Key Insights

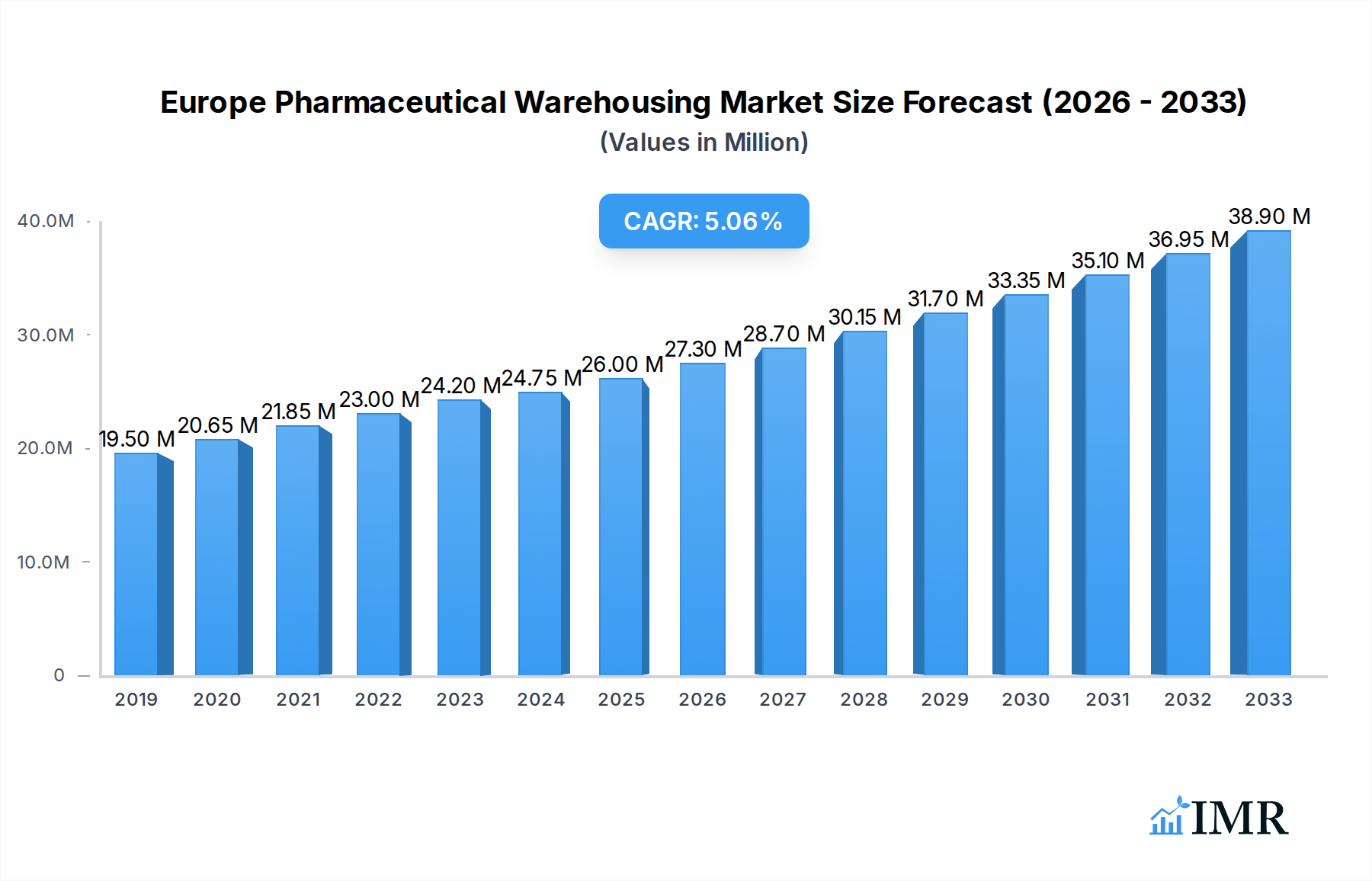

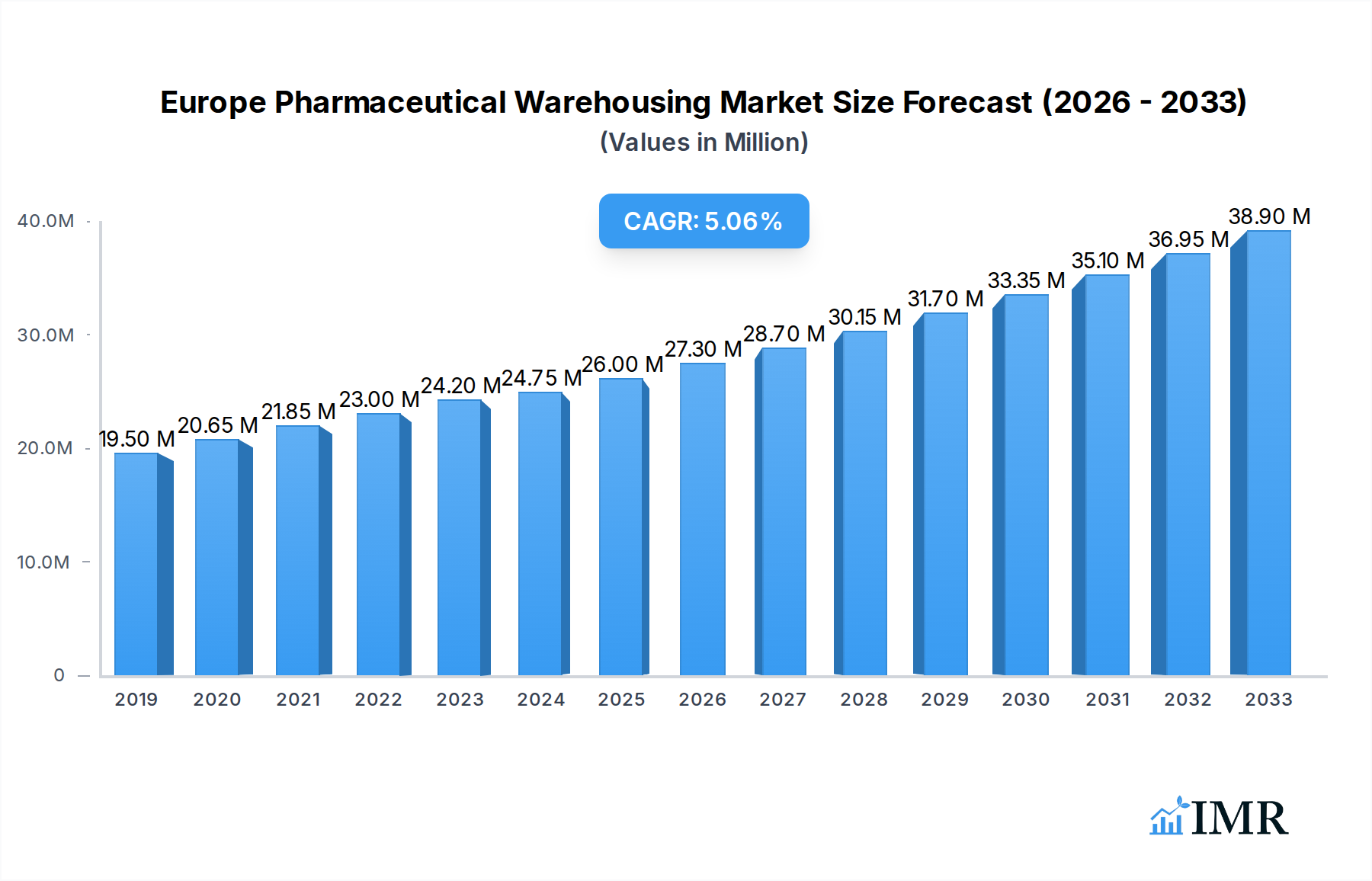

The Europe Pharmaceutical Warehousing Market is poised for significant expansion, projecting a current market size of 24.75 Million and a robust Compound Annual Growth Rate (CAGR) of over 8.26% through 2033. This dynamic growth is primarily propelled by the increasing complexity of pharmaceutical supply chains, a heightened demand for specialized cold chain logistics to preserve sensitive biologics and vaccines, and stringent regulatory compliance requirements across the continent. The expanding pharmaceutical manufacturing sector, coupled with a growing network of pharmacies and hospitals increasingly reliant on efficient and secure warehousing solutions, forms the bedrock of this upward trajectory. Furthermore, advancements in warehouse automation and digital supply chain technologies are enhancing operational efficiency and traceability, addressing the sector's need for precision and reliability.

Europe Pharmaceutical Warehousing Market Market Size (In Million)

Key market drivers include the escalating production of high-value biopharmaceuticals, requiring sophisticated temperature-controlled storage and handling. The rise of e-pharmacies and the growing emphasis on patient-centric healthcare models also contribute to the demand for agile and distributed warehousing networks. However, the market faces certain restraints, such as the high initial investment costs for establishing advanced cold chain facilities and the ongoing challenge of finding and retaining skilled labor proficient in pharmaceutical logistics. Navigating diverse national regulatory landscapes within Europe also presents complexities. Despite these challenges, the overarching trend towards supply chain optimization and the continuous innovation in warehousing technologies are expected to foster substantial market growth, with segments like cold chain warehouses and applications in pharmaceutical factories and hospitals leading the charge.

Europe Pharmaceutical Warehousing Market Company Market Share

This in-depth report offers a definitive analysis of the Europe Pharmaceutical Warehousing Market, a critical component of the continent's robust healthcare and pharmaceutical supply chain. Covering the Study Period of 2019–2033, with a Base Year and Estimated Year of 2025, and a Forecast Period of 2025–2033, this report meticulously details market dynamics, growth trends, regional dominance, product landscape, key drivers, barriers, challenges, emerging opportunities, and the strategic initiatives of leading players. Designed for industry professionals, logistics providers, pharmaceutical manufacturers, and investors, this report provides actionable insights into the evolving European cold chain logistics and pharmaceutical storage solutions.

Europe Pharmaceutical Warehousing Market Market Dynamics & Structure

The Europe Pharmaceutical Warehousing Market is characterized by a moderate to high level of concentration, with major global logistics providers and specialized healthcare logistics companies vying for market share. Technological innovation is a significant driver, particularly in the realm of advanced temperature monitoring, automation, and data analytics, essential for maintaining the integrity of sensitive pharmaceutical products. Regulatory frameworks, including Good Distribution Practices (GDP), play a crucial role in dictating operational standards and quality control. Competitive product substitutes are limited due to the highly specialized nature of pharmaceutical warehousing, but inefficiencies in existing facilities can be considered a form of indirect competition. End-user demographics are diverse, encompassing pharmaceutical factories, pharmacies, hospitals, and other healthcare entities, each with unique warehousing requirements. Mergers and acquisitions (M&A) are a notable trend, with companies expanding their network and capabilities to cater to increasing demand for integrated pharma logistics Europe.

- Market Concentration: Dominated by a mix of global giants and specialized players.

- Technological Innovation Drivers: Automation, IoT for temperature monitoring, AI for route optimization.

- Regulatory Frameworks: Strict adherence to GDP, EMA guidelines.

- Competitive Product Substitutes: Limited, but operational inefficiencies in existing infrastructure are a factor.

- End-User Demographics: Pharmaceutical manufacturers, wholesalers, hospitals, pharmacies, research institutions.

- M&A Trends: Strategic acquisitions to expand cold chain capacity and geographical reach.

Europe Pharmaceutical Warehousing Market Growth Trends & Insights

The Europe Pharmaceutical Warehousing Market is poised for substantial growth, driven by an aging population, increasing prevalence of chronic diseases, and the continuous development of new biologics and specialty pharmaceuticals requiring stringent storage conditions. The European cold chain warehouse market is particularly experiencing robust expansion, fueled by the growing demand for vaccines, biopharmaceuticals, and temperature-sensitive drugs. Market penetration of advanced logistics solutions is on the rise, as companies recognize the importance of reliable pharmaceutical warehousing solutions Europe for product integrity and patient safety. Technological disruptions, such as the implementation of blockchain for enhanced traceability and the use of robotics in warehouses, are transforming operational efficiencies. Consumer behavior shifts towards greater demand for timely and secure delivery of medications further underscore the need for sophisticated warehousing infrastructure. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period, reaching an estimated €45,000 million by 2033.

- Market Size Evolution: Steady growth driven by healthcare demand and biopharmaceutical advancements.

- Adoption Rates: Increasing adoption of advanced technologies and specialized warehousing.

- Technological Disruptions: Blockchain, AI, robotics, and IoT for enhanced efficiency and traceability.

- Consumer Behavior Shifts: Demand for faster, more reliable, and secure medication delivery.

- Key Metrics: Projected CAGR of 6.5% from 2025-2033.

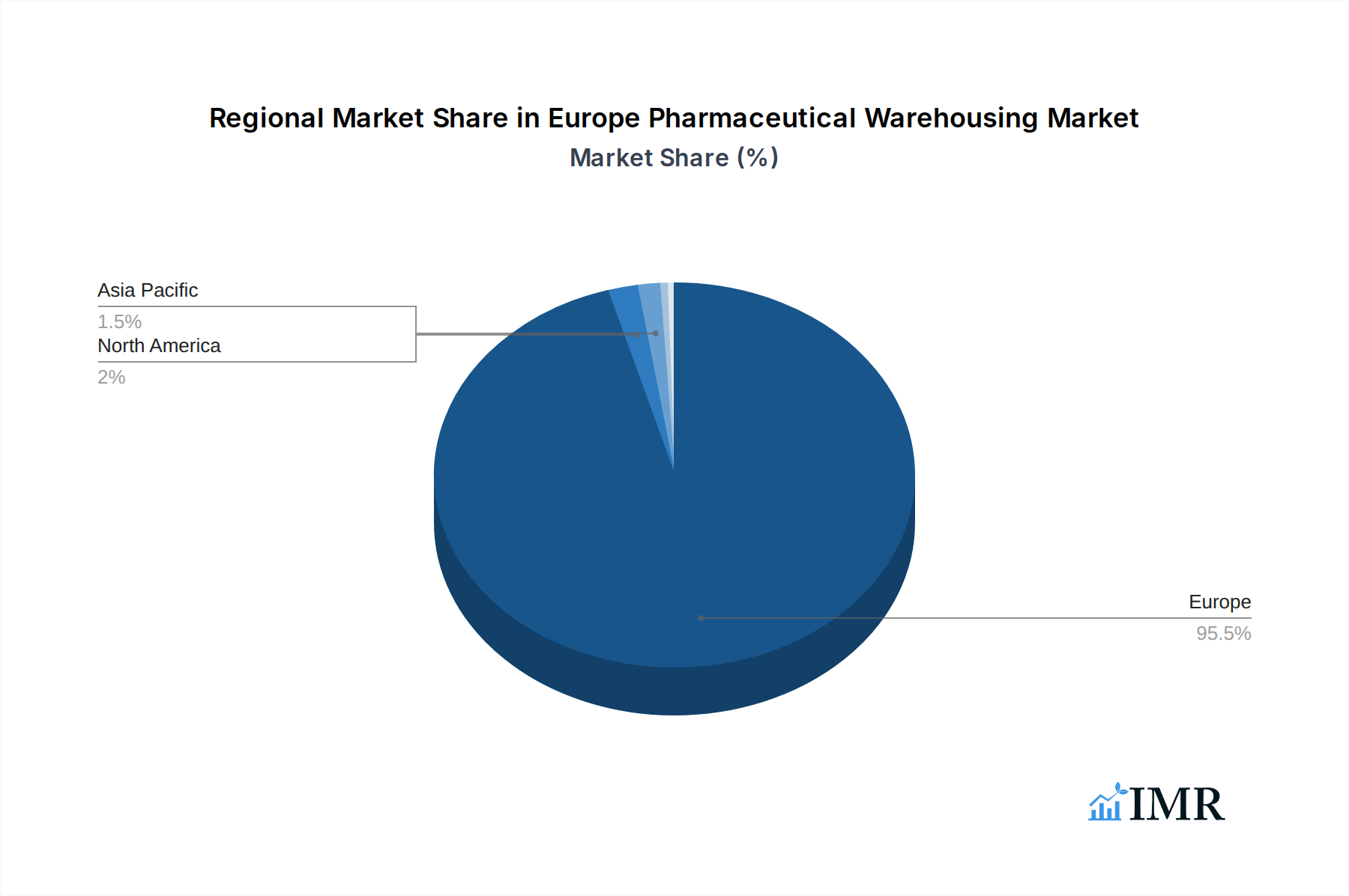

Dominant Regions, Countries, or Segments in Europe Pharmaceutical Warehousing Market

Within the Europe Pharmaceutical Warehousing Market, Germany consistently emerges as a dominant country, owing to its significant pharmaceutical manufacturing base, advanced healthcare infrastructure, and a strong network of logistics providers. The Cold Chain Warehouse segment is a primary growth engine, driven by the escalating production and distribution of vaccines, biologics, and gene therapies. These specialized facilities are critical for maintaining the efficacy of temperature-sensitive pharmaceuticals, and their demand significantly outweighs that of non-cold chain counterparts in many regions. Application-wise, the Pharmaceutical Factory segment holds a substantial market share, as manufacturers require secure and compliant storage for raw materials, work-in-progress, and finished goods. However, the Hospital segment is also witnessing rapid growth due to increasing direct-to-patient distribution models and the need for on-site pharmaceutical inventory management.

- Leading Region/Country: Germany, followed by the UK, France, and the Netherlands.

- Dominant Segment (Type): Cold Chain Warehouse, driven by biologics and vaccines.

- Key Drivers for Cold Chain Dominance: Biopharmaceutical innovation, vaccine distribution, stringent temperature requirements.

- Dominant Segment (Application): Pharmaceutical Factory due to large-scale production and storage needs.

- Growth Potential in Hospital Segment: Increasing demand for on-site inventory and direct-to-patient models.

- Market Share Snapshot: Cold Chain Warehousing estimated to capture 60% of the total market value by 2025.

Europe Pharmaceutical Warehousing Market Product Landscape

The product landscape in the Europe Pharmaceutical Warehousing Market is defined by innovative infrastructure and advanced technological integrations. This includes state-of-the-art temperature-controlled facilities equipped with redundant cooling systems and real-time monitoring capabilities, ensuring product integrity across a range of temperature requirements from ambient to ultra-low. Advanced Warehouse Management Systems (WMS) with specialized modules for pharmaceutical compliance, such as GDP compliance tracking and serialization management, are standard. Furthermore, the integration of Internet of Things (IoT) devices for continuous environmental monitoring and predictive maintenance is enhancing operational reliability. Performance metrics are rigorously tracked, focusing on temperature excursion rates (target <0.05%), order accuracy (target >99.5%), and inventory turnover.

Key Drivers, Barriers & Challenges in Europe Pharmaceutical Warehousing Market

Key Drivers:

- Increasing Biopharmaceutical Production: The burgeoning biopharmaceutical sector necessitates specialized cold chain logistics.

- Aging Population and Chronic Diseases: Growing demand for pharmaceuticals and their complex storage needs.

- Stricter Regulatory Compliance: Robust GDP regulations drive investment in compliant warehousing.

- Technological Advancements: Automation and IoT enhance efficiency and product integrity.

Barriers & Challenges:

- High Capital Investment: Establishing and maintaining specialized pharmaceutical warehouses, especially cold chain facilities, requires significant upfront investment.

- Complex Regulatory Landscape: Navigating diverse national and EU regulations can be challenging and costly.

- Supply Chain Disruptions: Geopolitical events, pandemics, and infrastructure limitations can impact the smooth flow of goods.

- Talent Shortage: Finding skilled personnel for specialized pharmaceutical logistics operations.

- Sustainability Pressures: Balancing operational efficiency with environmental considerations and reducing carbon footprint.

Emerging Opportunities in Europe Pharmaceutical Warehousing Market

Emerging opportunities in the Europe Pharmaceutical Warehousing Market lie in the expansion of specialized cold chain services to accommodate the growing pipeline of biologics, cell and gene therapies, and personalized medicine. The increasing adoption of direct-to-patient (DTP) delivery models presents a significant opportunity for localized, temperature-controlled micro-fulfillment centers within urban areas. Furthermore, the integration of advanced data analytics and AI for demand forecasting and inventory optimization offers a pathway for service providers to offer more value-added services. Untapped markets within Eastern Europe, with developing healthcare infrastructures, also present significant growth potential for well-established logistics players.

Growth Accelerators in the Europe Pharmaceutical Warehousing Market Industry

Several catalysts are accelerating the growth of the Europe Pharmaceutical Warehousing Market. Technological breakthroughs in cold chain infrastructure, such as advanced insulation materials and energy-efficient refrigeration systems, are reducing operational costs and environmental impact. Strategic partnerships between pharmaceutical manufacturers and specialized logistics providers are becoming increasingly common, fostering innovation and ensuring end-to-end supply chain visibility. Market expansion strategies, including the establishment of new facilities in key geographical hubs and the acquisition of smaller, specialized operators, are enabling companies to broaden their service offerings and geographical reach, thereby capturing a larger share of the growing market. The continuous innovation in drug discovery and development, particularly in areas requiring complex handling, directly fuels the demand for sophisticated warehousing solutions.

Key Players Shaping the Europe Pharmaceutical Warehousing Market Market

- DB Schenker

- United Parcel Service Inc

- Hellmann Worldwide Logistics SE and Co KG

- Alloga

- FedEx Corp

- Rhenus SE and Co KG

- Bio Pharma Logistics

- Kuehne Nagel Management AG

- XPO Logistics Inc

- GEODIS SA

- KRC Logistics

Notable Milestones in Europe Pharmaceutical Warehousing Market Sector

- June 2023: ViaPharma signed a 20-year lease agreement with the developer CTP for two Czech CTParks. CTP will prepare and hand over the premises, with a total area of almost 27,000 sq m and several specific modifications for the pharmaceutical industry, at the end of 2023. CTPark Ostrava Poruba and CTPark Brno Líšeň will be the next locations of cooperation. ViaPharma already leased three warehouses in Romania, including the largest ever pharmaceutical warehouse in the country with an area of 35,000 sq m in CTPark Mogosoaia. This expansion highlights increased investment in specialized pharmaceutical storage infrastructure across Central Europe.

- August 2022: UPS announced the acquisition of a top healthcare logistics provider in Italy, BomiGroup. This acquisition was expected to invoke the addition of temperature-controlled facilities in 14 countries. This strategic move significantly bolsters UPS's cold chain capabilities and expands its healthcare logistics network across key European markets, demonstrating a trend of consolidation and capability enhancement in the sector.

In-Depth Europe Pharmaceutical Warehousing Market Market Outlook

The future outlook for the Europe Pharmaceutical Warehousing Market is exceptionally positive, driven by persistent growth in the pharmaceutical sector and an increasing emphasis on supply chain resilience and efficiency. Key growth accelerators include the ongoing advancements in biologics and advanced therapy medicinal products (ATMPs) which demand highly specialized, temperature-controlled storage and handling. Strategic partnerships between pharmaceutical manufacturers and logistics providers will continue to foster innovation in areas like real-time data visibility and predictive analytics. Furthermore, the drive towards greater sustainability within the logistics industry will encourage the adoption of eco-friendly warehousing solutions, presenting opportunities for forward-thinking companies. The market is expected to witness further consolidation as larger players acquire specialized niche providers to enhance their service portfolios and geographical coverage, solidifying a robust and increasingly sophisticated European pharma logistics ecosystem.

Europe Pharmaceutical Warehousing Market Segmentation

-

1. Type

- 1.1. Cold Chain Warehouse

- 1.2. Non-Cold Chain Warehouse

-

2. Application

- 2.1. Pharmaceutical Factory

- 2.2. Pharmacy

- 2.3. Hospital

- 2.4. Others

Europe Pharmaceutical Warehousing Market Segmentation By Geography

-

1. Europe

- 1.1. Germany

- 1.2. UK

- 1.3. France

- 1.4. Russia

- 1.5. Spain

- 1.6. Rest of Europe

Europe Pharmaceutical Warehousing Market Regional Market Share

Geographic Coverage of Europe Pharmaceutical Warehousing Market

Europe Pharmaceutical Warehousing Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of > 8.26% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Cold Chain Warehouse

- 5.1.2. Non-Cold Chain Warehouse

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Pharmaceutical Factory

- 5.2.2. Pharmacy

- 5.2.3. Hospital

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Pharmaceutical Warehousing Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Cold Chain Warehouse

- 6.1.2. Non-Cold Chain Warehouse

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Pharmaceutical Factory

- 6.2.2. Pharmacy

- 6.2.3. Hospital

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 DB Schenker

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 United Parcel Service Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Hellmann Worldwide Logistics SE and Co KG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Alloga

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 FedEx Corp

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Rhenus SE and Co KG

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Bio Pharma Logistics

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Kuehne Nagel Management AG

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 XPO Logistics Inc **List Not Exhaustive

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 GEODIS SA

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 KRC Logistics

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.1 DB Schenker

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Pharmaceutical Warehousing Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Pharmaceutical Warehousing Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Pharmaceutical Warehousing Market Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Europe Pharmaceutical Warehousing Market Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Europe Pharmaceutical Warehousing Market Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Europe Pharmaceutical Warehousing Market Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Europe Pharmaceutical Warehousing Market Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Europe Pharmaceutical Warehousing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Germany Europe Pharmaceutical Warehousing Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: UK Europe Pharmaceutical Warehousing Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: France Europe Pharmaceutical Warehousing Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Russia Europe Pharmaceutical Warehousing Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe Pharmaceutical Warehousing Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Rest of Europe Europe Pharmaceutical Warehousing Market Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Pharmaceutical Warehousing Market?

The projected CAGR is approximately > 8.26%.

2. Which companies are prominent players in the Europe Pharmaceutical Warehousing Market?

Key companies in the market include DB Schenker, United Parcel Service Inc, Hellmann Worldwide Logistics SE and Co KG, Alloga, FedEx Corp, Rhenus SE and Co KG, Bio Pharma Logistics, Kuehne Nagel Management AG, XPO Logistics Inc **List Not Exhaustive, GEODIS SA, KRC Logistics.

3. What are the main segments of the Europe Pharmaceutical Warehousing Market?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 24.75 Million as of 2022.

5. What are some drivers contributing to market growth?

The rise in demand for outsourcing pharmaceutical warehousing services; The demand for efficiency. visibility. and product safety from pharmaceutical companies.

6. What are the notable trends driving market growth?

Rise in the demand Pharmaceutical.

7. Are there any restraints impacting market growth?

Lack of efficient logistics support in emerging economies.

8. Can you provide examples of recent developments in the market?

June 2023: ViaPharma signed a 20-year lease agreement with the developer CTP for two Czech CTParks. CTP will prepare and hand over the premises, with a total area of almost 27,000 sq m and several specific modifications for the pharmaceutical industry, at the end of 2023. CTPark Ostrava Poruba and CTPark Brno Líšeň will be the next locations of cooperation. ViaPharma already leased three warehouses in Romania, including the largest ever pharmaceutical warehouse in the country with an area of 35,000 sq m in CTPark Mogosoaia.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Pharmaceutical Warehousing Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Pharmaceutical Warehousing Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Pharmaceutical Warehousing Market?

To stay informed about further developments, trends, and reports in the Europe Pharmaceutical Warehousing Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence