Key Insights

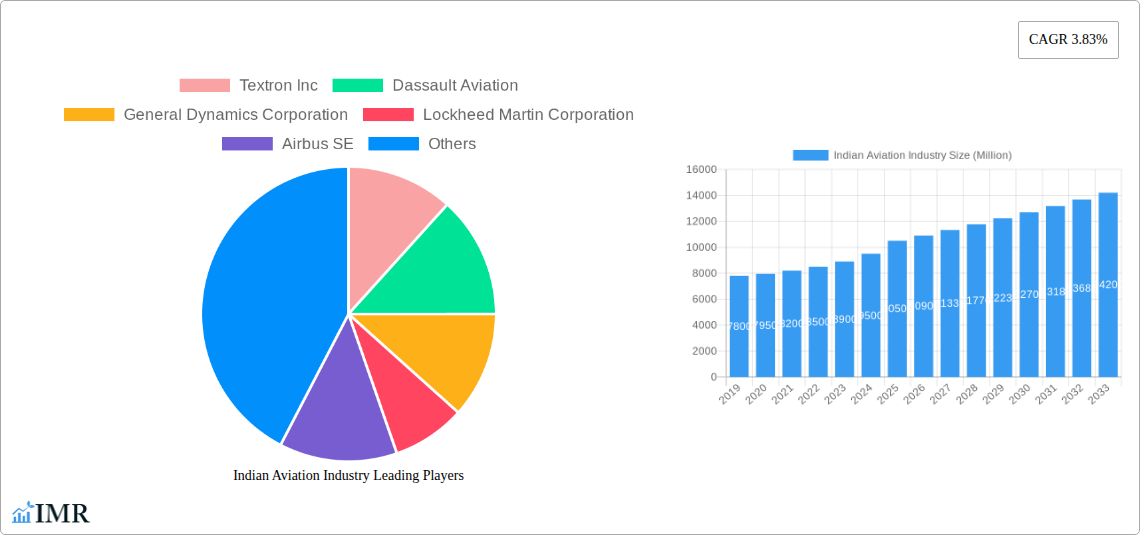

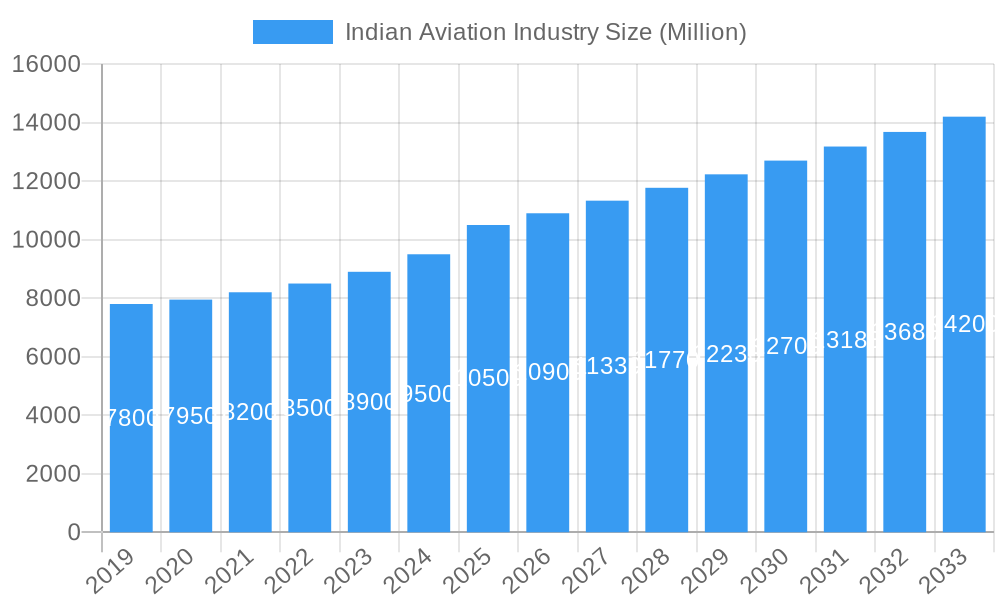

The Indian Aviation Industry is projected for substantial growth, estimated to reach $14.47 billion by 2032, with a Compound Annual Growth Rate (CAGR) of 12.21%. This expansion is fueled by rising disposable incomes, government initiatives like UDAN promoting air connectivity in Tier-II and Tier-III cities, and fleet modernization in both commercial and military aviation. Passenger aircraft, particularly narrow-body jets, are expected to lead demand due to cost-effectiveness. The defense sector's increasing budget and focus on indigenization are also driving the demand for advanced military aircraft.

Indian Aviation Industry Market Size (In Billion)

Key growth drivers include the adoption of advanced avionics, lightweight materials for improved fuel efficiency, and the expansion of low-cost carriers (LCCs) making air travel more accessible. Challenges such as high fuel costs, regulatory complexities, and infrastructure development needs are being addressed through strategic investments and supportive government policies. These factors position the Indian Aviation Industry for significant future potential.

Indian Aviation Industry Company Market Share

Unlocking India's Skies: A Comprehensive Report on the Indian Aviation Industry

This in-depth report provides a critical analysis of the Indian Aviation Industry, a rapidly expanding sector poised for significant growth. Covering the Study Period from 2019–2033, with a Base Year and Estimated Year of 2025, and a Forecast Period of 2025–2033, this research delves into the market dynamics, growth drivers, and future trajectory of India's skies. We meticulously examine the parent market (overall aviation) and its child markets (specific segments) to offer a holistic view. This report is an indispensable resource for stakeholders, investors, and industry professionals seeking to understand and capitalize on the burgeoning opportunities within the Indian aviation landscape. All values are presented in Million Units.

Indian Aviation Industry Market Dynamics & Structure

The Indian Aviation Industry is characterized by a dynamic interplay of factors shaping its market concentration, technological adoption, and competitive landscape. While the market is experiencing growth, it remains moderately concentrated, with key players dominating specific segments. Technological innovation is a significant driver, particularly in the adoption of fuel-efficient Narrowbody Aircraft and advanced avionics. The regulatory framework, though evolving, is crucial in influencing market access and operational standards. Substitute products, such as high-speed rail, offer competition for shorter domestic routes, but the unique advantages of air travel, especially for longer distances and cargo, ensure its sustained demand. End-user demographics are shifting, with a growing middle class and increasing business travel fueling demand for both Commercial Aviation and General Aviation services. Mergers and acquisitions (M&A) are expected to play a role in consolidating market share and enhancing operational efficiencies, although specific deal volumes are subject to market conditions.

- Market Concentration: Moderately concentrated, with major airlines and aircraft manufacturers holding significant market share.

- Technological Innovation Drivers: Fuel efficiency, passenger comfort, advanced navigation systems, and sustainable aviation fuels are key innovation areas.

- Regulatory Frameworks: Evolving government policies, including liberalization, infrastructure development, and safety regulations, are critical.

- Competitive Product Substitutes: High-speed rail for domestic travel, though air travel remains dominant for longer distances and time-sensitive cargo.

- End-User Demographics: Growing middle class, increasing disposable income, and a burgeoning business sector driving demand.

- M&A Trends: Potential for consolidation to achieve economies of scale and improve service offerings.

Indian Aviation Industry Growth Trends & Insights

The Indian Aviation Industry is projected to experience robust growth, driven by a confluence of economic development, increasing disposable incomes, and supportive government initiatives. The market size evolution is expected to be substantial, with a projected Compound Annual Growth Rate (CAGR) of XX% between 2025 and 2033. Adoption rates for new aircraft technologies, particularly in the Commercial Aviation segment, are on an upward trend as airlines prioritize fleet modernization for improved efficiency and passenger experience. Technological disruptions, such as advancements in electric and hybrid aircraft propulsion, are on the horizon and will likely influence future market dynamics. Consumer behavior shifts are evident, with a growing preference for air travel due to its speed and convenience, even for leisure trips. The penetration of aviation services into Tier 2 and Tier 3 cities is also a key growth area, expanding the reach of air connectivity. The General Aviation segment, particularly Business Jets, is witnessing increased demand from corporations and high-net-worth individuals seeking personalized travel solutions. The Military Aviation sector is also a significant contributor to overall growth, with ongoing modernization programs and defense spending.

Dominant Regions, Countries, or Segments in Indian Aviation Industry

The Indian Aviation Industry's growth is propelled by a diverse range of segments, with Commercial Aviation emerging as the dominant force. Within this, Passenger Aircraft are the primary revenue generators, further segmented by Narrowbody Aircraft and Widebody Aircraft. The increasing demand for domestic and international travel, fueled by a growing middle class and expanding tourism, directly contributes to the dominance of passenger operations. Key drivers include government policies aimed at enhancing regional connectivity, such as the UDAN scheme, and substantial investments in airport infrastructure development across major metropolitan areas and emerging economic hubs.

- Commercial Aviation (Passenger Aircraft): This segment is the leading growth engine, driven by rising disposable incomes and a growing middle-class population.

- Narrowbody Aircraft: Dominant for domestic and short-to-medium haul international routes due to their operational efficiency and flexibility.

- Widebody Aircraft: Increasingly important for long-haul international routes, connecting India to global destinations and supporting the growth of tourism and international business.

- Commercial Aviation (Freighter Aircraft): While smaller than passenger operations, the air cargo segment is experiencing significant growth, supported by e-commerce expansion and the need for rapid logistics.

- General Aviation: This segment, encompassing Business Jets (Large Jet, Light Jet, Mid-Size Jet) and Piston Fixed-Wing Aircraft, caters to corporate travel and niche markets, demonstrating steady growth potential.

- Military Aviation: This segment, including Multi-Role Aircraft, Training Aircraft, Transport Aircraft, and Rotorcraft (Multi-Mission Helicopter, Transport Helicopter), represents a substantial and consistent demand driven by defense modernization programs and national security imperatives.

The dominance of Commercial Aviation is further reinforced by the significant fleet expansion plans of major Indian carriers. For instance, the March 2023 contract awarded to Boeing by Air India for 220 aircraft, including 190 737 Max, 20 787, and 10 777X, highlights the massive scale of fleet modernization and expansion within the passenger segment. Similarly, the June 2023 discussions between Delta Air Lines Inc. and Airbus SE for A350 and A330neo wide-body aircraft indicate global manufacturers' keen interest in catering to the demand for larger aircraft to serve India's growing international connectivity needs. These developments underscore the pivotal role of passenger aircraft in shaping the overall Indian aviation market.

Indian Aviation Industry Product Landscape

The Indian Aviation Industry's product landscape is characterized by continuous innovation aimed at enhancing efficiency, safety, and passenger experience. Aircraft manufacturers are focusing on developing fuel-efficient Narrowbody Aircraft and advanced Widebody Aircraft to meet the growing demand for both domestic and international travel. In the General Aviation segment, the emphasis is on sleek and technologically advanced Business Jets offering unparalleled comfort and connectivity. The Military Aviation sector sees ongoing development in Multi-Role Aircraft and sophisticated Rotorcraft, equipped with cutting-edge defense technologies. Performance metrics like fuel burn, payload capacity, range, and noise reduction are key differentiators. The increasing integration of smart technologies and sustainable materials further elevates the product offerings.

Key Drivers, Barriers & Challenges in Indian Aviation Industry

Key Drivers: The Indian Aviation Industry is propelled by strong economic growth, a burgeoning middle class with increasing disposable incomes, and a government focus on improving air connectivity through initiatives like UDAN. The expansion of e-commerce and the need for efficient logistics also drive demand for air cargo services. Technological advancements leading to more fuel-efficient and advanced aircraft are crucial for airlines to remain competitive.

Barriers & Challenges: Significant barriers include high operational costs, including jet fuel prices and airport charges. Infrastructure bottlenecks, particularly at congested airports, and the need for skilled manpower pose challenges. Stringent regulatory requirements and environmental concerns related to emissions can also impact growth. Furthermore, intense competition among airlines, coupled with fluctuating global economic conditions and geopolitical uncertainties, can create market volatility. Supply chain disruptions for aircraft components, as seen in global markets, can also affect delivery schedules and operational readiness.

Emerging Opportunities in Indian Aviation Industry

Emerging opportunities in the Indian Aviation Industry are multifaceted. The rapid growth of Tier 2 and Tier 3 cities presents a significant untapped market for air connectivity, creating demand for regional aircraft and new routes. The expansion of the General Aviation sector, particularly in fractional ownership and air charter services, offers lucrative avenues for businesses. The increasing focus on sustainable aviation fuels (SAF) and the potential for electric and hybrid aircraft present opportunities for innovation and eco-friendly operations. Furthermore, the growing defense budget and modernization programs in Military Aviation create sustained demand for advanced platforms and services.

Growth Accelerators in the Indian Aviation Industry Industry

Several catalysts are accelerating the long-term growth of the Indian Aviation Industry. The government's proactive policies aimed at boosting air travel, including infrastructure development and attractive investment incentives, are fundamental. Technological breakthroughs in aircraft manufacturing, leading to more fuel-efficient and quieter planes, will drive fleet upgrades and operational cost reductions. Strategic partnerships between airlines, aircraft manufacturers, and technology providers are fostering innovation and expanding service offerings. The increasing digitalization of aviation services, from booking to in-flight connectivity, enhances customer experience and operational efficiency, further stimulating demand.

Key Players Shaping the Indian Aviation Industry Market

- Textron Inc.

- Dassault Aviation

- General Dynamics Corporation

- Lockheed Martin Corporation

- Airbus SE

- The Boeing Company

- Leonardo S.p.A.

- Bombardier Inc.

- ATR

- Hindustan Aeronautics Limited

Notable Milestones in Indian Aviation Industry Sector

- June 2023: Delta Air Lines Inc. is reportedly in talks with Airbus SE to order wide-body aircraft, specifically the A350 and A330neo twin-aisle aircraft, signaling continued demand for long-haul capacity.

- March 2023: Boeing was awarded a significant contract by Air India for 220 aircraft, including 190 737 Max, 20 787, and 10 777X, underscoring the massive fleet expansion and modernization efforts by Indian carriers.

- December 2022: Textron Inc.'s Bell unit was awarded a contract by the US Army to supply next-generation helicopters as part of the "Future Vertical Lift" program, highlighting advancements in military rotorcraft technology that could influence global defense procurement trends.

In-Depth Indian Aviation Industry Market Outlook

The Indian Aviation Industry presents a compelling outlook for future growth, driven by a confluence of strong economic fundamentals and strategic governmental support. The ongoing fleet modernization and expansion by major airlines, as evidenced by significant aircraft orders, will continue to fuel demand for new aircraft and related services. The expanding network of airports and improved regional connectivity will unlock new markets and passenger segments. Furthermore, the increasing integration of advanced technologies, from sustainable aviation fuels to digital operational solutions, is poised to enhance efficiency and environmental performance. Strategic partnerships and the potential for new market entrants will foster a competitive yet collaborative ecosystem, creating substantial opportunities for all stakeholders in this dynamic and expanding industry.

Indian Aviation Industry Segmentation

-

1. Aircraft Type

-

1.1. Commercial Aviation

-

1.1.1. By Sub Aircraft Type

- 1.1.1.1. Freighter Aircraft

-

1.1.1.2. Passenger Aircraft

-

1.1.1.2.1. By Body Type

- 1.1.1.2.1.1. Narrowbody Aircraft

- 1.1.1.2.1.2. Widebody Aircraft

-

1.1.1.2.1. By Body Type

-

1.1.1. By Sub Aircraft Type

-

1.2. General Aviation

-

1.2.1. Business Jets

- 1.2.1.1. Large Jet

- 1.2.1.2. Light Jet

- 1.2.1.3. Mid-Size Jet

- 1.2.2. Piston Fixed-Wing Aircraft

- 1.2.3. Others

-

1.2.1. Business Jets

-

1.3. Military Aviation

- 1.3.1. Multi-Role Aircraft

- 1.3.2. Training Aircraft

- 1.3.3. Transport Aircraft

-

1.3.4. Rotorcraft

- 1.3.4.1. Multi-Mission Helicopter

- 1.3.4.2. Transport Helicopter

-

1.1. Commercial Aviation

Indian Aviation Industry Segmentation By Geography

- 1. India

Indian Aviation Industry Regional Market Share

Geographic Coverage of Indian Aviation Industry

Indian Aviation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.21% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 5.1.1. Commercial Aviation

- 5.1.1.1. By Sub Aircraft Type

- 5.1.1.1.1. Freighter Aircraft

- 5.1.1.1.2. Passenger Aircraft

- 5.1.1.1.2.1. By Body Type

- 5.1.1.1.2.1.1. Narrowbody Aircraft

- 5.1.1.1.2.1.2. Widebody Aircraft

- 5.1.1.1.2.1. By Body Type

- 5.1.1.1. By Sub Aircraft Type

- 5.1.2. General Aviation

- 5.1.2.1. Business Jets

- 5.1.2.1.1. Large Jet

- 5.1.2.1.2. Light Jet

- 5.1.2.1.3. Mid-Size Jet

- 5.1.2.2. Piston Fixed-Wing Aircraft

- 5.1.2.3. Others

- 5.1.2.1. Business Jets

- 5.1.3. Military Aviation

- 5.1.3.1. Multi-Role Aircraft

- 5.1.3.2. Training Aircraft

- 5.1.3.3. Transport Aircraft

- 5.1.3.4. Rotorcraft

- 5.1.3.4.1. Multi-Mission Helicopter

- 5.1.3.4.2. Transport Helicopter

- 5.1.1. Commercial Aviation

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. India

- 5.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6. Indian Aviation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 6.1.1. Commercial Aviation

- 6.1.1.1. By Sub Aircraft Type

- 6.1.1.1.1. Freighter Aircraft

- 6.1.1.1.2. Passenger Aircraft

- 6.1.1.1.2.1. By Body Type

- 6.1.1.1.2.1.1. Narrowbody Aircraft

- 6.1.1.1.2.1.2. Widebody Aircraft

- 6.1.1.1.2.1. By Body Type

- 6.1.1.1. By Sub Aircraft Type

- 6.1.2. General Aviation

- 6.1.2.1. Business Jets

- 6.1.2.1.1. Large Jet

- 6.1.2.1.2. Light Jet

- 6.1.2.1.3. Mid-Size Jet

- 6.1.2.2. Piston Fixed-Wing Aircraft

- 6.1.2.3. Others

- 6.1.2.1. Business Jets

- 6.1.3. Military Aviation

- 6.1.3.1. Multi-Role Aircraft

- 6.1.3.2. Training Aircraft

- 6.1.3.3. Transport Aircraft

- 6.1.3.4. Rotorcraft

- 6.1.3.4.1. Multi-Mission Helicopter

- 6.1.3.4.2. Transport Helicopter

- 6.1.1. Commercial Aviation

- 6.1. Market Analysis, Insights and Forecast - by Aircraft Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Textron Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Dassault Aviation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 General Dynamics Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Lockheed Martin Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Airbus SE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 The Boeing Compan

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Leonardo S p A

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Bombardier Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 ATR

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Hindustan Aeronautics Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Textron Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Indian Aviation Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Indian Aviation Industry Share (%) by Company 2025

List of Tables

- Table 1: Indian Aviation Industry Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 2: Indian Aviation Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Indian Aviation Industry Revenue billion Forecast, by Aircraft Type 2020 & 2033

- Table 4: Indian Aviation Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Indian Aviation Industry?

The projected CAGR is approximately 12.21%.

2. Which companies are prominent players in the Indian Aviation Industry?

Key companies in the market include Textron Inc, Dassault Aviation, General Dynamics Corporation, Lockheed Martin Corporation, Airbus SE, The Boeing Compan, Leonardo S p A, Bombardier Inc, ATR, Hindustan Aeronautics Limited.

3. What are the main segments of the Indian Aviation Industry?

The market segments include Aircraft Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.47 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

June 2023: Delta Air Lines Inc. is in talks with Airbus SE to order wide-body aircraft, Bloomberg News reported Monday, citing people familiar with the matter. The discussion focuses on A350 and A330neo hai twin-aisle aircraft.March 2023: Boeing was awarded a contract by Air India for 220 Boeing aircraft, including 190 737 Max, 20 787, and 10 777X.December 2022: The US Army was awarded a contract to supply next-generation helicopters to Textron Inc.'s Bell unit. The Army`s "Future Vertical Lift" competition aimed at finding a replacement as the Army looks to retire more than 2,000 medium-class UH-60 Black Hawk utility helicopters.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Indian Aviation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Indian Aviation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Indian Aviation Industry?

To stay informed about further developments, trends, and reports in the Indian Aviation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence