Key Insights

The global market for connectors in food production is poised for significant expansion, driven by the increasing demand for efficient, hygienic, and automated food processing and packaging solutions. With an estimated market size of approximately USD 1.5 billion in 2025, the sector is projected to experience a robust Compound Annual Growth Rate (CAGR) of around 7.5% during the forecast period of 2025-2033. This growth is fueled by the industry's continuous investment in advanced machinery and automation to enhance productivity, ensure stringent food safety standards, and reduce operational costs. Key applications driving this demand include sophisticated food processing equipment that requires reliable and high-performance connectivity, as well as advanced food packaging machinery designed for speed and precision. The adoption of Industry 4.0 principles, including the Internet of Things (IoT) and smart manufacturing, further necessitates durable and high-quality connectors capable of withstanding harsh environments, frequent cleaning, and continuous operation.

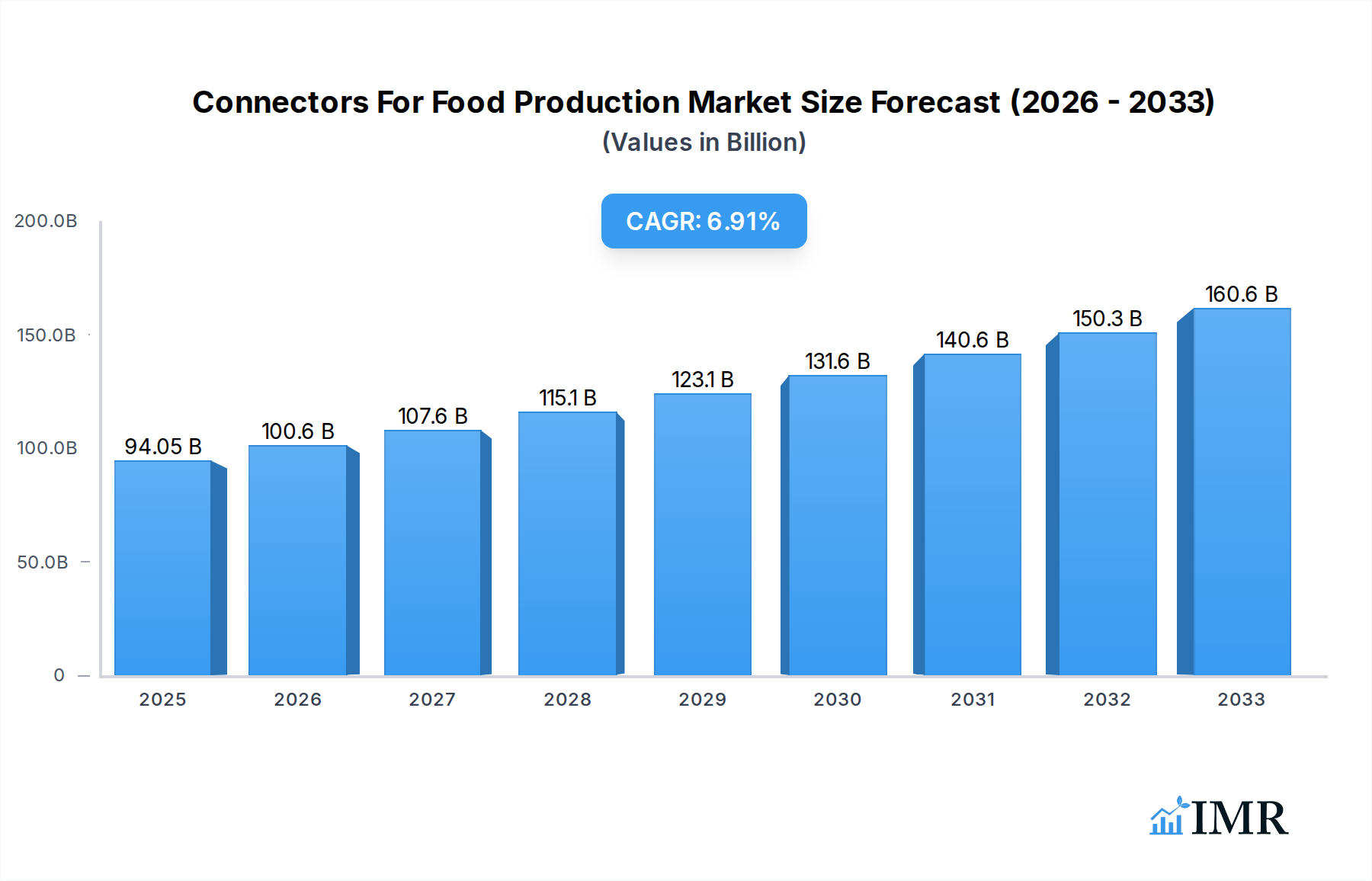

Connectors For Food Production Market Size (In Billion)

The market segments for M12 and M8 connectors are expected to see substantial growth, reflecting their widespread adoption in the food and beverage industry due to their compact size, robust sealing (IP67/IP69K), and resistance to chemicals and high-pressure washdowns. While food processing and packaging equipment represent the largest application segments, the growing emphasis on maintaining product integrity throughout the supply chain is also boosting the demand for specialized connectors in food transportation equipment. Major players like Harting, Binder, Belden, and Pepperl+Fuchs are at the forefront, investing in research and development to offer innovative solutions that meet the evolving needs of the food industry. Despite the promising growth, challenges such as the high cost of advanced connector technologies and the need for specialized training for installation and maintenance can pose moderate restraints. Geographically, North America and Europe are leading markets due to their established food industries and early adoption of automation, while the Asia Pacific region presents a rapidly growing opportunity driven by increasing food production and modernization efforts.

Connectors For Food Production Company Market Share

Connectors For Food Production Market Dynamics & Structure

The global Connectors for Food Production market is characterized by a moderately consolidated structure, with key players such as Harting, Binder, Belden, Colder Products Company, ESCHA, Northern Connectors, Fortop, U.I. Lapp, HUMMEL, Lumberg Automation, Pepperl+Fuchs, and Murrelektronik dominating market share. Technological innovation is a primary driver, fueled by the increasing demand for robust, hygienic, and high-performance connectivity solutions in food processing and packaging. Advancements in materials science, miniaturization, and signal integrity are crucial for meeting stringent industry standards. Regulatory frameworks, particularly those concerning food safety, hygiene (e.g., FDA, EU food contact regulations), and electrical safety, significantly shape product development and market access. Competitive product substitutes, while limited in specialized food-grade connectors, may include general-purpose connectors adapted for the environment, posing a potential threat in lower-tier applications. End-user demographics are shifting towards larger, automated food production facilities demanding integrated and smart connectivity. Mergers and acquisitions (M&A) trends are observed as companies seek to expand their product portfolios, geographical reach, and technological capabilities. For instance, recent M&A activities have focused on acquiring innovative technologies in areas like industrial Ethernet and wireless connectivity to cater to the Industry 4.0 evolution in food production.

- Market Concentration: Moderately consolidated with a strong presence of established players.

- Technological Innovation Drivers: Demand for hygienic, robust, and high-speed connectivity; Industry 4.0 integration.

- Regulatory Frameworks: Stringent food safety, hygiene, and electrical safety standards.

- Competitive Product Substitutes: Limited but present in less demanding applications.

- End-User Demographics: Shift towards large-scale, automated food production facilities.

- M&A Trends: Focus on portfolio expansion and technological acquisition.

Connectors For Food Production Growth Trends & Insights

The Connectors for Food Production market is poised for significant expansion, driven by the relentless demand for efficient, safe, and automated food processing and packaging operations. The market size is projected to witness a substantial CAGR, evolving from an estimated xx million units in 2025 to a projected xx million units by 2033. Adoption rates for specialized food-grade connectors are escalating as manufacturers prioritize compliance with increasingly rigorous food safety regulations and seek to minimize downtime due to connector failures. Technological disruptions are playing a pivotal role, with the integration of Industrial Internet of Things (IIoT) enabling smart factories. This necessitates connectors that support high-speed data transmission, power over Ethernet (PoE), and robust communication protocols. For instance, the widespread adoption of M12 connectors, known for their ruggedness and IP67/IP69K ratings, is a testament to this trend.

Consumer behavior shifts, such as the growing demand for convenience foods and the need for enhanced traceability throughout the supply chain, are indirectly fueling the growth of this sector. To meet these demands, food manufacturers are investing heavily in upgrading their production lines with advanced machinery, which in turn requires sophisticated and reliable connectivity solutions. The market penetration of advanced connector types, particularly those designed for washdown environments and extreme temperatures, is increasing. Furthermore, the ongoing trend towards automation across the entire food value chain, from primary processing to final packaging, is a fundamental growth driver. This includes the adoption of robotics, automated guided vehicles (AGVs), and advanced sensing technologies, all of which rely heavily on durable and high-performance industrial connectors. The market is also seeing a rise in demand for customized connector solutions tailored to specific application requirements, further contributing to its robust growth trajectory.

Dominant Regions, Countries, or Segments in Connectors For Food Production

The Food Processing Equipment segment, particularly within the Application category, is a dominant force driving growth in the global Connectors for Food Production market. This dominance is underpinned by several critical factors that resonate across key geographical regions. North America and Europe currently lead the market, exhibiting high adoption rates for advanced food processing technologies. In North America, the robust presence of large-scale food manufacturers, coupled with significant investments in automation and Industry 4.0 initiatives, propels the demand for sophisticated connectivity solutions. Stringent food safety regulations enforced by agencies like the FDA also necessitate the use of high-quality, reliable connectors.

Europe, with its established food processing industry and a strong emphasis on hygiene and quality standards, mirrors this trend. The European Union’s directives on food contact materials and machinery safety further mandate the use of certified and robust connectors. Economic policies supporting agricultural modernization and food security in these regions create a fertile ground for the expansion of food processing capabilities, directly impacting connector demand.

Among the Type segments, M12 Connectors are experiencing exceptional growth, often outperforming other types due to their inherent advantages in food production environments. M12 connectors, with their excellent sealing capabilities (IP67/IP69K), resistance to harsh chemicals and cleaning agents, and high vibration resistance, are ideally suited for wet, hygienic, and demanding processing conditions. Their versatility in supporting various data transmission protocols, including Industrial Ethernet, makes them indispensable for modern automated food lines. The increasing complexity of food processing equipment, from robotic arms on packaging lines to advanced sensors in processing machinery, necessitates the reliability and high-speed data transfer capabilities offered by M12 connectors. Countries like Germany, the United States, and France are at the forefront of M12 connector adoption within food processing applications, driven by their advanced manufacturing sectors and commitment to product quality and safety. The growth potential for M12 connectors within this segment remains exceptionally high as food manufacturers continue to invest in automation and digitalization.

Connectors For Food Production Product Landscape

The Connectors for Food Production market is witnessing a surge in product innovations focused on enhanced hygiene, durability, and data transmission capabilities. Manufacturers are introducing connectors made from food-grade, FDA-approved materials, capable of withstanding aggressive cleaning agents and high-pressure washdowns, exemplified by IP67 and IP69K rated M12 and M8 connectors. Advancements in sealing technologies and overmolding techniques ensure ingress protection against dust and moisture, crucial for food safety and operational reliability. Furthermore, there's a growing emphasis on miniaturization and high-density connector designs to accommodate increasingly compact food processing and packaging equipment. The integration of advanced shielding and signal integrity features in connectors is also a key trend, supporting the higher bandwidth requirements of Industry 4.0 applications and IIoT integration within the food industry.

Key Drivers, Barriers & Challenges in Connectors For Food Production

Key Drivers:

- Automation and Industry 4.0 Adoption: The drive towards smart factories and automated food production lines fuels demand for robust and high-performance connectors.

- Stringent Food Safety Regulations: Increasing global emphasis on food hygiene and traceability mandates the use of certified, reliable, and easily cleanable connectors.

- Demand for Hygienic Designs: The need for connectors that can withstand frequent washdowns and resist bacterial growth is paramount.

- Technological Advancements: Miniaturization, high-speed data transmission capabilities, and ruggedized designs meet evolving equipment needs.

Barriers & Challenges:

- Cost Sensitivity: While prioritizing safety, food producers can be sensitive to the cost of specialized, high-quality connectors, especially in price-competitive segments.

- Supply Chain Disruptions: Geopolitical events and global logistics challenges can impact the availability and lead times of critical connector components.

- Standardization and Interoperability: Ensuring seamless integration of connectors across diverse machinery from different manufacturers can be a challenge.

- Harsh Operating Environments: Connectors must withstand extreme temperatures, humidity, vibration, and chemical exposure, presenting ongoing engineering challenges.

Emerging Opportunities in Connectors For Food Production

Emerging opportunities in the Connectors for Food Production market lie in the burgeoning demand for wireless connectivity solutions that reduce cabling complexity and enhance hygiene in washdown areas. The integration of smart sensors directly into connectors, enabling real-time data collection on equipment performance and environmental conditions, presents a significant growth avenue. Furthermore, the expansion of the plant-based food sector and the increasing demand for specialty food products are driving the need for highly customized and specialized connector configurations for novel processing equipment. Untapped markets in developing economies, where food production is undergoing rapid modernization, also offer substantial potential for growth. The focus on sustainability is also creating opportunities for connectors made from recycled or bio-based materials, aligning with broader industry goals.

Growth Accelerators in the Connectors For Food Production Industry

The Connectors for Food Production industry's long-term growth is being significantly accelerated by the relentless pursuit of operational efficiency and food safety by global food manufacturers. The ongoing digital transformation of the food sector, spearheaded by the adoption of IIoT, AI, and advanced robotics, necessitates increasingly sophisticated connectivity. Strategic partnerships between connector manufacturers and machinery OEMs are crucial for co-developing integrated solutions that meet specific application needs. Market expansion strategies, targeting emerging economies undergoing rapid industrialization and agricultural modernization, are also key growth catalysts. The continuous innovation in materials science and manufacturing processes that leads to more durable, hygienic, and high-performance connectors will further propel sustained growth.

Key Players Shaping the Connectors For Food Production Market

- Harting

- Binder

- Belden

- Colder Products Company

- ESCHA

- Northern Connectors

- Fortop

- U.I. Lapp

- HUMMEL

- Lumberg Automation

- Pepperl+Fuchs

- Murrelektronik

Notable Milestones in Connectors For Food Production Sector

- 2020: Launch of new series of M12 connectors with enhanced IP69K ratings and food-grade materials to meet stringent hygiene standards.

- 2021: Introduction of compact M8 connectors optimized for space-constrained food packaging machinery.

- 2022: Significant advancements in hybrid connectors supporting both power and high-speed data transmission for automated food processing lines.

- 2023: Increased M&A activity focused on acquiring companies with expertise in wireless connectivity solutions for the food industry.

- Q1 2024: Release of new connector families with improved chemical resistance for enhanced longevity in demanding cleaning cycles.

In-Depth Connectors For Food Production Market Outlook

The future of the Connectors for Food Production market is exceptionally promising, driven by a confluence of technological innovation, evolving regulatory landscapes, and the relentless pursuit of efficiency and safety in the global food industry. Growth accelerators such as the pervasive adoption of Industry 4.0 principles, the demand for smart manufacturing solutions, and the increasing focus on traceability will continue to fuel the demand for advanced, high-performance connectors. Strategic investments in research and development by key players, aimed at creating connectors that are not only robust and hygienic but also offer enhanced data capabilities and miniaturization, will shape market offerings. Emerging opportunities in wireless connectivity and integrated sensor technologies within connectors represent significant untapped potential. Overall, the market is on a strong upward trajectory, poised for substantial growth through 2033, driven by the essential role connectors play in modern, safe, and efficient food production.

Connectors For Food Production Segmentation

-

1. Application

- 1.1. Food Processing Equipment

- 1.2. Food Packaging Equipment

- 1.3. Food Transportation Equipment

- 1.4. Others

-

2. Type

- 2.1. M12 Connectors

- 2.2. M8 Connectors

- 2.3. Others

Connectors For Food Production Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

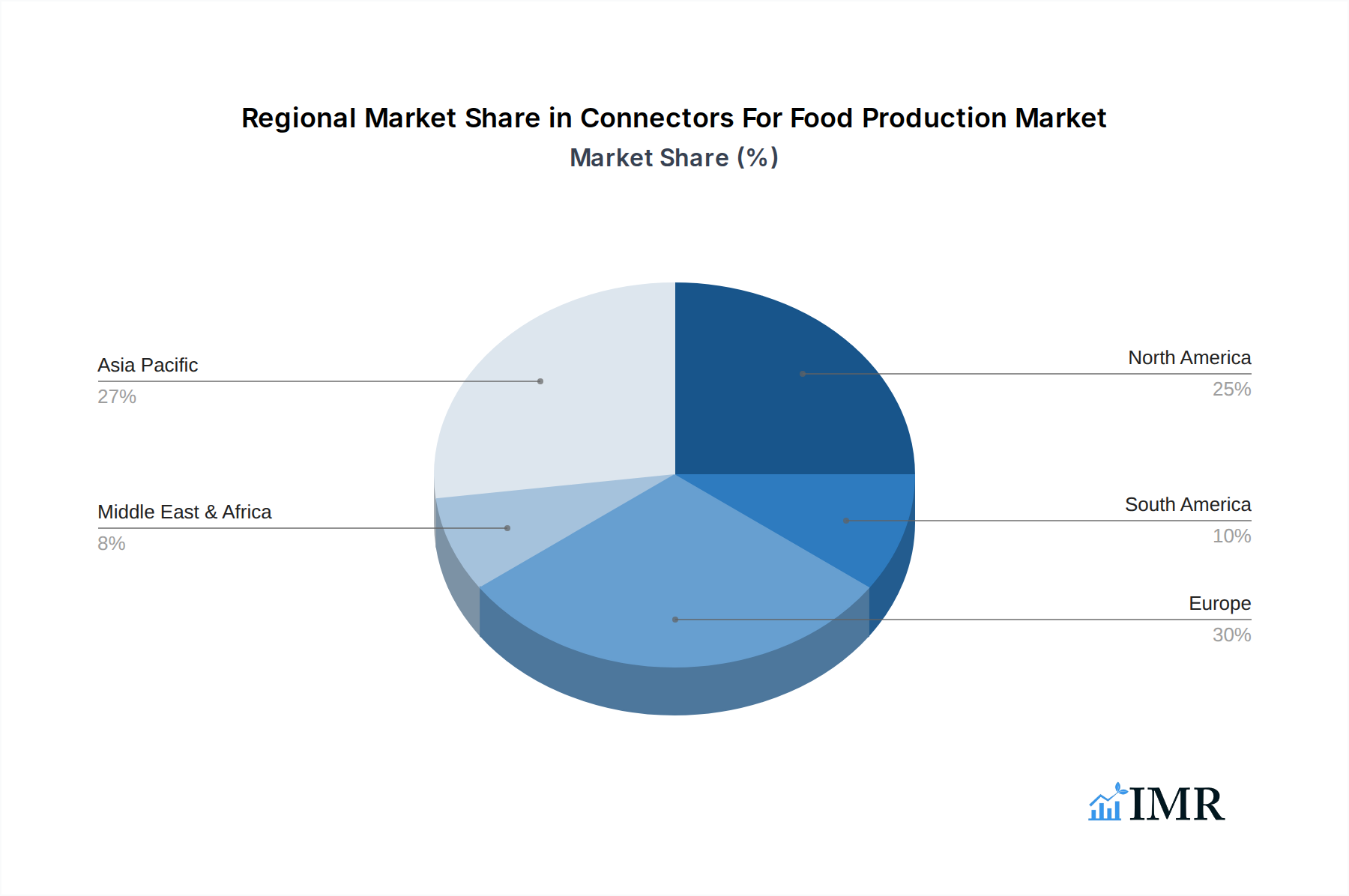

Connectors For Food Production Regional Market Share

Geographic Coverage of Connectors For Food Production

Connectors For Food Production REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Connectors For Food Production Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food Processing Equipment

- 5.1.2. Food Packaging Equipment

- 5.1.3. Food Transportation Equipment

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. M12 Connectors

- 5.2.2. M8 Connectors

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Connectors For Food Production Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food Processing Equipment

- 6.1.2. Food Packaging Equipment

- 6.1.3. Food Transportation Equipment

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. M12 Connectors

- 6.2.2. M8 Connectors

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Connectors For Food Production Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food Processing Equipment

- 7.1.2. Food Packaging Equipment

- 7.1.3. Food Transportation Equipment

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. M12 Connectors

- 7.2.2. M8 Connectors

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Connectors For Food Production Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food Processing Equipment

- 8.1.2. Food Packaging Equipment

- 8.1.3. Food Transportation Equipment

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. M12 Connectors

- 8.2.2. M8 Connectors

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Connectors For Food Production Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food Processing Equipment

- 9.1.2. Food Packaging Equipment

- 9.1.3. Food Transportation Equipment

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. M12 Connectors

- 9.2.2. M8 Connectors

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Connectors For Food Production Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food Processing Equipment

- 10.1.2. Food Packaging Equipment

- 10.1.3. Food Transportation Equipment

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. M12 Connectors

- 10.2.2. M8 Connectors

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Harting

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Binder

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Belden

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Colder Products Company

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 ESCHA

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Northern Connectors

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Fortop

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 U.I. Lapp

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 HUMMEL

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Lumberg Automation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Pepperl+Fuchs

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Murrelektronik

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Harting

List of Figures

- Figure 1: Global Connectors For Food Production Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Connectors For Food Production Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Connectors For Food Production Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Connectors For Food Production Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Connectors For Food Production Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Connectors For Food Production Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Connectors For Food Production Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Connectors For Food Production Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Connectors For Food Production Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Connectors For Food Production Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Connectors For Food Production Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Connectors For Food Production Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Connectors For Food Production Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Connectors For Food Production Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Connectors For Food Production Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Connectors For Food Production Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Connectors For Food Production Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Connectors For Food Production Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Connectors For Food Production Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Connectors For Food Production Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Connectors For Food Production Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Connectors For Food Production Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Connectors For Food Production Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Connectors For Food Production Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Connectors For Food Production Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Connectors For Food Production Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Connectors For Food Production Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Connectors For Food Production Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Connectors For Food Production Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Connectors For Food Production Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Connectors For Food Production Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Connectors For Food Production Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Connectors For Food Production Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Connectors For Food Production Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Connectors For Food Production Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Connectors For Food Production Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Connectors For Food Production Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Connectors For Food Production Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Connectors For Food Production Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Connectors For Food Production Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Connectors For Food Production Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Connectors For Food Production Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Connectors For Food Production Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Connectors For Food Production Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Connectors For Food Production Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Connectors For Food Production Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Connectors For Food Production Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Connectors For Food Production Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Connectors For Food Production Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Connectors For Food Production Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Connectors For Food Production?

The projected CAGR is approximately 6.85%.

2. Which companies are prominent players in the Connectors For Food Production?

Key companies in the market include Harting, Binder, Belden, Colder Products Company, ESCHA, Northern Connectors, Fortop, U.I. Lapp, HUMMEL, Lumberg Automation, Pepperl+Fuchs, Murrelektronik.

3. What are the main segments of the Connectors For Food Production?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Connectors For Food Production," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Connectors For Food Production report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Connectors For Food Production?

To stay informed about further developments, trends, and reports in the Connectors For Food Production, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence