Key Insights

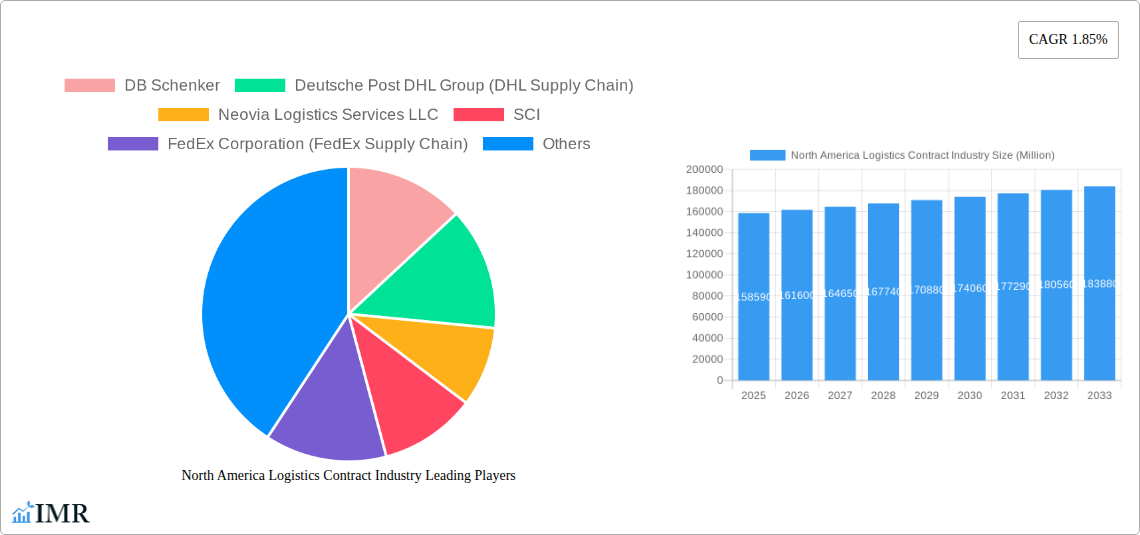

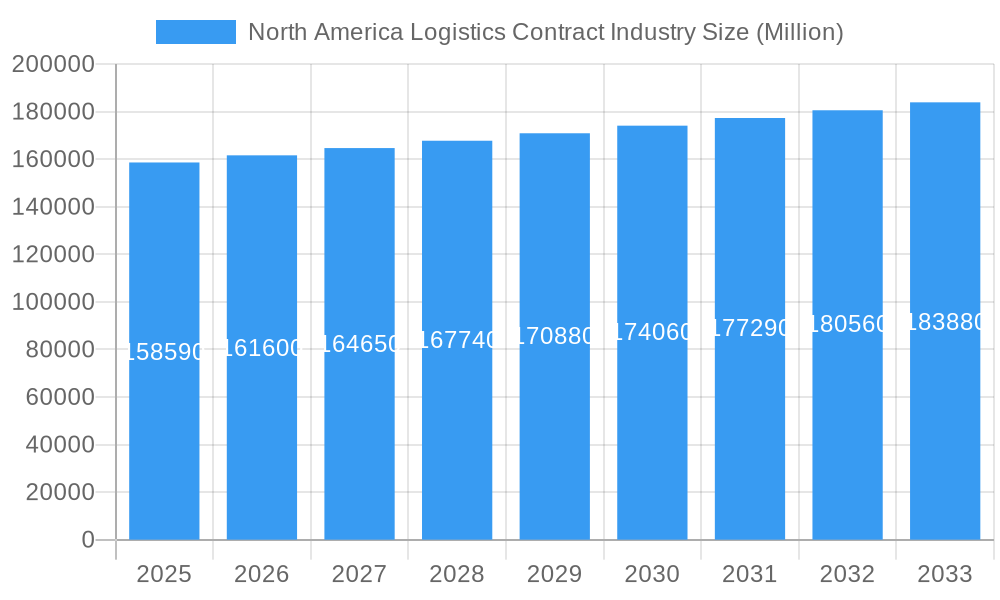

The North American logistics contract industry, valued at $158.59 billion in 2025, is poised for steady growth, projected at a compound annual growth rate (CAGR) of 1.85% from 2025 to 2033. This growth is driven by several factors. The burgeoning e-commerce sector necessitates efficient and reliable supply chain solutions, fueling demand for contract logistics services. Furthermore, the increasing complexity of global supply chains, coupled with a focus on optimizing operational efficiency and reducing costs, prompts businesses to outsource logistics functions to specialized providers. The automotive and manufacturing sectors, significant contributors to this market, are expected to continue driving growth, along with the expanding healthcare and pharmaceuticals industries. Technological advancements, such as the integration of automation and data analytics in logistics operations, are also contributing to market expansion, enabling improved tracking, inventory management, and overall efficiency. However, challenges remain, including fluctuating fuel prices, labor shortages, and the ongoing need to adapt to evolving regulatory landscapes, potentially tempering the overall growth rate.

North America Logistics Contract Industry Market Size (In Billion)

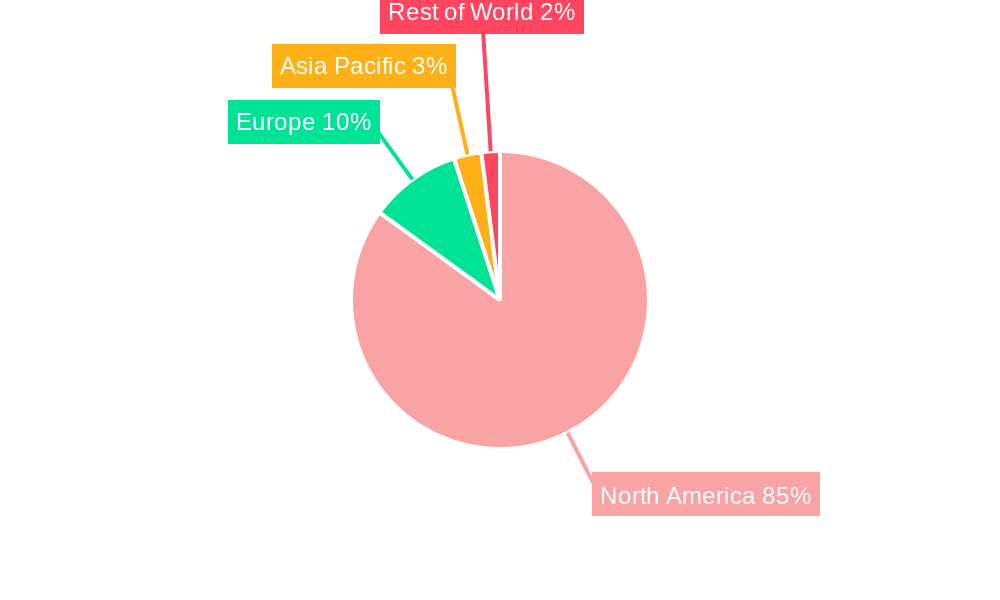

Regional analysis reveals the United States as the dominant market within North America, followed by Canada and Mexico. The market is segmented by service type (insourced versus outsourced) and end-user industry. The outsourced segment is expected to hold the largest market share, driven by the aforementioned factors like cost optimization and expertise. Within the end-user segments, manufacturing and automotive, and consumer goods and retail, are expected to remain key drivers of market growth. Competitive landscape analysis reveals several key players, including DB Schenker, DHL Supply Chain, FedEx Supply Chain, UPS Supply Chain Solutions, and others, actively competing through service differentiation, technological innovation, and strategic acquisitions. The forecast period (2025-2033) anticipates consistent market growth, though the rate may fluctuate based on macroeconomic conditions and evolving industry trends.

North America Logistics Contract Industry Company Market Share

This comprehensive report provides a deep dive into the North America logistics contract industry, analyzing market dynamics, growth trends, key players, and future opportunities. Covering the period from 2019 to 2033, with a focus on 2025, this report is an essential resource for industry professionals, investors, and strategic decision-makers. The report examines both parent market (Logistics Industry) and child market (Contract Logistics) dynamics to offer a holistic view.

North America Logistics Contract Industry Market Dynamics & Structure

The North American contract logistics market is characterized by high competition, significant technological advancements, and evolving regulatory landscapes. Market concentration is moderate, with a few major players holding substantial market share, while numerous smaller companies compete in niche segments. The market is segmented by type (insourced vs. outsourced) and end-user (manufacturing, automotive, consumer goods, high-tech, healthcare, and others).

- Market Concentration: The top 5 players hold approximately xx% of the market share in 2025. Smaller players focus on niche services or geographic areas.

- Technological Innovation: Automation (e.g., robotics, AI), data analytics, and blockchain technology are key drivers of innovation, improving efficiency and transparency. However, high implementation costs and integration challenges remain barriers for some businesses.

- Regulatory Framework: Regulations concerning transportation, safety, and data privacy impact industry operations and require compliance.

- Competitive Substitutes: Companies offering in-house logistics solutions are key competitors to contract logistics providers.

- End-User Demographics: The increasing demand for efficient supply chains across various industries fuels market growth.

- M&A Trends: Consolidation through mergers and acquisitions is expected to continue, with xx major deals projected between 2025 and 2033, driven by the desire for economies of scale and expanded service offerings.

North America Logistics Contract Industry Growth Trends & Insights

The North America logistics contract industry is experiencing robust growth, driven by e-commerce expansion, globalization, and the increasing outsourcing of logistics functions by businesses seeking operational efficiency. Market size is projected to reach xx million by 2033, with a compound annual growth rate (CAGR) of xx% during the forecast period (2025-2033). This growth is fueled by:

- E-commerce Boom: The surge in online shopping is significantly boosting demand for efficient last-mile delivery and warehouse management services.

- Globalization and Supply Chain Complexity: Businesses increasingly rely on contract logistics providers to manage complex, global supply chains.

- Technological Disruptions: The adoption of advanced technologies is enhancing productivity and reducing costs, contributing to market expansion.

- Shifting Consumer Behavior: Consumers expect faster and more reliable delivery, placing pressure on logistics providers to innovate and optimize their operations.

Dominant Regions, Countries, or Segments in North America Logistics Contract Industry

The United States dominates the North American contract logistics market, accounting for approximately xx% of the total market value in 2025. This dominance stems from:

- Large and Diverse Economy: The US boasts a vast and diversified economy with a high volume of goods movement.

- Developed Infrastructure: Extensive transportation networks (roads, railways, ports) facilitate efficient logistics operations.

- High Technological Adoption: US companies are early adopters of advanced technologies in logistics.

Canada and Mexico also contribute significantly to the market, with growth driven by increasing industrial activity and cross-border trade. Within segments, the Outsourced segment holds the largest market share, reflecting companies' increasing preference for outsourcing non-core logistics functions. The Manufacturing and Automotive, and Consumer Goods and Retail end-user segments are the largest contributors, driven by high-volume goods movement.

- Key Drivers: Strong economic growth, robust infrastructure development, technological advancements, and increasing demand from key industries are key drivers in the US. In Canada, investments in infrastructure and supportive government policies drive growth, while in Mexico, its proximity to the US market and growing manufacturing sector are major factors.

- Dominance Factors: The US market dominance results from its larger economy, advanced infrastructure, and higher technological adoption. Market share and growth potential are highest in the US for all segments, followed by Canada and then Mexico.

North America Logistics Contract Industry Product Landscape

The contract logistics market offers a wide range of services, including warehousing, transportation management, order fulfillment, and supply chain consulting. Recent innovations include the integration of AI-powered systems for route optimization, predictive analytics for inventory management, and the use of robotics for automated warehousing. These technologies enhance efficiency, reduce costs, and improve traceability, giving companies a competitive edge. Unique selling propositions increasingly involve customized solutions tailored to specific client needs and industry requirements.

Key Drivers, Barriers & Challenges in North America Logistics Contract Industry

Key Drivers: E-commerce growth, technological advancements (automation, AI, data analytics), and the increasing complexity of global supply chains are major drivers. Government initiatives promoting infrastructure development and trade also contribute.

Key Challenges and Restraints: Driver shortages, fluctuating fuel prices, rising labor costs, and port congestion pose significant operational challenges. Stringent regulatory compliance requirements, cybersecurity risks, and intense competition also impede growth. These factors can cause unpredictable delays and increased operating costs, with an estimated impact of xx million annually on profit margins.

Emerging Opportunities in North America Logistics Contract Industry

Growth opportunities lie in the expansion of e-commerce logistics, the growing demand for specialized services (e.g., cold chain logistics for pharmaceuticals), and the increasing adoption of sustainable logistics practices. Untapped markets exist in rural areas and underserved communities. The development of innovative solutions for last-mile delivery, utilizing drones or autonomous vehicles, presents further opportunities.

Growth Accelerators in the North America Logistics Contract Industry Industry

Technological advancements, strategic partnerships (e.g., collaborations between logistics providers and technology companies), and expansion into new geographic markets and service areas will drive long-term growth. Investments in sustainable practices (e.g., green transportation solutions) will increasingly attract customers and boost market share. Government policies supporting infrastructure development and technological innovation will also play a crucial role.

Key Players Shaping the North America Logistics Contract Industry Market

- DB Schenker

- Deutsche Post DHL Group (DHL Supply Chain)

- Neovia Logistics Services LLC

- SCI

- FedEx Corporation (FedEx Supply Chain)

- United Parcel Service Inc (UPS Supply Chain Solutions)

- Schnedier National

- 3 Other Companies (Key Information/Overview)

- Yusen Logistics Co Ltd

- Penske Logistics Inc

- Kuehne + Nagel International AG

- CEVA Logistics

- PiVAL International

- TIBA

- XPO Logistics Inc

- Americold

- Hellmann Worldwide Logistics GmbH & Co KG

- Geodis

- J B Hunt Transport Services Inc

- Ryder System Inc

Notable Milestones in North America Logistics Contract Industry Sector

- June 2022: DHL Supply Chain surpasses 100 million units picked by LocusBots in North American facilities.

- February 2022: Deutsche Post DHL Group invests USD 400 million to expand its healthcare logistics network by 3 million sq ft.

In-Depth North America Logistics Contract Industry Market Outlook

The North America contract logistics market is poised for continued growth, driven by sustained e-commerce expansion, technological innovation, and the increasing outsourcing of logistics functions. Strategic partnerships, investments in automation and sustainability, and expansion into new markets will be key to success. The focus on efficient, resilient, and technology-driven supply chains will further shape market dynamics and create lucrative opportunities for established and emerging players alike.

North America Logistics Contract Industry Segmentation

-

1. Type

- 1.1. Insourced

- 1.2. Outsourced

-

2. End User

- 2.1. Manufacturing and Automotive

- 2.2. Consumer Goods and Retail

- 2.3. High-tech

- 2.4. Healthcare and Pharmaceuticals

- 2.5. Other End Users

North America Logistics Contract Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

North America Logistics Contract Industry Regional Market Share

Geographic Coverage of North America Logistics Contract Industry

North America Logistics Contract Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.85% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Insourced

- 5.1.2. Outsourced

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Manufacturing and Automotive

- 5.2.2. Consumer Goods and Retail

- 5.2.3. High-tech

- 5.2.4. Healthcare and Pharmaceuticals

- 5.2.5. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Logistics Contract Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Insourced

- 6.1.2. Outsourced

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Manufacturing and Automotive

- 6.2.2. Consumer Goods and Retail

- 6.2.3. High-tech

- 6.2.4. Healthcare and Pharmaceuticals

- 6.2.5. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 DB Schenker

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Deutsche Post DHL Group (DHL Supply Chain)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Neovia Logistics Services LLC

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 SCI

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 FedEx Corporation (FedEx Supply Chain)

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 United Parcel Service Inc (UPS Supply Chain Solutions)

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Schnedier National*6 3 Other Companies (Key Information/Overview)

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Yusen Logistics Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Penske Logistics Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Kuehne + Nagel International AG

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 CEVA Logistics

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 PiVAL International

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 TIBA

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 XPO Logistics Inc

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Americold

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 Hellmann Worldwide Logistics GmbH & Co KG

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 Geodis

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 J B Hunt Transport Services Inc

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.19 Ryder System Inc

- 7.1.19.1. Company Overview

- 7.1.19.2. Products

- 7.1.19.3. Company Financials

- 7.1.19.4. SWOT Analysis

- 7.1.1 DB Schenker

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: North America Logistics Contract Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: North America Logistics Contract Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Logistics Contract Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: North America Logistics Contract Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: North America Logistics Contract Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: North America Logistics Contract Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: North America Logistics Contract Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: North America Logistics Contract Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States North America Logistics Contract Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Canada North America Logistics Contract Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Mexico North America Logistics Contract Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Logistics Contract Industry?

The projected CAGR is approximately 1.85%.

2. Which companies are prominent players in the North America Logistics Contract Industry?

Key companies in the market include DB Schenker, Deutsche Post DHL Group (DHL Supply Chain), Neovia Logistics Services LLC, SCI, FedEx Corporation (FedEx Supply Chain), United Parcel Service Inc (UPS Supply Chain Solutions), Schnedier National*6 3 Other Companies (Key Information/Overview), Yusen Logistics Co Ltd, Penske Logistics Inc, Kuehne + Nagel International AG, CEVA Logistics, PiVAL International, TIBA, XPO Logistics Inc, Americold, Hellmann Worldwide Logistics GmbH & Co KG, Geodis, J B Hunt Transport Services Inc, Ryder System Inc.

3. What are the main segments of the North America Logistics Contract Industry?

The market segments include Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 158.59 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increased Outsourcing of Services4.; Increasing Demand For Contract Logistics In Italy. France. And Poland4.; Growth Of Ecommerce Sector Across Europe.

6. What are the notable trends driving market growth?

Growing E-commerce in the Region Driving the Contract Logistics Market.

7. Are there any restraints impacting market growth?

4.; Increasing Competition In The European Contract Logistics Market.

8. Can you provide examples of recent developments in the market?

Jun 2022: DHL Supply Chain, in contract logistics in the Americas and a division of Deutsche Post DHL Group, revealed that LocusBots from Locus Robotics had selected more than 100 million units in its North American facilities. The achievement was made at the DHL facility in Hanover Township, Pennsylvania, while completing orders for a significant clothes retailer. The facility where the milestone was reached is one of over a dozen DHL locations in North America that employ more than 2,000 LocusBots-more than any other contract logistics provider.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Logistics Contract Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Logistics Contract Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Logistics Contract Industry?

To stay informed about further developments, trends, and reports in the North America Logistics Contract Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence