Key Insights

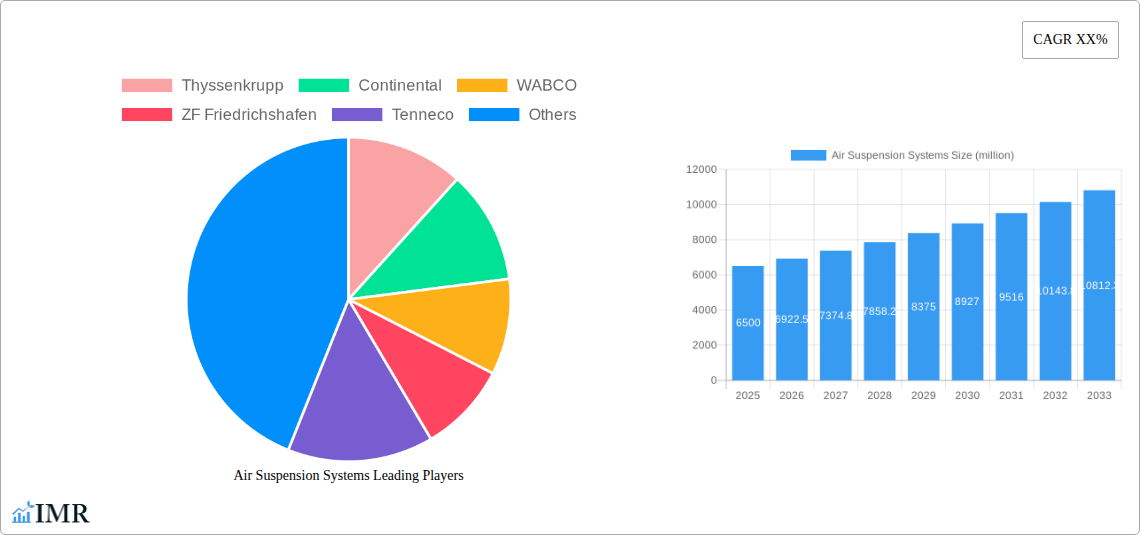

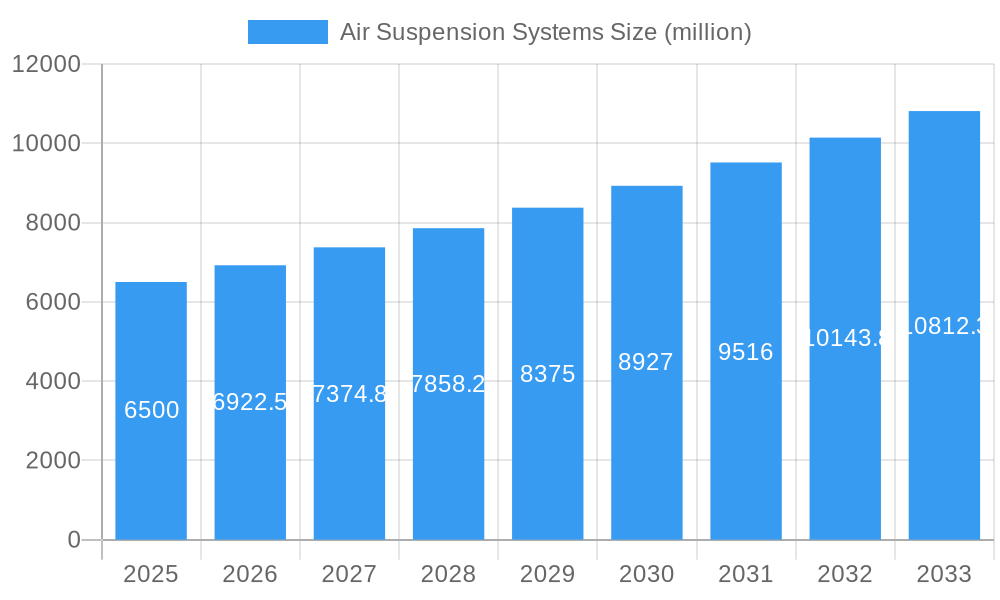

The global Air Suspension Systems market is poised for significant growth, estimated to reach approximately \$6,500 million by 2025, with a projected Compound Annual Growth Rate (CAGR) of around 6.5% through 2033. This expansion is driven by increasing demand for enhanced ride comfort, improved vehicle handling, and greater fuel efficiency across both passenger cars and commercial vehicles. The growing adoption of advanced driver-assistance systems (ADAS) and the trend towards autonomous vehicles further bolster the market, as air suspension systems play a crucial role in maintaining vehicle stability and optimizing sensor performance in these sophisticated applications.

Air Suspension Systems Market Size (In Billion)

Key market drivers include stringent emission regulations and the growing preference for premium vehicles that often feature air suspension as a standard or optional upgrade. Furthermore, the development of lighter and more durable materials, coupled with advancements in electronic control technologies, is making air suspension systems more accessible and reliable. However, the market faces restraints such as the relatively higher initial cost compared to traditional suspension systems and the need for specialized maintenance. Geographically, Asia Pacific, particularly China and India, is emerging as a pivotal growth region due to the burgeoning automotive industry and increasing disposable incomes, while North America and Europe continue to be significant markets driven by technological innovation and fleet modernization. The market segmentation by type reveals a strong inclination towards electronically controlled systems due to their superior performance and adaptability.

Air Suspension Systems Company Market Share

Air Suspension Systems Market Report: Dynamics, Growth, and Future Outlook (2019-2033)

This comprehensive report provides an in-depth analysis of the global air suspension systems market, covering its dynamics, growth trajectories, regional dominance, product innovations, key players, and future outlook. Leveraging advanced analytical tools and extensive industry data, this report is essential for stakeholders seeking to understand the evolving landscape of air suspension technology.

Study Period: 2019–2033 Base Year: 2025 Estimated Year: 2025 Forecast Period: 2025–2033 Historical Period: 2019–2024

Air Suspension Systems Market Dynamics & Structure

The global air suspension systems market exhibits a moderate concentration, with key players like Thyssenkrupp, Continental, WABCO, ZF Friedrichshafen, Tenneco, and KYB Corporation dominating the landscape. Technological innovation is a primary driver, fueled by the increasing demand for enhanced vehicle comfort, safety, and performance. Advancements in electronically controlled air suspension systems, offering superior ride quality and adaptive capabilities, are gaining significant traction. Regulatory frameworks, particularly those related to vehicle emissions and safety standards, indirectly influence the adoption of air suspension systems by mandating or incentivizing lighter and more efficient vehicle designs.

- Market Concentration: Moderate, with a few key global players holding significant market share.

- Technological Innovation Drivers: Demand for enhanced comfort, improved handling, vehicle height adjustment, and advanced driver-assistance systems (ADAS) integration.

- Regulatory Frameworks: Stringent safety regulations and emissions standards are encouraging the adoption of lightweight and efficient suspension solutions.

- Competitive Product Substitutes: Traditional hydraulic and passive suspension systems remain competitive, particularly in cost-sensitive segments. However, the superior performance and feature set of air suspension systems are gradually eroding their market share.

- End-User Demographics: Growing preference for premium vehicle features among affluent consumers and the increasing demand for specialized vehicles in commercial applications.

- M&A Trends: Strategic acquisitions and collaborations are observed as companies seek to expand their product portfolios, technological capabilities, and geographical reach. For example, recent M&A activities in the automotive components sector have seen integration of air suspension expertise to offer more complete solutions.

Air Suspension Systems Growth Trends & Insights

The air suspension systems market is poised for robust growth, driven by a confluence of factors including evolving consumer preferences for premium vehicle features, increasing production of luxury and performance vehicles, and the growing adoption of advanced suspension technologies in commercial vehicles. The market size is projected to witness a significant expansion over the forecast period. The CAGR is estimated to be approximately 7.5% from 2025 to 2033. Increasing penetration of electronically controlled air suspension systems, offering superior ride comfort, dynamic handling, and customizable ride height, is a key growth determinant.

Consumer behavior shifts towards a greater emphasis on vehicle comfort and a desire for a more refined driving experience are directly translating into higher demand for air suspension solutions in passenger cars. In the commercial vehicle segment, the benefits of air suspension, such as reduced cargo damage, improved fuel efficiency through aerodynamic optimization, and enhanced driver comfort for long-haul operations, are driving adoption. Technological disruptions, including advancements in sensor technology, actuator precision, and sophisticated control algorithms, are further enhancing the performance and cost-effectiveness of air suspension systems.

- Market Size Evolution: The global air suspension systems market is expected to grow from an estimated $8,500 million in 2025 to over $15,000 million by 2033.

- Adoption Rates: Increasing adoption in both OEM and aftermarket segments, with a particular surge in premium passenger car models and heavy-duty commercial vehicles.

- Technological Disruptions: Integration with AI and machine learning for predictive suspension adjustments, leading to enhanced performance and reduced wear.

- Consumer Behavior Shifts: Growing demand for personalized driving experiences, comfort-oriented features, and advanced vehicle dynamics.

Dominant Regions, Countries, or Segments in Air Suspension Systems

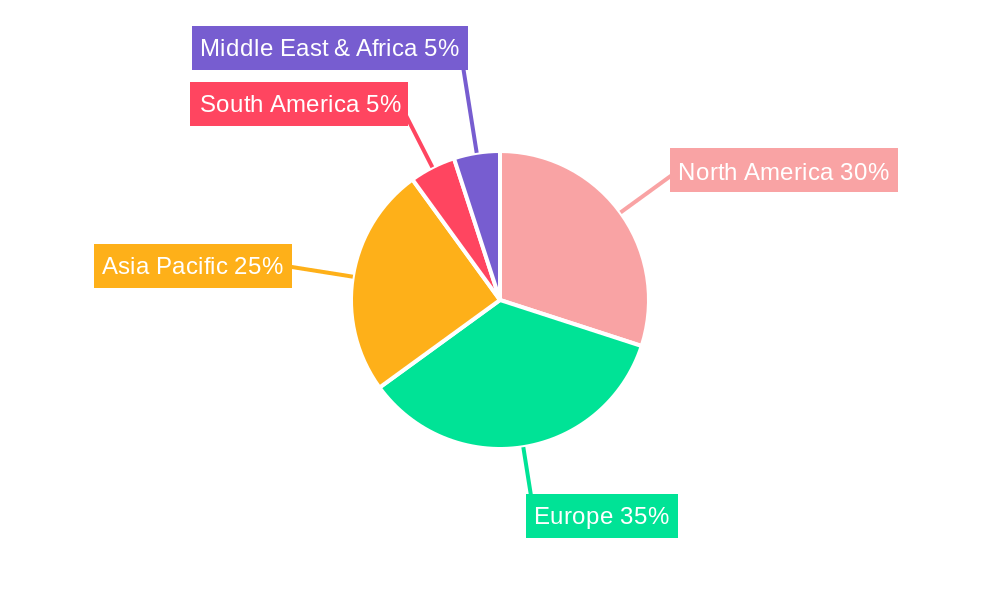

North America and Europe currently lead the air suspension systems market, primarily driven by the high concentration of premium passenger car manufacturers and a strong demand for advanced automotive technologies. The United States, in particular, stands out as a dominant country due to its large automotive market, high disposable incomes, and a robust aftermarket segment for vehicle upgrades. The increasing adoption of air suspension in electric vehicles (EVs) in these regions also contributes significantly to market growth.

In the commercial vehicle segment, Europe's stringent regulations on fleet efficiency and driver comfort, coupled with the significant presence of heavy-duty truck and bus manufacturers, position it as a key growth area. Asia Pacific, led by China, is emerging as a rapidly growing market, fueled by the burgeoning automotive industry, increasing disposable incomes, and a rising demand for technologically advanced vehicles.

- Dominant Application Segment: Passenger Cars, accounting for an estimated 65% of the global market share in 2025. This is driven by the premium segment's demand for comfort and performance.

- Dominant Type Segment: Electronically Controlled air suspension systems are gaining prominence, projected to capture over 70% of the market by 2033, due to their superior functionality and adaptive capabilities.

- Key Drivers in North America & Europe:

- High per capita income and consumer spending on premium vehicles.

- Presence of leading automotive OEMs and Tier-1 suppliers.

- Stringent safety and comfort regulations pushing for advanced suspension.

- Strong aftermarket demand for performance and comfort upgrades.

- Growth Potential in Asia Pacific:

- Rapidly expanding automotive production and sales.

- Increasing consumer preference for comfort and luxury features.

- Growing adoption of commercial vehicles with enhanced payload capacity and driver comfort requirements.

- Government initiatives supporting automotive technological advancements.

Air Suspension Systems Product Landscape

The air suspension systems market is characterized by continuous product innovation focused on enhancing ride quality, safety, and energy efficiency. Manufacturers are developing lighter, more compact, and more durable air springs, compressors, and control units. Key advancements include the integration of smart sensors for real-time road condition analysis, enabling predictive suspension adjustments. Electronically controlled systems are increasingly offering features like automatic leveling, load compensation, and adaptive damping.

- Product Innovations: Development of advanced air springs with improved durability and reduced weight. Smart control modules with AI capabilities for predictive road surface adaptation.

- Applications: From enhancing the driving experience in luxury SUVs and sedans to providing crucial load support and ride comfort in heavy-duty trucks and buses.

- Performance Metrics: Focus on improving ride comfort index, reducing NVH (Noise, Vibration, and Harshness) levels, and optimizing vehicle handling dynamics.

Key Drivers, Barriers & Challenges in Air Suspension Systems

Key Drivers:

- Growing demand for vehicle comfort and ride quality: Consumers increasingly expect a premium driving experience, making air suspension a desirable feature.

- Technological advancements: Innovations in electronic control systems and sensor technology enhance performance and reliability.

- Increased adoption in commercial vehicles: Benefits like reduced cargo damage and driver fatigue drive demand in trucking and logistics.

- Growth in luxury and performance vehicle segments: These segments are early adopters of advanced suspension technologies.

Barriers & Challenges:

- Higher initial cost compared to conventional systems: This can be a restraint in cost-sensitive markets and entry-level vehicle segments.

- Complexity of installation and maintenance: Requires specialized knowledge and equipment, potentially increasing aftermarket service costs.

- Weight penalty: Although efforts are being made to reduce weight, air suspension systems can still be heavier than traditional systems, impacting fuel efficiency.

- Potential for component failure: While reliability is improving, components like air springs and compressors can be susceptible to wear and tear, leading to repair costs.

Emerging Opportunities in Air Suspension Systems

The burgeoning electric vehicle (EV) market presents a significant opportunity for air suspension systems. EVs, with their inherently quieter operation, amplify the importance of ride comfort, making air suspension an attractive proposition for EV manufacturers. Furthermore, the development of active and semi-active air suspension systems that can dynamically adjust to driving conditions and driver inputs opens new avenues for enhanced vehicle performance and safety. The aftermarket segment for retrofitting air suspension systems in older or commercial vehicles also represents an untapped market.

- Integration with Electric Vehicles (EVs): Offering enhanced comfort and contributing to battery range optimization through aerodynamic adjustments.

- Smart and Connected Suspension: Development of systems that communicate with navigation and V2X (Vehicle-to-Everything) technology for proactive ride adjustments.

- Aftermarket Customization: Growing demand for performance and comfort upgrades in the aftermarket sector.

Growth Accelerators in the Air Suspension Systems Industry

The sustained growth of the automotive industry, particularly in emerging economies, coupled with the increasing consumer appetite for premium vehicle features, acts as a major growth accelerator. Strategic collaborations between automotive OEMs and air suspension system manufacturers are crucial for integrating these systems early in vehicle development, leading to optimized performance and cost efficiencies. The continuous push for enhanced safety and fuel efficiency standards by regulatory bodies will also drive the adoption of advanced and lightweight air suspension solutions. The development of more cost-effective manufacturing processes and materials will further democratize access to air suspension technology.

Key Players Shaping the Air Suspension Systems Market

- Thyssenkrupp

- Continental AG

- WABCO

- ZF Friedrichshafen AG

- Tenneco Inc.

- Magneti Marelli S.p.A.

- KYB Corporation

- Hendrickson International

- Accuair Suspension

- Hitachi Automotive Systems, Ltd.

- Haldex AB

- Dunlop Systems and Components Ltd.

- Mando Corporation

- BWI Group

- Firestone Industrial Products Company, LLC

Notable Milestones in Air Suspension Systems Sector

- 2019: Increased focus on lightweight materials and advanced control algorithms for enhanced efficiency and performance.

- 2020: Growing integration of air suspension systems in electric vehicle prototypes, highlighting their compatibility and benefits for EVs.

- 2021: Advancements in sensor technology allowing for more precise and real-time adjustments to suspension parameters.

- 2022: Strategic partnerships formed between major automotive OEMs and air suspension suppliers to co-develop next-generation suspension solutions.

- 2023: Introduction of advanced diagnostic and predictive maintenance features for air suspension systems, reducing downtime and service costs.

- 2024: Significant investments in R&D for fully active and intelligent air suspension systems capable of adapting to complex driving scenarios.

In-Depth Air Suspension Systems Market Outlook

The air suspension systems market is projected for substantial growth, driven by ongoing technological innovations, increasing integration in electric vehicles, and a persistent consumer demand for enhanced comfort and performance. Strategic initiatives by key players, including product diversification and market expansion, coupled with favorable regulatory landscapes promoting advanced vehicle technologies, will further accelerate this growth. The market is anticipated to witness a dynamic evolution, with a strong emphasis on intelligent and sustainable suspension solutions. Stakeholders can expect significant opportunities in both the OEM and aftermarket segments, particularly in regions with a burgeoning automotive sector and a high propensity for premium vehicle features.

Air Suspension Systems Segmentation

-

1. Application

- 1.1. Passenger Cars

- 1.2. Commercial Vehicles

-

2. Types

- 2.1. Electronically Controlled

- 2.2. Non-Electronically Controlled

Air Suspension Systems Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Air Suspension Systems Regional Market Share

Geographic Coverage of Air Suspension Systems

Air Suspension Systems REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 0.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Cars

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Electronically Controlled

- 5.2.2. Non-Electronically Controlled

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Air Suspension Systems Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Cars

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Electronically Controlled

- 6.2.2. Non-Electronically Controlled

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Air Suspension Systems Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Cars

- 7.1.2. Commercial Vehicles

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Electronically Controlled

- 7.2.2. Non-Electronically Controlled

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Air Suspension Systems Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Cars

- 8.1.2. Commercial Vehicles

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Electronically Controlled

- 8.2.2. Non-Electronically Controlled

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Air Suspension Systems Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Cars

- 9.1.2. Commercial Vehicles

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Electronically Controlled

- 9.2.2. Non-Electronically Controlled

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Air Suspension Systems Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Cars

- 10.1.2. Commercial Vehicles

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Electronically Controlled

- 10.2.2. Non-Electronically Controlled

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Air Suspension Systems Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Passenger Cars

- 11.1.2. Commercial Vehicles

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Electronically Controlled

- 11.2.2. Non-Electronically Controlled

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Thyssenkrupp

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Continental

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 WABCO

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 ZF Friedrichshafen

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Tenneco

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Magneti Marelli

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 KYB Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Hendrickson International

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Accuair Suspension

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Hitachi

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Haldex

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Dunlop Systems and Components

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Mando Corporation

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 BWI Group

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Firestone Industrial Products

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Thyssenkrupp

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Air Suspension Systems Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Air Suspension Systems Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Air Suspension Systems Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Air Suspension Systems Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Air Suspension Systems Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Air Suspension Systems Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Air Suspension Systems Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Air Suspension Systems Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Air Suspension Systems Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Air Suspension Systems Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Air Suspension Systems Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Air Suspension Systems Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Air Suspension Systems Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Air Suspension Systems Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Air Suspension Systems Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Air Suspension Systems Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Air Suspension Systems Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Air Suspension Systems Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Air Suspension Systems Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Air Suspension Systems Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Air Suspension Systems Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Air Suspension Systems Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Air Suspension Systems Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Air Suspension Systems Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Air Suspension Systems Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Air Suspension Systems Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Air Suspension Systems Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Air Suspension Systems Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Air Suspension Systems Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Air Suspension Systems Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Air Suspension Systems Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Air Suspension Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Air Suspension Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Air Suspension Systems Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Air Suspension Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Air Suspension Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Air Suspension Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Air Suspension Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Air Suspension Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Air Suspension Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Air Suspension Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Air Suspension Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Air Suspension Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Air Suspension Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Air Suspension Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Air Suspension Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Air Suspension Systems Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Air Suspension Systems Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Air Suspension Systems Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Air Suspension Systems Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Air Suspension Systems?

The projected CAGR is approximately 0.9%.

2. Which companies are prominent players in the Air Suspension Systems?

Key companies in the market include Thyssenkrupp, Continental, WABCO, ZF Friedrichshafen, Tenneco, Magneti Marelli, KYB Corporation, Hendrickson International, Accuair Suspension, Hitachi, Haldex, Dunlop Systems and Components, Mando Corporation, BWI Group, Firestone Industrial Products.

3. What are the main segments of the Air Suspension Systems?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Air Suspension Systems," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Air Suspension Systems report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Air Suspension Systems?

To stay informed about further developments, trends, and reports in the Air Suspension Systems, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence