Key Insights

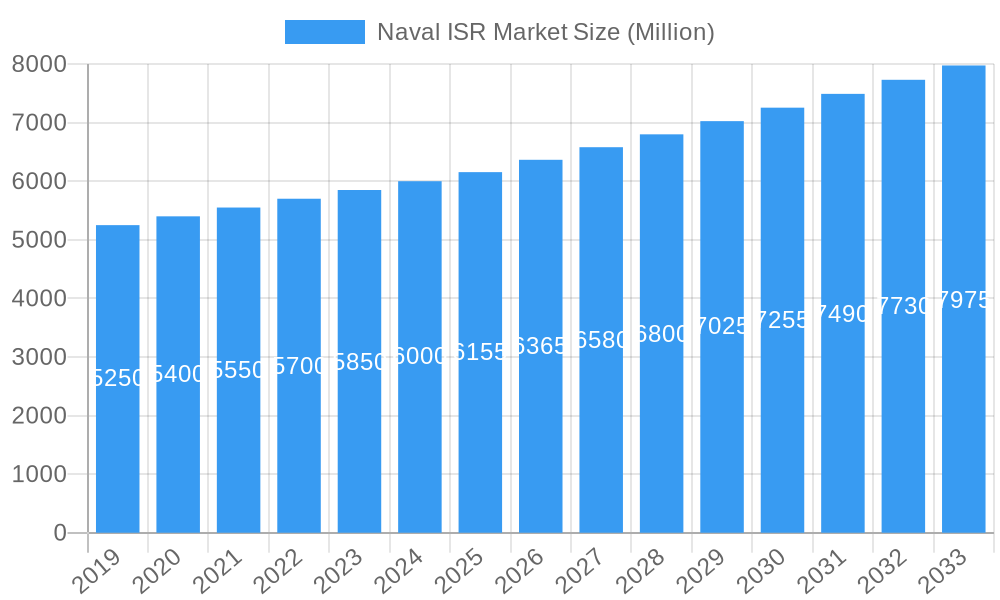

The Naval Intelligence, Surveillance, and Reconnaissance (ISR) market is poised for significant expansion, projected to reach a substantial market size by 2025 and demonstrating a steady compound annual growth rate (CAGR) of 3.50% through 2033. This growth is primarily fueled by the escalating geopolitical tensions and an increasing demand for enhanced maritime security across the globe. Nations are prioritizing the modernization of their naval fleets and investing heavily in advanced ISR capabilities to maintain situational awareness, deter potential adversaries, and protect vital maritime interests. The market is witnessing a strong impetus from defense applications, particularly in intelligence gathering, coastal surveillance, and tactical support, where real-time, accurate data is paramount for operational success. Furthermore, the growing emphasis on search and rescue operations, coupled with the expanding commercial use of naval ISR for activities such as fisheries monitoring and environmental protection, is contributing to this positive market trajectory. The increasing complexity of maritime threats, ranging from piracy and illegal trafficking to state-sponsored aggression, necessitates sophisticated ISR solutions, thereby driving innovation and market penetration.

Naval ISR Market Market Size (In Billion)

The evolution of naval ISR technology is characterized by the integration of artificial intelligence (AI), machine learning (ML), and advanced sensor technologies to process and analyze vast amounts of data more efficiently. Both surface vessel and underwater vessel ISR segments are experiencing robust growth, with advancements in drone technology, unmanned underwater vehicles (UUVs), and sophisticated radar and sonar systems enhancing operational capabilities. Key players such as General Dynamics Corporation, Leonardo SpA, and Lockheed Martin Corporation are at the forefront of this innovation, investing in research and development to offer cutting-edge solutions. Geographically, North America and Europe are expected to dominate the market, driven by substantial defense expenditures and the presence of major industry stakeholders. However, the Asia Pacific region is emerging as a high-growth market, propelled by increasing naval modernization efforts in countries like China and India. Restraints such as the high cost of advanced ISR systems and the complexities associated with integration and data management are being addressed through technological advancements and strategic partnerships, ensuring the continued upward momentum of the naval ISR market.

Naval ISR Market Company Market Share

Here is a comprehensive, SEO-optimized report description for the Naval ISR Market, designed for immediate use without modification.

Naval ISR Market: Comprehensive Market Intelligence and Future Outlook (2019-2033)

This in-depth report delivers critical market intelligence on the global Naval Intelligence, Surveillance, and Reconnaissance (ISR) market, a vital sector for maritime security, defense, and commercial operations. Spanning the historical period from 2019 to 2024, the base year of 2025, and a detailed forecast period extending to 2033, this analysis provides actionable insights for stakeholders. We examine market dynamics, growth trends, regional dominance, product innovations, key drivers, emerging opportunities, and the competitive landscape, with all values presented in Million Units.

Naval ISR Market Market Dynamics & Structure

The Naval ISR market is characterized by a moderate to high concentration, with major defense contractors and specialized technology providers dominating. Technological innovation remains a primary driver, fueled by advancements in artificial intelligence (AI), machine learning, sensor fusion, and unmanned systems. These innovations are crucial for enhancing situational awareness, threat detection, and operational effectiveness in complex maritime environments. Regulatory frameworks, primarily driven by national defense policies and international maritime law, significantly influence market access and product development, particularly for dual-use technologies. Competitive product substitutes are emerging, especially from commercial off-the-shelf (COTS) technologies being adapted for naval applications, posing a challenge to traditional, highly specialized systems. End-user demographics are predominantly government defense agencies, naval forces, and coast guards, with a growing segment of commercial maritime operators focusing on safety and security. Mergers and Acquisitions (M&A) trends indicate a strategic consolidation among key players to gain market share, acquire specialized technologies, and broaden their product portfolios. For instance, the market has witnessed several strategic acquisitions focused on expanding capabilities in areas like electronic warfare and autonomous systems, reflecting a drive for integrated solutions.

- Market Concentration: Moderate to High, with a few key players holding significant market share.

- Technological Innovation Drivers: AI, ML, sensor fusion, unmanned systems (UAVs, UUVs), advanced data analytics, secure communication networks.

- Regulatory Frameworks: Driven by national security mandates, international maritime laws, and defense procurement processes.

- Competitive Product Substitutes: Increasing adoption of COTS technologies adapted for naval use, open-architecture systems.

- End-User Demographics: Primarily naval forces, coast guards, maritime security agencies; growing commercial sector involvement.

- M&A Trends: Strategic consolidation for technology acquisition, market expansion, and portfolio integration.

Naval ISR Market Growth Trends & Insights

The global Naval ISR market is poised for robust growth, projected to expand at a significant Compound Annual Growth Rate (CAGR) from 2025 to 2033. This expansion is driven by an increasing recognition of the critical role of persistent maritime surveillance and reconnaissance in an era of escalating geopolitical tensions, piracy, illegal fishing, and environmental monitoring needs. The adoption rates for advanced ISR systems are accelerating as navies worldwide invest heavily in modernizing their fleets and enhancing their operational capabilities. Technological disruptions, particularly the integration of AI and machine learning into data processing and decision-making, are revolutionizing how naval forces gather and interpret intelligence, leading to faster response times and more effective mission outcomes. Consumer behavior shifts, characterized by a demand for more integrated, autonomous, and data-driven ISR solutions, are compelling manufacturers to innovate and offer smarter platforms. The market penetration of unmanned systems, both aerial and underwater, is a key indicator of this evolution, offering cost-effective and persistent surveillance capabilities without risking human lives. Furthermore, the increasing emphasis on cybersecurity for naval systems is a crucial factor shaping product development and adoption.

The market size evolution is a direct reflection of these trends. For example, the demand for advanced sonar systems for underwater surveillance is growing due to increased activity in underwater warfare and the need to monitor subsea infrastructure. Similarly, the proliferation of sophisticated electronic warfare capabilities within ISR platforms is becoming a standard requirement for modern naval forces. The shift towards multi-domain operations, where naval forces need to seamlessly integrate with air, land, and cyber domains, is further spurring the development of interoperable ISR systems. This necessitates platforms that can collect, process, and share vast amounts of data across different environments. The rising number of maritime incidents, from territorial disputes to humanitarian crises, underscores the indispensable nature of effective naval ISR, thereby creating sustained demand for cutting-edge solutions. The market is also influenced by evolving procurement strategies, with many nations opting for modular and scalable systems that can be upgraded as technology advances, ensuring long-term value and adaptability. The growing awareness of the importance of the blue economy and the need for maritime domain awareness (MDA) for resource management and environmental protection are also contributing to market expansion beyond purely defense applications.

Dominant Regions, Countries, or Segments in Naval ISR Market

The Defense operation segment is currently the dominant force driving growth in the global Naval ISR market. This dominance is propelled by sustained and increasing defense budgets across key nations, driven by geopolitical uncertainties, territorial disputes, and the imperative to maintain maritime superiority. Naval forces are the primary end-users, investing heavily in advanced Intelligence, Surveillance, and Reconnaissance capabilities to monitor vast ocean expanses, detect threats, and ensure national security. The application of Intelligence Gathering is intrinsically linked to this defense spending, as sophisticated ISR systems are crucial for collecting actionable intelligence on adversary activities, potential threats, and strategic movements.

- Dominant Segment: Defense Operation. This segment accounts for the largest market share due to significant government investment in naval modernization and security.

- Key Drivers: Rising geopolitical tensions, territorial disputes, piracy, illegal maritime activities, and the need for advanced situational awareness.

- Market Share: Expected to hold over 85% of the total market value within the forecast period.

- Growth Potential: Continued high growth driven by ongoing defense procurements and the modernization of existing naval fleets.

- Leading Application: Intelligence Gathering. This application is paramount for modern navies to maintain a strategic advantage.

- Key Drivers: The need for real-time threat assessment, intelligence collection on enemy forces, and proactive response to maritime incidents.

- Growth Potential: High growth, closely following defense spending, with advancements in data analytics and AI enhancing intelligence processing capabilities.

- Emerging Trends in Dominant Segments: Increasing integration of AI and machine learning for automated data analysis and threat identification within defense ISR operations.

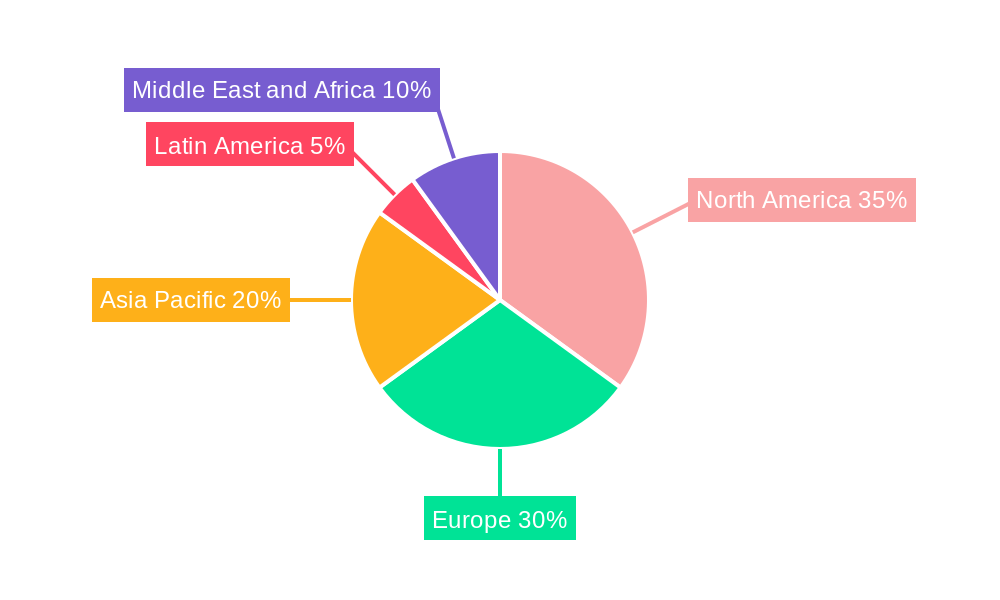

- Regional Dominance: North America and Europe currently lead due to established naval powers and significant R&D investments. However, the Asia-Pacific region is exhibiting the fastest growth, fueled by increasing naval capabilities and maritime security concerns.

- North America: High spending on advanced naval platforms and ISR technologies, driven by U.S. and Canadian defense initiatives.

- Europe: Strong emphasis on maritime security, naval modernization, and collaborative defense programs among EU nations.

- Asia-Pacific: Rapidly growing defense expenditure, particularly in countries like China, India, and South Korea, leading to substantial investment in naval ISR.

Naval ISR Market Product Landscape

The Naval ISR market is witnessing rapid product innovation focused on enhanced sensor capabilities, improved data processing, and greater platform autonomy. Innovations include the development of multi-spectral sensors, advanced radar systems with synthetic aperture radar (SAR) capabilities, and highly sensitive sonar arrays for underwater detection. Integration of AI and machine learning is a key trend, enabling real-time data analysis, target recognition, and automated anomaly detection. The performance metrics being enhanced include longer range detection, higher resolution imaging, improved signal-to-noise ratio, and greater endurance for unmanned systems. Unique selling propositions revolve around the ability to provide persistent, real-time situational awareness in challenging maritime environments. Technological advancements are also geared towards miniaturization and modularity, allowing for easier integration onto various naval platforms, from surface vessels to submarines and unmanned aerial vehicles (UAVs).

Key Drivers, Barriers & Challenges in Naval ISR Market

The Naval ISR market is propelled by several key drivers. The escalating geopolitical tensions and the rise of asymmetric warfare necessitate enhanced maritime domain awareness and persistent surveillance capabilities. Technological advancements in AI, sensor technology, and unmanned systems are enabling more sophisticated and cost-effective ISR solutions. Increasing focus on maritime security, including anti-piracy operations, counter-terrorism, and border patrol, further fuels demand. Growing adoption of dual-use technologies for commercial applications like search and rescue and environmental monitoring also contributes to market expansion.

- Technological Drivers: AI/ML for data analysis, advanced sensors (radar, sonar, EO/IR), unmanned systems (UAVs, UUVs), secure communication systems.

- Economic Drivers: Increased defense budgets, investments in naval modernization, demand for cost-effective surveillance.

- Policy Drivers: National security strategies, maritime security initiatives, international cooperation in defense.

However, the market faces significant barriers and challenges. High development and procurement costs for advanced naval ISR systems are a substantial restraint. The complex and lengthy procurement cycles within defense sectors can slow down market adoption. Cybersecurity threats and the need for robust data protection are critical challenges, requiring significant investment in secure infrastructure. Integration complexities with existing legacy systems and the need for skilled personnel to operate and maintain advanced ISR technology also pose hurdles. Supply chain disruptions and geopolitical instability can impact the availability of specialized components.

- High Costs: Significant capital investment required for R&D and procurement of advanced systems.

- Long Procurement Cycles: Extended timelines for defense contract awards and system deployments.

- Cybersecurity Threats: Vulnerability of connected systems to cyberattacks requires constant vigilance and investment.

- Integration Complexity: Challenges in integrating new systems with existing naval platforms and infrastructure.

- Skilled Workforce: Demand for highly trained personnel to operate, maintain, and interpret data from advanced ISR systems.

- Supply Chain Vulnerability: Reliance on specialized components can be impacted by global disruptions.

Emerging Opportunities in Naval ISR Market

Emerging opportunities in the Naval ISR market lie in the increasing integration of AI and machine learning for predictive analytics and autonomous operations. The expansion of unmanned underwater vehicles (UUVs) for persistent, long-duration surveillance missions presents a significant growth area. Furthermore, the growing demand for integrated ISR solutions that combine data from multiple sensor types (e.g., radar, electro-optical/infrared, acoustic) to create a comprehensive maritime picture offers substantial potential. The increasing need for maritime domain awareness (MDA) for commercial applications, such as fisheries monitoring, environmental protection, and offshore resource management, opens up new market segments beyond traditional defense. The development of sovereign ISR capabilities by emerging naval powers also presents a lucrative opportunity for technology providers.

Growth Accelerators in the Naval ISR Market Industry

Key growth accelerators in the Naval ISR market include the relentless pursuit of technological superiority by major naval powers, driving continuous innovation and investment in next-generation ISR systems. The growing adoption of AI and machine learning is fundamentally transforming data processing and decision-making, making ISR capabilities more efficient and effective. Strategic partnerships and collaborations between defense contractors, technology companies, and research institutions are fostering accelerated development and deployment of advanced solutions. Market expansion strategies, particularly the increasing focus on the Asia-Pacific region due to its rapidly growing naval capacities and maritime security concerns, are significant growth catalysts. The evolving nature of warfare, emphasizing information dominance and multi-domain operations, further underscores the critical importance and demand for robust naval ISR capabilities.

Key Players Shaping the Naval ISR Market Market

- General Dynamics Corporation

- Leonardo SpA

- Lockheed Martin Corporation

- Kratos Defense and Security Solutions

- Atlas Elektronik

- Thales Group

- BAE Systems PLC

- Rheinmetall Defense

- Northrop Grumann Corporation

- Elbit Systems

- L3 Harris Technologies

- Ultra Electronics

Notable Milestones in Naval ISR Market Sector

- 2019: Introduction of AI-powered data fusion algorithms significantly enhancing target identification accuracy.

- 2020: Launch of advanced, long-endurance Unmanned Surface Vehicles (USVs) for persistent maritime surveillance.

- 2021: Major defense contracts awarded for the development of next-generation integrated electronic warfare and ISR systems for naval fleets.

- 2022: Significant advancements in synthetic aperture radar (SAR) technology for all-weather maritime surveillance.

- 2023: Increased investment in cybersecurity solutions for naval ISR platforms to combat evolving threats.

- January 2024: Unveiling of new, modular ISR payloads for rapid deployment on various naval platforms.

- March 2024: Strategic acquisition by a major defense player to enhance its capabilities in unmanned underwater systems.

- June 2024: Demonstration of advanced sensor fusion capabilities from multi-domain assets for enhanced maritime situational awareness.

- August 2024: Development of secure quantum communication protocols for naval ISR data transmission.

- October 2024: Increased focus on predictive maintenance for naval ISR equipment to ensure operational readiness.

In-Depth Naval ISR Market Market Outlook

The future outlook for the Naval ISR market is exceptionally strong, driven by an unyielding demand for enhanced maritime security and an accelerating pace of technological innovation. Growth accelerators such as the widespread integration of AI for sophisticated data analysis and autonomous decision-making, coupled with the proliferation of advanced unmanned systems (UUVs and UAVs), will redefine operational paradigms. Strategic partnerships and significant investments in emerging markets, particularly in the Asia-Pacific region, will further fuel expansion. The continuous evolution of warfare, demanding superior information dominance and multi-domain interoperability, ensures that naval ISR will remain a cornerstone of national defense strategies, presenting sustained opportunities for market growth and development.

Naval ISR Market Segmentation

-

1. Type

- 1.1. Surface Vessel ISR

- 1.2. Underwater Vessel ISR

-

2. Operation

- 2.1. Defense

- 2.2. Commercial

-

3. Application

- 3.1. Search & Rescue

- 3.2. Intelligence Gathering

- 3.3. Coastal Surveillance

- 3.4. Tactical Support

Naval ISR Market Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Russia

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Latin America

-

5. Middle East and Africa

- 5.1. United Arab Emirates

- 5.2. Saudi Arabia

- 5.3. Rest of Middle East and Africa

Naval ISR Market Regional Market Share

Geographic Coverage of Naval ISR Market

Naval ISR Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.35% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Surface Vessel ISR

- 5.1.2. Underwater Vessel ISR

- 5.2. Market Analysis, Insights and Forecast - by Operation

- 5.2.1. Defense

- 5.2.2. Commercial

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Search & Rescue

- 5.3.2. Intelligence Gathering

- 5.3.3. Coastal Surveillance

- 5.3.4. Tactical Support

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Naval ISR Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Surface Vessel ISR

- 6.1.2. Underwater Vessel ISR

- 6.2. Market Analysis, Insights and Forecast - by Operation

- 6.2.1. Defense

- 6.2.2. Commercial

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Search & Rescue

- 6.3.2. Intelligence Gathering

- 6.3.3. Coastal Surveillance

- 6.3.4. Tactical Support

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Naval ISR Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Surface Vessel ISR

- 7.1.2. Underwater Vessel ISR

- 7.2. Market Analysis, Insights and Forecast - by Operation

- 7.2.1. Defense

- 7.2.2. Commercial

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Search & Rescue

- 7.3.2. Intelligence Gathering

- 7.3.3. Coastal Surveillance

- 7.3.4. Tactical Support

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Naval ISR Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Surface Vessel ISR

- 8.1.2. Underwater Vessel ISR

- 8.2. Market Analysis, Insights and Forecast - by Operation

- 8.2.1. Defense

- 8.2.2. Commercial

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Search & Rescue

- 8.3.2. Intelligence Gathering

- 8.3.3. Coastal Surveillance

- 8.3.4. Tactical Support

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Asia Pacific Naval ISR Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Surface Vessel ISR

- 9.1.2. Underwater Vessel ISR

- 9.2. Market Analysis, Insights and Forecast - by Operation

- 9.2.1. Defense

- 9.2.2. Commercial

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Search & Rescue

- 9.3.2. Intelligence Gathering

- 9.3.3. Coastal Surveillance

- 9.3.4. Tactical Support

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Latin America Naval ISR Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Surface Vessel ISR

- 10.1.2. Underwater Vessel ISR

- 10.2. Market Analysis, Insights and Forecast - by Operation

- 10.2.1. Defense

- 10.2.2. Commercial

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Search & Rescue

- 10.3.2. Intelligence Gathering

- 10.3.3. Coastal Surveillance

- 10.3.4. Tactical Support

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Middle East and Africa Naval ISR Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Surface Vessel ISR

- 11.1.2. Underwater Vessel ISR

- 11.2. Market Analysis, Insights and Forecast - by Operation

- 11.2.1. Defense

- 11.2.2. Commercial

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Search & Rescue

- 11.3.2. Intelligence Gathering

- 11.3.3. Coastal Surveillance

- 11.3.4. Tactical Support

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 General Dynamics Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Leonardo SpA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Lockheed Martin Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Kratos Defense and Security Solutions

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Atlas Elektronik

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Thales Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 BAE Systems PLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Rheinmetall Defense*List Not Exhaustive

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Northrop Grumann Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Elbit Systems

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 L3 Harris Technologies

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Ultra Electronics

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 General Dynamics Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Naval ISR Market Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Naval ISR Market Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Naval ISR Market Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Naval ISR Market Revenue (billion), by Operation 2025 & 2033

- Figure 5: North America Naval ISR Market Revenue Share (%), by Operation 2025 & 2033

- Figure 6: North America Naval ISR Market Revenue (billion), by Application 2025 & 2033

- Figure 7: North America Naval ISR Market Revenue Share (%), by Application 2025 & 2033

- Figure 8: North America Naval ISR Market Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Naval ISR Market Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Naval ISR Market Revenue (billion), by Type 2025 & 2033

- Figure 11: Europe Naval ISR Market Revenue Share (%), by Type 2025 & 2033

- Figure 12: Europe Naval ISR Market Revenue (billion), by Operation 2025 & 2033

- Figure 13: Europe Naval ISR Market Revenue Share (%), by Operation 2025 & 2033

- Figure 14: Europe Naval ISR Market Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Naval ISR Market Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Naval ISR Market Revenue (billion), by Country 2025 & 2033

- Figure 17: Europe Naval ISR Market Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Naval ISR Market Revenue (billion), by Type 2025 & 2033

- Figure 19: Asia Pacific Naval ISR Market Revenue Share (%), by Type 2025 & 2033

- Figure 20: Asia Pacific Naval ISR Market Revenue (billion), by Operation 2025 & 2033

- Figure 21: Asia Pacific Naval ISR Market Revenue Share (%), by Operation 2025 & 2033

- Figure 22: Asia Pacific Naval ISR Market Revenue (billion), by Application 2025 & 2033

- Figure 23: Asia Pacific Naval ISR Market Revenue Share (%), by Application 2025 & 2033

- Figure 24: Asia Pacific Naval ISR Market Revenue (billion), by Country 2025 & 2033

- Figure 25: Asia Pacific Naval ISR Market Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Naval ISR Market Revenue (billion), by Type 2025 & 2033

- Figure 27: Latin America Naval ISR Market Revenue Share (%), by Type 2025 & 2033

- Figure 28: Latin America Naval ISR Market Revenue (billion), by Operation 2025 & 2033

- Figure 29: Latin America Naval ISR Market Revenue Share (%), by Operation 2025 & 2033

- Figure 30: Latin America Naval ISR Market Revenue (billion), by Application 2025 & 2033

- Figure 31: Latin America Naval ISR Market Revenue Share (%), by Application 2025 & 2033

- Figure 32: Latin America Naval ISR Market Revenue (billion), by Country 2025 & 2033

- Figure 33: Latin America Naval ISR Market Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Naval ISR Market Revenue (billion), by Type 2025 & 2033

- Figure 35: Middle East and Africa Naval ISR Market Revenue Share (%), by Type 2025 & 2033

- Figure 36: Middle East and Africa Naval ISR Market Revenue (billion), by Operation 2025 & 2033

- Figure 37: Middle East and Africa Naval ISR Market Revenue Share (%), by Operation 2025 & 2033

- Figure 38: Middle East and Africa Naval ISR Market Revenue (billion), by Application 2025 & 2033

- Figure 39: Middle East and Africa Naval ISR Market Revenue Share (%), by Application 2025 & 2033

- Figure 40: Middle East and Africa Naval ISR Market Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East and Africa Naval ISR Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Naval ISR Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Naval ISR Market Revenue billion Forecast, by Operation 2020 & 2033

- Table 3: Global Naval ISR Market Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Global Naval ISR Market Revenue billion Forecast, by Region 2020 & 2033

- Table 5: Global Naval ISR Market Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Naval ISR Market Revenue billion Forecast, by Operation 2020 & 2033

- Table 7: Global Naval ISR Market Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Naval ISR Market Revenue billion Forecast, by Country 2020 & 2033

- Table 9: United States Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Canada Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Global Naval ISR Market Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Naval ISR Market Revenue billion Forecast, by Operation 2020 & 2033

- Table 13: Global Naval ISR Market Revenue billion Forecast, by Application 2020 & 2033

- Table 14: Global Naval ISR Market Revenue billion Forecast, by Country 2020 & 2033

- Table 15: Germany Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: United Kingdom Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: France Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Russia Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Spain Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Global Naval ISR Market Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Global Naval ISR Market Revenue billion Forecast, by Operation 2020 & 2033

- Table 23: Global Naval ISR Market Revenue billion Forecast, by Application 2020 & 2033

- Table 24: Global Naval ISR Market Revenue billion Forecast, by Country 2020 & 2033

- Table 25: China Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: India Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Japan Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: South Korea Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: Rest of Asia Pacific Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Global Naval ISR Market Revenue billion Forecast, by Type 2020 & 2033

- Table 31: Global Naval ISR Market Revenue billion Forecast, by Operation 2020 & 2033

- Table 32: Global Naval ISR Market Revenue billion Forecast, by Application 2020 & 2033

- Table 33: Global Naval ISR Market Revenue billion Forecast, by Country 2020 & 2033

- Table 34: Brazil Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Latin America Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Global Naval ISR Market Revenue billion Forecast, by Type 2020 & 2033

- Table 37: Global Naval ISR Market Revenue billion Forecast, by Operation 2020 & 2033

- Table 38: Global Naval ISR Market Revenue billion Forecast, by Application 2020 & 2033

- Table 39: Global Naval ISR Market Revenue billion Forecast, by Country 2020 & 2033

- Table 40: United Arab Emirates Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: Saudi Arabia Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Rest of Middle East and Africa Naval ISR Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Naval ISR Market?

The projected CAGR is approximately 5.35%.

2. Which companies are prominent players in the Naval ISR Market?

Key companies in the market include General Dynamics Corporation, Leonardo SpA, Lockheed Martin Corporation, Kratos Defense and Security Solutions, Atlas Elektronik, Thales Group, BAE Systems PLC, Rheinmetall Defense*List Not Exhaustive, Northrop Grumann Corporation, Elbit Systems, L3 Harris Technologies, Ultra Electronics.

3. What are the main segments of the Naval ISR Market?

The market segments include Type, Operation, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 8.8 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Underwater Vessel ISR is Expected to Witness Growth During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Naval ISR Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Naval ISR Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Naval ISR Market?

To stay informed about further developments, trends, and reports in the Naval ISR Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence