Key Insights

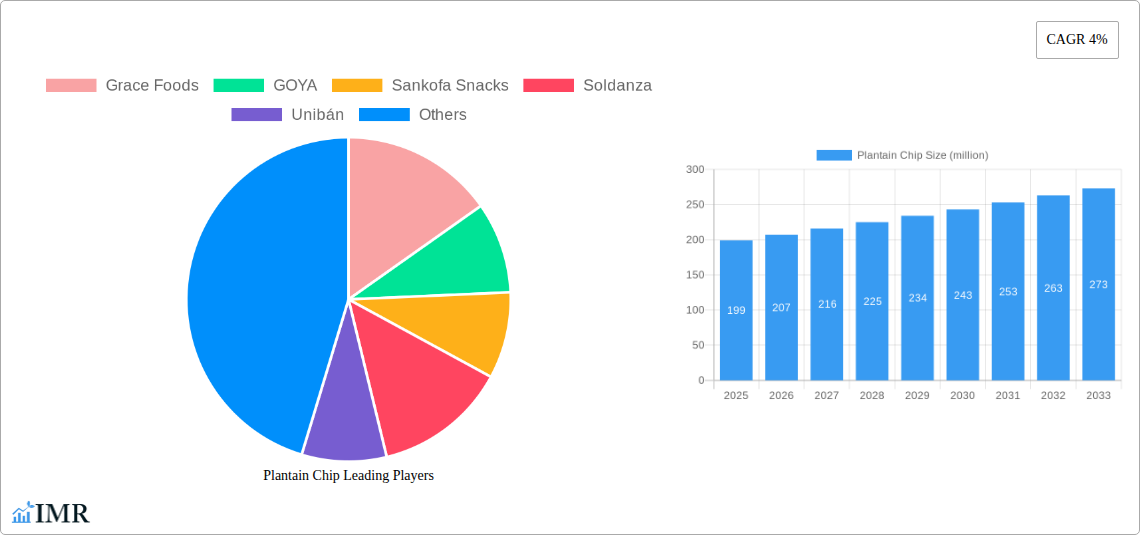

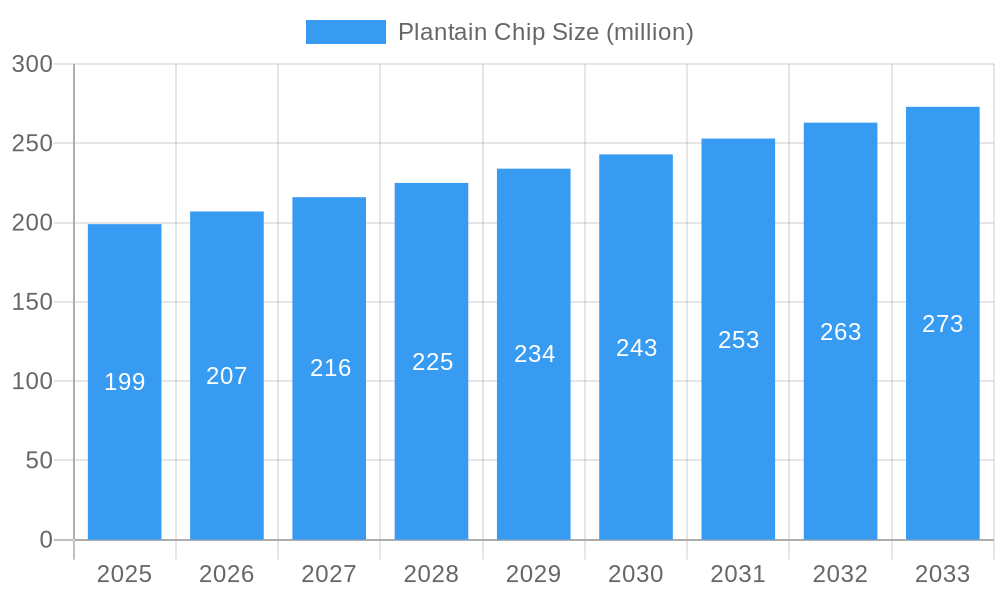

The global plantain chip market is poised for steady growth, projected to reach approximately $199 million with a Compound Annual Growth Rate (CAGR) of around 4% from 2025 to 2033. This expansion is primarily fueled by the increasing consumer preference for healthier snack alternatives, the growing popularity of ethnic and international cuisines, and the versatile nature of plantain chips as a gluten-free and often allergen-friendly option. The convenience of online sales channels is significantly contributing to market penetration, making these snacks accessible to a wider audience. Furthermore, the rising disposable incomes in emerging economies and a growing awareness of the nutritional benefits associated with plantains are expected to drive demand. Innovations in flavor profiles, including both sweet and unsweetened varieties, are catering to diverse palates, further stimulating market engagement. The convenience factor, coupled with the appealing taste and texture of plantain chips, solidifies their position as a sought-after snack in the global market.

Plantain Chip Market Size (In Million)

The market landscape is characterized by a dynamic competitive environment, with key players like Grace Foods, GOYA, and Sankofa Snacks actively engaged in product innovation and market expansion. The strategic presence of these companies across North America, South America, Europe, and the Middle East & Africa highlights the global appeal of plantain chips. While the market is experiencing robust growth, certain factors could pose challenges. These might include the price volatility of raw plantain crops, which can impact production costs, and intense competition from established snack categories. Nevertheless, the upward trend in health-conscious snacking and the ongoing exploration of new product formulations and distribution strategies by industry leaders are expected to outweigh these restraints, ensuring a positive trajectory for the plantain chip market in the coming years. The increasing adoption of offline sales channels in traditional markets also continues to be a crucial component of market strategy.

Plantain Chip Company Market Share

Here is the comprehensive, SEO-optimized report description for the Plantain Chip market, designed for immediate use without further modification.

Plantain Chip Market Dynamics & Structure

The global plantain chip market exhibits a moderate concentration, with leading players like Grace Foods, GOYA, Sankofa Snacks, Soldanza, and Unibán holding significant market shares. Technological innovation is primarily driven by advancements in processing and packaging to enhance shelf-life and introduce novel flavors, catering to evolving consumer preferences. Regulatory frameworks, particularly concerning food safety standards and labeling requirements across different geographies, play a crucial role in market entry and operations. Competitive product substitutes, such as potato chips and other root vegetable snacks, present a constant challenge, necessitating differentiation through unique product offerings and marketing strategies. End-user demographics are increasingly diverse, with a growing appeal among health-conscious consumers seeking gluten-free and natural snack options, as well as a strong presence in ethnic food markets. Mergers and acquisitions (M&A) trends are present, albeit not at a highly accelerated pace, with smaller players being acquired by larger entities to expand product portfolios and geographical reach. For instance, the acquisition of a regional snack producer by a national player can increase market share by 5-10 million units in the parent market. Innovation barriers include the high cost of specialized processing equipment and the challenges in sourcing consistent quality plantains year-round.

- Market Concentration: Moderate, with key players like Grace Foods, GOYA, Sankofa Snacks, Soldanza, and Unibán dominating.

- Technological Drivers: Innovations in processing, packaging, and flavor development.

- Regulatory Frameworks: Stringent food safety and labeling standards impacting market access.

- Competitive Substitutes: Potato chips, other root vegetable snacks.

- End-User Demographics: Health-conscious individuals, ethnic food consumers.

- M&A Trends: Gradual consolidation, with strategic acquisitions to expand reach.

- Innovation Barriers: Equipment costs, raw material sourcing consistency.

Plantain Chip Growth Trends & Insights

The global plantain chip market is poised for robust growth, driven by a confluence of factors that underscore its expanding appeal and market penetration. Over the historical period of 2019–2024, the market witnessed a steady upward trajectory, fueled by increasing consumer awareness of plantains as a versatile and nutritious ingredient. This upward trend is projected to accelerate significantly through the forecast period of 2025–2033, with a compound annual growth rate (CAGR) estimated at approximately 7.5%. The base year of 2025 serves as a pivotal point, with the market size projected to reach an estimated $7,800 million units. This evolution is characterized by a discernible shift in consumer behavior, moving beyond traditional ethnic food aisles towards mainstream grocery offerings. Health and wellness trends are playing a pivotal role, with plantain chips gaining traction as a gluten-free, naturally sweet, and often perceived as a healthier alternative to conventional fried snacks. This perception is further amplified by the growing demand for minimally processed and natural food products. Technological disruptions, while not entirely revolutionizing the production process, are contributing to enhanced product quality, extended shelf life through advanced packaging techniques, and the introduction of a wider array of flavors and textures, from classic unsweetened varieties to innovative sweet and spicy blends. The adoption rates of plantain chips are increasing across diverse demographics, as consumers become more adventurous in their snack choices and seek out globally inspired flavors. Market penetration is deepening, particularly in developed economies where the appeal of exotic and wholesome snack options is on the rise. The increasing availability of plantain chips through both online and offline sales channels further bolsters their accessibility and encourages trial among new consumer segments. The market size is expected to expand from an estimated $7,200 million units in 2024 to reach $12,500 million units by 2033. Consumer preference for snacking occasions beyond traditional mealtimes also contributes to the sustained growth of the plantain chip market.

Dominant Regions, Countries, or Segments in Plantain Chip

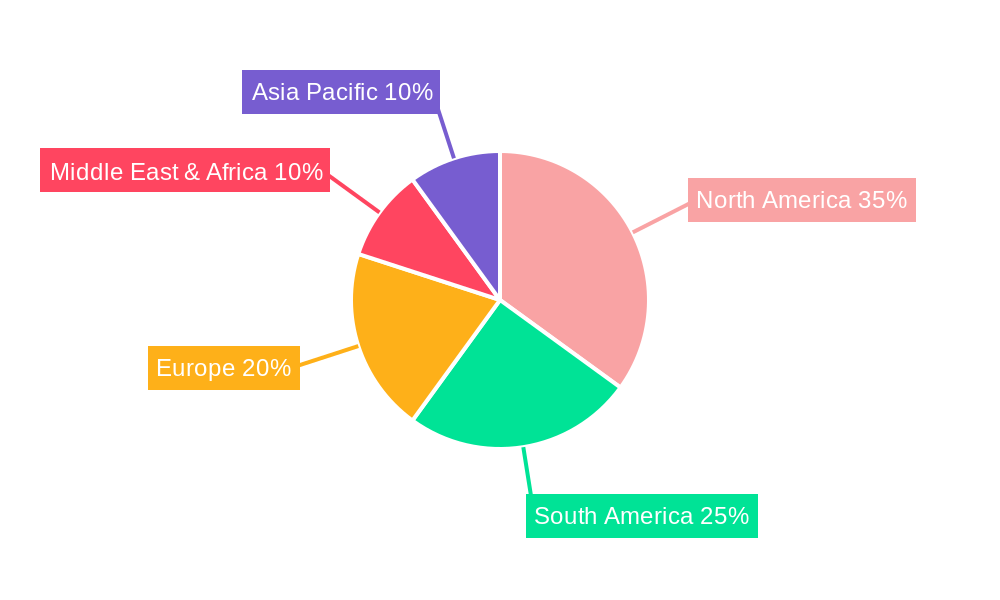

The global plantain chip market's growth is significantly influenced by a complex interplay of regional economic factors, infrastructural development, and evolving consumer preferences. Currently, North America stands out as a dominant region, propelled by a strong and growing Hispanic population alongside an increasing mainstream adoption of plantain chips as a healthy and versatile snack alternative. The United States, as the largest market within North America, accounts for an estimated 35% of the global plantain chip consumption, driven by the presence of major players like GOYA and Prime Planet, who have established extensive distribution networks. Economic policies supporting small businesses and agricultural imports further bolster the market in this region. Latin America, particularly countries like Colombia and Ecuador, are not only major producers of plantains but also significant consumers, contributing approximately 25% to the global market. The inherent cultural familiarity with plantain-based products in this region ensures consistent demand.

Within the application segments, Offline Sale currently holds a dominant position, representing an estimated 70% of the market share. This is attributed to the widespread availability of plantain chips in traditional grocery stores, convenience stores, supermarkets, and specialty ethnic food markets across the globe. Established distribution channels and the impulse purchase nature of snack products favor the offline retail environment. However, the Online Sale segment is experiencing rapid growth, projected to expand at a CAGR of 12% over the forecast period, driven by the convenience of e-commerce platforms and the increasing reach of online grocery delivery services.

Considering the product types, Unsweetened plantain chips represent the larger segment, accounting for approximately 60% of the market. This is due to their versatility as a savory snack and their appeal to consumers seeking to control their sugar intake. However, the Sweetened segment is gaining significant traction, with a projected CAGR of 9%, as manufacturers introduce innovative sweet and spiced varieties that cater to evolving taste preferences. Companies like Sankofa Snacks and CHIKA'S are actively innovating in this space, offering products with natural sweeteners and appealing flavor profiles. The growth in sweetened plantain chips is also linked to their use in desserts and as ingredients in culinary applications.

- Dominant Region: North America (especially the United States)

- Key Drivers: Large Hispanic population, increasing mainstream appeal, strong distribution networks, supportive economic policies.

- Market Share: Approximately 35% of global consumption.

- Dominant Application Segment: Offline Sale

- Market Share: Approximately 70% of the market.

- Growth Potential: Mature but stable, supported by traditional retail.

- Emerging Trend: Rapid growth in Online Sale segment (CAGR of 12%).

- Dominant Product Type: Unsweetened

- Market Share: Approximately 60% of the market.

- Appeal: Versatile savory snack, health-conscious consumers.

- Growing Product Type: Sweetened

- Projected CAGR: 9%

- Innovations: Sweet and spiced varieties, natural sweeteners, culinary applications.

Plantain Chip Product Landscape

The plantain chip product landscape is characterized by a growing emphasis on innovation and diversification to meet evolving consumer demands. Beyond the traditional, naturally flavored unsweetened varieties, manufacturers are introducing a wide array of novel products. These include plantain chips infused with diverse seasonings such as chili lime, garlic herb, and truffle oil, catering to sophisticated palates. Sweetened variants, incorporating natural sweeteners like honey or maple syrup and spices like cinnamon or nutmeg, are also gaining popularity, positioning plantain chips as a dessert-adjacent snack. Innovations in processing, such as air frying and baked methods, are being explored to offer healthier alternatives to traditionally fried chips, appealing to health-conscious consumers. Companies like TropicMax and Sunmo are at the forefront of introducing unique flavor profiles and healthier preparation methods, enhancing the perceived value and expanding the consumption occasions for plantain chips.

Key Drivers, Barriers & Challenges in Plantain Chip

The global plantain chip market is propelled by several key drivers, primarily the increasing consumer preference for healthier snack alternatives. Plantains are naturally gluten-free and offer a good source of potassium and fiber, aligning with growing health and wellness trends. The rising popularity of ethnic cuisines and global flavors also contributes to the demand for plantain chips as consumers seek out authentic and unique snack experiences. Furthermore, advancements in processing technologies that enhance shelf life and flavor profiles are making plantain chips more accessible and appealing to a wider audience.

However, the market faces significant barriers and challenges. The supply chain for plantains can be susceptible to seasonal fluctuations and climate-related disruptions, impacting raw material availability and cost stability. Competition from established snack categories like potato chips and other root vegetable snacks is intense, requiring significant marketing efforts for differentiation. Regulatory hurdles related to food safety, labeling, and import/export standards across different countries can also pose challenges for market entry and expansion. For instance, unpredictable weather patterns impacting yields could lead to a 10-15% increase in raw material costs, impacting profit margins.

- Key Drivers:

- Growing demand for healthy, gluten-free snacks.

- Increasing consumer interest in global flavors and ethnic foods.

- Technological advancements in processing and packaging.

- Key Barriers & Challenges:

- Vulnerability of plantain supply chain to weather and seasonality.

- Intense competition from established snack categories.

- Navigating diverse international food safety and labeling regulations.

- Potential for 10-15% increase in raw material costs due to supply disruptions.

Emerging Opportunities in Plantain Chip

Emerging opportunities in the plantain chip market lie in the development of value-added products and the penetration of untapped markets. There is a significant opportunity in creating plantain chips with functional ingredients, such as added vitamins, minerals, or probiotics, to cater to the burgeoning health and wellness segment. Innovations in sustainable packaging solutions also present an opportunity to appeal to environmentally conscious consumers. Furthermore, expanding into emerging economies in Asia and Africa, where plantains are a staple, offers substantial untapped market potential. Strategic partnerships with food service providers and airlines can also broaden distribution and consumer reach.

Growth Accelerators in the Plantain Chip Industry

Several catalysts are accelerating growth in the plantain chip industry. Technological breakthroughs in dehydration and baking techniques are enabling the production of lower-fat, crispier plantain chips, appealing to health-conscious consumers. Strategic partnerships between plantain chip manufacturers and ingredient suppliers are ensuring a more stable and consistent supply of high-quality raw materials. Furthermore, market expansion strategies, including targeted marketing campaigns highlighting the health benefits and unique taste profiles of plantain chips, are driving consumer adoption. The increasing focus on plant-based diets also indirectly fuels demand, as plantains are a versatile plant-based ingredient.

Key Players Shaping the Plantain Chip Market

- Grace Foods

- GOYA

- Sankofa Snacks

- Soldanza

- Unibán

- TropicMax

- Sunmo

- CHIKA'S

- Ara Food Corporation

- Pacifico Snacks

- Arca Continental

- Olu Olu

- Chifles Chips

- Prime Planet

Notable Milestones in Plantain Chip Sector

- 2021: Grace Foods launches a new line of seasoned plantain chips targeting premium markets.

- 2022: GOYA expands its snack portfolio with innovative sweet and savory plantain chip varieties.

- 2022: Sankofa Snacks secures funding to scale production and distribution of its organic plantain chips.

- 2023: Soldanza introduces a fully compostable packaging solution for its plantain chip range.

- 2023: Unibán invests in advanced processing technology to improve product quality and efficiency.

- 2024: CHIKA'S introduces limited-edition, globally inspired flavor combinations for its plantain chips.

- 2024: Prime Planet expands its distribution into European markets, increasing its global presence.

In-Depth Plantain Chip Market Outlook

The future outlook for the plantain chip market is exceptionally promising, driven by sustained consumer demand for healthier and globally inspired snack options. Growth accelerators, including ongoing product innovation, strategic market expansion into underserved regions, and the increasing adoption of plant-based diets, are poised to significantly boost market value. The convergence of technological advancements in processing and packaging with evolving consumer preferences for natural and convenient foods will continue to shape the industry. Strategic partnerships and targeted marketing will be crucial for players to capitalize on these opportunities and secure a dominant position in this dynamic and expanding market. The market is expected to see a significant increase in its valuation, reaching potentially $12,500 million units by 2033.

Plantain Chip Segmentation

-

1. Application

- 1.1. Online Sale

- 1.2. Offline Sale

-

2. Type

- 2.1. Sweetened

- 2.2. Unsweetened

Plantain Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Plantain Chip Regional Market Share

Geographic Coverage of Plantain Chip

Plantain Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Plantain Chip Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Online Sale

- 5.1.2. Offline Sale

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Sweetened

- 5.2.2. Unsweetened

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Plantain Chip Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Online Sale

- 6.1.2. Offline Sale

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Sweetened

- 6.2.2. Unsweetened

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Plantain Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Online Sale

- 7.1.2. Offline Sale

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Sweetened

- 7.2.2. Unsweetened

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Plantain Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Online Sale

- 8.1.2. Offline Sale

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Sweetened

- 8.2.2. Unsweetened

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Plantain Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Online Sale

- 9.1.2. Offline Sale

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Sweetened

- 9.2.2. Unsweetened

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Plantain Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Online Sale

- 10.1.2. Offline Sale

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Sweetened

- 10.2.2. Unsweetened

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Grace Foods

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 GOYA

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sankofa Snacks

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Soldanza

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Unibán

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 TropicMax

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Sunmo

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 CHIKA'S

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Ara Food Corporation

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Pacifico Snacks

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Arca Continental

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Olu Olu

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Chifles Chips

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Prime Planet

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Grace Foods

List of Figures

- Figure 1: Global Plantain Chip Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Plantain Chip Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Plantain Chip Revenue (million), by Application 2025 & 2033

- Figure 4: North America Plantain Chip Volume (K), by Application 2025 & 2033

- Figure 5: North America Plantain Chip Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Plantain Chip Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Plantain Chip Revenue (million), by Type 2025 & 2033

- Figure 8: North America Plantain Chip Volume (K), by Type 2025 & 2033

- Figure 9: North America Plantain Chip Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Plantain Chip Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Plantain Chip Revenue (million), by Country 2025 & 2033

- Figure 12: North America Plantain Chip Volume (K), by Country 2025 & 2033

- Figure 13: North America Plantain Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Plantain Chip Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Plantain Chip Revenue (million), by Application 2025 & 2033

- Figure 16: South America Plantain Chip Volume (K), by Application 2025 & 2033

- Figure 17: South America Plantain Chip Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Plantain Chip Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Plantain Chip Revenue (million), by Type 2025 & 2033

- Figure 20: South America Plantain Chip Volume (K), by Type 2025 & 2033

- Figure 21: South America Plantain Chip Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Plantain Chip Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Plantain Chip Revenue (million), by Country 2025 & 2033

- Figure 24: South America Plantain Chip Volume (K), by Country 2025 & 2033

- Figure 25: South America Plantain Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Plantain Chip Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Plantain Chip Revenue (million), by Application 2025 & 2033

- Figure 28: Europe Plantain Chip Volume (K), by Application 2025 & 2033

- Figure 29: Europe Plantain Chip Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Plantain Chip Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Plantain Chip Revenue (million), by Type 2025 & 2033

- Figure 32: Europe Plantain Chip Volume (K), by Type 2025 & 2033

- Figure 33: Europe Plantain Chip Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Plantain Chip Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Plantain Chip Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Plantain Chip Volume (K), by Country 2025 & 2033

- Figure 37: Europe Plantain Chip Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Plantain Chip Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Plantain Chip Revenue (million), by Application 2025 & 2033

- Figure 40: Middle East & Africa Plantain Chip Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Plantain Chip Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Plantain Chip Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Plantain Chip Revenue (million), by Type 2025 & 2033

- Figure 44: Middle East & Africa Plantain Chip Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Plantain Chip Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Plantain Chip Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Plantain Chip Revenue (million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Plantain Chip Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Plantain Chip Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Plantain Chip Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Plantain Chip Revenue (million), by Application 2025 & 2033

- Figure 52: Asia Pacific Plantain Chip Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Plantain Chip Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Plantain Chip Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Plantain Chip Revenue (million), by Type 2025 & 2033

- Figure 56: Asia Pacific Plantain Chip Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Plantain Chip Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Plantain Chip Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Plantain Chip Revenue (million), by Country 2025 & 2033

- Figure 60: Asia Pacific Plantain Chip Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Plantain Chip Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Plantain Chip Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Plantain Chip Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Plantain Chip Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Plantain Chip Revenue million Forecast, by Type 2020 & 2033

- Table 4: Global Plantain Chip Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Plantain Chip Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Plantain Chip Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Plantain Chip Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Plantain Chip Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Plantain Chip Revenue million Forecast, by Type 2020 & 2033

- Table 10: Global Plantain Chip Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Plantain Chip Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Plantain Chip Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United States Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Plantain Chip Revenue million Forecast, by Application 2020 & 2033

- Table 20: Global Plantain Chip Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Plantain Chip Revenue million Forecast, by Type 2020 & 2033

- Table 22: Global Plantain Chip Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Plantain Chip Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Plantain Chip Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Plantain Chip Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Plantain Chip Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Plantain Chip Revenue million Forecast, by Type 2020 & 2033

- Table 34: Global Plantain Chip Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Plantain Chip Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Plantain Chip Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Germany Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: France Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Italy Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Spain Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Russia Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Plantain Chip Revenue million Forecast, by Application 2020 & 2033

- Table 56: Global Plantain Chip Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Plantain Chip Revenue million Forecast, by Type 2020 & 2033

- Table 58: Global Plantain Chip Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Plantain Chip Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global Plantain Chip Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Israel Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: GCC Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Plantain Chip Revenue million Forecast, by Application 2020 & 2033

- Table 74: Global Plantain Chip Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Plantain Chip Revenue million Forecast, by Type 2020 & 2033

- Table 76: Global Plantain Chip Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Plantain Chip Revenue million Forecast, by Country 2020 & 2033

- Table 78: Global Plantain Chip Volume K Forecast, by Country 2020 & 2033

- Table 79: China Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 80: China Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: India Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Japan Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Plantain Chip Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Plantain Chip Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Plantain Chip?

The projected CAGR is approximately 4%.

2. Which companies are prominent players in the Plantain Chip?

Key companies in the market include Grace Foods, GOYA, Sankofa Snacks, Soldanza, Unibán, TropicMax, Sunmo, CHIKA'S, Ara Food Corporation, Pacifico Snacks, Arca Continental, Olu Olu, Chifles Chips, Prime Planet.

3. What are the main segments of the Plantain Chip?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 199 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Plantain Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Plantain Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Plantain Chip?

To stay informed about further developments, trends, and reports in the Plantain Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence