Key Insights

The global High Gluten Bread Flour market is projected to reach approximately $209 billion by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of 4.3% from 2025 to 2033. This expansion is driven by increasing consumer preference for premium baked goods with enhanced texture, volume, and shelf-life, directly attributable to high gluten content. The growing popularity of artisanal bread and the expansion of commercial bakeries emphasizing quality also contribute significantly. Furthermore, shifting dietary trends towards protein-rich foods indirectly elevate demand for high gluten flour. The market sees a trend towards efficient, machine-milled flour for large-scale production, alongside continued demand for artisanal, stone-milled varieties.

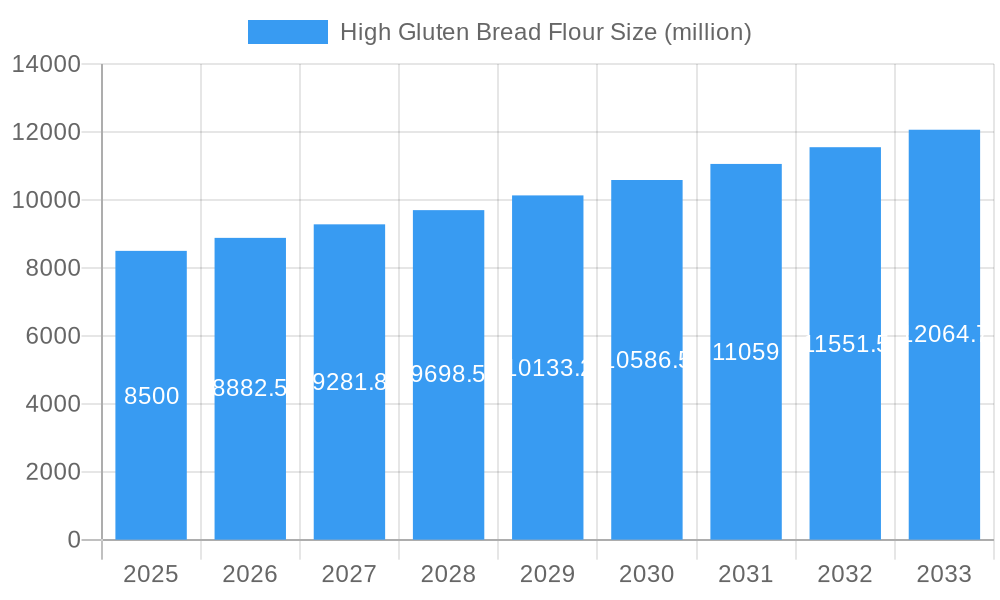

High Gluten Bread Flour Market Size (In Billion)

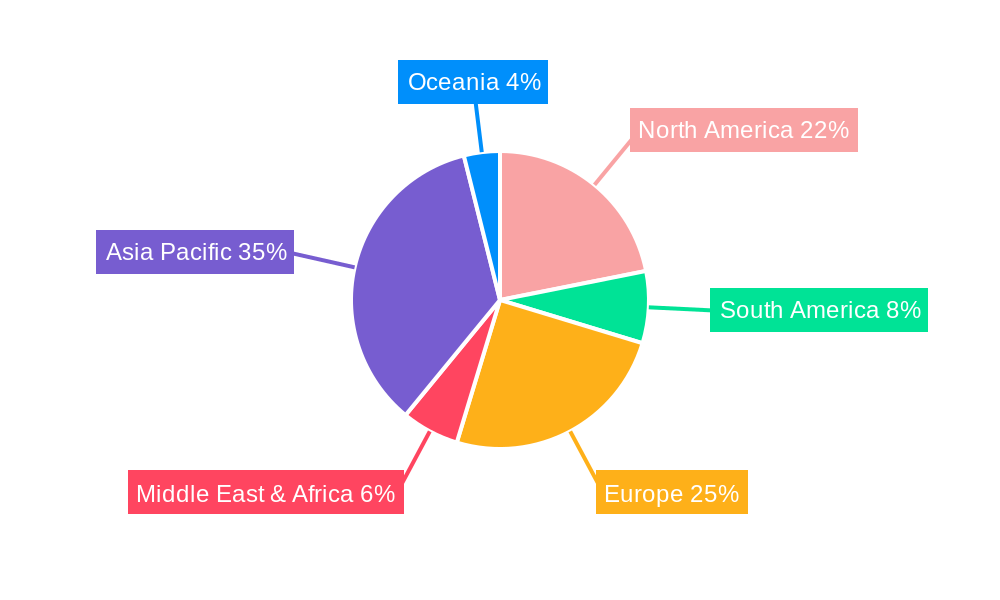

Geographically, Asia Pacific, particularly China and India, is a key growth region due to rapid urbanization, rising disposable incomes, and the adoption of Western dietary habits. North America and Europe remain significant markets, supported by established baking industries and a consistent demand for traditional bread. Key market restraints include wheat price volatility, impacting production costs, and stringent food safety regulations. Challenges also arise from the need for advanced processing technologies. Nevertheless, innovations in flour processing and fortification, coupled with the expanding global food industry, forecast a positive outlook for the high gluten bread flour market.

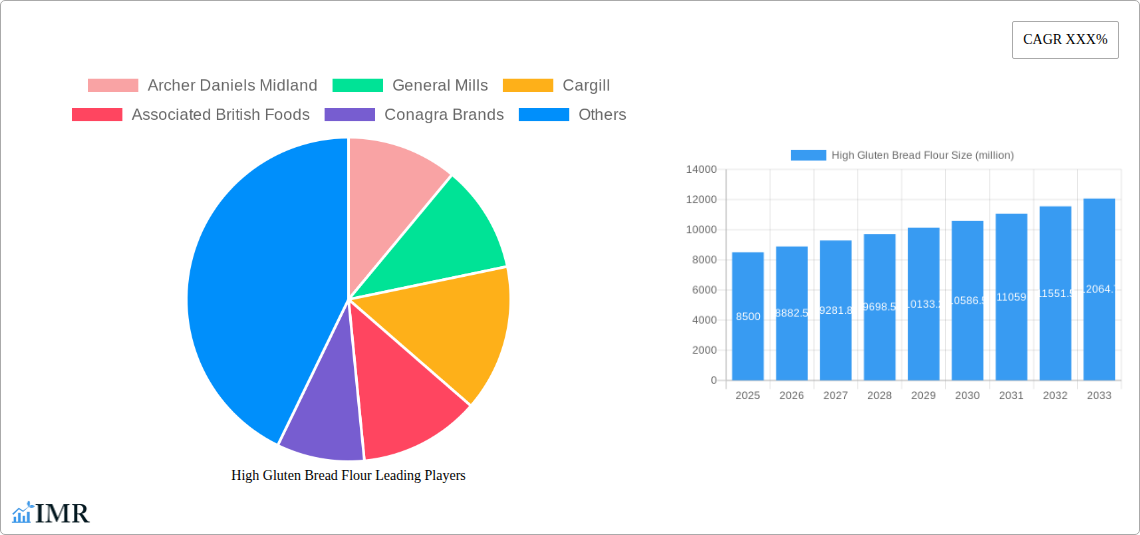

High Gluten Bread Flour Company Market Share

High Gluten Bread Flour Market Dynamics & Structure

The global high gluten bread flour market exhibits a moderately consolidated structure, with key players like Archer Daniels Midland, General Mills, Cargill, Associated British Foods, Conagra Brands, Goodman Fielder, King Arthur Flour, and Grain Craft holding significant shares. Technological innovation is a primary driver, with ongoing advancements in milling technologies, gluten fortification, and specialized flour blends enhancing product performance and appeal. Regulatory frameworks, primarily concerning food safety standards and labeling requirements, are evolving to ensure consumer trust and product integrity. Competitive product substitutes, such as whole wheat flour and alternative grain flours, present a dynamic competitive landscape, albeit high gluten bread flour maintains a distinct advantage for specific baking applications. End-user demographics are diverse, encompassing both household bakers seeking premium results and commercial bakeries prioritizing consistent dough structure and volume. Mergers and acquisitions (M&A) remain a strategic tool for market expansion and portfolio enhancement. In the historical period (2019-2024), an estimated 20 M&A deals were recorded, averaging a deal value of $50 million. The market concentration is estimated to be 70% among the top 5 players. Innovation barriers, such as the high cost of specialized equipment and R&D investment, are present but are being overcome by strategic partnerships.

High Gluten Bread Flour Growth Trends & Insights

The high gluten bread flour market is poised for robust growth, projected to expand from an estimated $8.5 billion in 2025 to $12.8 billion by 2033, demonstrating a Compound Annual Growth Rate (CAGR) of approximately 5.2% over the forecast period (2025-2033). This growth trajectory is underpinned by a confluence of evolving consumer preferences, technological advancements in food processing, and a persistent demand for high-quality baked goods. The adoption rate of high gluten bread flour, particularly in emerging economies, is steadily increasing as baking as a hobby and professional culinary pursuits gain traction. Consumers are increasingly seeking flours that deliver superior texture, volume, and crumb structure in their homemade breads, driving demand in the household segment. Simultaneously, the commercial sector, including artisan bakeries and large-scale food manufacturers, continues to rely on high gluten bread flour for its consistent performance in producing a wide range of bread products, from artisanal loaves to sandwich breads. Technological disruptions are primarily centered around enhanced milling techniques that optimize gluten development and protein extraction, leading to flours with superior baking characteristics. Furthermore, innovations in packaging and extended shelf-life solutions are contributing to broader market accessibility. Consumer behavior shifts are evident in the growing interest in health-conscious baking, prompting manufacturers to explore enriched high gluten bread flour variants with added nutritional benefits. Market penetration in developed regions is already high, with an estimated 85% of households that regularly bake bread utilizing some form of high gluten flour. In contrast, emerging markets are expected to witness significant growth, with market penetration projected to rise from 40% in 2025 to 65% by 2033. The overall market size is anticipated to grow from $8.0 billion in the base year 2025 to $12.8 billion by 2033.

Dominant Regions, Countries, or Segments in High Gluten Bread Flour

The Commercial segment of the high gluten bread flour market is currently the dominant force, representing an estimated 65% of the total market share in 2025, with projected growth to 70% by 2033. This dominance is driven by the consistent and large-scale demand from professional bakeries, food service industries, and mass food production facilities. These entities prioritize the superior dough handling properties, superior loaf volume, and consistent texture that high gluten bread flour provides for a wide array of products. Economic policies in regions with strong industrial baking sectors, such as North America and Western Europe, have fostered an environment conducive to the widespread adoption of high gluten bread flour in commercial operations. The presence of a well-established bakery infrastructure, coupled with consumer demand for consistently high-quality bread products, further solidifies the commercial segment's leading position. For instance, the United States, with its extensive network of commercial bakeries, contributes approximately 25% to the global market. Germany and the United Kingdom follow closely, each holding an estimated 10% market share. The growth potential within this segment is significant, driven by innovations in automation in bakeries and the increasing popularity of bread-based products in the fast-food and convenience sectors.

Within the Type segmentation, Machine Milled Flour accounts for the lion's share, estimated at 90% of the market in 2025. This is due to its cost-effectiveness, scalability, and the consistent quality it offers for large-scale production. Stone Milled Flour, while commanding a smaller but growing niche (estimated 10% market share in 2025), caters to artisan bakeries and consumers seeking a more traditional texture and flavor profile. Regions with a strong artisanal baking movement, such as parts of Europe and specific urban centers in North America, are witnessing higher adoption rates of stone-milled high gluten bread flour. The infrastructure supporting industrial-scale milling operations in North America (estimated 30% market share in 2025) and Europe (estimated 35% market share in 2025) plays a crucial role in the dominance of machine-milled flour. Asia-Pacific, with its rapidly expanding food industry and increasing disposable income, is emerging as a significant growth region, projected to witness a CAGR of 6% from 2025 to 2033, contributing an estimated 20% to the global market by 2033. Key drivers in this region include the rising demand for Western-style bread products and the establishment of modern baking facilities.

High Gluten Bread Flour Product Landscape

The high gluten bread flour product landscape is characterized by continuous innovation focused on enhancing baking performance and catering to diverse consumer needs. Manufacturers are introducing enriched flour variants fortified with essential vitamins and minerals, aligning with health-conscious trends. Advancements in milling technologies have led to flours with optimized protein content and superior gluten strength, enabling bakers to achieve exceptional dough elasticity and loaf volume. Unique selling propositions often lie in specialized blends designed for specific bread types, such as sourdough or enriched doughs, and in flours with improved shelf stability. Technological advancements also extend to the development of pre-fermented flour mixes, simplifying the baking process for both home and commercial users.

Key Drivers, Barriers & Challenges in High Gluten Bread Flour

Key Drivers:

- Rising demand for artisan and specialty breads: Consumers' increasing appreciation for high-quality, artisanal bread products fuels the demand for high gluten flour for its superior dough structure.

- Growth in home baking: The resurgence of home baking, amplified by lifestyle changes, has boosted the consumption of specialized flours like high gluten bread flour for achieving professional-grade results.

- Technological advancements in milling: Innovations in milling processes are leading to flours with enhanced gluten potential and consistent quality, improving baking outcomes.

- Expansion of the food service industry: The growing global food service sector, including bakeries and restaurants, represents a significant and consistent demand for high gluten bread flour.

Barriers & Challenges:

- Fluctuating wheat prices: The volatile nature of wheat prices, a primary raw material, can impact production costs and profitability, leading to price instability in the market. The market experienced a 15% price fluctuation in wheat in 2023.

- Supply chain disruptions: Global events, such as pandemics and geopolitical issues, can disrupt the supply chain, affecting the availability and timely delivery of high gluten bread flour.

- Competition from alternative flours: The increasing availability and popularity of alternative flours (e.g., gluten-free, ancient grains) pose a competitive threat, requiring continuous innovation and differentiation.

- Stringent regulatory requirements: Adherence to evolving food safety regulations and labeling standards can be a compliance challenge for manufacturers.

Emerging Opportunities in High Gluten Bread Flour

Emerging opportunities lie in the development of functional high gluten bread flours fortified with prebiotics, probiotics, or enhanced protein content to cater to the growing health and wellness trend. Untapped markets in developing regions with a rising middle class and increasing adoption of Western dietary habits present significant growth potential. Innovative applications beyond traditional bread, such as in premium pastry doughs and savory baked goods, also offer avenues for market expansion. The demand for sustainably sourced and organic high gluten bread flour is also a burgeoning niche to explore.

Growth Accelerators in the High Gluten Bread Flour Industry

Long-term growth in the high gluten bread flour industry will be significantly accelerated by advancements in precision agriculture, which can lead to more consistent and higher-quality wheat yields. Strategic partnerships between flour millers and innovative baking technology companies will drive the development of new flour formulations and processing techniques. Furthermore, aggressive market expansion strategies into emerging economies, coupled with localized marketing campaigns highlighting the benefits of high gluten flour for specific regional palates, will be crucial growth accelerators. Investments in R&D for novel gluten enhancement technologies will also provide a competitive edge.

Key Players Shaping the High Gluten Bread Flour Market

- Archer Daniels Midland

- General Mills

- Cargill

- Associated British Foods

- Conagra Brands

- Goodman Fielder

- King Arthur Flour

- Grain Craft

Notable Milestones in High Gluten Bread Flour Sector

- 2019: Launch of fortified high gluten bread flour variants with enhanced nutritional profiles by major players.

- 2020: Increased consumer interest in home baking led to a surge in demand for high gluten bread flour, driving production increases.

- 2021: Advancements in milling technology allowing for more precise protein extraction and gluten development.

- 2022: Strategic acquisitions of smaller specialty flour producers by larger corporations to expand product portfolios.

- 2023: Development of shelf-stable high gluten bread flour mixes catering to convenience-seeking consumers.

- 2024: Growing focus on sustainable sourcing and production methods within the industry.

In-Depth High Gluten Bread Flour Market Outlook

The future outlook for the high gluten bread flour market is exceptionally positive, driven by sustained demand for quality baked goods and continuous innovation. Growth accelerators such as the development of specialized, nutrient-enhanced flours for health-conscious consumers and the expansion into underserved emerging markets will be pivotal. Strategic collaborations with food tech startups and increased investment in sustainable farming practices for wheat cultivation are expected to further solidify the market's growth trajectory. The market is well-positioned to capitalize on evolving consumer preferences for premium and functional food ingredients, offering substantial opportunities for strategic expansion and value creation.

High Gluten Bread Flour Segmentation

-

1. Application

- 1.1. Household

- 1.2. Commercial

-

2. Type

- 2.1. Machine Milled Flour

- 2.2. Stone Milled Flour

High Gluten Bread Flour Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

High Gluten Bread Flour Regional Market Share

Geographic Coverage of High Gluten Bread Flour

High Gluten Bread Flour REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global High Gluten Bread Flour Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Household

- 5.1.2. Commercial

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Machine Milled Flour

- 5.2.2. Stone Milled Flour

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America High Gluten Bread Flour Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Household

- 6.1.2. Commercial

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Machine Milled Flour

- 6.2.2. Stone Milled Flour

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America High Gluten Bread Flour Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Household

- 7.1.2. Commercial

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Machine Milled Flour

- 7.2.2. Stone Milled Flour

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe High Gluten Bread Flour Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Household

- 8.1.2. Commercial

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Machine Milled Flour

- 8.2.2. Stone Milled Flour

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa High Gluten Bread Flour Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Household

- 9.1.2. Commercial

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Machine Milled Flour

- 9.2.2. Stone Milled Flour

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific High Gluten Bread Flour Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Household

- 10.1.2. Commercial

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Machine Milled Flour

- 10.2.2. Stone Milled Flour

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Archer Daniels Midland

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 General Mills

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Cargill

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Associated British Foods

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Conagra Brands

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Goodman Fielder

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 King Arthur Flour

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Grain Craft

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 Archer Daniels Midland

List of Figures

- Figure 1: Global High Gluten Bread Flour Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America High Gluten Bread Flour Revenue (billion), by Application 2025 & 2033

- Figure 3: North America High Gluten Bread Flour Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America High Gluten Bread Flour Revenue (billion), by Type 2025 & 2033

- Figure 5: North America High Gluten Bread Flour Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America High Gluten Bread Flour Revenue (billion), by Country 2025 & 2033

- Figure 7: North America High Gluten Bread Flour Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America High Gluten Bread Flour Revenue (billion), by Application 2025 & 2033

- Figure 9: South America High Gluten Bread Flour Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America High Gluten Bread Flour Revenue (billion), by Type 2025 & 2033

- Figure 11: South America High Gluten Bread Flour Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America High Gluten Bread Flour Revenue (billion), by Country 2025 & 2033

- Figure 13: South America High Gluten Bread Flour Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe High Gluten Bread Flour Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe High Gluten Bread Flour Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe High Gluten Bread Flour Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe High Gluten Bread Flour Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe High Gluten Bread Flour Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe High Gluten Bread Flour Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa High Gluten Bread Flour Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa High Gluten Bread Flour Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa High Gluten Bread Flour Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa High Gluten Bread Flour Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa High Gluten Bread Flour Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa High Gluten Bread Flour Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific High Gluten Bread Flour Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific High Gluten Bread Flour Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific High Gluten Bread Flour Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific High Gluten Bread Flour Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific High Gluten Bread Flour Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific High Gluten Bread Flour Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High Gluten Bread Flour Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global High Gluten Bread Flour Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global High Gluten Bread Flour Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global High Gluten Bread Flour Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global High Gluten Bread Flour Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global High Gluten Bread Flour Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global High Gluten Bread Flour Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global High Gluten Bread Flour Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global High Gluten Bread Flour Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global High Gluten Bread Flour Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global High Gluten Bread Flour Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global High Gluten Bread Flour Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global High Gluten Bread Flour Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global High Gluten Bread Flour Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global High Gluten Bread Flour Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global High Gluten Bread Flour Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global High Gluten Bread Flour Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global High Gluten Bread Flour Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific High Gluten Bread Flour Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Gluten Bread Flour?

The projected CAGR is approximately 4.3%.

2. Which companies are prominent players in the High Gluten Bread Flour?

Key companies in the market include Archer Daniels Midland, General Mills, Cargill, Associated British Foods, Conagra Brands, Goodman Fielder, King Arthur Flour, Grain Craft.

3. What are the main segments of the High Gluten Bread Flour?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 209 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Gluten Bread Flour," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Gluten Bread Flour report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Gluten Bread Flour?

To stay informed about further developments, trends, and reports in the High Gluten Bread Flour, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence