Key Insights

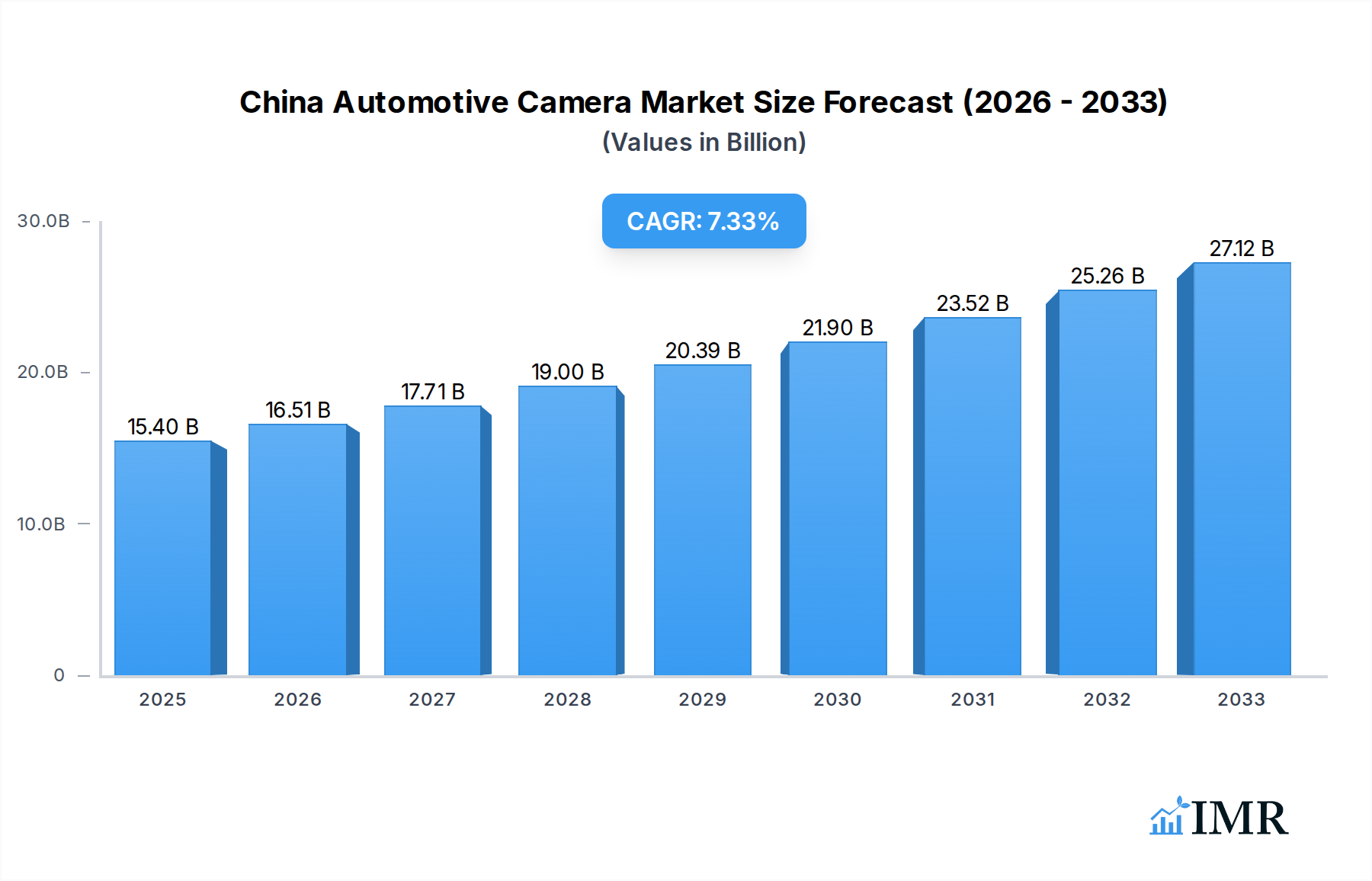

The China Automotive Camera Market is poised for significant expansion, projected to reach $15.4 billion in 2025, driven by a robust Compound Annual Growth Rate (CAGR) of 7.21%. This impressive growth trajectory is fueled by the increasing adoption of Advanced Driver Assistance Systems (ADAS) and sophisticated parking technologies within the country's rapidly evolving automotive sector. The demand for both viewing and sensing cameras is escalating as automakers prioritize enhanced safety, driver convenience, and the integration of autonomous driving features. Passenger vehicles and commercial vehicles alike are increasingly equipped with these advanced camera systems, signifying a widespread commitment to modern automotive innovation. Key market players are actively investing in research and development, pushing the boundaries of camera technology to meet the stringent safety regulations and consumer expectations prevalent in the Chinese market.

China Automotive Camera Market Market Size (In Billion)

This dynamic market is shaped by several influential drivers, including government initiatives promoting automotive safety and smart mobility, coupled with a growing consumer preference for vehicles equipped with cutting-edge features. The increasing sophistication of ADAS, such as adaptive cruise control, lane keeping assist, and automatic emergency braking, directly contributes to the demand for high-performance automotive cameras. While the market is experiencing substantial growth, certain restraints, such as the initial high cost of advanced camera systems and the potential for supply chain disruptions, could pose challenges. However, ongoing technological advancements, including improvements in sensor resolution, artificial intelligence integration, and miniaturization, are expected to mitigate these concerns and further propel the market forward throughout the forecast period. The competitive landscape is characterized by the presence of established global technology giants and specialized automotive component manufacturers, all vying for a significant share of this lucrative market.

China Automotive Camera Market Company Market Share

This comprehensive report offers a deep dive into the China Automotive Camera Market, a rapidly evolving sector critical for the future of autonomous and connected vehicles. Covering the period from 2019 to 2033, with a base and estimated year of 2025, this analysis provides unparalleled insights into market dynamics, growth trends, regional dominance, product landscape, and future opportunities. Whether you are a manufacturer, supplier, investor, or industry analyst, this report is your definitive guide to navigating the complexities and capitalizing on the immense potential of China's automotive camera industry.

The report utilizes high-traffic keywords such as "China automotive camera market," "ADAS cameras," "parking cameras," "vehicle cameras," "automotive sensing cameras," "automotive viewing cameras," "passenger vehicles," "commercial vehicles," "connected car technology," and "autonomous driving" to maximize search engine visibility.

Key Data Points:

- Study Period: 2019–2033

- Base Year: 2025

- Estimated Year: 2025

- Forecast Period: 2025–2033

- Historical Period: 2019–2024

- Market Size (Units): xx billion units (Base Year 2025)

- CAGR (Forecast Period): xx%

China Automotive Camera Market Market Dynamics & Structure

The China Automotive Camera Market is characterized by a moderately concentrated structure, with a handful of global automotive suppliers and emerging domestic players holding significant market share. Technological innovation is the primary driver, fueled by the relentless pursuit of advanced driver-assistance systems (ADAS) and the burgeoning autonomous driving landscape. Stringent regulatory frameworks, particularly those mandating safety features and emissions standards, indirectly boost camera adoption. Competitive product substitutes, while present in basic rearview mirrors, are increasingly rendered obsolete by sophisticated camera-based solutions. End-user demographics are shifting towards a younger, tech-savvy consumer base in China demanding advanced safety and convenience features. Mergers and acquisitions (M&A) are a growing trend, as larger players seek to consolidate their market position, acquire cutting-edge technology, and expand their product portfolios.

- Market Concentration: Dominated by a mix of established Tier-1 suppliers and innovative Chinese companies.

- Technological Innovation: Driven by AI, machine learning, and sensor fusion for enhanced ADAS and autonomous capabilities.

- Regulatory Frameworks: Increasing mandates for safety features (e.g., AEB, LKA) are driving camera integration.

- Competitive Landscape: Traditional mirrors are being replaced by intelligent camera systems offering superior functionality.

- End-User Demographics: Growing demand for enhanced safety, convenience, and a premium in-car experience.

- M&A Trends: Strategic acquisitions to gain market share, technological prowess, and expand product offerings. For instance, xx M&A deals were recorded in the historical period, signifying consolidation efforts.

China Automotive Camera Market Growth Trends & Insights

The China Automotive Camera Market is poised for explosive growth, driven by a confluence of technological advancements, robust government support, and shifting consumer preferences. The market size is projected to expand significantly from xx billion units in 2025 to an estimated xx billion units by 2033, reflecting a robust Compound Annual Growth Rate (CAGR) of xx% during the forecast period. This surge is primarily attributed to the escalating adoption of Advanced Driver Assistance Systems (ADAS) across both passenger vehicles and commercial vehicles. As safety regulations become more stringent and consumer awareness of the benefits of ADAS, such as enhanced collision avoidance, lane-keeping assistance, and adaptive cruise control, continues to rise, the demand for sophisticated viewing cameras and sensing cameras is expected to skyrocket.

Technological disruptions are playing a pivotal role in shaping market trajectories. The integration of artificial intelligence (AI) and machine learning algorithms into automotive cameras is enabling more intelligent perception and decision-making capabilities, pushing the boundaries of what’s possible in autonomous driving. Innovations in sensor technology, including higher resolution, wider fields of view, and improved low-light performance, are further enhancing the effectiveness and reliability of these systems. Consumer behavior is also evolving rapidly, with a growing segment of the Chinese population prioritizing safety and technological sophistication in their vehicle purchases. This is compelling automakers to equip vehicles with an increasing number of cameras, from surround-view parking systems to advanced front-facing cameras for ADAS.

Furthermore, the burgeoning electric vehicle (EV) segment in China is also a significant growth accelerator. EVs are often at the forefront of adopting new technologies, and cameras are integral to their advanced safety and navigation features. The development of sophisticated parking assist systems and 360-degree camera views is transforming the driving experience, making complex maneuvers easier and safer. The historical period of 2019–2024 witnessed a steady increase in automotive camera penetration, laying a strong foundation for the accelerated growth anticipated in the coming years. The estimated market size of xx billion units in 2025 serves as a crucial benchmark, underscoring the market's significant scale and the immense opportunities for stakeholders.

Dominant Regions, Countries, or Segments in China Automotive Camera Market

The Passenger Vehicles segment, specifically within the Advanced Driver Assistance Systems (ADAS) application, is currently the dominant force driving growth in the China Automotive Camera Market. This dominance is rooted in a powerful synergy of economic policies, evolving consumer demands, and strategic industry advancements. China's commitment to becoming a global leader in intelligent and connected vehicles, coupled with stringent safety regulations for passenger cars, has created a fertile ground for ADAS technology adoption. The sheer volume of passenger vehicles produced and sold in China, accounting for approximately xx% of total vehicle sales, naturally makes this segment the largest consumer of automotive cameras.

Within the passenger vehicle segment, the increasing integration of ADAS features such as automatic emergency braking (AEB), lane keeping assist (LKA), adaptive cruise control (ACC), and blind-spot detection is a primary growth catalyst. These systems rely heavily on a sophisticated array of viewing cameras and sensing cameras, including front-facing cameras, rear-view cameras, and side-view cameras, to perceive the vehicle's surroundings and enable autonomous or semi-autonomous driving functions. The market penetration of these features in new passenger vehicles has been steadily increasing, with estimates suggesting that over xx% of new passenger cars sold in China in 2025 will be equipped with at least one ADAS feature.

Economically, the growing disposable income of Chinese consumers has fueled a demand for premium features, including advanced safety technologies. Automakers are responding by making ADAS a standard offering in mid-range and high-end passenger vehicles, and even offering it as an option in entry-level models. This widespread adoption is further supported by government initiatives promoting vehicle safety and the development of intelligent transportation systems. For instance, the "Made in China 2025" strategy and subsequent policies have emphasized technological self-sufficiency and innovation in the automotive sector, directly benefiting the growth of domestic camera manufacturers and suppliers. The projected market share of passenger vehicles within the overall automotive camera market is estimated to be around xx% in 2025, with a projected growth rate of xx% during the forecast period.

While commercial vehicles are also adopting camera technology, particularly for safety and efficiency in logistics, their current adoption rate and market volume lag behind passenger vehicles. Similarly, while parking applications are a significant driver for cameras, their growth is somewhat outpaced by the broader integration of cameras within comprehensive ADAS suites for active driving safety. Therefore, the Passenger Vehicles segment, powered by the widespread demand for Advanced Driver Assistance Systems (ADAS), stands as the undisputed leader in shaping the current and future trajectory of the China Automotive Camera Market.

China Automotive Camera Market Product Landscape

The product landscape of the China Automotive Camera Market is characterized by rapid innovation, focusing on enhanced performance, miniaturization, and intelligent integration. Manufacturers are continuously developing cameras with higher resolutions (e.g., 2MP, 8MP), wider dynamic ranges for superior low-light and high-contrast performance, and expanded fields of view to capture more environmental data. Sensing cameras, often incorporating advanced image processing algorithms and AI capabilities, are crucial for object recognition, lane detection, and pedestrian identification. Viewing cameras, including surround-view systems and digital rearview mirrors, offer enhanced situational awareness for drivers and are becoming standard in an increasing number of vehicle models. Unique selling propositions revolve around cost-effectiveness, robust environmental resistance (e.g., water, dust, temperature extremes), and seamless integration with vehicle electronic architectures.

Key Drivers, Barriers & Challenges in China Automotive Camera Market

Key Drivers:

- Government Mandates & Safety Regulations: Increasing requirements for ADAS features like AEB and LKA.

- Technological Advancements: Development of AI-powered image processing and sensor fusion.

- Consumer Demand for Safety & Convenience: Growing preference for vehicles with advanced driver assistance features.

- Growth of Autonomous Driving Technology: Essential for perception and navigation in self-driving vehicles.

- Electric Vehicle (EV) Adoption: EVs often lead in integrating cutting-edge automotive technologies.

Key Barriers & Challenges:

- High R&D Costs: Significant investment required for developing sophisticated camera technologies.

- Supply Chain Disruptions: Potential for component shortages and price volatility, as seen with global semiconductor shortages impacting production by xx%.

- Regulatory Complexity & Standardization: Evolving standards and homologation processes can slow down market entry.

- Cybersecurity Concerns: Protecting camera systems from malicious attacks and ensuring data privacy.

- Cost Sensitivity: Balancing advanced features with affordable pricing for mass-market adoption.

Emerging Opportunities in China Automotive Camera Market

Emerging opportunities in the China Automotive Camera Market lie in the increasing demand for sophisticated in-cabin monitoring systems for driver alertness and passenger safety, alongside the expansion of sensor fusion technologies that combine camera data with radar and lidar for more robust perception. The development of smart cameras with integrated AI capabilities for edge computing, reducing reliance on central processing units, presents a significant avenue for growth. Furthermore, the application of automotive cameras in commercial vehicle fleet management, for enhanced safety, driver behavior analysis, and cargo security, offers substantial untapped potential. The continuous innovation in compact and durable camera designs for specialized applications, such as truck and bus ADAS, also presents a burgeoning market.

Growth Accelerators in the China Automotive Camera Market Industry

Several key catalysts are accelerating the growth of the China Automotive Camera Market. Continuous technological breakthroughs in image sensors, processing power, and AI algorithms are enabling more advanced and affordable camera solutions. Strategic partnerships and collaborations between automotive OEMs, Tier-1 suppliers, and technology companies are fostering innovation and faster product development cycles. The increasing investment in smart city initiatives and intelligent transportation systems by the Chinese government indirectly drives the demand for vehicle-based camera technologies. Moreover, market expansion strategies, including the development of more cost-effective camera solutions for entry-level vehicles and the exploration of aftermarket integration, are broadening the market's reach and accelerating adoption rates.

Key Players Shaping the China Automotive Camera Market Market

- Denso Corporation

- Delphi Automotive PLC

- Continental AG

- Autoliv Inc

- GWR safety system

- Robert Bosch GmbH

- Sony Electronics

- Panasonic Corporation

Notable Milestones in China Automotive Camera Market Sector

- 2019/05: Sony announces its new automotive image sensor with enhanced dynamic range, improving low-light performance.

- 2020/11: Continental AG launches its advanced surround-view camera system, enhancing parking assist capabilities.

- 2021/07: Bosch introduces its AI-powered vision system for ADAS, boosting object recognition accuracy.

- 2022/03: Panasonic showcases its high-resolution automotive camera for autonomous driving applications.

- 2022/09: Denso Corporation invests in a startup specializing in AI for automotive computer vision.

- 2023/01: Autoliv Inc expands its collaboration with an OEM to integrate advanced camera-based safety features.

- 2023/08: GWR Safety System receives significant funding to scale its automotive camera production.

- 2024/02: Delphi Automotive PLC announces a new generation of sensing cameras with improved thermal imaging capabilities.

In-Depth China Automotive Camera Market Market Outlook

The future outlook for the China Automotive Camera Market is exceptionally promising, driven by accelerating trends in vehicle electrification, autonomous driving, and enhanced safety. Growth accelerators such as continuous innovation in AI-powered perception systems and strategic collaborations will ensure that cameras remain at the forefront of automotive technology. The market is expected to witness significant expansion in advanced applications beyond traditional ADAS, including in-cabin monitoring and driver behavior analysis. The ongoing commitment to smart mobility by the Chinese government will further fuel demand. Stakeholders who can offer cost-effective, high-performance, and secure camera solutions are well-positioned to capitalize on the substantial growth opportunities and shape the future of automotive vision systems in China.

China Automotive Camera Market Segmentation

-

1. Vehicle Type

- 1.1. Passenger Vehicles

- 1.2. Commercial Vehicles

-

2. Type

- 2.1. Viewing Camera

- 2.2. Sensing Camera

-

3. Application

- 3.1. Advanced Driver Assistance Systems (ADAS)

- 3.2. Parking

China Automotive Camera Market Segmentation By Geography

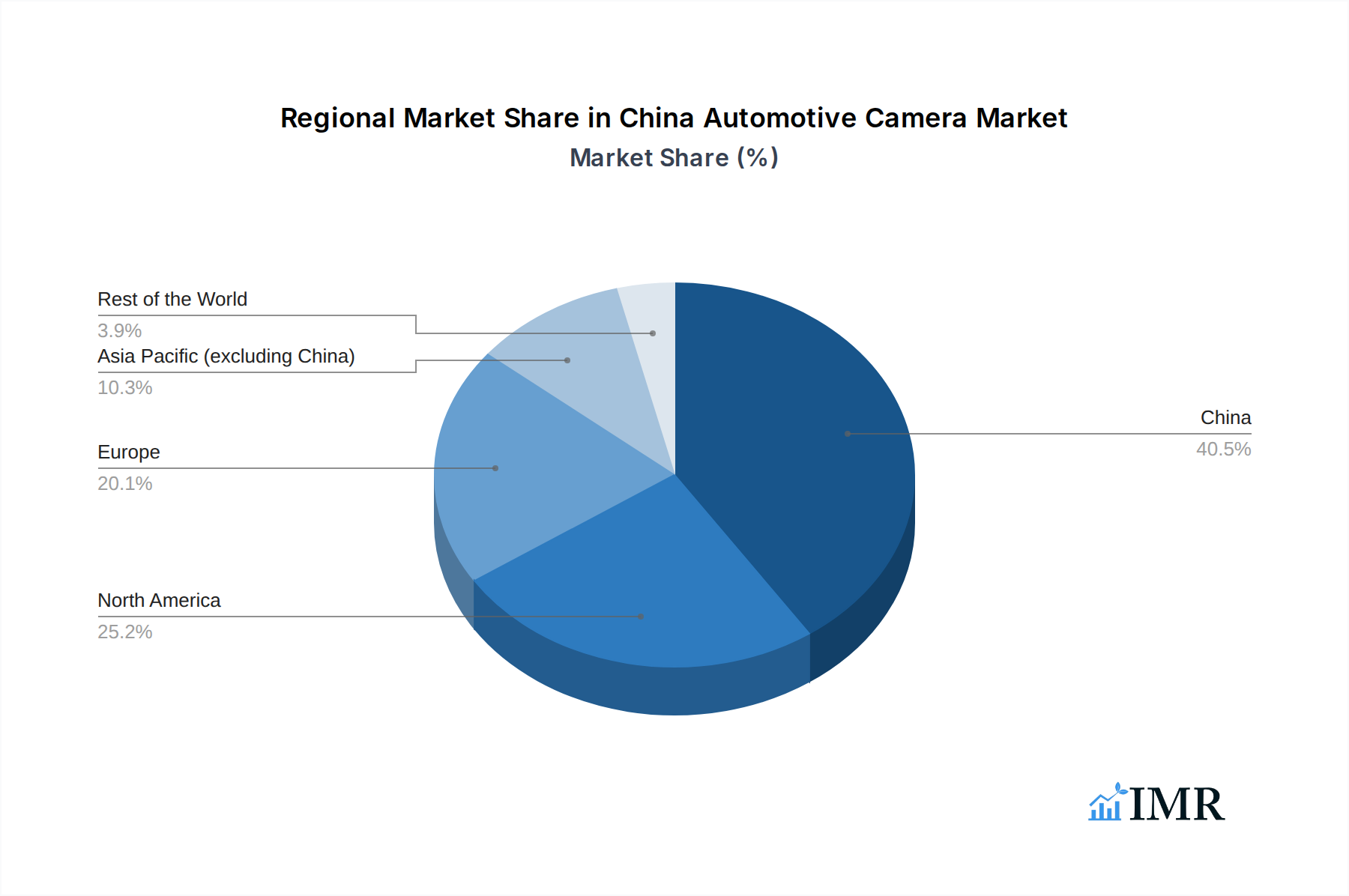

- 1. China

China Automotive Camera Market Regional Market Share

Geographic Coverage of China Automotive Camera Market

China Automotive Camera Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.21% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 5.1.1. Passenger Vehicles

- 5.1.2. Commercial Vehicles

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Viewing Camera

- 5.2.2. Sensing Camera

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Advanced Driver Assistance Systems (ADAS)

- 5.3.2. Parking

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6. China Automotive Camera Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 6.1.1. Passenger Vehicles

- 6.1.2. Commercial Vehicles

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Viewing Camera

- 6.2.2. Sensing Camera

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Advanced Driver Assistance Systems (ADAS)

- 6.3.2. Parking

- 6.1. Market Analysis, Insights and Forecast - by Vehicle Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Denso Corporation

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Delphi Automotive PLC

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Continental AG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Autoliv Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 GWR safety system

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Robert Bosch GmbH

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Sony Electronics

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Panasonic Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.1 Denso Corporation

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China Automotive Camera Market Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: China Automotive Camera Market Share (%) by Company 2025

List of Tables

- Table 1: China Automotive Camera Market Revenue undefined Forecast, by Vehicle Type 2020 & 2033

- Table 2: China Automotive Camera Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: China Automotive Camera Market Revenue undefined Forecast, by Application 2020 & 2033

- Table 4: China Automotive Camera Market Revenue undefined Forecast, by Region 2020 & 2033

- Table 5: China Automotive Camera Market Revenue undefined Forecast, by Vehicle Type 2020 & 2033

- Table 6: China Automotive Camera Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 7: China Automotive Camera Market Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: China Automotive Camera Market Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Automotive Camera Market?

The projected CAGR is approximately 7.21%.

2. Which companies are prominent players in the China Automotive Camera Market?

Key companies in the market include Denso Corporation, Delphi Automotive PLC, Continental AG, Autoliv Inc, GWR safety system, Robert Bosch GmbH, Sony Electronics, Panasonic Corporation.

3. What are the main segments of the China Automotive Camera Market?

The market segments include Vehicle Type, Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

ADOPTION OF STEER-BY-WIRE SYSTEM AIDING MARKET GROWTH; Others.

6. What are the notable trends driving market growth?

Increasing Demand for Safety Features.

7. Are there any restraints impacting market growth?

RAW MATERIAL PRICE INCREASES ARE EXPECTED TO STIFLE MARKET GROWTH; Others.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Automotive Camera Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Automotive Camera Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Automotive Camera Market?

To stay informed about further developments, trends, and reports in the China Automotive Camera Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence