Key Insights

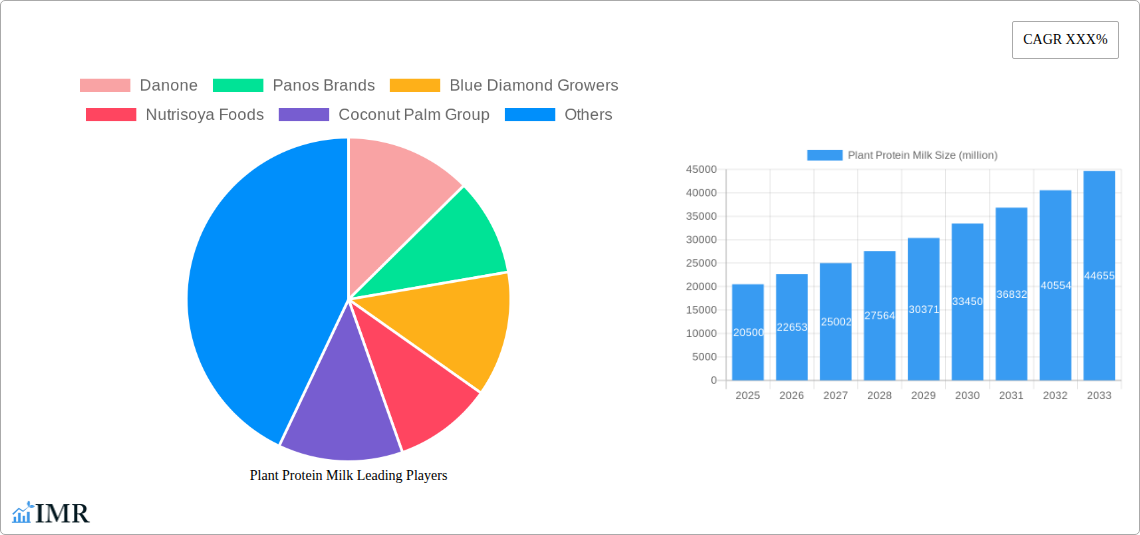

The global plant protein milk market is experiencing robust expansion, projected to reach an estimated USD 20,500 million by 2025, with a Compound Annual Growth Rate (CAGR) of approximately 10.5% anticipated between 2025 and 2033. This significant growth is primarily fueled by a confluence of escalating consumer awareness regarding health benefits, including lactose intolerance and dairy allergies, and a burgeoning demand for sustainable and ethically produced food alternatives. The "plant-based movement" is no longer a niche trend but a mainstream dietary shift, driven by increasing concerns over environmental impact, animal welfare, and the perceived health advantages of plant-derived proteins. This has propelled products like oat milk, almond milk, and soy milk to the forefront, capturing substantial market share. Furthermore, product innovation, including the development of novel flavors, fortified options, and ready-to-drink formats, continues to attract a wider consumer base, encompassing not only vegans and vegetarians but also flexitarians and health-conscious individuals seeking to diversify their protein sources.

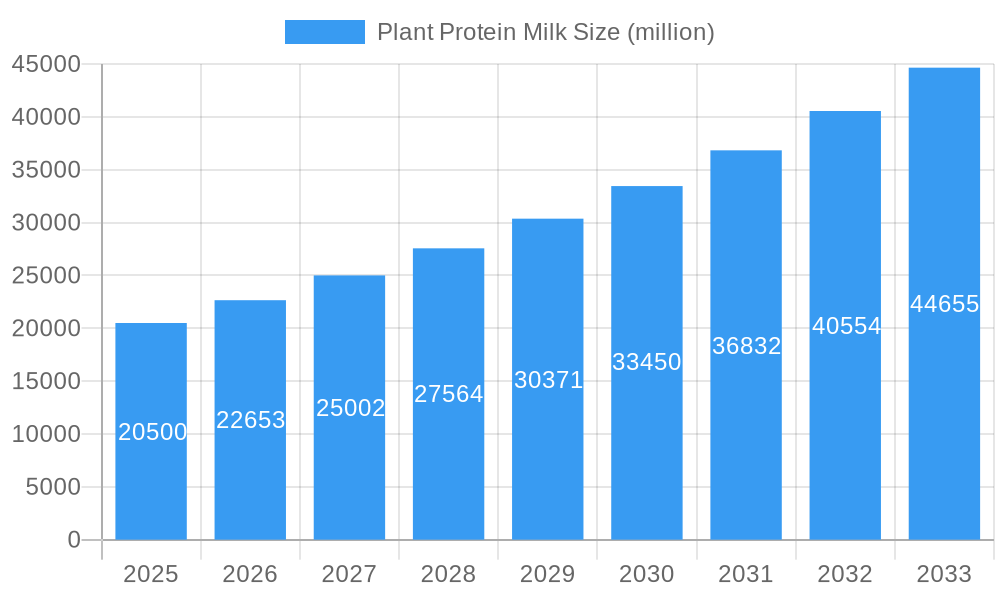

Plant Protein Milk Market Size (In Billion)

The market's trajectory is further bolstered by evolving distribution channels, with online sales platforms witnessing exponential growth, offering convenience and wider product availability. This digital shift complements traditional offline retail, ensuring accessibility across diverse consumer demographics. Key market drivers include increasing disposable incomes in emerging economies, leading to greater adoption of premium plant-based products, and supportive government initiatives promoting healthy lifestyles and sustainable agriculture. However, the market also faces certain restraints, such as the higher cost of some plant-based milk alternatives compared to conventional dairy milk and potential supply chain challenges related to sourcing raw ingredients. Despite these hurdles, the overwhelming positive consumer sentiment, coupled with continuous product development and expanding distribution networks, solidifies a promising outlook for the plant protein milk industry. The diverse range of applications, from beverages and smoothies to cooking and baking, underscores its versatility and integral role in modern diets.

Plant Protein Milk Company Market Share

Plant Protein Milk Market: A Comprehensive Analysis (2019-2033)

This in-depth report provides an indispensable analysis of the global Plant Protein Milk market, offering critical insights for industry professionals, investors, and stakeholders. Covering a comprehensive study period from 2019 to 2033, with a base year of 2025, this report dissects market dynamics, growth trends, regional dominance, product innovations, and key players. We delve into the nuances of market concentration, technological advancements, regulatory landscapes, competitive substitutes, end-user demographics, and mergers and acquisitions, presenting quantitative data in millions of units and qualitative factors to drive strategic decision-making. The report further explores the evolution of market size, adoption rates, technological disruptions, and consumer behavior shifts. Identifying dominant regions, countries, and segments across online and offline sales, and types including oat, almond, coconut, and soy milk, we provide a granular understanding of market penetration and growth potential. Product innovations, unique selling propositions, and technological advancements are detailed, alongside a thorough examination of key drivers, barriers, challenges, and emerging opportunities. Finally, the report spotlights growth accelerators and notable milestones, culminating in a robust market outlook for sustained growth.

Plant Protein Milk Market Dynamics & Structure

The global plant protein milk market exhibits a moderately concentrated structure, with a blend of established dairy alternatives giants and emerging specialized brands vying for market share. Technological innovation acts as a primary driver, fueled by advancements in extraction processes for diverse plant bases, flavor enhancement, and nutritional fortification. Regulatory frameworks, particularly those pertaining to labeling and health claims, play a significant role in shaping consumer trust and market access. Competitive product substitutes extend beyond traditional dairy to include other plant-based beverages and functional drinks, necessitating continuous product differentiation. End-user demographics are increasingly diverse, encompassing health-conscious consumers, vegans, lactose-intolerant individuals, and those seeking sustainable food options. Mergers and acquisitions (M&A) are a notable trend, with larger food and beverage companies acquiring smaller, innovative plant-based brands to expand their portfolios and leverage their expertise.

- Market Concentration: Top 10 companies hold approximately 60% of the market share, indicating a competitive yet manageable landscape.

- Technological Innovation Drivers: Improved palatability, extended shelf life through aseptic processing, and enhanced protein content through fortification are key innovation areas.

- Regulatory Frameworks: Evolving food safety standards and clear labeling requirements for plant-based claims are crucial.

- Competitive Product Substitutes: Dairy milk, other plant-based beverages (e.g., rice milk, hemp milk), and fortified juices.

- End-User Demographics: Predominantly millennials and Gen Z, with growing adoption among older demographics and families.

- M&A Trends: In the historical period (2019-2024), there were an estimated 15 significant M&A deals valued at over $100 million each, indicating consolidation and strategic expansion by larger players.

Plant Protein Milk Growth Trends & Insights

The plant protein milk market has witnessed exponential growth over the historical period (2019-2024), propelled by a confluence of escalating consumer health awareness, ethical considerations surrounding animal agriculture, and environmental sustainability concerns. As consumers increasingly scrutinize ingredient lists and seek alternatives to conventional dairy, plant-based milk has transitioned from a niche product to a mainstream staple. This shift is vividly reflected in the market size evolution, which is projected to reach an estimated value of $25,000 million in 2025 and grow at a Compound Annual Growth Rate (CAGR) of approximately 12.5% during the forecast period (2025-2033). Adoption rates have surged globally, with market penetration in developed economies exceeding 35% and showing significant upward momentum in emerging markets. Technological disruptions have been pivotal, encompassing advancements in sourcing and processing of diverse plant bases like oats and almonds, leading to improved taste, texture, and nutritional profiles. Innovations in fermentation techniques and allergen-free formulations further broaden consumer appeal. Consumer behavior shifts are characterized by a growing preference for functional beverages, with plant protein milk being sought not just for its dairy-alternative properties but also for its inherent nutritional benefits, such as higher protein content, lower saturated fat, and essential vitamins and minerals. The demand for clean labels and sustainable sourcing practices further influences purchasing decisions, driving manufacturers to adopt more transparent and eco-friendly production methods. The perceived health benefits, including improved digestion and reduced risk of certain chronic diseases, are significant psychological drivers encouraging trial and repeat purchases. Furthermore, the convenience offered by ready-to-drink formats and the increasing availability across various retail channels, from supermarkets to online platforms, contribute to its widespread acceptance.

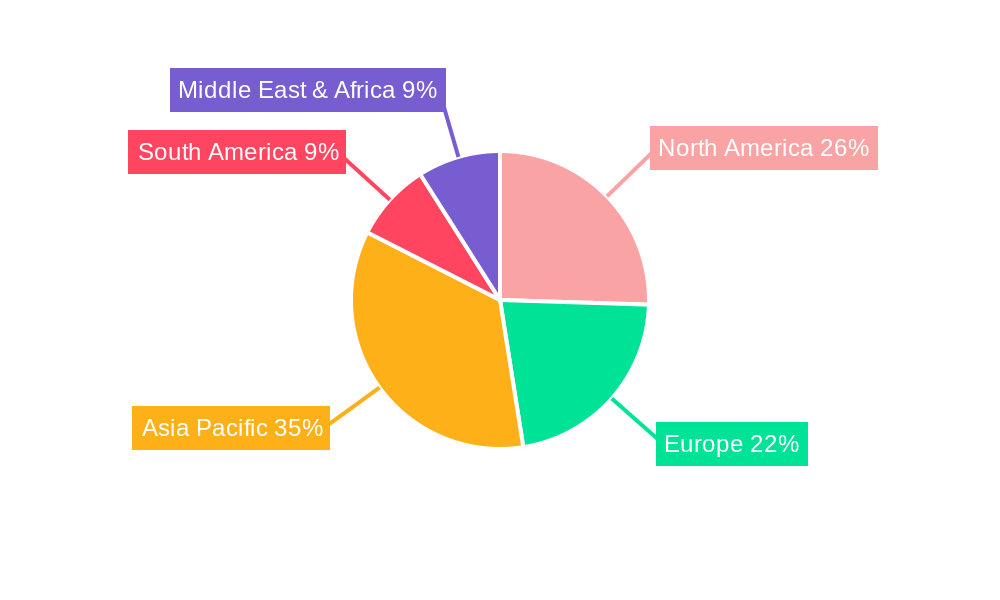

Dominant Regions, Countries, or Segments in Plant Protein Milk

North America, particularly the United States, stands out as the dominant region driving the global plant protein milk market. This dominance is attributed to a confluence of factors, including a highly health-conscious consumer base, robust awareness of lactose intolerance and dairy allergies, and a well-established infrastructure for plant-based food production and distribution. The United States, with an estimated market share of over 30% in 2025, benefits from proactive regulatory environments that encourage innovation and transparency in food labeling, coupled with significant investment in research and development by key players. Economic policies supportive of sustainable agriculture and the growing popularity of vegan and flexitarian diets further bolster market growth.

Among the various types of plant protein milk, Oat Milk has emerged as a leading segment, accounting for approximately 35% of the global market in 2025. Its rise is attributed to its creamy texture, neutral flavor profile, and versatility in both culinary applications and direct consumption, making it a close substitute for dairy milk. The segment's growth potential is immense, driven by continuous product innovation, including barista-edition formulations and fortified variants with added vitamins and calcium.

- Dominant Region: North America (United States, Canada)

- Key Drivers: High consumer awareness of health and wellness, strong vegan/vegetarian adoption, supportive regulatory landscape, widespread availability, and significant R&D investment.

- Market Share (2025 Estimate): Approximately 30% of the global market.

- Growth Potential: Continued strong growth fueled by evolving dietary trends and product innovation.

- Dominant Segment (Type): Oat Milk

- Key Drivers: Superior taste and texture, versatility in consumption and culinary uses, strong marketing efforts, and perceived health benefits.

- Market Share (2025 Estimate): Approximately 35% of the global market.

- Growth Potential: Sustained high growth as manufacturers expand product lines and refine formulations.

While Oat Milk leads, Almond Milk remains a significant segment, holding an estimated 25% market share in 2025, owing to its long-standing popularity and availability. Coconut Milk and Soy Milk also represent substantial portions of the market, catering to specific consumer preferences and culinary applications, with Soy Milk historically a pioneer in the plant-based beverage category. The Application segment of Online Sales is experiencing rapid growth, estimated to capture 25% of the market in 2025 and projected to expand at a CAGR of 15% from 2025-2033, reflecting the increasing preference for e-commerce convenience and personalized shopping experiences. Offline sales continue to dominate, however, with a projected 75% market share in 2025.

Plant Protein Milk Product Landscape

The plant protein milk product landscape is characterized by a rapid influx of innovative offerings, focusing on enhanced nutritional profiles, superior taste, and diverse plant bases. Brands are increasingly fortifying their beverages with essential vitamins (D, B12), minerals (calcium), and protein, catering to the growing demand for functional foods. Unique selling propositions often revolve around specific plant sources like oat, almond, soy, and coconut, with brands differentiating through extraction methods, protein content, and allergen-free formulations. Technological advancements are evident in the development of barista-friendly options with optimal foaming capabilities and the introduction of single-serve, ready-to-drink formats for on-the-go consumption. Performance metrics are measured by taste, texture, protein content, and shelf stability, with ongoing research aiming to mimic the creaminess and mouthfeel of traditional dairy milk.

Key Drivers, Barriers & Challenges in Plant Protein Milk

Key Drivers: The plant protein milk market is primarily propelled by the escalating global demand for healthier and more sustainable food choices. Growing consumer awareness regarding the environmental impact of dairy farming, coupled with increasing rates of lactose intolerance and dairy allergies, are significant demand generators. Technological advancements in processing and ingredient formulation are enhancing taste, texture, and nutritional value, making plant-based alternatives more appealing. Government initiatives promoting plant-based diets and the expansion of distribution channels, especially online retail, are further accelerating market growth.

Barriers & Challenges: Despite its robust growth, the plant protein milk market faces several challenges. Supply chain disruptions and the availability of raw materials can impact production costs and consistency. Stringent regulatory hurdles concerning labeling, health claims, and food safety across different regions can pose market entry barriers. Intense competition from both established dairy giants and numerous plant-based startups necessitates continuous innovation and aggressive marketing strategies. Furthermore, achieving price parity with conventional dairy milk remains a challenge for some plant-based options, limiting accessibility for price-sensitive consumers. The estimated impact of supply chain volatility on production costs is around 5-8% annually.

Emerging Opportunities in Plant Protein Milk

Emerging opportunities lie in tapping into the burgeoning demand for plant-based protein in emerging economies, where awareness and adoption rates are still in their nascent stages. The development of novel plant sources for milk extraction, beyond the traditional oat and almond, presents a significant avenue for product diversification. Innovations in functional plant protein milk, such as those fortified with adaptogens, probiotics, or specific micronutrients tailored for different life stages (e.g., pregnancy, athletes), hold immense potential. Furthermore, exploring sustainable packaging solutions and transparent sourcing narratives can resonate with eco-conscious consumers, creating brand loyalty.

Growth Accelerators in the Plant Protein Milk Industry

Several key catalysts are accelerating the growth of the plant protein milk industry. Technological breakthroughs in enzyme processing and plant protein isolation are leading to improved sensory attributes and nutritional completeness. Strategic partnerships between ingredient suppliers and beverage manufacturers are fostering innovation and scalability. The expanding direct-to-consumer (DTC) sales channels and the growing presence in foodservice, particularly in coffee shops and restaurants, are significantly broadening market reach. Moreover, aggressive marketing campaigns highlighting the health and environmental benefits of plant protein milk are effectively driving consumer adoption and brand preference.

Key Players Shaping the Plant Protein Milk Market

- Danone

- Panos Brands

- Blue Diamond Growers

- Nutrisoya Foods

- Coconut Palm Group

- Cheng De Lolo Co., Ltd.

- Vitasoy

- OCAK

- Califia Farms

- Earth’s Own Food Company

- SunOpta

- Ripple Foods

- Marusan-Ai Co. Ltd

- Orgain

- Koia

- Oatly

- Elmhurst Milked Direct

- Kikkoman Corporation

- Milkadamia

Notable Milestones in Plant Protein Milk Sector

- 2019: Increased regulatory focus on plant-based labeling clarity in North America and Europe, leading to revised marketing strategies by key players.

- 2020: Significant surge in online sales of plant protein milk globally, driven by pandemic-induced shopping habits and increased e-commerce penetration.

- 2021: Introduction of new barista-grade oat milk formulations by multiple brands, enhancing their appeal to coffee shops and home baristas.

- 2022: Acquisition of smaller innovative plant-based milk brands by major food conglomerates, signaling industry consolidation and strategic portfolio expansion.

- 2023: Greater emphasis on product fortification with added vitamins, minerals, and functional ingredients to cater to health-conscious consumers.

- 2024: Expansion of plant protein milk into emerging markets, with targeted marketing and product localization efforts.

In-Depth Plant Protein Milk Market Outlook

The future outlook for the plant protein milk market is exceptionally bright, poised for sustained and robust growth. Growth accelerators, including ongoing technological innovations in taste and texture enhancement, alongside advancements in the extraction and fortification of diverse plant bases, will continue to fuel consumer demand. Strategic partnerships and expanded distribution networks, encompassing both online and offline channels, will broaden market access and penetration. The increasing consumer preference for sustainable and ethically sourced products, coupled with evolving dietary trends towards plant-centric diets, will solidify plant protein milk’s position as a mainstream beverage category. The market is projected to reach an estimated $30,000 million by 2028, driven by continued innovation and increasing consumer awareness.

Plant Protein Milk Segmentation

-

1. Application

- 1.1. Online Sales

- 1.2. Offline Sales

-

2. Type

- 2.1. Oat Milk

- 2.2. Almond Milk

- 2.3. Coconut Milk

- 2.4. Soy Milk

- 2.5. Others

Plant Protein Milk Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Plant Protein Milk Regional Market Share

Geographic Coverage of Plant Protein Milk

Plant Protein Milk REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XXX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Plant Protein Milk Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Online Sales

- 5.1.2. Offline Sales

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Oat Milk

- 5.2.2. Almond Milk

- 5.2.3. Coconut Milk

- 5.2.4. Soy Milk

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Plant Protein Milk Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Online Sales

- 6.1.2. Offline Sales

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Oat Milk

- 6.2.2. Almond Milk

- 6.2.3. Coconut Milk

- 6.2.4. Soy Milk

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Plant Protein Milk Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Online Sales

- 7.1.2. Offline Sales

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Oat Milk

- 7.2.2. Almond Milk

- 7.2.3. Coconut Milk

- 7.2.4. Soy Milk

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Plant Protein Milk Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Online Sales

- 8.1.2. Offline Sales

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Oat Milk

- 8.2.2. Almond Milk

- 8.2.3. Coconut Milk

- 8.2.4. Soy Milk

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Plant Protein Milk Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Online Sales

- 9.1.2. Offline Sales

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Oat Milk

- 9.2.2. Almond Milk

- 9.2.3. Coconut Milk

- 9.2.4. Soy Milk

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Plant Protein Milk Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Online Sales

- 10.1.2. Offline Sales

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Oat Milk

- 10.2.2. Almond Milk

- 10.2.3. Coconut Milk

- 10.2.4. Soy Milk

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Danone

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Panos Brands

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Blue Diamond Growers

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Nutrisoya Foods

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Coconut Palm Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Cheng De Lolo Co

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Ltd.

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Vitasoy

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 OCAK

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Califia Farms

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Earth’s Own Food Company

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 SunOpta

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Ripple Foods

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Marusan-Ai Co. Ltd

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Orgain

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Koia

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Oatly

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Elmhurst Milked Direct

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Kikkoman Corporation

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Milkadamia

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 Danone

List of Figures

- Figure 1: Global Plant Protein Milk Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Plant Protein Milk Revenue (million), by Application 2025 & 2033

- Figure 3: North America Plant Protein Milk Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Plant Protein Milk Revenue (million), by Type 2025 & 2033

- Figure 5: North America Plant Protein Milk Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Plant Protein Milk Revenue (million), by Country 2025 & 2033

- Figure 7: North America Plant Protein Milk Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Plant Protein Milk Revenue (million), by Application 2025 & 2033

- Figure 9: South America Plant Protein Milk Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Plant Protein Milk Revenue (million), by Type 2025 & 2033

- Figure 11: South America Plant Protein Milk Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Plant Protein Milk Revenue (million), by Country 2025 & 2033

- Figure 13: South America Plant Protein Milk Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Plant Protein Milk Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Plant Protein Milk Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Plant Protein Milk Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Plant Protein Milk Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Plant Protein Milk Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Plant Protein Milk Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Plant Protein Milk Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Plant Protein Milk Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Plant Protein Milk Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Plant Protein Milk Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Plant Protein Milk Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Plant Protein Milk Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Plant Protein Milk Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Plant Protein Milk Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Plant Protein Milk Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Plant Protein Milk Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Plant Protein Milk Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Plant Protein Milk Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Plant Protein Milk Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Plant Protein Milk Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Plant Protein Milk Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Plant Protein Milk Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Plant Protein Milk Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Plant Protein Milk Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Plant Protein Milk Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Plant Protein Milk Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Plant Protein Milk Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Plant Protein Milk Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Plant Protein Milk Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Plant Protein Milk Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Plant Protein Milk Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Plant Protein Milk Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Plant Protein Milk Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Plant Protein Milk Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Plant Protein Milk Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Plant Protein Milk Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Plant Protein Milk Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Plant Protein Milk?

The projected CAGR is approximately XXX%.

2. Which companies are prominent players in the Plant Protein Milk?

Key companies in the market include Danone, Panos Brands, Blue Diamond Growers, Nutrisoya Foods, Coconut Palm Group, Cheng De Lolo Co, Ltd., Vitasoy, OCAK, Califia Farms, Earth’s Own Food Company, SunOpta, Ripple Foods, Marusan-Ai Co. Ltd, Orgain, Koia, Oatly, Elmhurst Milked Direct, Kikkoman Corporation, Milkadamia.

3. What are the main segments of the Plant Protein Milk?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Plant Protein Milk," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Plant Protein Milk report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Plant Protein Milk?

To stay informed about further developments, trends, and reports in the Plant Protein Milk, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence