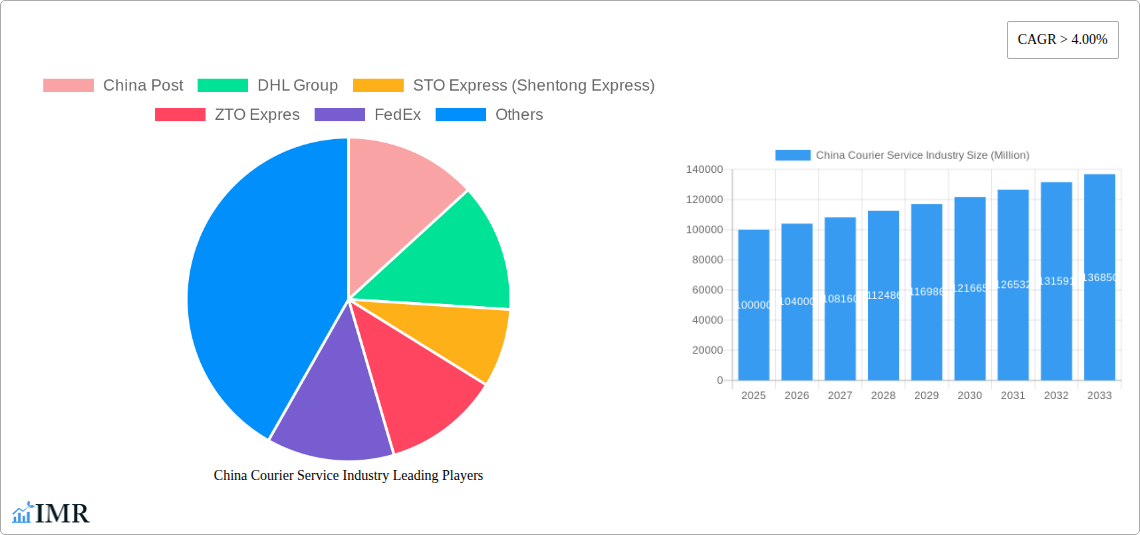

China Courier Service Industry Market Size (In Billion)

Conservative estimates forecast sustained, though potentially moderated, growth in the coming years, influenced by infrastructure enhancements, technological advancements such as automation and AI in logistics, supportive government policies, and the dynamic competitive environment. Maintaining operational efficiency amidst global economic fluctuations will be critical for market participants. Strategic international expansion and innovative service offerings will be pivotal for individual companies' success within the competitive China courier service landscape.

China Courier Service Industry Company Market Share

China Courier Service Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the dynamic China courier service industry, encompassing market size, growth trends, competitive landscape, and future outlook. The study period covers 2019-2033, with 2025 as the base and estimated year. This report is invaluable for industry professionals, investors, and strategic planners seeking to navigate this rapidly evolving market.

Keywords: China courier service, express delivery, logistics, e-commerce logistics, B2B courier, B2C courier, C2C courier, China Post, DHL, STO Express, ZTO Express, FedEx, UPS, SF Express, Yunda Express, YTO Express, market analysis, market size, market share, growth forecast, industry trends, competitive landscape, technological innovation.

China Courier Service Industry Market Dynamics & Structure

The China courier service market is characterized by intense competition, rapid technological advancements, and evolving regulatory frameworks. Market concentration is high, with a few dominant players controlling a significant share. The market is segmented by destination (domestic and international), speed of delivery (express and non-express), business model (B2B, B2C, C2C), shipment weight (light, medium, heavy), mode of transport (air, road, others), and end-user industry (e-commerce, BFSI, healthcare, manufacturing, primary industry, wholesale & retail, others).

- Market Concentration: The top five players (China Post, SF Express, STO Express, Yunda Express, and ZTO Express) hold approximately xx% of the market share in 2025. This high concentration reflects significant barriers to entry, including substantial capital investment and established logistics networks.

- Technological Innovation: The industry is driven by technological innovation, particularly in areas such as automation, AI-powered delivery solutions, and advanced tracking systems. However, integrating new technologies presents challenges, including high initial investment costs and the need for skilled workforce.

- Regulatory Framework: Government regulations, including licensing requirements and safety standards, influence market dynamics. Recent regulatory changes have focused on enhancing service quality and consumer protection.

- Competitive Product Substitutes: While direct substitutes are limited, alternative delivery options such as same-day delivery services and specialized niche carriers pose some level of competition.

- End-User Demographics: The market is primarily driven by the growth of e-commerce and increasing consumer demand for faster and more reliable delivery services. The rise of mobile commerce and online shopping further fuels industry expansion.

- M&A Trends: The past five years have witnessed xx M&A deals in the Chinese courier service industry, primarily focused on consolidating market share and expanding service offerings. These mergers and acquisitions highlight the highly competitive nature of the market.

China Courier Service Industry Growth Trends & Insights

The China courier service industry has experienced significant growth over the past five years (2019-2024). The market size reached xx million units in 2024 and is projected to reach xx million units in 2025, exhibiting a CAGR of xx% during the historical period. This robust growth is fueled by several factors: the explosive expansion of e-commerce, increasing disposable incomes, improved infrastructure, and government support for logistics development. The adoption rate of express delivery services has significantly increased among both businesses and consumers, and the shift towards online shopping continues to drive demand. Technological disruptions, such as the introduction of automated sorting facilities and drone delivery, are enhancing efficiency and scalability. Consumer behavior is evolving towards expecting faster, more convenient, and trackable delivery options, impacting the service offerings of courier companies. The forecast period (2025-2033) anticipates continued growth, driven by ongoing e-commerce expansion and evolving consumer expectations.

Dominant Regions, Countries, or Segments in China Courier Service Industry

The domestic market segment dominates the China courier service industry, accounting for approximately xx% of the total market revenue in 2025. This dominance is attributed to the rapid growth of e-commerce and the concentration of online retail activities within China. However, the international segment is also experiencing significant growth, driven by increasing cross-border e-commerce transactions.

Key Drivers for Domestic Market Growth:

- Rapid expansion of e-commerce, driven by increasing internet penetration and mobile commerce.

- Growing consumer preference for faster and more convenient delivery services.

- Government initiatives aimed at improving logistics infrastructure.

- Strong economic growth and rising disposable incomes.

Key Drivers for Express Delivery Segment Growth:

- Increasing consumer demand for speed and reliability.

- Growing adoption of time-sensitive delivery services by businesses.

- Technological advancements leading to improved efficiency.

Key Drivers for B2C Segment Growth:

- Expansion of online retail platforms and marketplace growth.

- Rise in consumer spending on online goods and services.

- Growing demand for convenience and home delivery options.

China Courier Service Industry Product Landscape

The product landscape encompasses a range of services, including express delivery, same-day delivery, freight forwarding, and value-added services such as insurance and packaging. Innovation is focused on enhancing delivery speed and efficiency through technological advancements, including AI-powered routing and automated sorting systems. Unique selling propositions include next-day or same-day delivery guarantees, advanced tracking systems, and specialized handling for fragile or temperature-sensitive goods. Companies increasingly offer customized solutions tailored to specific customer needs. Key performance indicators include delivery speed, on-time delivery rates, damage rates, and customer satisfaction.

Key Drivers, Barriers & Challenges in China Courier Service Industry

Key Drivers:

- E-commerce boom: The rapid growth of e-commerce continues to be a major driver of demand.

- Technological advancements: Automation, AI, and data analytics improve efficiency and reduce costs.

- Government support: Infrastructure development and regulatory improvements promote growth.

Key Challenges:

- Intense competition: The market is highly fragmented and competitive, putting pressure on pricing and profitability. This leads to a price war, affecting the bottom lines.

- Rising labor costs: Increasing wages and benefits for delivery personnel pose a significant cost challenge.

- Infrastructure limitations: Congestion in major cities and inadequate infrastructure in rural areas can hinder efficient delivery.

- Regulatory hurdles: Compliance with regulations and evolving government policies can be complex and costly.

Emerging Opportunities in China Courier Service Industry

- Growth of cross-border e-commerce: Expanding international shipping capabilities to tap into the increasing demand for global delivery services.

- Last-mile delivery solutions: Implementing innovative approaches, such as drone delivery and automated delivery robots, to enhance efficiency and reduce costs.

- Specialized delivery services: Catering to niche markets with specialized handling for temperature-sensitive goods, high-value items, or bulky shipments.

- Data analytics and AI-powered services: Leveraging data analytics to optimize routing, predict demand, and improve customer service.

Growth Accelerators in the China Courier Service Industry

Technological advancements, strategic partnerships, and expansion into underserved markets are key growth accelerators. Investments in automation, AI, and data analytics are crucial for efficiency gains. Strategic collaborations with e-commerce platforms and businesses can boost market share and access new customer segments. Expanding into less-developed regions and providing services to previously underserved populations present significant opportunities for growth.

Key Players Shaping the China Courier Service Industry Market

- China Post

- DHL Group

- STO Express (Shentong Express)

- ZTO Express

- FedEx

- United Parcel Service of America Inc (UPS)

- Hongkong Post

- Yunda Express

- YTO Express

- La Poste Group

- SF Express (KEX-SF)

Notable Milestones in China Courier Service Industry Sector

- June 2023: China Post launched its first integrated indoor and outdoor “Robot Plus” AI delivery solution. This signifies a significant step towards automation in last-mile delivery.

- April 2023: China Post and Ping An Bank launched an intelligent archives service center, integrating auto finance and logistics services. This exemplifies the growing convergence between financial services and logistics.

- March 2023: UPS partnered with Google Cloud for improved package tracking using RFID technology, enhancing efficiency and transparency. This partnership showcases the growing importance of data analytics in logistics.

In-Depth China Courier Service Industry Market Outlook

The China courier service industry is poised for sustained growth driven by the continued expansion of e-commerce, technological advancements, and supportive government policies. Opportunities exist in expanding into underserved regions, developing innovative delivery solutions, and leveraging data analytics to improve efficiency and customer satisfaction. Strategic partnerships and investments in automation will be crucial for maintaining a competitive edge in this dynamic market. The market is expected to continue its robust growth trajectory through 2033, presenting significant opportunities for both established players and new entrants.

China Courier Service Industry Segmentation

-

1. Destination

- 1.1. Domestic

- 1.2. International

-

2. Speed Of Delivery

- 2.1. Express

- 2.2. Non-Express

-

3. Model

- 3.1. Business-to-Business (B2B)

- 3.2. Business-to-Consumer (B2C)

- 3.3. Consumer-to-Consumer (C2C)

-

4. Shipment Weight

- 4.1. Heavy Weight Shipments

- 4.2. Light Weight Shipments

- 4.3. Medium Weight Shipments

-

5. Mode Of Transport

- 5.1. Air

- 5.2. Road

- 5.3. Others

-

6. End User Industry

- 6.1. E-Commerce

- 6.2. Financial Services (BFSI)

- 6.3. Healthcare

- 6.4. Manufacturing

- 6.5. Primary Industry

- 6.6. Wholesale and Retail Trade (Offline)

- 6.7. Others

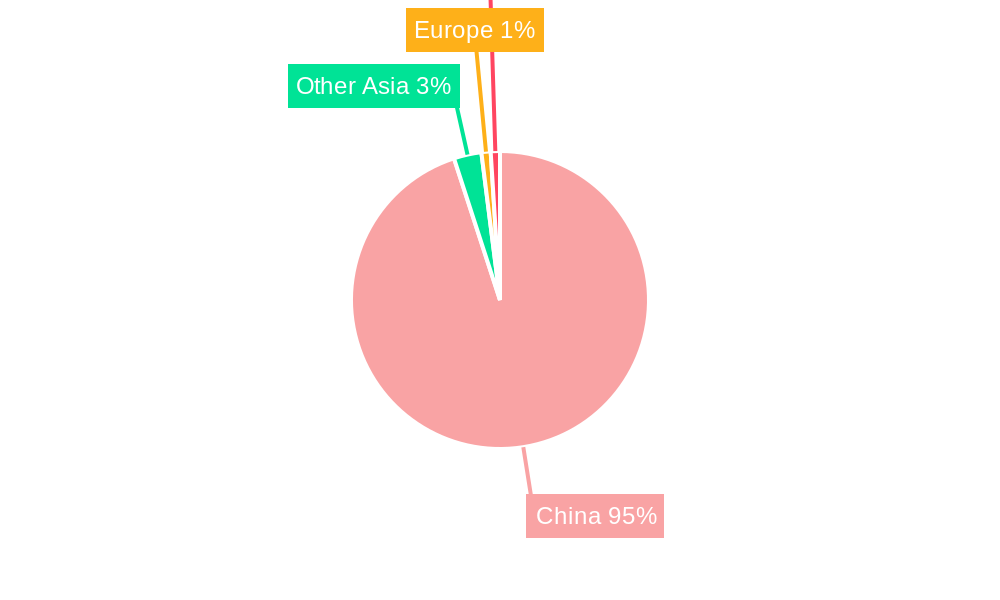

China Courier Service Industry Segmentation By Geography

- 1. China

China Courier Service Industry Regional Market Share

Geographic Coverage of China Courier Service Industry

China Courier Service Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.21% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Destination

- 5.1.1. Domestic

- 5.1.2. International

- 5.2. Market Analysis, Insights and Forecast - by Speed Of Delivery

- 5.2.1. Express

- 5.2.2. Non-Express

- 5.3. Market Analysis, Insights and Forecast - by Model

- 5.3.1. Business-to-Business (B2B)

- 5.3.2. Business-to-Consumer (B2C)

- 5.3.3. Consumer-to-Consumer (C2C)

- 5.4. Market Analysis, Insights and Forecast - by Shipment Weight

- 5.4.1. Heavy Weight Shipments

- 5.4.2. Light Weight Shipments

- 5.4.3. Medium Weight Shipments

- 5.5. Market Analysis, Insights and Forecast - by Mode Of Transport

- 5.5.1. Air

- 5.5.2. Road

- 5.5.3. Others

- 5.6. Market Analysis, Insights and Forecast - by End User Industry

- 5.6.1. E-Commerce

- 5.6.2. Financial Services (BFSI)

- 5.6.3. Healthcare

- 5.6.4. Manufacturing

- 5.6.5. Primary Industry

- 5.6.6. Wholesale and Retail Trade (Offline)

- 5.6.7. Others

- 5.7. Market Analysis, Insights and Forecast - by Region

- 5.7.1. China

- 5.1. Market Analysis, Insights and Forecast - by Destination

- 6. China Courier Service Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Destination

- 6.1.1. Domestic

- 6.1.2. International

- 6.2. Market Analysis, Insights and Forecast - by Speed Of Delivery

- 6.2.1. Express

- 6.2.2. Non-Express

- 6.3. Market Analysis, Insights and Forecast - by Model

- 6.3.1. Business-to-Business (B2B)

- 6.3.2. Business-to-Consumer (B2C)

- 6.3.3. Consumer-to-Consumer (C2C)

- 6.4. Market Analysis, Insights and Forecast - by Shipment Weight

- 6.4.1. Heavy Weight Shipments

- 6.4.2. Light Weight Shipments

- 6.4.3. Medium Weight Shipments

- 6.5. Market Analysis, Insights and Forecast - by Mode Of Transport

- 6.5.1. Air

- 6.5.2. Road

- 6.5.3. Others

- 6.6. Market Analysis, Insights and Forecast - by End User Industry

- 6.6.1. E-Commerce

- 6.6.2. Financial Services (BFSI)

- 6.6.3. Healthcare

- 6.6.4. Manufacturing

- 6.6.5. Primary Industry

- 6.6.6. Wholesale and Retail Trade (Offline)

- 6.6.7. Others

- 6.1. Market Analysis, Insights and Forecast - by Destination

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 China Post

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 DHL Group

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 STO Express (Shentong Express)

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 ZTO Expres

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 FedEx

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 United Parcel Service of America Inc (UPS)

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Hongkong Post

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Yunda Express

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 YTO Express

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 La Poste Group

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 SF Express (KEX-SF)

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 China Post

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Courier Service Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China Courier Service Industry Share (%) by Company 2025

List of Tables

- Table 1: China Courier Service Industry Revenue billion Forecast, by Destination 2020 & 2033

- Table 2: China Courier Service Industry Revenue billion Forecast, by Speed Of Delivery 2020 & 2033

- Table 3: China Courier Service Industry Revenue billion Forecast, by Model 2020 & 2033

- Table 4: China Courier Service Industry Revenue billion Forecast, by Shipment Weight 2020 & 2033

- Table 5: China Courier Service Industry Revenue billion Forecast, by Mode Of Transport 2020 & 2033

- Table 6: China Courier Service Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 7: China Courier Service Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: China Courier Service Industry Revenue billion Forecast, by Destination 2020 & 2033

- Table 9: China Courier Service Industry Revenue billion Forecast, by Speed Of Delivery 2020 & 2033

- Table 10: China Courier Service Industry Revenue billion Forecast, by Model 2020 & 2033

- Table 11: China Courier Service Industry Revenue billion Forecast, by Shipment Weight 2020 & 2033

- Table 12: China Courier Service Industry Revenue billion Forecast, by Mode Of Transport 2020 & 2033

- Table 13: China Courier Service Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 14: China Courier Service Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Courier Service Industry?

The projected CAGR is approximately 7.21%.

2. Which companies are prominent players in the China Courier Service Industry?

Key companies in the market include China Post, DHL Group, STO Express (Shentong Express), ZTO Expres, FedEx, United Parcel Service of America Inc (UPS), Hongkong Post, Yunda Express, YTO Express, La Poste Group, SF Express (KEX-SF).

3. What are the main segments of the China Courier Service Industry?

The market segments include Destination, Speed Of Delivery, Model, Shipment Weight, Mode Of Transport, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 131.84 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing production of chemical and allied products driving the market4.; Rising demand for green warehouses.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

4.; Stringent Rules and Regulations4.; Higher Costs.

8. Can you provide examples of recent developments in the market?

June 2023: China Post launched its first integrated indoor and outdoor “Robot Plus” AI delivery solution in China. The intelligent delivery solution relies on a combination of unmanned vehicles outdoors and robots indoors, constructing an integrated indoor and outdoor unmanned distribution mode and developing a last-mile logistics network with AI transport capacity sharing.April 2023: China Post and the Automobile Consumption Financial Center of Ping An Bank Co. Ltd launched an intelligent archives service center in Guangdong to promote the service integration of auto finance and express and logistics businesses.March 2023: UPS entered a partnership with Google Cloud, where Google will help UPS by putting radio-frequency identification chips on packages to track them efficiently.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Courier Service Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Courier Service Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Courier Service Industry?

To stay informed about further developments, trends, and reports in the China Courier Service Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence