Key Insights

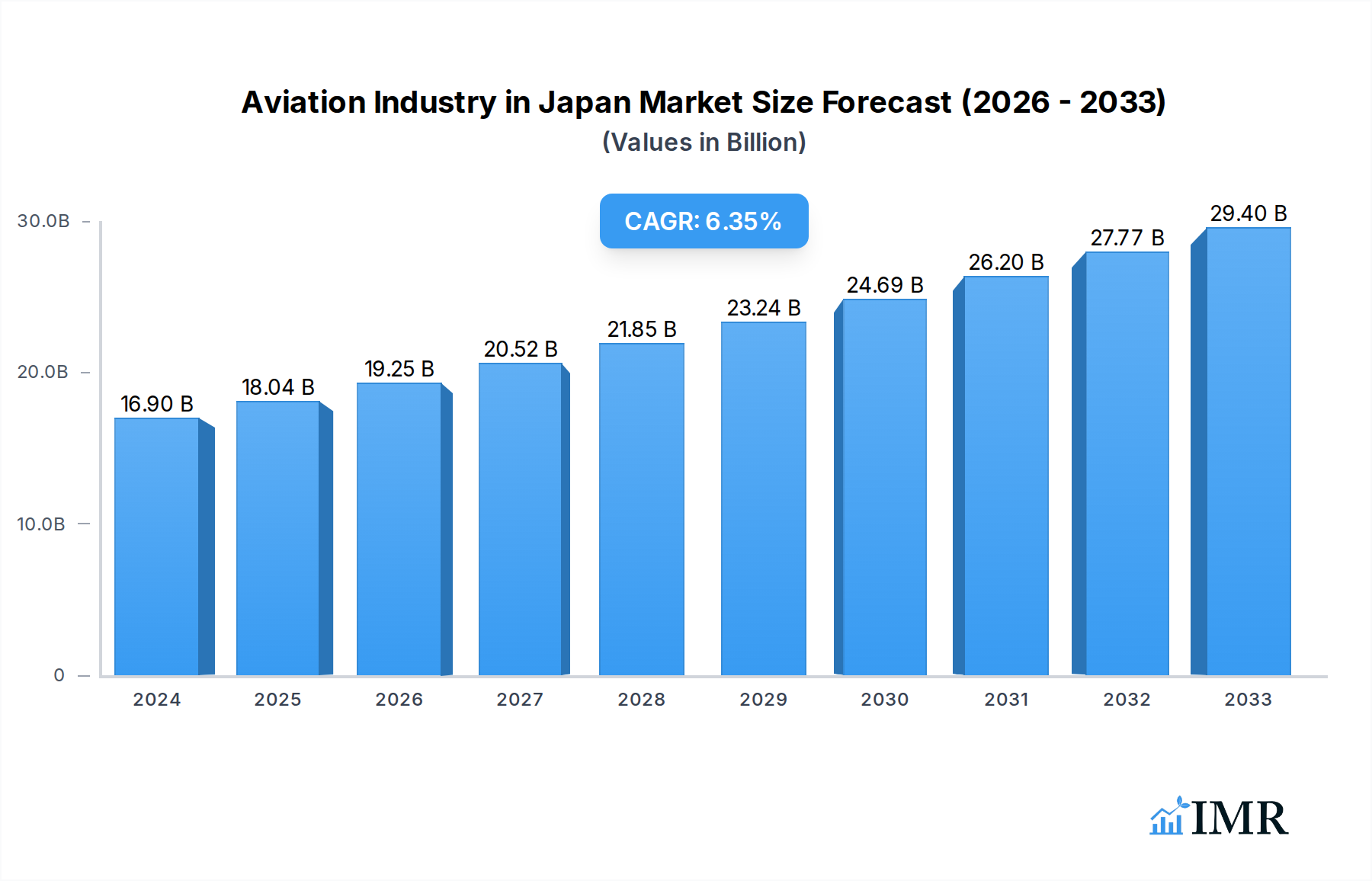

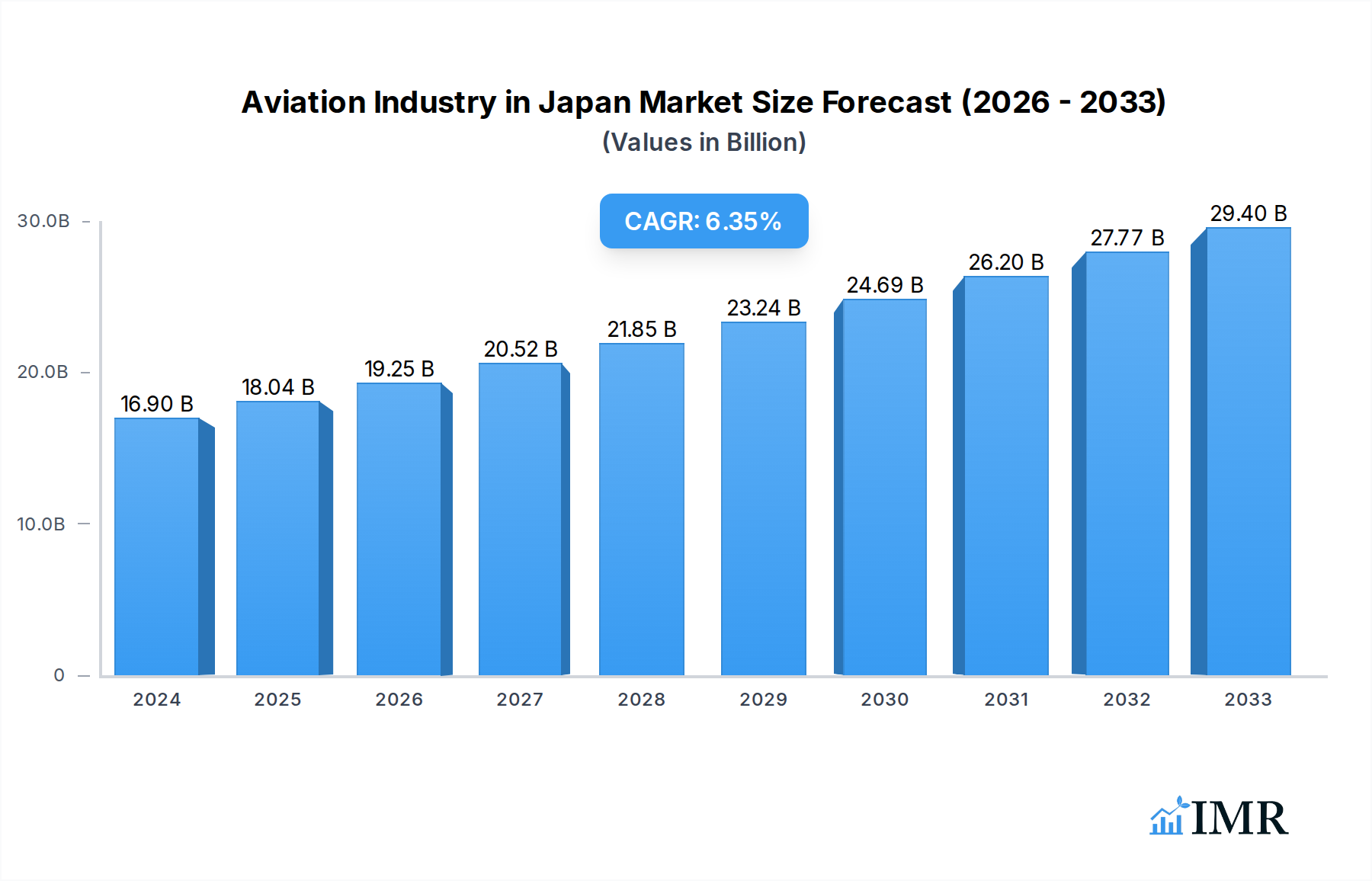

The global aviation industry is poised for substantial growth, with a projected market size of USD 16.9 billion in 2024, driven by an estimated 6.7% CAGR through 2033. This expansion is largely fueled by increasing air travel demand, particularly in emerging economies, and the continuous technological advancements in aircraft design and manufacturing. Key drivers include the growing middle class, expanding global trade routes necessitating efficient air cargo, and the ongoing need for defense and military aviation capabilities. Furthermore, the resurgence of tourism post-pandemic and the sustained growth in business travel are significant contributors to the industry's upward trajectory. Investments in sustainable aviation technologies and the development of new aircraft models capable of enhanced fuel efficiency and reduced emissions are also shaping the market landscape.

Aviation Industry in Japan Market Size (In Billion)

Within this dynamic global context, the Japanese aviation industry plays a crucial role, contributing significantly to both commercial and military aviation sectors. While specific Japanese market data is not detailed here, it is logical to infer that Japan, as a technologically advanced and economically strong nation with a well-developed aerospace sector, actively participates in and benefits from these global trends. The market in Japan is likely influenced by factors such as a robust domestic travel market, a strong presence in aircraft manufacturing and component supply, and a growing demand for business and general aviation. The country's commitment to innovation in areas like electric and hybrid-electric aircraft, alongside its participation in international aerospace collaborations, positions it to capitalize on the overall industry growth. The segment breakdown suggests significant opportunities across commercial, general, and military aviation, each with unique growth drivers and challenges.

Aviation Industry in Japan Company Market Share

This comprehensive report delves into the dynamic Japanese aviation industry, offering an in-depth analysis of its market structure, growth trajectory, and future potential. Covering the period from 2019 to 2033, with a base year of 2025, this report provides critical insights for stakeholders seeking to navigate this complex and evolving sector. We examine parent and child market segments within commercial aviation, general aviation, and military aviation, presenting all values in billion units for clarity.

Aviation Industry in Japan Market Dynamics & Structure

The Japanese aviation industry is characterized by a moderate market concentration, with a few major players like Kawasaki Heavy Industries Ltd. dominating key manufacturing segments. Technological innovation is a primary driver, fueled by substantial government investment in R&D and the pursuit of advanced aerospace technologies, particularly in areas like eVTOL (electric Vertical Take-Off and Landing) aircraft and next-generation passenger aircraft. Regulatory frameworks, primarily overseen by the Ministry of Land, Infrastructure, Transport and Tourism (MLIT), promote safety and efficiency, though stringent certification processes can present innovation barriers. Competitive product substitutes exist, primarily in the form of improved older technologies and alternative transportation modes for certain domestic routes. End-user demographics are shifting, with an aging population influencing demand for accessible air travel and a growing emphasis on sustainable aviation solutions. Mergers and acquisitions (M&A) trends are relatively subdued, focusing more on strategic partnerships and joint ventures for technology development rather than outright company takeovers.

- Market Concentration: Moderate, with key players dominating specific sub-segments.

- Technological Innovation: High, driven by government initiatives and R&D investment.

- Regulatory Framework: Robust safety and efficiency focus, potentially impacting new entrants.

- Competitive Product Substitutes: Limited for long-haul, but emerging alternatives for short-haul.

- End-User Demographics: Shifting, with an aging population and demand for sustainability.

- M&A Trends: Focus on strategic partnerships and R&D collaborations.

Aviation Industry in Japan Growth Trends & Insights

The Japanese aviation market is projected to experience robust growth, driven by a combination of factors including increasing passenger traffic, a growing defense budget, and advancements in aerospace technology. The market size evolution is expected to see a healthy CAGR throughout the forecast period. Adoption rates for new technologies, such as advanced composite materials and more fuel-efficient commercial aircraft, are on the rise, significantly impacting operational costs and environmental footprints. Technological disruptions are at the forefront, with the development of autonomous flight systems, sustainable aviation fuels (SAFs), and advanced manufacturing techniques reshaping the industry. Consumer behavior shifts are evident, with a growing preference for eco-friendly travel options and a demand for enhanced in-flight experiences. The integration of digital technologies across the aviation value chain, from manufacturing to passenger services, will further accelerate market penetration and optimize operational efficiencies.

The Japanese aviation industry is poised for significant expansion. Market size is anticipated to grow from an estimated $75.2 billion in 2025 to $110.5 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 4.9% during the forecast period. This growth is underpinned by a burgeoning demand for both commercial aviation and military aviation solutions. In the commercial aviation segment, passenger traffic is projected to rebound strongly post-pandemic, with an increasing need for modern, fuel-efficient passenger aircraft, particularly narrowbody aircraft for domestic and regional routes, and widebody aircraft for international travel. Freighter aircraft demand is also expected to rise, driven by e-commerce growth and global supply chain dynamics.

Within general aviation, the market for business jets is set to expand, catering to the sophisticated needs of Japanese corporations and high-net-worth individuals. Large jets, mid-size jets, and light jets will all see demand, supported by advancements in performance and cabin comfort. Piston fixed-wing aircraft will continue to serve niche markets and training requirements.

The military aviation segment is a key growth driver, with Japan increasing its defense spending to address evolving geopolitical landscapes. This will translate into higher demand for multi-role aircraft, training aircraft, and advanced rotorcraft, including multi-mission helicopters and transport helicopters. The ongoing modernization of the Japan Air Self-Defense Force (JASDF) and the Japan Maritime Self-Defense Force (JMSDF) will further fuel this segment.

Technological disruptions are playing a crucial role, with innovations in electric and hybrid-electric propulsion, advanced materials, and digitalization shaping the future of aircraft design and operation. The adoption of these technologies will enhance efficiency, reduce emissions, and improve safety across all aviation segments. Consumer behavior is also evolving, with a growing emphasis on sustainable travel options and personalized in-flight experiences, which will influence aircraft configuration and service offerings.

Dominant Regions, Countries, or Segments in Aviation Industry in Japan

Commercial Aviation, specifically Passenger Aircraft, is the dominant segment driving growth within the Japanese aviation industry. This dominance is fueled by a confluence of economic policies, demographic trends, and infrastructure development.

- Passenger Aircraft (Commercial Aviation): This segment is the primary engine of growth due to Japan's high population density, a robust tourism industry, and a strong domestic travel culture.

- Narrowbody Aircraft: These aircraft are crucial for connecting major metropolitan hubs and serving the extensive domestic air travel network. Their efficiency and versatility make them ideal for the high-frequency routes prevalent in Japan. The demand is further boosted by airline fleet modernization programs aimed at reducing operational costs and environmental impact.

- Widebody Aircraft: Essential for international long-haul routes, connecting Japan to global markets and supporting its role as a major economic power. Growing inbound and outbound tourism, alongside international business travel, underpins demand for these aircraft.

- General Aviation: While smaller in scale compared to commercial aviation, Business Jets are experiencing significant growth. This is attributed to the presence of numerous multinational corporations and a wealthy demographic seeking efficient and flexible travel solutions.

- Large Jet, Mid-Size Jet, Light Jet: Each category caters to specific corporate and private travel needs, from long-distance executive travel to regional point-to-point connectivity.

- Military Aviation: This segment plays a vital role, driven by national security imperatives and ongoing modernization efforts.

- Multi-Role Aircraft: Essential for maintaining air superiority and responding to diverse threats, these aircraft are a cornerstone of Japan's defense strategy.

- Rotorcraft: Multi-mission helicopters are critical for search and rescue, troop transport, and special operations, while transport helicopters are vital for logistical support.

The dominance of Passenger Aircraft is further amplified by government initiatives promoting air travel as a key component of the nation's transportation infrastructure. Investments in airport modernization, air traffic management systems, and the promotion of sustainable aviation practices all contribute to the sector's sustained growth. The high adoption rate of advanced technologies by Japanese airlines ensures that the Passenger Aircraft segment remains at the cutting edge of aviation innovation, further solidifying its leading position.

Aviation Industry in Japan Product Landscape

The Japanese aviation product landscape is characterized by sophisticated technological advancements and a focus on high-performance, reliable aircraft. Innovations span across commercial, general, and military sectors. In commercial aviation, advancements in aerodynamics, engine efficiency, and lightweight composite materials are leading to the development of more fuel-efficient and quieter passenger aircraft. The rise of sustainable aviation fuels (SAFs) and electric/hybrid-electric propulsion technologies is shaping the future of aircraft design. For general aviation, the focus is on enhancing cabin comfort, connectivity, and operational range for business jets. Military applications are seeing the integration of advanced avionics, enhanced survivability features, and multi-role capabilities in multi-role aircraft and rotorcraft. Unique selling propositions often lie in the precision engineering, stringent quality control, and the integration of cutting-edge digital technologies by Japanese manufacturers.

Key Drivers, Barriers & Challenges in Aviation Industry in Japan

Key Drivers:

- Technological Advancements: Continuous innovation in propulsion systems, materials science, and avionics.

- Government Support: Robust R&D funding and strategic initiatives to boost aerospace capabilities.

- Growing Defense Expenditure: Increased investment in modern military aircraft and defense systems.

- Tourism Growth: Rising inbound and outbound tourism driving demand for commercial aviation.

- Economic Stability: A strong and diversified economy supports investment in aviation infrastructure and services.

Barriers & Challenges:

- High Development Costs: The capital-intensive nature of aerospace R&D and manufacturing presents significant financial hurdles.

- Strict Regulatory Environment: Stringent safety and environmental regulations, while crucial, can extend development and certification timelines.

- Global Competition: Intense competition from established international aerospace giants like Boeing and Airbus.

- Supply Chain Vulnerabilities: Reliance on global supply chains can lead to disruptions and price volatility.

- Skilled Workforce Shortage: A potential deficit in highly skilled engineers and technicians needed for advanced aerospace manufacturing.

Emerging Opportunities in Aviation Industry in Japan

Emerging opportunities in the Japanese aviation industry lie in the burgeoning urban air mobility (UAM) market, with the development of eVTOL aircraft for passenger transport and cargo delivery in congested urban areas. The increasing focus on sustainability presents a significant opportunity for companies investing in SAF production and the development of electric and hybrid-electric propulsion systems. Furthermore, the growing demand for advanced training solutions for both civilian and military pilots, coupled with the integration of AI and simulation technologies, opens up new avenues in the training aircraft and simulation markets. Japan's advanced robotics and automation expertise also positions it well to lead in the development of next-generation manufacturing processes for aircraft components.

Growth Accelerators in the Aviation Industry in Japan Industry

Growth in the Japanese aviation industry is being significantly accelerated by a potent combination of factors. Strategic partnerships and collaborations between domestic aerospace manufacturers and international players are fostering knowledge transfer and accelerating the development of cutting-edge technologies, particularly in areas like sustainable aviation and advanced materials. Government-led initiatives, such as the promotion of regional aviation and the development of eVTOL infrastructure, are creating new market segments and stimulating investment. Furthermore, the continuous push for greater fuel efficiency and reduced environmental impact in commercial aviation is driving innovation in aircraft design and engine technology, leading to the adoption of more advanced and sustainable solutions.

Key Players Shaping the Aviation Industry in Japan Market

- Textron Inc.

- Lockheed Martin Corporation

- Airbus SE

- The Boeing Company

- Bombardier Inc.

- ATR

- Kawasaki Heavy Industries Ltd.

Notable Milestones in Aviation Industry in Japan Sector

- December 2022: The US Army awarded a contract to Textron Inc.'s Bell unit for next-generation helicopters, a significant development in the "Future Vertical Lift" competition aimed at replacing UH-60 Black Hawk utility helicopters.

- November 2022: Boeing was awarded a contract to deliver two additional KC-46A Pegasus tankers to the Japan Air Self-Defense Force (JASDF), bringing the total on contract for Japan to six.

- November 2022: Bell Textron Inc. (a Textron Inc. company) agreed to sell 10 Bell 505 helicopters to the Royal Jordanian Air Force (RJAF) at SOFEX in Jordan, highlighting global demand for their rotorcraft.

In-Depth Aviation Industry in Japan Market Outlook

The future outlook for the Japanese aviation industry is exceptionally bright, underpinned by a strong foundation of technological prowess and strategic foresight. The continued investment in military aviation modernization, driven by evolving geopolitical dynamics, will ensure sustained demand for advanced defense platforms. In commercial aviation, the imperative for sustainability will accelerate the adoption of greener technologies and aircraft, creating opportunities for innovation in SAFs and electric propulsion. The anticipated growth in both domestic and international passenger traffic will further bolster the market. Emerging sectors like urban air mobility offer transformative potential, positioning Japan as a leader in the next generation of air transport. Strategic collaborations and a commitment to research and development will be key to realizing this expansive market potential and solidifying Japan's position as a global aerospace powerhouse.

Aviation Industry in Japan Segmentation

-

1. Aircraft Type

-

1.1. Commercial Aviation

-

1.1.1. By Sub Aircraft Type

- 1.1.1.1. Freighter Aircraft

-

1.1.1.2. Passenger Aircraft

-

1.1.1.2.1. By Body Type

- 1.1.1.2.1.1. Narrowbody Aircraft

- 1.1.1.2.1.2. Widebody Aircraft

-

1.1.1.2.1. By Body Type

-

1.1.1. By Sub Aircraft Type

-

1.2. General Aviation

-

1.2.1. Business Jets

- 1.2.1.1. Large Jet

- 1.2.1.2. Light Jet

- 1.2.1.3. Mid-Size Jet

- 1.2.2. Piston Fixed-Wing Aircraft

- 1.2.3. Others

-

1.2.1. Business Jets

-

1.3. Military Aviation

- 1.3.1. Multi-Role Aircraft

- 1.3.2. Training Aircraft

- 1.3.3. Transport Aircraft

-

1.3.4. Rotorcraft

- 1.3.4.1. Multi-Mission Helicopter

- 1.3.4.2. Transport Helicopter

-

1.1. Commercial Aviation

Aviation Industry in Japan Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

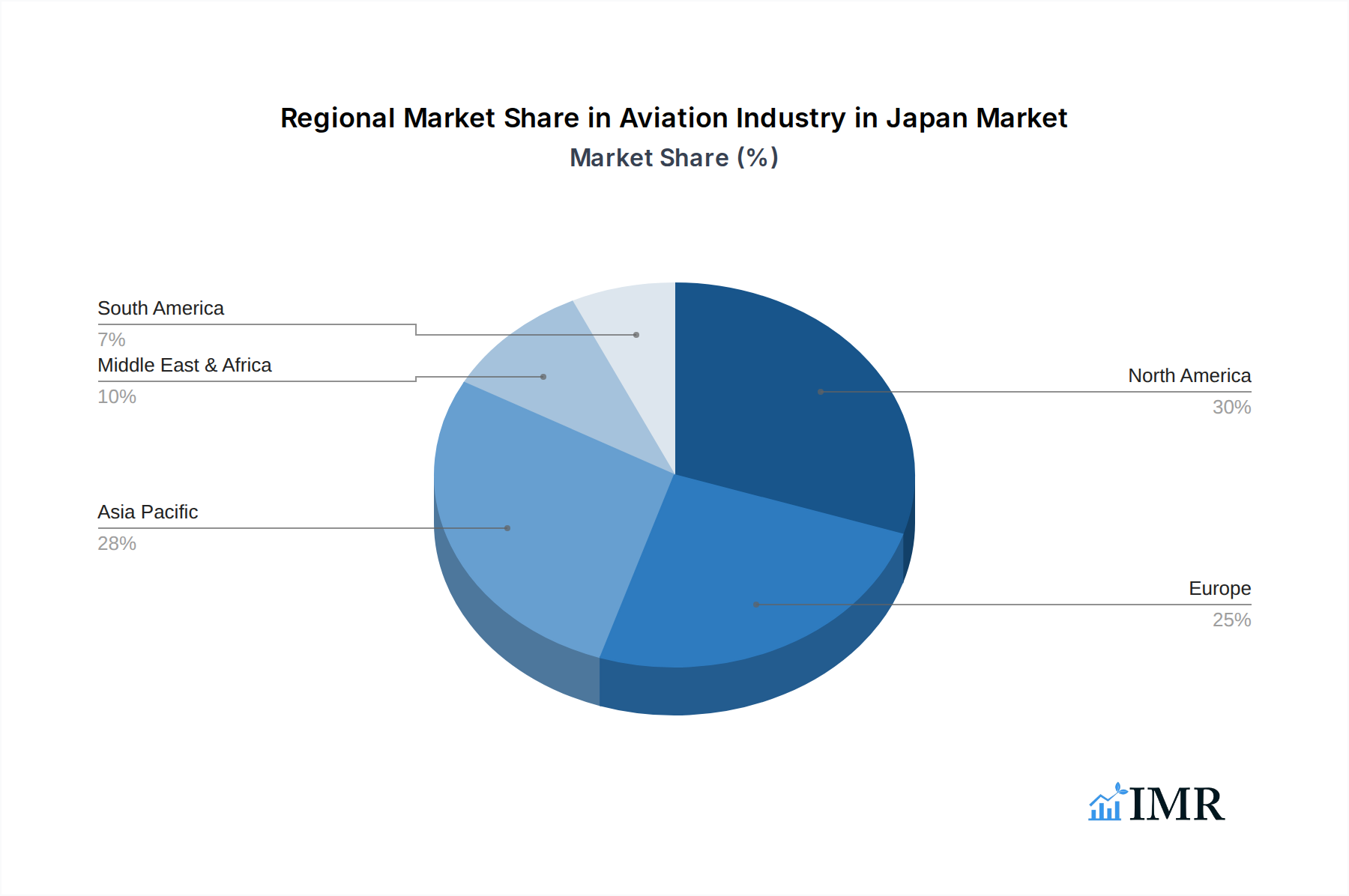

Aviation Industry in Japan Regional Market Share

Geographic Coverage of Aviation Industry in Japan

Aviation Industry in Japan REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 5.1.1. Commercial Aviation

- 5.1.1.1. By Sub Aircraft Type

- 5.1.1.1.1. Freighter Aircraft

- 5.1.1.1.2. Passenger Aircraft

- 5.1.1.1.2.1. By Body Type

- 5.1.1.1.2.1.1. Narrowbody Aircraft

- 5.1.1.1.2.1.2. Widebody Aircraft

- 5.1.1.1.2.1. By Body Type

- 5.1.1.1. By Sub Aircraft Type

- 5.1.2. General Aviation

- 5.1.2.1. Business Jets

- 5.1.2.1.1. Large Jet

- 5.1.2.1.2. Light Jet

- 5.1.2.1.3. Mid-Size Jet

- 5.1.2.2. Piston Fixed-Wing Aircraft

- 5.1.2.3. Others

- 5.1.2.1. Business Jets

- 5.1.3. Military Aviation

- 5.1.3.1. Multi-Role Aircraft

- 5.1.3.2. Training Aircraft

- 5.1.3.3. Transport Aircraft

- 5.1.3.4. Rotorcraft

- 5.1.3.4.1. Multi-Mission Helicopter

- 5.1.3.4.2. Transport Helicopter

- 5.1.1. Commercial Aviation

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6. Global Aviation Industry in Japan Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6.1.1. Commercial Aviation

- 6.1.1.1. By Sub Aircraft Type

- 6.1.1.1.1. Freighter Aircraft

- 6.1.1.1.2. Passenger Aircraft

- 6.1.1.1.2.1. By Body Type

- 6.1.1.1.2.1.1. Narrowbody Aircraft

- 6.1.1.1.2.1.2. Widebody Aircraft

- 6.1.1.1.2.1. By Body Type

- 6.1.1.1. By Sub Aircraft Type

- 6.1.2. General Aviation

- 6.1.2.1. Business Jets

- 6.1.2.1.1. Large Jet

- 6.1.2.1.2. Light Jet

- 6.1.2.1.3. Mid-Size Jet

- 6.1.2.2. Piston Fixed-Wing Aircraft

- 6.1.2.3. Others

- 6.1.2.1. Business Jets

- 6.1.3. Military Aviation

- 6.1.3.1. Multi-Role Aircraft

- 6.1.3.2. Training Aircraft

- 6.1.3.3. Transport Aircraft

- 6.1.3.4. Rotorcraft

- 6.1.3.4.1. Multi-Mission Helicopter

- 6.1.3.4.2. Transport Helicopter

- 6.1.1. Commercial Aviation

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7. North America Aviation Industry in Japan Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7.1.1. Commercial Aviation

- 7.1.1.1. By Sub Aircraft Type

- 7.1.1.1.1. Freighter Aircraft

- 7.1.1.1.2. Passenger Aircraft

- 7.1.1.1.2.1. By Body Type

- 7.1.1.1.2.1.1. Narrowbody Aircraft

- 7.1.1.1.2.1.2. Widebody Aircraft

- 7.1.1.1.2.1. By Body Type

- 7.1.1.1. By Sub Aircraft Type

- 7.1.2. General Aviation

- 7.1.2.1. Business Jets

- 7.1.2.1.1. Large Jet

- 7.1.2.1.2. Light Jet

- 7.1.2.1.3. Mid-Size Jet

- 7.1.2.2. Piston Fixed-Wing Aircraft

- 7.1.2.3. Others

- 7.1.2.1. Business Jets

- 7.1.3. Military Aviation

- 7.1.3.1. Multi-Role Aircraft

- 7.1.3.2. Training Aircraft

- 7.1.3.3. Transport Aircraft

- 7.1.3.4. Rotorcraft

- 7.1.3.4.1. Multi-Mission Helicopter

- 7.1.3.4.2. Transport Helicopter

- 7.1.1. Commercial Aviation

- 7.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 8. South America Aviation Industry in Japan Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 8.1.1. Commercial Aviation

- 8.1.1.1. By Sub Aircraft Type

- 8.1.1.1.1. Freighter Aircraft

- 8.1.1.1.2. Passenger Aircraft

- 8.1.1.1.2.1. By Body Type

- 8.1.1.1.2.1.1. Narrowbody Aircraft

- 8.1.1.1.2.1.2. Widebody Aircraft

- 8.1.1.1.2.1. By Body Type

- 8.1.1.1. By Sub Aircraft Type

- 8.1.2. General Aviation

- 8.1.2.1. Business Jets

- 8.1.2.1.1. Large Jet

- 8.1.2.1.2. Light Jet

- 8.1.2.1.3. Mid-Size Jet

- 8.1.2.2. Piston Fixed-Wing Aircraft

- 8.1.2.3. Others

- 8.1.2.1. Business Jets

- 8.1.3. Military Aviation

- 8.1.3.1. Multi-Role Aircraft

- 8.1.3.2. Training Aircraft

- 8.1.3.3. Transport Aircraft

- 8.1.3.4. Rotorcraft

- 8.1.3.4.1. Multi-Mission Helicopter

- 8.1.3.4.2. Transport Helicopter

- 8.1.1. Commercial Aviation

- 8.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 9. Europe Aviation Industry in Japan Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 9.1.1. Commercial Aviation

- 9.1.1.1. By Sub Aircraft Type

- 9.1.1.1.1. Freighter Aircraft

- 9.1.1.1.2. Passenger Aircraft

- 9.1.1.1.2.1. By Body Type

- 9.1.1.1.2.1.1. Narrowbody Aircraft

- 9.1.1.1.2.1.2. Widebody Aircraft

- 9.1.1.1.2.1. By Body Type

- 9.1.1.1. By Sub Aircraft Type

- 9.1.2. General Aviation

- 9.1.2.1. Business Jets

- 9.1.2.1.1. Large Jet

- 9.1.2.1.2. Light Jet

- 9.1.2.1.3. Mid-Size Jet

- 9.1.2.2. Piston Fixed-Wing Aircraft

- 9.1.2.3. Others

- 9.1.2.1. Business Jets

- 9.1.3. Military Aviation

- 9.1.3.1. Multi-Role Aircraft

- 9.1.3.2. Training Aircraft

- 9.1.3.3. Transport Aircraft

- 9.1.3.4. Rotorcraft

- 9.1.3.4.1. Multi-Mission Helicopter

- 9.1.3.4.2. Transport Helicopter

- 9.1.1. Commercial Aviation

- 9.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 10. Middle East & Africa Aviation Industry in Japan Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 10.1.1. Commercial Aviation

- 10.1.1.1. By Sub Aircraft Type

- 10.1.1.1.1. Freighter Aircraft

- 10.1.1.1.2. Passenger Aircraft

- 10.1.1.1.2.1. By Body Type

- 10.1.1.1.2.1.1. Narrowbody Aircraft

- 10.1.1.1.2.1.2. Widebody Aircraft

- 10.1.1.1.2.1. By Body Type

- 10.1.1.1. By Sub Aircraft Type

- 10.1.2. General Aviation

- 10.1.2.1. Business Jets

- 10.1.2.1.1. Large Jet

- 10.1.2.1.2. Light Jet

- 10.1.2.1.3. Mid-Size Jet

- 10.1.2.2. Piston Fixed-Wing Aircraft

- 10.1.2.3. Others

- 10.1.2.1. Business Jets

- 10.1.3. Military Aviation

- 10.1.3.1. Multi-Role Aircraft

- 10.1.3.2. Training Aircraft

- 10.1.3.3. Transport Aircraft

- 10.1.3.4. Rotorcraft

- 10.1.3.4.1. Multi-Mission Helicopter

- 10.1.3.4.2. Transport Helicopter

- 10.1.1. Commercial Aviation

- 10.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 11. Asia Pacific Aviation Industry in Japan Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 11.1.1. Commercial Aviation

- 11.1.1.1. By Sub Aircraft Type

- 11.1.1.1.1. Freighter Aircraft

- 11.1.1.1.2. Passenger Aircraft

- 11.1.1.1.2.1. By Body Type

- 11.1.1.1.2.1.1. Narrowbody Aircraft

- 11.1.1.1.2.1.2. Widebody Aircraft

- 11.1.1.1.2.1. By Body Type

- 11.1.1.1. By Sub Aircraft Type

- 11.1.2. General Aviation

- 11.1.2.1. Business Jets

- 11.1.2.1.1. Large Jet

- 11.1.2.1.2. Light Jet

- 11.1.2.1.3. Mid-Size Jet

- 11.1.2.2. Piston Fixed-Wing Aircraft

- 11.1.2.3. Others

- 11.1.2.1. Business Jets

- 11.1.3. Military Aviation

- 11.1.3.1. Multi-Role Aircraft

- 11.1.3.2. Training Aircraft

- 11.1.3.3. Transport Aircraft

- 11.1.3.4. Rotorcraft

- 11.1.3.4.1. Multi-Mission Helicopter

- 11.1.3.4.2. Transport Helicopter

- 11.1.1. Commercial Aviation

- 11.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Textron Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Lockheed Martin Corporation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Airbus SE

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 The Boeing Compan

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Bombardier Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 ATR

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Kawasaki Heavy Industries Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.1 Textron Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Aviation Industry in Japan Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Aviation Industry in Japan Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 3: North America Aviation Industry in Japan Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 4: North America Aviation Industry in Japan Revenue (billion), by Country 2025 & 2033

- Figure 5: North America Aviation Industry in Japan Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America Aviation Industry in Japan Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 7: South America Aviation Industry in Japan Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 8: South America Aviation Industry in Japan Revenue (billion), by Country 2025 & 2033

- Figure 9: South America Aviation Industry in Japan Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Aviation Industry in Japan Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 11: Europe Aviation Industry in Japan Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 12: Europe Aviation Industry in Japan Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Aviation Industry in Japan Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa Aviation Industry in Japan Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 15: Middle East & Africa Aviation Industry in Japan Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 16: Middle East & Africa Aviation Industry in Japan Revenue (billion), by Country 2025 & 2033

- Figure 17: Middle East & Africa Aviation Industry in Japan Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Aviation Industry in Japan Revenue (billion), by Aircraft Type 2025 & 2033

- Figure 19: Asia Pacific Aviation Industry in Japan Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 20: Asia Pacific Aviation Industry in Japan Revenue (billion), by Country 2025 & 2033

- Figure 21: Asia Pacific Aviation Industry in Japan Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aviation Industry in Japan Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 2: Global Aviation Industry in Japan Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Aviation Industry in Japan Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 4: Global Aviation Industry in Japan Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United States Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Canada Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Mexico Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Global Aviation Industry in Japan Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 9: Global Aviation Industry in Japan Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Brazil Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Argentina Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Global Aviation Industry in Japan Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 14: Global Aviation Industry in Japan Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Italy Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Russia Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Benelux Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Nordics Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Global Aviation Industry in Japan Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 25: Global Aviation Industry in Japan Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Turkey Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Israel Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: GCC Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: North Africa Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Africa Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global Aviation Industry in Japan Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 33: Global Aviation Industry in Japan Revenue billion Forecast, by Country 2020 & 2033

- Table 34: China Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: India Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Japan Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Korea Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: ASEAN Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Oceania Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific Aviation Industry in Japan Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aviation Industry in Japan?

The projected CAGR is approximately 6.7%.

2. Which companies are prominent players in the Aviation Industry in Japan?

Key companies in the market include Textron Inc, Lockheed Martin Corporation, Airbus SE, The Boeing Compan, Bombardier Inc, ATR, Kawasaki Heavy Industries Ltd.

3. What are the main segments of the Aviation Industry in Japan?

The market segments include Aircraft Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 16.9 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

December 2022: The US Army was awarded a contract to supply next-generation helicopters to Textron Inc.'s Bell unit. The Army`s "Future Vertical Lift" competition aimed at finding a replacement as the Army looks to retire more than 2,000 medium-class UH-60 Black Hawk utility helicopters.November 2022: Boeing was awarded a contract to deliver two additional KC-46A Pegasus tankers to the Japan Air Self-Defense Force (JASDF), bringing the total on contract for Japan to six.November 2022: Bell Textron Inc., a company of Textron Inc., forged an agreement to sell 10 Bell 505 helicopters to the Royal Jordanian Air Force (RJAF) at the Forces Exhibition and Conference. Combat Air Force (SOFEX) in Aqaba, Jordan.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aviation Industry in Japan," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aviation Industry in Japan report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aviation Industry in Japan?

To stay informed about further developments, trends, and reports in the Aviation Industry in Japan, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence