Key Insights

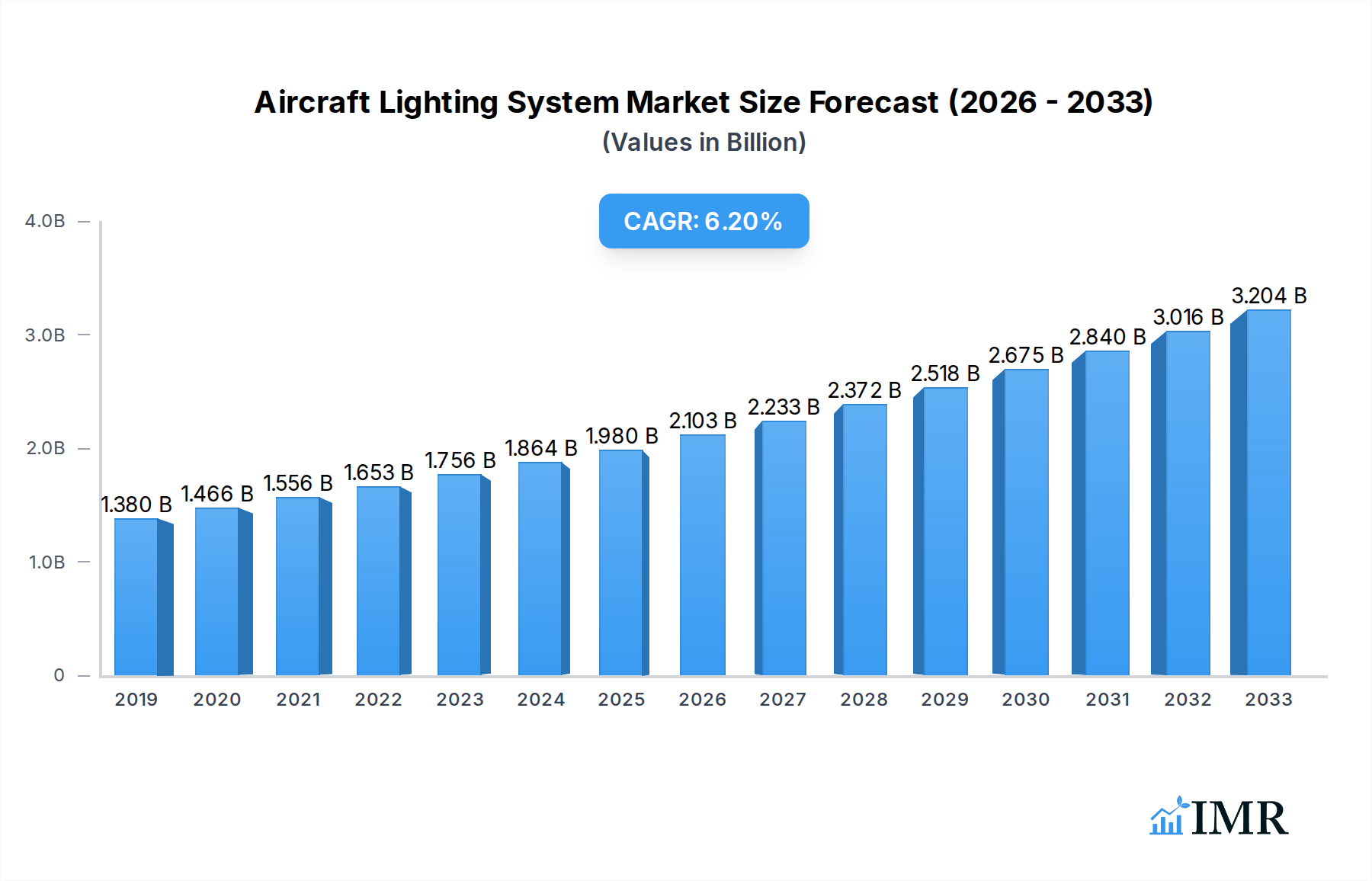

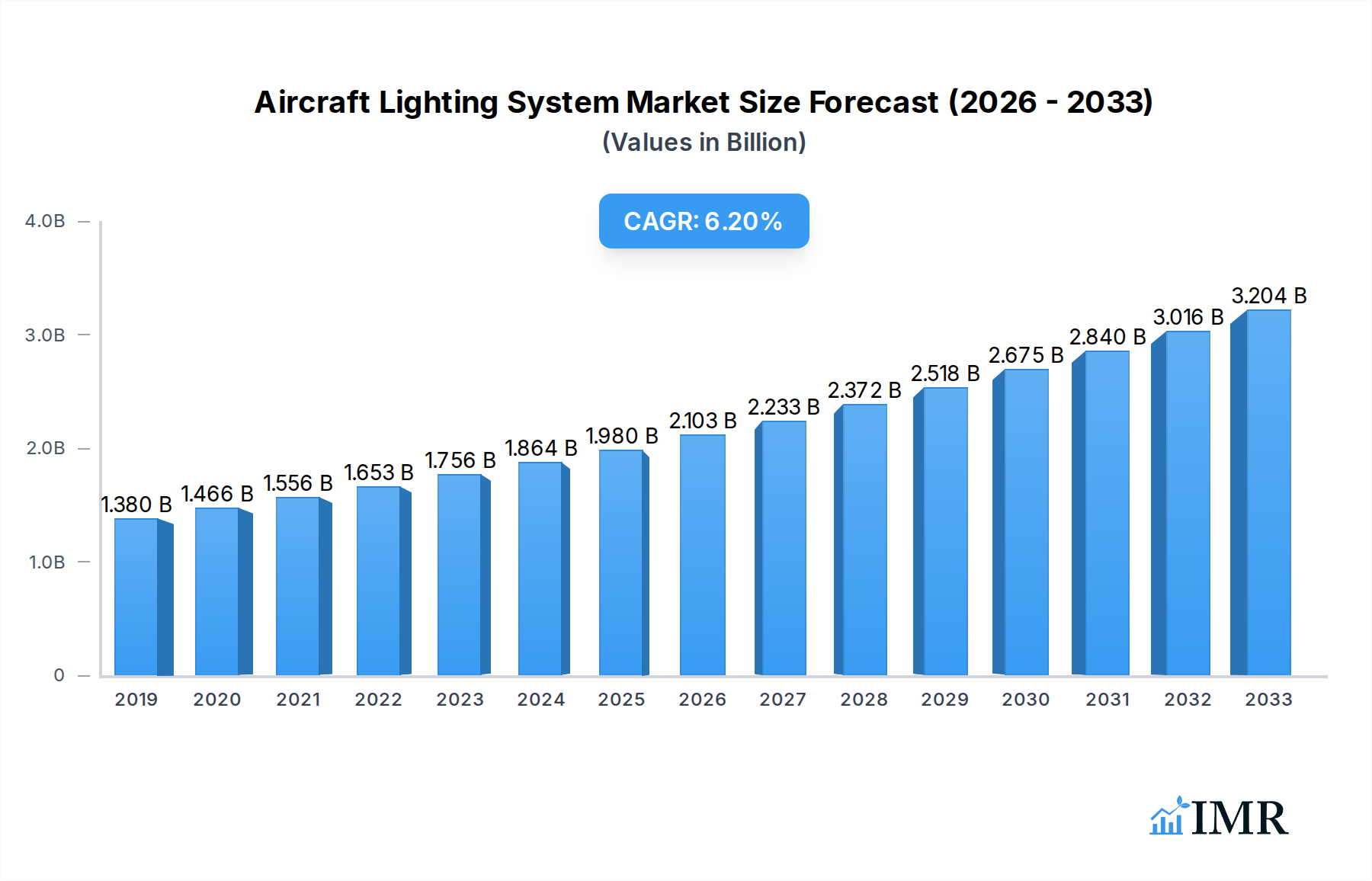

The global Aircraft Lighting System market is poised for robust growth, driven by an escalating demand for advanced aviation solutions and a focus on enhanced operational efficiency and passenger experience. Valued at approximately $1.86 billion in 2024, the market is projected to expand significantly, exhibiting a compound annual growth rate (CAGR) of 6.2% from 2025 to 2033. This growth trajectory is primarily fueled by the continuous expansion of the global commercial aircraft fleet, increased aircraft deliveries, and a heightened emphasis on retrofitting existing aircraft with modern, energy-efficient lighting technologies, particularly LEDs. Technological advancements in solid-state lighting (SSL), including the integration of smart and dynamic cabin lighting systems, are pivotal trends enhancing passenger comfort, reducing maintenance costs, and improving safety. Moreover, stringent aviation regulations mandating superior illumination for safety and visibility continue to underpin market expansion, pushing manufacturers towards innovative and compliant lighting solutions across all aircraft types.

Aircraft Lighting System Market Size (In Billion)

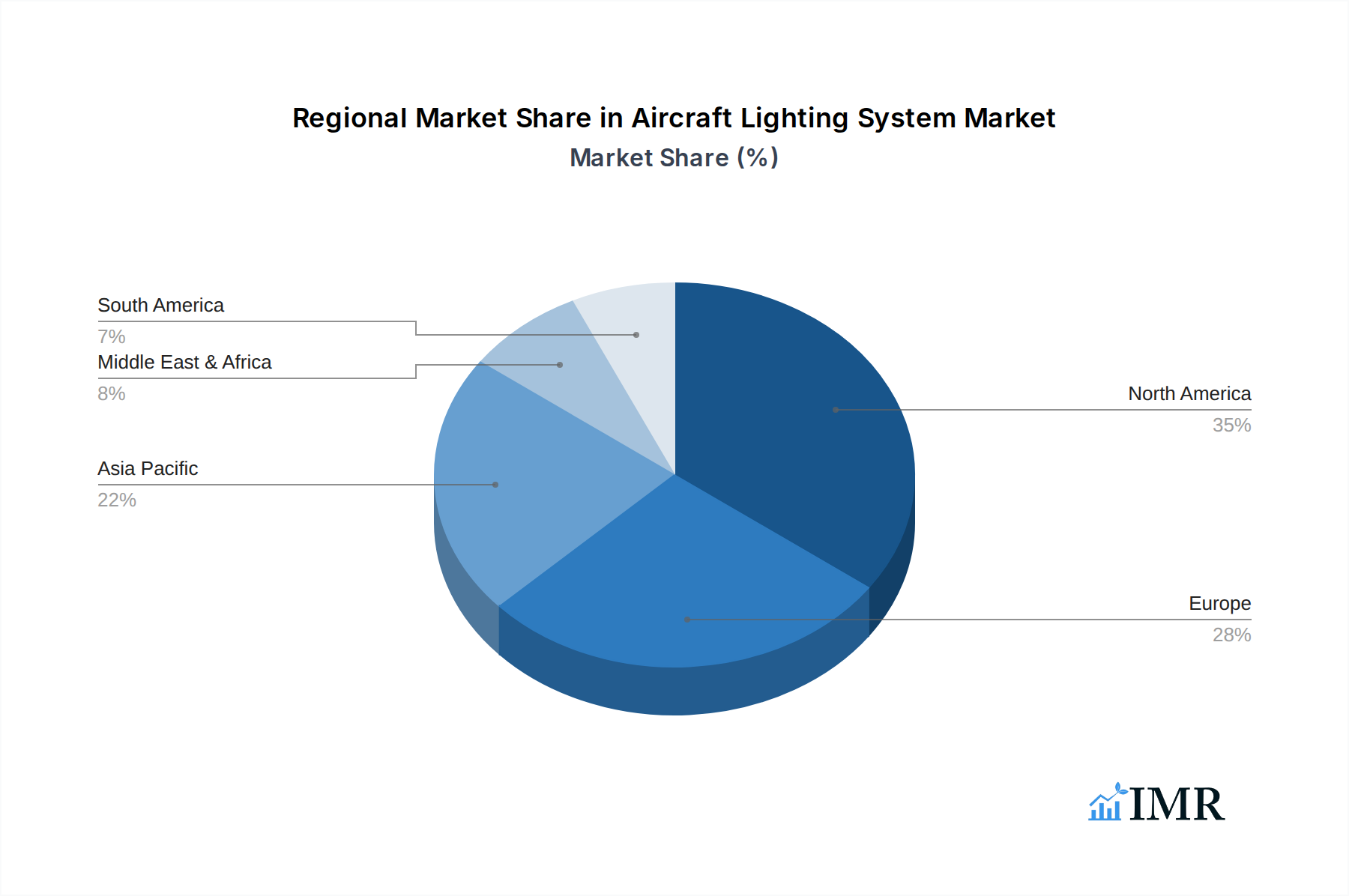

Key drivers include the burgeoning air travel demand, which necessitates a larger and more modern fleet, and the aerospace industry's shift towards sustainable and lightweight components. The adoption of advanced lighting systems such as OLEDs and intelligent controls for adaptive lighting environments further elevates the market's potential. While opportunities abound, the market also navigates challenges such as the high initial investment costs associated with advanced lighting technologies and the complex, time-consuming certification processes required for aviation components. Nevertheless, leading companies like Collins Aerospace, Bruce Aerospace, and Astronics Corporation are continually innovating across segments, from interior cabin lighting focused on passenger wellness to robust external and emergency lighting crucial for flight safety. The market sees significant activity in North America and Europe, traditional aerospace hubs, with Asia Pacific emerging as a rapidly growing region due to its expanding aviation infrastructure and increasing aircraft production.

Aircraft Lighting System Company Market Share

Aircraft Lighting System Market: Illuminating Growth and Innovation (2019-2033)

Unlock unparalleled insights into the dynamic Aircraft Lighting System Market with our comprehensive report, meticulously analyzing aviation lighting systems from 2019 to 2033. Positioned as a critical segment within the broader Aerospace & Defense MRO and Aircraft Components Market (parent market), the aircraft lighting system market (child market) is poised for significant expansion, driven by advancements in LED aircraft lights, stringent safety regulations, and the global demand for upgraded cabin lighting, exterior aircraft lighting, and emergency aircraft lighting. This report offers an in-depth exploration of market trends, competitive landscapes, and technological innovations shaping the future of aerospace lighting, providing stakeholders with the strategic intelligence needed to capitalize on emerging opportunities in this high-growth sector.

With an estimated market valuation reaching $xx billion in 2025 and projected to grow to $yy billion by 2033 at a compelling CAGR of 6.8%, the aircraft lighting system industry is undergoing a profound transformation. Our analysis spans a historical period from 2019–2024, establishes 2025 as the base and estimated year, and provides a robust forecast through 2033. This report is indispensable for industry professionals, investors, and manufacturers seeking to understand the intricacies of military aircraft lighting, commercial aircraft lighting, and private plane lighting while navigating technological disruptions and evolving market dynamics.

Aircraft Lighting System Market Dynamics & Structure

The Aircraft Lighting System Market exhibits a moderately concentrated structure, with a few major players holding significant market share, alongside numerous specialized niche providers. Technological innovation is a primary driver, continually pushing for enhanced energy efficiency, reduced weight, and improved longevity through the adoption of advanced LED aircraft lights and smart control systems. Regulatory frameworks, notably those set by organizations like the FAA, EASA, and ICAO, are paramount, dictating rigorous safety, performance, and certification standards for all lighting components, from emergency exit path marking to cockpit illumination. These regulations often necessitate substantial R&D investments and lengthy approval processes, acting as both a barrier to entry and a guarantee of quality.

Competitive product substitutes primarily involve legacy lighting technologies (e.g., incandescent, fluorescent) being phased out in favor of LEDs, offering superior performance metrics. While direct substitutes are limited due to specialized aviation requirements, innovation within the LED segment continuously introduces newer, more advanced options. End-user demographics are diverse, encompassing commercial airlines focused on passenger experience and operational cost reduction, military operators prioritizing durability and mission-specific capabilities (e.g., NVG compatibility), and private plane owners seeking luxury and customization. This segmentation influences product design, pricing strategies, and sales channels.

Mergers and Acquisitions (M&A) trends indicate a drive towards consolidation and technological integration. Larger aerospace component manufacturers frequently acquire smaller, innovative lighting specialists to expand their portfolios and gain access to cutting-edge technologies. For instance, the market has seen M&A deal volumes totaling approximately $3.5 billion over the historical period (2019-2024), reflecting a strategic move to strengthen market positions. The top three companies (e.g., Collins Aerospace, Honeywell, Astronics) collectively command an estimated 45-50% market share, underscoring the influence of established players. Innovation barriers include high initial R&D costs, the need for extensive flight testing, and complex supply chain management, particularly for specialized components. These factors make it challenging for new entrants to quickly establish a foothold, reinforcing the dominance of seasoned industry veterans.

Aircraft Lighting System Growth Trends & Insights

The Aircraft Lighting System Market is undergoing a robust evolution, with market size demonstrating a consistent upward trajectory. From an estimated $5.2 billion in 2019, the market is projected to reach $7.5 billion by 2025 and further expand to $11.8 billion by 2033, exhibiting a compound annual growth rate (CAGR) of 6.8% over the forecast period. This growth is primarily fueled by the accelerating adoption rates of energy-efficient and long-lasting LED aircraft lighting solutions, both in new aircraft deliveries and through comprehensive retrofit programs for existing fleets. The shift from traditional incandescent and fluorescent lighting to LED technology is a significant technological disruption, offering benefits such as reduced power consumption, lower maintenance costs, and enhanced customization capabilities.

Technological disruptions extend beyond mere LED integration to include the emergence of "smart lighting" systems, which incorporate sensors, connectivity, and intelligent controls. These systems can dynamically adjust lighting levels and color temperatures based on flight phases, time of day, and even passenger preferences, significantly enhancing the cabin experience. Advancements in miniaturization and lightweight designs are also reducing overall aircraft weight, contributing to fuel efficiency—a critical concern for airlines globally. Furthermore, the integration of lighting with other onboard systems, such as in-flight entertainment (IFE) and communication networks, is creating sophisticated, interconnected environments.

Consumer behavior shifts, particularly among airlines, are heavily influencing market demand. There is a growing emphasis on creating a comfortable, aesthetically pleasing, and brand-consistent passenger environment, driving demand for advanced interior lighting systems that offer dynamic mood lighting and personalized control. For military applications, the focus remains on reliability, stealth capabilities (e.g., reduced electromagnetic interference, IR lighting), and extreme durability to withstand harsh operating conditions. Private plane owners, conversely, prioritize bespoke, luxurious, and highly customizable lighting solutions that reflect personal style and enhance comfort. The market penetration of LED technology in new aircraft is approaching near saturation, suggesting that the retrofit market, particularly for older commercial aircraft and general aviation, represents a substantial and ongoing growth opportunity. This continuous modernization cycle, coupled with the global expansion of air travel and the replacement of aging fleets, underpins the sustained growth of the aircraft lighting system market.

Dominant Regions, Countries, or Segments in Aircraft Lighting System

Analyzing the Aircraft Lighting System Market across its various dimensions reveals key areas of dominance. Geographically, North America consistently leads the market, holding an estimated 38% market share in 2025. This dominance is attributed to the presence of major aircraft OEMs, a vast existing fleet requiring MRO and upgrades, and substantial defense spending driving demand for advanced military aircraft lighting. Following North America, Europe and Asia-Pacific represent significant and rapidly growing markets, driven by fleet expansion and modernization programs.

From an application perspective, the Commercial Aircraft segment is the undeniable frontrunner, accounting for approximately 62% of the market share. The sheer volume of commercial aircraft in operation, coupled with airlines' continuous efforts to enhance passenger experience, improve operational efficiency, and adhere to stringent safety regulations, fuels this segment's growth. High utilization rates of commercial aircraft also necessitate frequent maintenance and upgrades of lighting systems, contributing significantly to the aftermarket segment.

- Key Drivers for Commercial Aircraft Dominance:

- Passenger Experience Enhancement: Airlines invest in advanced cabin lighting to create dynamic ambiances, reduce jet lag, and improve overall passenger comfort and satisfaction.

- Operational Efficiency: Adoption of LED lighting drastically reduces power consumption, extending maintenance cycles, and lowering fuel costs.

- Fleet Modernization: A global trend of replacing older aircraft with new, more efficient models that come equipped with advanced lighting systems.

- Safety and Regulations: Continuous updates to safety standards for emergency lighting and exterior lighting systems (e.g., anti-collision lights, runway illumination).

- MRO Demand: The extensive maintenance, repair, and overhaul needs of a large commercial fleet ensure a steady demand for replacement and upgrade components.

Within the 'Type' segment, Interior Lighting holds the largest market share, estimated at 55%. This is driven by the complexity and customization required for cabin illumination, cockpit lighting, and specialized passenger service units, all of which contribute to the passenger experience and flight crew functionality. Exterior lighting, encompassing navigation lights, landing lights, and anti-collision lights, follows, driven by safety imperatives and technological advancements in visibility. Emergency lighting, while critical, represents a smaller but highly regulated segment focused on reliability and certification. The dominance of commercial aviation and interior lighting is expected to persist, although military applications and specialized external lighting systems will continue to grow, driven by technological advancements and defense budgets.

Aircraft Lighting System Product Landscape

The Aircraft Lighting System product landscape is characterized by continuous innovation, primarily driven by the transition to LED technology. Modern systems offer full-spectrum, dynamic cabin lighting capable of simulating natural daylight cycles, drastically improving passenger comfort and reducing jet lag. Cockpit lighting has evolved to include NVG-compatible options and highly customizable displays that minimize pilot fatigue. External lighting, such as landing, taxi, and anti-collision lights, now leverages high-intensity, energy-efficient LEDs, providing superior visibility and extending operational life significantly. Performance metrics highlight exceptional energy efficiency (up to 80% less power consumption compared to traditional systems), extended operational lifespans exceeding 50,000 hours, and robust resistance to vibration and temperature extremes. Unique selling propositions include enhanced passenger experience through personalized lighting zones, reduced maintenance burden for airlines, and improved safety through fail-safe designs. Technological advancements are focusing on miniaturization, seamless integration with cabin management systems, and the potential for Li-Fi (Light Fidelity) integration for in-flight connectivity, further solidifying the industry's move towards intelligent and connected aircraft environments.

Key Drivers, Barriers & Challenges in Aircraft Lighting System

Key Drivers

The Aircraft Lighting System market is propelled by several potent forces. Technologically, the pervasive adoption of LED aircraft lights is paramount, offering unparalleled energy efficiency, extended operational lifespan, and enhanced design flexibility. This shift directly addresses economic drivers, as airlines face intense pressure to reduce operational costs, making LEDs' lower power consumption and reduced maintenance needs highly attractive. Policy-driven factors, such as stringent safety regulations from aviation authorities (e.g., FAA, EASA) and environmental mandates for greener aircraft, necessitate constant upgrades to compliant and sustainable lighting solutions. For example, the continuous modernization of global airline fleets and military aircraft programs worldwide fuels demand for advanced, certified lighting systems. Furthermore, a growing emphasis on passenger comfort and customizable cabin lighting to enhance the in-flight experience is a significant market accelerator, driving innovation in interior lighting.

Barriers & Challenges

Despite robust growth, the Aircraft Lighting System market faces notable barriers and challenges. Supply chain issues, particularly related to the availability of specialized semiconductor components and raw materials, can lead to production delays and increased costs. Regulatory hurdles present a significant restraint; the rigorous and often lengthy certification processes for new aviation products, essential for ensuring safety and reliability, can be expensive (often running into millions of dollars per product line) and time-consuming, delaying market entry for innovations. Competitive pressures are intense, with a constant demand for cost-effective solutions without compromising quality or compliance. Moreover, the long design and integration cycles within aircraft manufacturing demand that lighting system developers anticipate future trends years in advance. Intellectual property disputes and the rapid obsolescence of certain electronic components also pose continuous challenges for manufacturers striving to remain competitive and compliant.

Emerging Opportunities in Aircraft Lighting System

The Aircraft Lighting System market is ripe with emerging opportunities, particularly in untapped markets and innovative applications. The extensive global fleet of older aircraft presents a substantial retrofit market, where the upgrade from legacy lighting to modern LED aircraft lights offers significant energy savings and operational benefits. Emerging economies, rapidly expanding their aviation infrastructure and fleets, represent growing demand centers. Innovative applications include the integration of Li-Fi technology for secure, high-speed in-flight connectivity directly through cabin lighting, offering a dual-purpose system. Personalized passenger zones with individual lighting controls and color settings are gaining traction, enhancing passenger experience. Furthermore, adaptive exterior lighting systems that adjust brightness and beam patterns based on ambient conditions or specific flight phases represent an untapped safety and efficiency enhancement. The potential for UV-C sanitation lighting in cabins for enhanced hygiene post-pandemic also presents a novel and significant opportunity.

Growth Accelerators in the Aircraft Lighting System Industry

Growth in the Aircraft Lighting System industry is significantly accelerated by continuous technological breakthroughs, strategic partnerships, and focused market expansion strategies. Advances in material science enable lighter, more durable lighting components, while miniaturization allows for greater design flexibility and integration. Breakthroughs in intelligent lighting control systems, leveraging AI and machine learning, are leading to truly adaptive and predictive lighting environments both inside and outside the aircraft. Strategic partnerships between lighting manufacturers, avionics suppliers, and major aircraft OEMs are crucial for developing integrated, full-system solutions that meet future aircraft demands. Collaborations with MRO providers enhance aftermarket service capabilities and accelerate retrofit installations. Market expansion strategies include targeting the burgeoning general aviation and business jet sectors with premium, customized solutions, as well as deepening penetration in the fast-growing Asia-Pacific and Middle Eastern aviation markets, driven by new fleet acquisitions and infrastructure development.

Key Players Shaping the Aircraft Lighting System Market

- Bruce Aerospace

- Collins Aerospace

- Astronics Corporation

- Cobham Aerospace Communications

- Diehl Stiftung & Co. KG

- STG Aerospace Limited

- Luminator Aerospace

- Honeywell International Inc

- Hoffman Engineering

- Safran

- Geltronix

Notable Milestones in Aircraft Lighting System Sector

- 2020: Introduction of advanced full-spectrum LED cabin lighting solutions by Collins Aerospace, designed to mitigate jet lag and enhance passenger well-being on long-haul flights.

- 2021: Astronics Corporation launches a new generation of smart LED cockpit lighting systems, offering enhanced visibility and customizable settings for reduced pilot fatigue.

- 2022: STG Aerospace Limited achieves significant certification for its Saf-T-Glo® photoluminescent floor path marking system, setting new standards for emergency egress in commercial aircraft.

- 2023: Honeywell International Inc. announces a strategic partnership with a major airframe manufacturer to co-develop integrated exterior lighting systems for next-generation aircraft, focusing on adaptive visibility and energy efficiency.

- 2024: Geltronix, a specialized LED technology provider, is acquired by a leading aerospace component supplier, bolstering its capabilities in the burgeoning market for lightweight and durable aviation lighting.

In-Depth Aircraft Lighting System Market Outlook

The Aircraft Lighting System Market is set for sustained and dynamic growth, primarily driven by relentless technological innovation, a global push towards sustainability, and the evolving demands of an enhanced passenger experience. The widespread adoption of LED aircraft lights will continue to be a core accelerator, offering unparalleled energy efficiency, extended operational lifespans, and significant maintenance cost reductions for airlines. Strategic opportunities abound in the retrofit market, catering to an extensive installed base of older aircraft eager for modernization, and in developing highly integrated, "smart" lighting solutions that seamlessly interact with other onboard systems. The future will see more personalized, adaptive, and connected lighting environments, leveraging digitalization and advanced analytics to optimize both safety and passenger comfort. This forward trajectory, underpinned by stringent regulatory frameworks and a focus on operational excellence, solidifies the aircraft lighting system industry's position as a vital and expanding segment within the broader aerospace sector.

Aircraft Lighting System Segmentation

-

1. Application

- 1.1. Military Aircraft

- 1.2. Commercial Aircraft

- 1.3. Private Plane

- 1.4. Others

-

2. Type

- 2.1. Interior Lighting

- 2.2. External Lighting

- 2.3. Emergency Lighting

Aircraft Lighting System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Aircraft Lighting System Regional Market Share

Geographic Coverage of Aircraft Lighting System

Aircraft Lighting System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Military Aircraft

- 5.1.2. Commercial Aircraft

- 5.1.3. Private Plane

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Interior Lighting

- 5.2.2. External Lighting

- 5.2.3. Emergency Lighting

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Aircraft Lighting System Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Military Aircraft

- 6.1.2. Commercial Aircraft

- 6.1.3. Private Plane

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Interior Lighting

- 6.2.2. External Lighting

- 6.2.3. Emergency Lighting

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Aircraft Lighting System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Military Aircraft

- 7.1.2. Commercial Aircraft

- 7.1.3. Private Plane

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Interior Lighting

- 7.2.2. External Lighting

- 7.2.3. Emergency Lighting

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Aircraft Lighting System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Military Aircraft

- 8.1.2. Commercial Aircraft

- 8.1.3. Private Plane

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Interior Lighting

- 8.2.2. External Lighting

- 8.2.3. Emergency Lighting

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Aircraft Lighting System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Military Aircraft

- 9.1.2. Commercial Aircraft

- 9.1.3. Private Plane

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Interior Lighting

- 9.2.2. External Lighting

- 9.2.3. Emergency Lighting

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Aircraft Lighting System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Military Aircraft

- 10.1.2. Commercial Aircraft

- 10.1.3. Private Plane

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Interior Lighting

- 10.2.2. External Lighting

- 10.2.3. Emergency Lighting

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Aircraft Lighting System Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Military Aircraft

- 11.1.2. Commercial Aircraft

- 11.1.3. Private Plane

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Interior Lighting

- 11.2.2. External Lighting

- 11.2.3. Emergency Lighting

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Bruce Aerospace

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Collins Aerospace

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Astronics Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Cobham Aerospace Communications

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Diehl Stiftung & Co. KG

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 STG Aerospace Limited

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Luminator Aerospace

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Honeywell International Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Hoffman Engineering

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Safran

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Geltronix

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Bruce Aerospace

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Aircraft Lighting System Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Aircraft Lighting System Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Aircraft Lighting System Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Aircraft Lighting System Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Aircraft Lighting System Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Aircraft Lighting System Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Aircraft Lighting System Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Aircraft Lighting System Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Aircraft Lighting System Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Aircraft Lighting System Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Aircraft Lighting System Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Aircraft Lighting System Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Aircraft Lighting System Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Aircraft Lighting System Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Aircraft Lighting System Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Aircraft Lighting System Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Aircraft Lighting System Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Aircraft Lighting System Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Aircraft Lighting System Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Aircraft Lighting System Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Aircraft Lighting System Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Aircraft Lighting System Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Aircraft Lighting System Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Aircraft Lighting System Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Aircraft Lighting System Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Aircraft Lighting System Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Aircraft Lighting System Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Aircraft Lighting System Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Aircraft Lighting System Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Aircraft Lighting System Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Aircraft Lighting System Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aircraft Lighting System Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Aircraft Lighting System Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Aircraft Lighting System Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Aircraft Lighting System Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Aircraft Lighting System Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Aircraft Lighting System Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Aircraft Lighting System Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Aircraft Lighting System Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Aircraft Lighting System Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Aircraft Lighting System Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Aircraft Lighting System Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Aircraft Lighting System Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Aircraft Lighting System Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Aircraft Lighting System Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Aircraft Lighting System Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Aircraft Lighting System Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Aircraft Lighting System Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Aircraft Lighting System Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Aircraft Lighting System Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aircraft Lighting System?

The projected CAGR is approximately 6.2%.

2. Which companies are prominent players in the Aircraft Lighting System?

Key companies in the market include Bruce Aerospace, Collins Aerospace, Astronics Corporation, Cobham Aerospace Communications, Diehl Stiftung & Co. KG, STG Aerospace Limited, Luminator Aerospace, Honeywell International Inc, Hoffman Engineering, Safran, Geltronix.

3. What are the main segments of the Aircraft Lighting System?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.98 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aircraft Lighting System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aircraft Lighting System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aircraft Lighting System?

To stay informed about further developments, trends, and reports in the Aircraft Lighting System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence