Key Insights

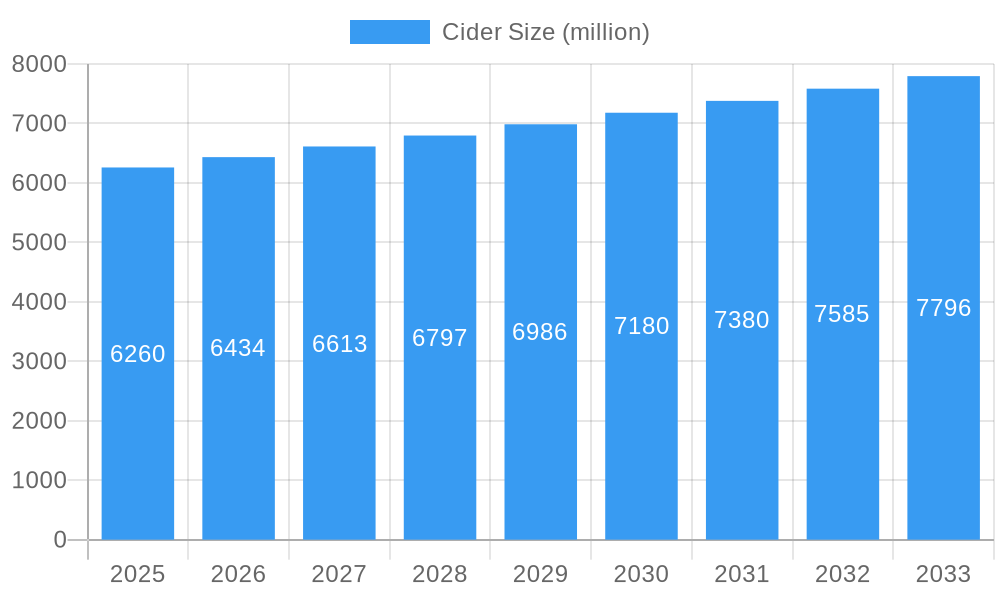

The global cider market is projected to experience significant growth, reaching a market size of $109.8 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 4.3% through 2033. This expansion is fueled by shifting consumer preferences towards lower-alcohol and craft beverages, alongside rising disposable incomes in emerging economies. Cider's appeal as a healthier alternative to traditional alcoholic drinks, coupled with innovative flavor profiles and reduced ABV options, is broadening its consumer base. The on-trade sector is expected to drive demand through social consumption.

Cider Market Size (In Billion)

Despite robust growth potential, the market faces challenges including regulatory complexities, fluctuating raw material costs, and competition from established alcoholic beverages, hard seltzers, and RTDs. The off-trade sector is anticipated to grow substantially due to the convenience of packaged products. Within product segmentation, ciders with 5.0%-6.0% ABV are expected to dominate, while those under 5.0% are projected to gain popularity due to the prevailing health and wellness trend.

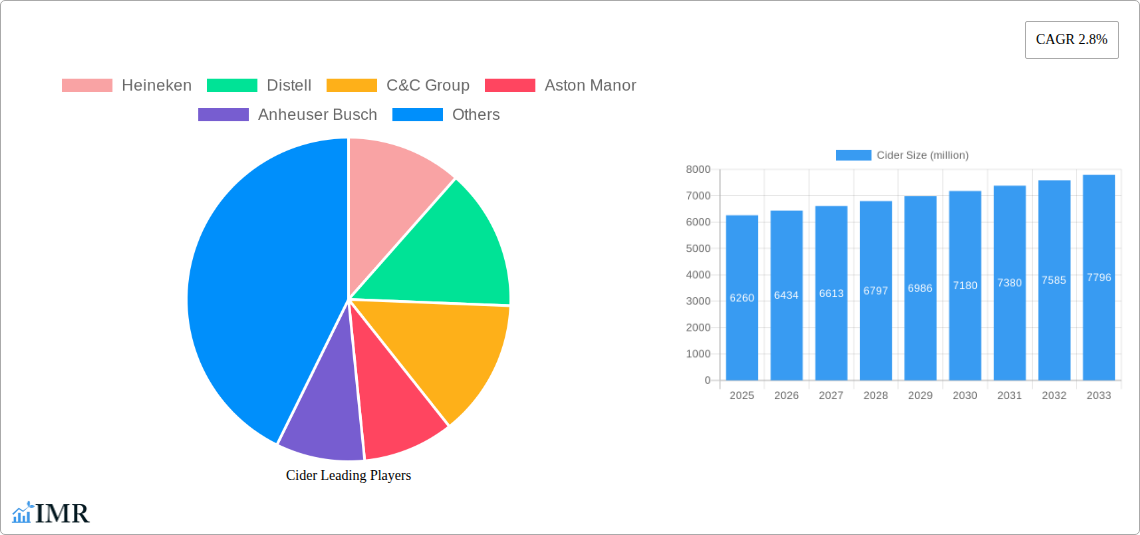

Cider Company Market Share

Comprehensive Cider Market Report: Global Insights, Trends, and Future Outlook (2019-2033)

This in-depth report provides a definitive analysis of the global cider market, offering unparalleled insights for industry stakeholders. Covering historical performance, current dynamics, and future projections, this study delves into every facet of the cider industry. With a granular approach, we dissect market segmentation, regional dominance, product innovation, and the strategic landscape of key players. This report is an essential resource for understanding the evolution and future trajectory of the cider market, driven by high-traffic keywords and robust data.

Cider Market Dynamics & Structure

The global cider market exhibits a moderately concentrated structure, with a few dominant players like Heineken, Distell, and C&C Group holding significant market share. Technological innovation, particularly in flavor development, packaging advancements, and production efficiency, is a key driver. Regulatory frameworks, including alcohol taxation and labeling requirements, influence market access and product formulation. The threat of competitive product substitutes, such as beer, wine, and ready-to-drink (RTD) beverages, remains a constant factor, necessitating continuous product differentiation. End-user demographics are shifting, with a growing appeal to younger adult consumers and an increasing demand for low-alcohol and craft cider options. Mergers and acquisitions (M&A) trends are evident, with Distell and C&C Group actively consolidating their market positions through strategic acquisitions.

- Market Concentration: Top 5 players hold approximately 65% of the global market share.

- Technological Innovation: Focus on novel fermentation techniques, natural flavor infusions, and sustainable packaging solutions.

- Regulatory Impact: Varying alcohol excise duties and marketing restrictions across key regions.

- Competitive Substitutes: Beer and RTDs are primary competitors, especially in convenience and price segments.

- Demographic Shifts: Increasing preference for artisanal, fruit-infused, and lower-ABV ciders among millennials and Gen Z.

- M&A Activity: Distell acquired Halewood International Holdings in 2023, strengthening its European presence. C&C Group has also pursued strategic acquisitions to expand its portfolio.

Cider Growth Trends & Insights

The global cider market is poised for robust expansion, driven by evolving consumer preferences and innovative product offerings. The market size is projected to witness significant growth, with increasing adoption rates for both traditional and hard cider varieties. Technological disruptions, such as advancements in yeast strains for unique flavor profiles and automated production processes, are streamlining operations and improving product quality. Consumer behavior shifts, including a move towards healthier beverage choices and a growing appreciation for craft and premium products, are actively shaping demand. The on-trade sector, encompassing bars, restaurants, and pubs, is experiencing a resurgence in cider popularity, while the off-trade segment, including supermarkets and liquor stores, continues to be a dominant sales channel due to convenience and a wider selection. The demand for low-alcohol cider (under 5.0%) is accelerating, catering to health-conscious consumers and those seeking lighter alcoholic options.

- Market Size Evolution: Projected to grow from an estimated \$28,500 million in 2025 to over \$38,000 million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 3.5% during the forecast period.

- Adoption Rates: Increasing penetration of cider as a mainstream beverage alternative to beer and wine across developed and emerging markets.

- Technological Disruptions: Innovations in fermentation, natural flavoring, and packaging technology enhancing product appeal and shelf-life.

- Consumer Behavior Shifts: Growing preference for authentic, artisanal, and fruit-forward cider profiles; rising demand for non-alcoholic and low-alcohol options.

- Market Penetration: Expected to reach 15% in key developed markets by 2033, up from 12% in 2024.

Dominant Regions, Countries, or Segments in Cider

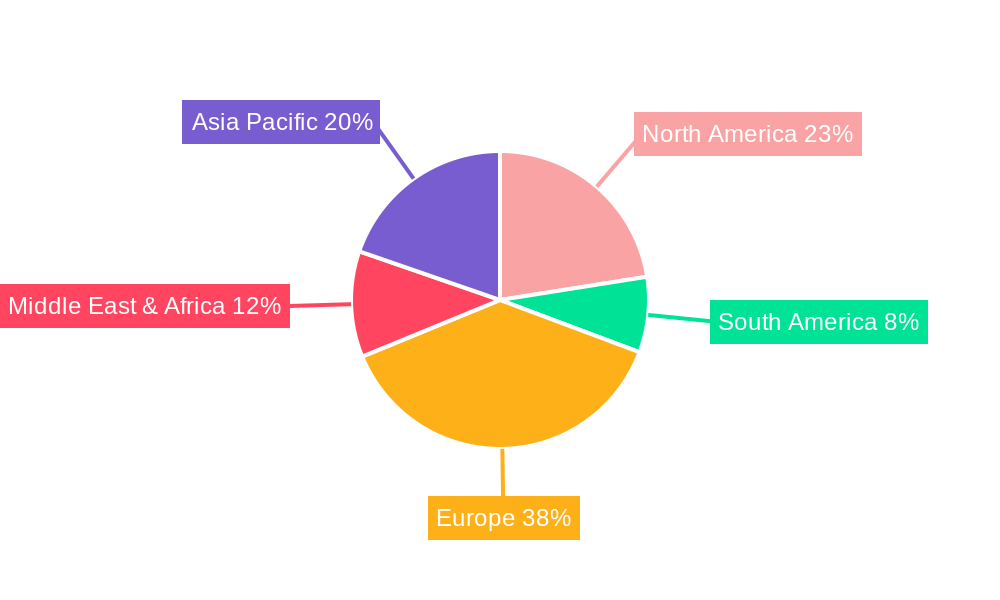

The United Kingdom consistently emerges as the leading region in the global cider market, driven by a deeply entrenched cultural appreciation and a mature consumer base. This dominance is fueled by a well-developed off-trade sector, offering a vast array of brands and styles, and a resilient on-trade sector that continues to champion traditional and craft ciders. Within the UK, the 5.0%-6.0% ABV (Alcohol by Volume) segment remains a significant volume driver, appealing to a broad consumer base seeking a balanced alcoholic content. However, the under 5.0% ABV segment is experiencing rapid growth, reflecting a broader health and wellness trend and an increasing demand for lighter alcoholic beverages.

- Dominant Region: Europe, with the United Kingdom as the standout country.

- Key Drivers in the UK:

- Strong Heritage and Cultural Acceptance: Cider is a traditional beverage with a long history of consumption.

- Well-Established Distribution Networks: Extensive reach across both on-trade and off-trade channels.

- Innovation in Craft and Premium Ciders: A vibrant craft cider scene catering to discerning consumers.

- Growing Demand for Low-Alcohol Options: Significant growth in the under 5.0% ABV segment.

- Market Share Dominance (UK): The UK accounts for approximately 30% of the global cider market volume.

- Growth Potential: Emerging markets in North America and Asia-Pacific are showing increasing interest, driven by Western lifestyle influences and the appeal of new beverage categories.

Cider Product Landscape

The cider product landscape is characterized by a dynamic evolution of flavor innovation, diverse applications, and enhanced performance metrics. Manufacturers are increasingly focusing on natural fruit infusions, botanical blends, and hybrid styles to capture consumer attention. Hard cider, particularly its premium and craft variants, continues to dominate the market, offering a refreshing alternative to traditional alcoholic beverages. Sparkling cider remains a popular choice for celebratory occasions, while still cider appeals to those seeking a more traditional taste. The growing demand for low-alcohol and non-alcoholic ciders is a significant product development, expanding accessibility and catering to diverse consumer needs. Key performance metrics include shelf-life extension through advanced pasteurization techniques and consistent flavor profiles across batches, ensuring brand loyalty.

Key Drivers, Barriers & Challenges in Cider

Key Drivers:

- Growing Consumer Preference for Natural and Lower-Alcohol Beverages: This aligns with health and wellness trends.

- Innovation in Flavors and Styles: Continuous introduction of new taste profiles and craft options keeps the market dynamic.

- Expanding Distribution Networks: Increased availability in both on-trade and off-trade channels globally.

- Influence of Craft Beverage Culture: The premiumization of beverages extends to cider, driving demand for artisanal products.

Key Barriers & Challenges:

- Intense Competition from Beer and RTD Beverages: These established categories pose a significant threat in terms of price and consumer habit.

- Supply Chain Volatility: Fluctuations in apple availability and quality, coupled with rising logistics costs, can impact production and profitability.

- Regulatory Hurdles: Navigating varying alcohol taxation and labeling laws across different countries presents complexity.

- Consumer Perception and Awareness: In some emerging markets, cider may still be perceived as a niche product, requiring educational marketing efforts. The cost of raw materials like apples is projected to increase by 8% year-on-year.

Emerging Opportunities in Cider

Emerging opportunities in the cider industry lie in the burgeoning non-alcoholic and low-alcohol cider segment, driven by increasing health consciousness and a desire for inclusive beverage options. Regional and artisanal cider producers have significant potential to capture market share by focusing on unique local apple varieties and traditional production methods. The expansion into emerging markets in Asia-Pacific and Latin America, where cider is gaining traction, presents untapped potential. Furthermore, innovative product formats, such as cider-based cocktails and ready-to-drink cider infusions, are poised to attract new consumer demographics and expand usage occasions.

Growth Accelerators in the Cider Industry

Catalysts driving long-term growth in the cider industry are multi-faceted. Technological breakthroughs in fermentation and flavor encapsulation are enabling the creation of novel and more appealing cider profiles. Strategic partnerships between established beverage companies and emerging craft cider brands are facilitating wider distribution and market penetration. Market expansion strategies targeting younger demographics through digital marketing and influencer collaborations are proving effective in building brand awareness and trial. The increasing demand for sustainable production practices and ethically sourced ingredients also presents an opportunity for growth and brand differentiation.

Key Players Shaping the Cider Market

- Heineken

- Distell

- C&C Group

- Aston Manor

- Anheuser Busch

- The Boston Beer Company

- Carlsberg

- Halewood International Holdings

Notable Milestones in Cider Sector

- 2019: C&C Group acquired Finch Drinks, expanding its RTD portfolio.

- 2020: Distell launched a significant marketing campaign for its Savanna cider brand in emerging markets.

- 2021: Anheuser-Busch InBev increased its investment in craft cider production in North America.

- 2022: Aston Manor invested in new bottling and packaging technology to enhance efficiency.

- 2023: Halewood International Holdings experienced significant growth in its artisanal cider offerings in the UK market.

- 2024: The Boston Beer Company continued to innovate with new flavor profiles in its Hard Seltzer line, which also impacts cider demand.

In-Depth Cider Market Outlook

The future of the cider market is characterized by sustained growth, propelled by evolving consumer preferences for healthier, more flavorful, and accessible alcoholic beverages. Innovation in low-alcohol and non-alcoholic options will continue to be a significant growth accelerator, appealing to a broader consumer base. The expansion into untapped geographic markets and the strategic consolidation of smaller brands by larger players will reshape the competitive landscape. Companies that prioritize sustainability, authentic branding, and a deep understanding of regional tastes are best positioned to capitalize on the expanding opportunities within this dynamic beverage sector. The overall market outlook remains exceptionally positive, with robust potential for both established and emerging players.

Cider Segmentation

-

1. Application

- 1.1. On Trade

- 1.2. Off Trade

-

2. Type

- 2.1. Under 5.0%

- 2.2. 5.0%-6.0%

- 2.3. Above 6.0%

Cider Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cider Regional Market Share

Geographic Coverage of Cider

Cider REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Cider Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. On Trade

- 5.1.2. Off Trade

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Under 5.0%

- 5.2.2. 5.0%-6.0%

- 5.2.3. Above 6.0%

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Cider Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. On Trade

- 6.1.2. Off Trade

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Under 5.0%

- 6.2.2. 5.0%-6.0%

- 6.2.3. Above 6.0%

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Cider Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. On Trade

- 7.1.2. Off Trade

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Under 5.0%

- 7.2.2. 5.0%-6.0%

- 7.2.3. Above 6.0%

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Cider Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. On Trade

- 8.1.2. Off Trade

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Under 5.0%

- 8.2.2. 5.0%-6.0%

- 8.2.3. Above 6.0%

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Cider Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. On Trade

- 9.1.2. Off Trade

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Under 5.0%

- 9.2.2. 5.0%-6.0%

- 9.2.3. Above 6.0%

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Cider Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. On Trade

- 10.1.2. Off Trade

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Under 5.0%

- 10.2.2. 5.0%-6.0%

- 10.2.3. Above 6.0%

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Heineken

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Distell

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 C&C Group

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Aston Manor

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Anheuser Busch

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 The Boston Beer Company

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Carlsberg

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Halewood International Holdings

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Heineken

List of Figures

- Figure 1: Global Cider Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Cider Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Cider Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Cider Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Cider Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Cider Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Cider Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Cider Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Cider Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Cider Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Cider Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Cider Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Cider Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Cider Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Cider Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Cider Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Cider Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Cider Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Cider Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Cider Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Cider Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Cider Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Cider Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Cider Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Cider Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Cider Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Cider Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Cider Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Cider Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Cider Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Cider Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Cider Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Cider Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Cider Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Cider Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Cider Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Cider Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Cider Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Cider Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Cider Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Cider Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Cider Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Cider Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Cider Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Cider Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Cider Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Cider Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Cider Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Cider Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Cider Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Cider Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Cider?

The projected CAGR is approximately 4.3%.

2. Which companies are prominent players in the Cider?

Key companies in the market include Heineken, Distell, C&C Group, Aston Manor, Anheuser Busch, The Boston Beer Company, Carlsberg, Halewood International Holdings.

3. What are the main segments of the Cider?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 109.8 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Cider," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Cider report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Cider?

To stay informed about further developments, trends, and reports in the Cider, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence