Key Insights

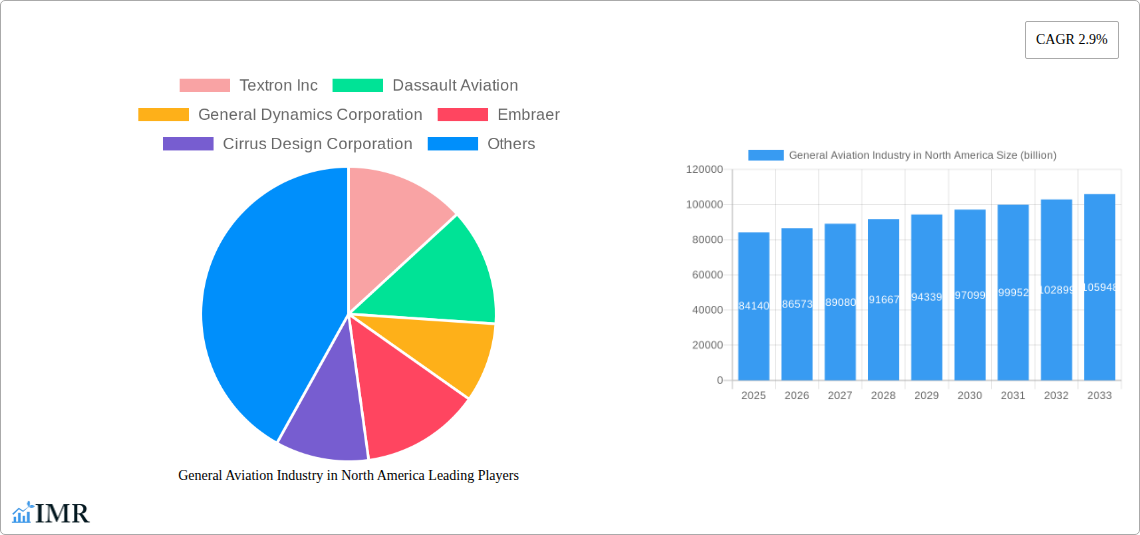

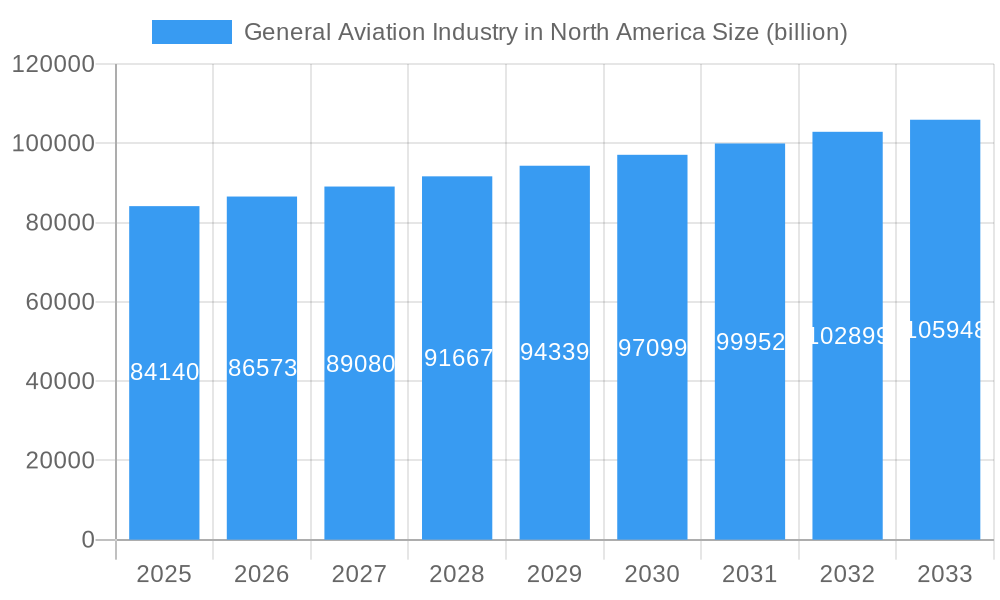

The General Aviation Industry in North America is poised for robust expansion, demonstrating a healthy market size of $84.14 billion in 2025, growing at a compelling CAGR of 2.9% through 2033. This growth is underpinned by a confluence of factors including an increasing demand for business aviation services, driven by the need for efficient and flexible travel solutions for corporate executives and high-net-worth individuals. The burgeoning fractional ownership and jet card programs are making private aviation more accessible, thereby expanding the customer base. Furthermore, advancements in aircraft technology, such as improved fuel efficiency, enhanced safety features, and the introduction of new, lighter, and more capable aircraft models across business jet categories (large, light, and mid-size), are stimulating market activity. The resilience of the North American economy and a continuous appetite for premium travel experiences are key enablers of this sustained growth trajectory.

General Aviation Industry in North America Market Size (In Billion)

Looking ahead, the market is expected to benefit from the increasing adoption of advanced avionics and connectivity solutions, further enhancing operational efficiency and passenger experience. While the Piston Fixed-Wing Aircraft segment will continue to cater to training and recreational flying, the dominance of business jets in terms of value generation is anticipated. Emerging trends like the development of electric and hybrid-electric aircraft within the general aviation sphere, though nascent, represent a significant future growth avenue. Challenges such as rising operational costs, including fuel prices and maintenance, and stringent regulatory landscapes, require continuous innovation and strategic adaptation from industry players. However, the inherent value proposition of general aviation in providing unparalleled convenience and time savings for its users is expected to outweigh these restraints, ensuring a positive outlook for the North American market.

General Aviation Industry in North America Company Market Share

General Aviation Industry in North America: Market Dynamics, Growth Trends, and Future Outlook (2019-2033)

This comprehensive report offers an in-depth analysis of the North American General Aviation Industry, covering market dynamics, growth trends, key players, and future opportunities. With a detailed study period from 2019 to 2033, and a base year of 2025, this report leverages high-traffic keywords and presents quantitative insights in billion units to maximize search engine visibility and deliver crucial intelligence to industry professionals. Explore parent and child market segments including Business Jets (Large Jet, Light Jet, Mid-Size Jet), Piston Fixed-Wing Aircraft, and Others.

General Aviation Industry in North America Market Dynamics & Structure

The North American General Aviation Industry exhibits a dynamic and evolving market structure, characterized by increasing technological integration and strategic consolidations. Market concentration is observed among a few key players in the higher-value segments, such as business jets, while a more fragmented landscape exists for piston-fixed-wing aircraft and other specialized aviation services. Technological innovation serves as a primary driver, with advancements in avionics, engine efficiency, and sustainable aviation fuels shaping product development. Regulatory frameworks, including FAA and Transport Canada oversight, play a critical role in dictating safety standards, operational procedures, and market entry barriers. Competitive product substitutes, while limited for high-performance business jets, emerge in the form of fractional ownership programs and jet card services as alternatives to outright aircraft purchase. End-user demographics are shifting, with an increasing demand from ultra-high-net-worth individuals and corporations seeking enhanced mobility and efficiency. Mergers and acquisitions (M&A) trends indicate a strategic push for market share expansion and vertical integration within the industry.

- Market Concentration: Dominated by a few large manufacturers in business jets, with moderate concentration in other segments.

- Technological Innovation: Driven by demand for fuel efficiency, enhanced safety features, and digital cockpit solutions.

- Regulatory Frameworks: Strict adherence to FAA and Transport Canada regulations, influencing product certification and operational standards.

- Competitive Product Substitutes: Fractional ownership and charter services offer alternatives to direct aircraft acquisition.

- End-User Demographics: Growing demand from corporate clients and high-net-worth individuals.

- M&A Trends: Strategic acquisitions aimed at expanding product portfolios and market reach.

General Aviation Industry in North America Growth Trends & Insights

The North American General Aviation Industry is poised for robust growth over the forecast period (2025–2033), driven by a confluence of economic recovery, technological advancements, and evolving consumer preferences. The market size is projected to expand significantly, fueled by an increasing demand for private and business aviation solutions. Adoption rates for advanced aircraft, particularly light and mid-size business jets, are expected to rise as companies prioritize efficient travel and connectivity. Technological disruptions, such as the integration of advanced composites, sustainable propulsion systems, and sophisticated avionics, are not only improving aircraft performance but also enhancing passenger experience and operational safety. Shifts in consumer behavior are evident, with a growing appreciation for the flexibility, privacy, and time-saving benefits offered by general aviation. This segment of the aviation industry is witnessing a surge in demand for on-demand charter services and fractional ownership models, reflecting a desire for accessibility without the full commitment of aircraft ownership. The market penetration of new technologies and aircraft models is further amplified by strategic marketing efforts and a focus on customer-centric solutions. The overall compound annual growth rate (CAGR) for the North American General Aviation Industry is anticipated to be substantial, reflecting a healthy expansion trajectory.

Dominant Regions, Countries, or Segments in General Aviation Industry in North America

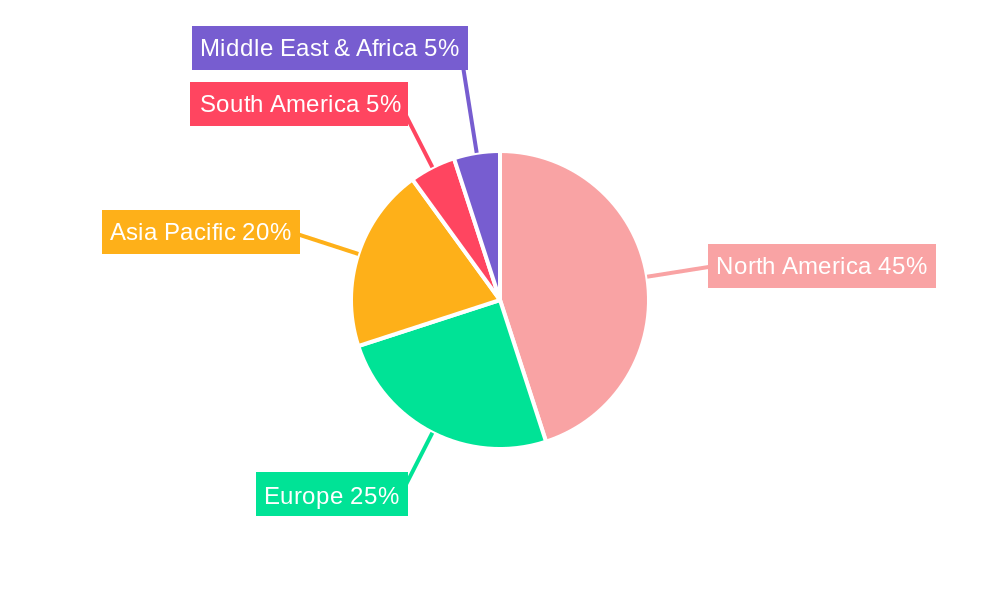

Within the North American General Aviation Industry, Business Jets, particularly Mid-Size Jets and Large Jets, emerge as the dominant segment driving market growth. The United States, as the largest aviation market globally, consistently leads in terms of aircraft production, sales, and operational activity. Several key drivers contribute to this dominance. Economic policies that foster business growth and investment directly translate into increased demand for private and corporate aircraft, facilitating executive travel and enabling access to remote business locations. Significant infrastructure investments in airports and air traffic control systems across the US ensure a robust operational environment. Furthermore, the presence of major general aviation manufacturers, including Textron Inc., Dassault Aviation, General Dynamics Corporation, Embraer, Cirrus Design Corporation, Pilatus Aircraft Ltd, Bombardier Inc., and Honda Motor Co Ltd, with their extensive product lines and global sales networks, solidifies the dominance of the US market. The continuous development and introduction of technologically advanced business jets, offering superior range, speed, and cabin amenities, cater to the sophisticated needs of corporations and high-net-worth individuals. The market share held by business jets, especially in the higher-value categories, significantly outpaces that of piston-fixed-wing aircraft and other specialized aviation sub-segments, underscoring their pivotal role in the overall industry's economic output and growth potential.

- Leading Segment: Business Jets (Mid-Size Jet and Large Jet).

- Dominant Country: United States.

- Key Drivers: Favorable economic policies, substantial infrastructure, presence of major manufacturers, and continuous technological innovation in business jet design.

- Market Share: Business jets hold a significant portion of the market value and revenue.

- Growth Potential: Strong demand from corporate clients and a continuous pipeline of new, advanced aircraft models.

General Aviation Industry in North America Product Landscape

The product landscape of the North American General Aviation Industry is characterized by a spectrum of aircraft designed for diverse applications, from personal travel to sophisticated corporate transport. Innovations in materials science have led to lighter and more durable airframes, enhancing fuel efficiency and performance. Advanced avionics suites, featuring integrated digital systems and enhanced situational awareness tools, are becoming standard across all aircraft types, improving safety and pilot workload. Applications range from private ownership and charter services for business jets to training, recreational flying, and specialized missions for piston-fixed-wing aircraft. Performance metrics such as range, speed, payload capacity, and fuel consumption are continuously being optimized through engineering advancements. Unique selling propositions often lie in cabin comfort, technological integration, and operational cost-effectiveness, with manufacturers differentiating their offerings through customization options and cutting-edge features.

Key Drivers, Barriers & Challenges in General Aviation Industry in North America

Key Drivers:

The North American General Aviation Industry is propelled by several key drivers. Technological innovation, particularly in avionics, engine technology, and airframe design, enhances performance and safety. The growing demand for efficient business travel and luxury transportation from corporations and high-net-worth individuals is a significant economic driver. Favorable government policies, including tax incentives and regulatory support, further stimulate market growth.

Barriers & Challenges:

Despite its growth, the industry faces significant barriers and challenges. High acquisition and operational costs remain a substantial restraint for many potential buyers. Supply chain disruptions, particularly for critical components, can lead to production delays and increased costs. Stringent regulatory requirements and evolving environmental standards necessitate continuous investment in compliance and technological upgrades. Intense competition among manufacturers and service providers also presents a challenge to market share expansion and profitability.

Emerging Opportunities in General Aviation Industry in North America

Emerging opportunities in the North American General Aviation Industry lie in the growing demand for sustainable aviation solutions, including electric and hybrid-electric aircraft, which are gaining traction due to environmental concerns. The expansion of fractional ownership and on-demand charter services presents a significant opportunity to broaden the customer base beyond traditional aircraft owners. Furthermore, advancements in urban air mobility (UAM) and the development of advanced air mobility (AAM) platforms open new markets for vertical take-off and landing (VTOL) aircraft. The integration of AI and advanced data analytics in aircraft operations and maintenance promises enhanced efficiency and predictive capabilities, creating opportunities for service providers.

Growth Accelerators in the General Aviation Industry in North America Industry

Several factors are accelerating long-term growth in the North American General Aviation Industry. Continuous technological breakthroughs in areas like advanced propulsion systems, lighter composite materials, and sophisticated fly-by-wire controls are leading to more efficient, capable, and safer aircraft. Strategic partnerships between manufacturers, technology providers, and service companies are fostering innovation and expanding market reach. Market expansion strategies, including the development of new aircraft models tailored to emerging market needs and the penetration into underserved regions or niche applications, are also key accelerators. Furthermore, the increasing focus on customer experience, from cabin interiors to in-flight connectivity, is driving demand and brand loyalty.

Key Players Shaping the General Aviation Industry in North America Market

- Textron Inc.

- Dassault Aviation

- General Dynamics Corporation

- Embraer

- Cirrus Design Corporation

- Pilatus Aircraft Ltd

- Bombardier Inc.

- Honda Motor Co Ltd

Notable Milestones in General Aviation Industry in North America Sector

- October 2023: Textron Aviation announced a purchase agreement with Fly Alliance for up to 20 Cessna Citation business jets, with options for 16 additional aircraft. This agreement is expected to support Fly Alliance's luxury private jet charter operations, with the first delivery of an XLS Gen2 anticipated in 2023, highlighting strong demand for new business jet deliveries.

- June 2023: Gulfstream Aerospace Corp. announced a significant expansion of its completions and outfitting operations at St. Louis Downtown Airport. This strategic investment of USD 28.5 million includes modernizing existing spaces and adding state-of-the-art equipment, aiming to increase completion operations and bolster its service capabilities within the business jet segment.

- June 2023: Gulfstream Aerospace Corp. announced further expansion of its completions and outfitting operations at St. Louis Downtown Airport. This reiterates Gulfstream's commitment to enhancing its infrastructure and service offerings, impacting the completion and outfitting market by increasing capacity and efficiency, and representing a substantial capital investment.

In-Depth General Aviation Industry in North America Market Outlook

The future outlook for the North American General Aviation Industry is exceptionally promising, fueled by sustained demand for personalized and efficient air travel. Growth accelerators, including rapid technological advancements in sustainable aviation and advanced avionics, are set to redefine aircraft capabilities and operational efficiency. Strategic market expansion efforts by key players, coupled with innovative service models like fractional ownership and on-demand charter, are broadening the industry's appeal to a wider demographic. The continuous evolution of business jet technology, catering to demands for longer range, enhanced comfort, and reduced environmental impact, will be a significant factor in driving future market value. The industry's capacity to adapt to evolving regulatory landscapes and embrace sustainable practices will be crucial in unlocking its full long-term potential.

General Aviation Industry in North America Segmentation

-

1. Sub Aircraft Type

-

1.1. Business Jets

- 1.1.1. Large Jet

- 1.1.2. Light Jet

- 1.1.3. Mid-Size Jet

- 1.2. Piston Fixed-Wing Aircraft

- 1.3. Others

-

1.1. Business Jets

General Aviation Industry in North America Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

General Aviation Industry in North America Regional Market Share

Geographic Coverage of General Aviation Industry in North America

General Aviation Industry in North America REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 5.1.1. Business Jets

- 5.1.1.1. Large Jet

- 5.1.1.2. Light Jet

- 5.1.1.3. Mid-Size Jet

- 5.1.2. Piston Fixed-Wing Aircraft

- 5.1.3. Others

- 5.1.1. Business Jets

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. South America

- 5.2.3. Europe

- 5.2.4. Middle East & Africa

- 5.2.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 6. Global General Aviation Industry in North America Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 6.1.1. Business Jets

- 6.1.1.1. Large Jet

- 6.1.1.2. Light Jet

- 6.1.1.3. Mid-Size Jet

- 6.1.2. Piston Fixed-Wing Aircraft

- 6.1.3. Others

- 6.1.1. Business Jets

- 6.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 7. North America General Aviation Industry in North America Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 7.1.1. Business Jets

- 7.1.1.1. Large Jet

- 7.1.1.2. Light Jet

- 7.1.1.3. Mid-Size Jet

- 7.1.2. Piston Fixed-Wing Aircraft

- 7.1.3. Others

- 7.1.1. Business Jets

- 7.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 8. South America General Aviation Industry in North America Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 8.1.1. Business Jets

- 8.1.1.1. Large Jet

- 8.1.1.2. Light Jet

- 8.1.1.3. Mid-Size Jet

- 8.1.2. Piston Fixed-Wing Aircraft

- 8.1.3. Others

- 8.1.1. Business Jets

- 8.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 9. Europe General Aviation Industry in North America Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 9.1.1. Business Jets

- 9.1.1.1. Large Jet

- 9.1.1.2. Light Jet

- 9.1.1.3. Mid-Size Jet

- 9.1.2. Piston Fixed-Wing Aircraft

- 9.1.3. Others

- 9.1.1. Business Jets

- 9.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 10. Middle East & Africa General Aviation Industry in North America Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 10.1.1. Business Jets

- 10.1.1.1. Large Jet

- 10.1.1.2. Light Jet

- 10.1.1.3. Mid-Size Jet

- 10.1.2. Piston Fixed-Wing Aircraft

- 10.1.3. Others

- 10.1.1. Business Jets

- 10.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 11. Asia Pacific General Aviation Industry in North America Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 11.1.1. Business Jets

- 11.1.1.1. Large Jet

- 11.1.1.2. Light Jet

- 11.1.1.3. Mid-Size Jet

- 11.1.2. Piston Fixed-Wing Aircraft

- 11.1.3. Others

- 11.1.1. Business Jets

- 11.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Textron Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Dassault Aviation

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 General Dynamics Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Embraer

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Cirrus Design Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Pilatus Aircraft Ltd

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Bombardier Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Honda Motor Co Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 Textron Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global General Aviation Industry in North America Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America General Aviation Industry in North America Revenue (billion), by Sub Aircraft Type 2025 & 2033

- Figure 3: North America General Aviation Industry in North America Revenue Share (%), by Sub Aircraft Type 2025 & 2033

- Figure 4: North America General Aviation Industry in North America Revenue (billion), by Country 2025 & 2033

- Figure 5: North America General Aviation Industry in North America Revenue Share (%), by Country 2025 & 2033

- Figure 6: South America General Aviation Industry in North America Revenue (billion), by Sub Aircraft Type 2025 & 2033

- Figure 7: South America General Aviation Industry in North America Revenue Share (%), by Sub Aircraft Type 2025 & 2033

- Figure 8: South America General Aviation Industry in North America Revenue (billion), by Country 2025 & 2033

- Figure 9: South America General Aviation Industry in North America Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe General Aviation Industry in North America Revenue (billion), by Sub Aircraft Type 2025 & 2033

- Figure 11: Europe General Aviation Industry in North America Revenue Share (%), by Sub Aircraft Type 2025 & 2033

- Figure 12: Europe General Aviation Industry in North America Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe General Aviation Industry in North America Revenue Share (%), by Country 2025 & 2033

- Figure 14: Middle East & Africa General Aviation Industry in North America Revenue (billion), by Sub Aircraft Type 2025 & 2033

- Figure 15: Middle East & Africa General Aviation Industry in North America Revenue Share (%), by Sub Aircraft Type 2025 & 2033

- Figure 16: Middle East & Africa General Aviation Industry in North America Revenue (billion), by Country 2025 & 2033

- Figure 17: Middle East & Africa General Aviation Industry in North America Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific General Aviation Industry in North America Revenue (billion), by Sub Aircraft Type 2025 & 2033

- Figure 19: Asia Pacific General Aviation Industry in North America Revenue Share (%), by Sub Aircraft Type 2025 & 2033

- Figure 20: Asia Pacific General Aviation Industry in North America Revenue (billion), by Country 2025 & 2033

- Figure 21: Asia Pacific General Aviation Industry in North America Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global General Aviation Industry in North America Revenue billion Forecast, by Sub Aircraft Type 2020 & 2033

- Table 2: Global General Aviation Industry in North America Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global General Aviation Industry in North America Revenue billion Forecast, by Sub Aircraft Type 2020 & 2033

- Table 4: Global General Aviation Industry in North America Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United States General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Canada General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Mexico General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Global General Aviation Industry in North America Revenue billion Forecast, by Sub Aircraft Type 2020 & 2033

- Table 9: Global General Aviation Industry in North America Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Brazil General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Argentina General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Rest of South America General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Global General Aviation Industry in North America Revenue billion Forecast, by Sub Aircraft Type 2020 & 2033

- Table 14: Global General Aviation Industry in North America Revenue billion Forecast, by Country 2020 & 2033

- Table 15: United Kingdom General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Germany General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Italy General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Russia General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Benelux General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Nordics General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Rest of Europe General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Global General Aviation Industry in North America Revenue billion Forecast, by Sub Aircraft Type 2020 & 2033

- Table 25: Global General Aviation Industry in North America Revenue billion Forecast, by Country 2020 & 2033

- Table 26: Turkey General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Israel General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: GCC General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: North Africa General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Africa General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East & Africa General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Global General Aviation Industry in North America Revenue billion Forecast, by Sub Aircraft Type 2020 & 2033

- Table 33: Global General Aviation Industry in North America Revenue billion Forecast, by Country 2020 & 2033

- Table 34: China General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: India General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Japan General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: South Korea General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: ASEAN General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Oceania General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Rest of Asia Pacific General Aviation Industry in North America Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the General Aviation Industry in North America?

The projected CAGR is approximately 2.9%.

2. Which companies are prominent players in the General Aviation Industry in North America?

Key companies in the market include Textron Inc, Dassault Aviation, General Dynamics Corporation, Embraer, Cirrus Design Corporation, Pilatus Aircraft Ltd, Bombardier Inc, Honda Motor Co Ltd.

3. What are the main segments of the General Aviation Industry in North America?

The market segments include Sub Aircraft Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 84.14 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

The increasing HNWI population is driving the sales of general aviation aircraft in the region.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

October 2023: Textron Aviation announced that it entered a purchase agreement with Fly Alliance for up to 20 Cessna Citation business jets, with options for 16 additional aircraft. Fly Alliance is expected to use the aircraft for its luxury private jet charter operations. It expected the delivery of the first aircraft, an XLS Gen2, in 2023.June 2023: Gulfstream Aerospace Corp. announced further expansion of its completions and outfitting operations at the St. Louis Downtown Airport. With this latest expansion, Gulfstream is expected to increase completion operations at the site while modernizing its existing spaces by adding new, state-of-the-art equipment and tooling, representing a total capital investment of USD 28.5 million.June 2023: Gulfstream Aerospace Corp. announced further expansion of its completions and outfitting operations at St. Louis Downtown Airport. With this latest expansion, Gulfstream expects to increase operations at the site while modernizing its existing spaces by adding new, state-of-the-art equipment and tooling, representing a total capital investment of USD 28.5 million.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "General Aviation Industry in North America," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the General Aviation Industry in North America report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the General Aviation Industry in North America?

To stay informed about further developments, trends, and reports in the General Aviation Industry in North America, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence