Key Insights

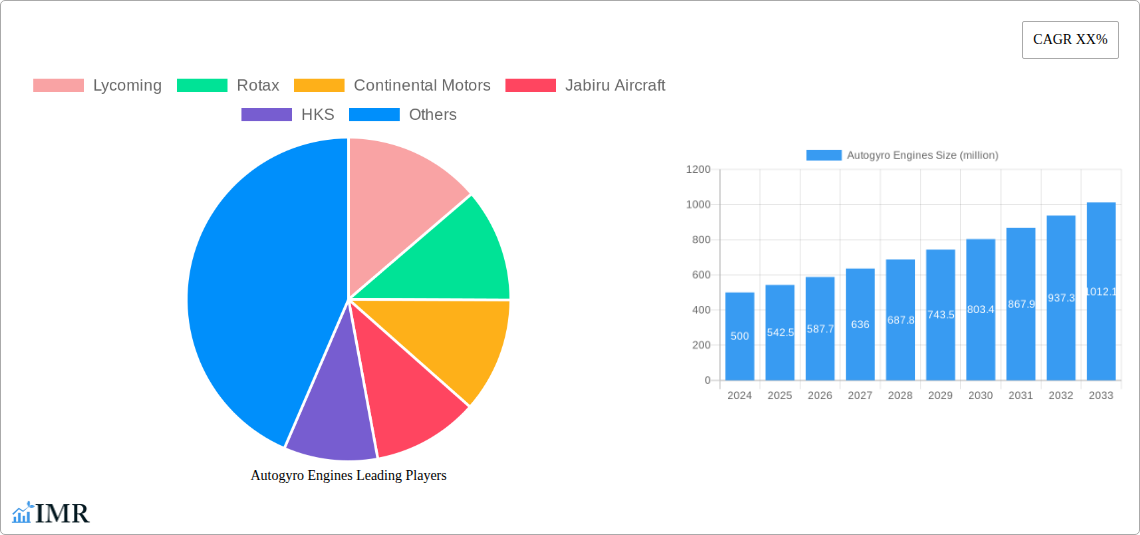

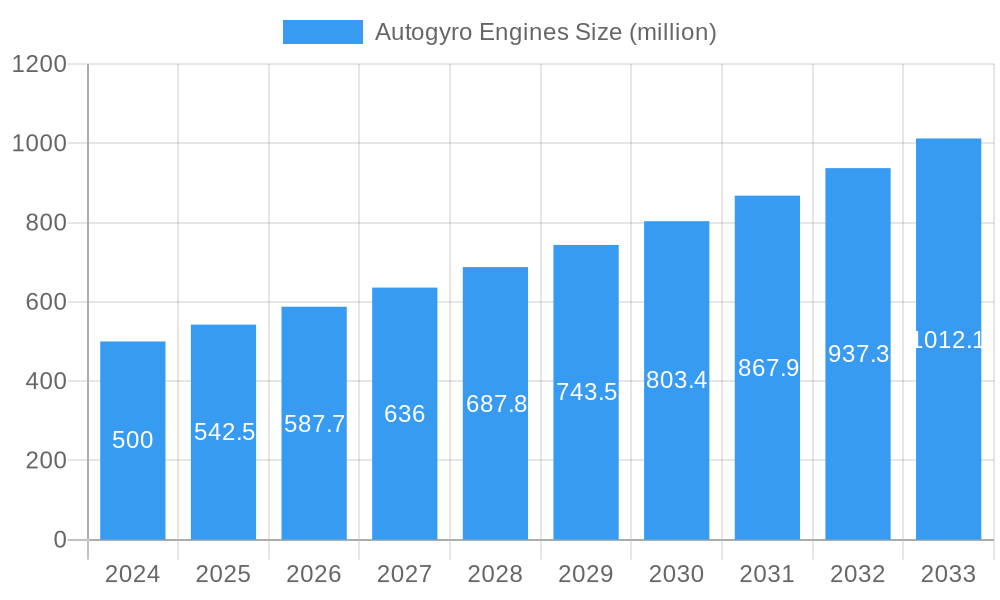

The global autogyro engine market is poised for substantial growth, projecting a market size of $0.5 billion in 2024, with an anticipated Compound Annual Growth Rate (CAGR) of 8.5% through 2033. This expansion is primarily driven by the increasing demand for personal and recreational aviation, coupled with the inherent safety and operational advantages of autogyros. The versatility of autogyro engines, catering to both civil and military applications, further fuels market momentum. Civil use applications, ranging from recreational flying and aerial tourism to agricultural surveying and emergency services, represent a significant segment. In the military sphere, autogyros offer cost-effective reconnaissance, surveillance, and training platforms, contributing to sustained demand. The market is segmented by engine type, with both 2-stroke and 4-stroke engines playing crucial roles, each offering distinct performance characteristics and applications within the autogyro landscape.

Autogyro Engines Market Size (In Million)

Key trends shaping the autogyro engine market include advancements in engine technology leading to improved fuel efficiency, reduced emissions, and enhanced reliability. The integration of lightweight materials and sophisticated control systems is also a prominent trend, contributing to the overall performance and appeal of autogyros. While the market is experiencing robust growth, certain restraints need consideration. The initial cost of autogyro acquisition and the specialized training required for operation can pose challenges for wider adoption. Furthermore, stringent aviation regulations and the need for consistent maintenance can also impact market penetration. Despite these hurdles, the inherent advantages of autogyros, such as their ability to operate from short, unprepared surfaces and their intrinsic stability, continue to drive interest and investment in the market. Leading companies like Lycoming, Rotax, and Continental Motors are at the forefront of innovation, developing advanced engine solutions to meet the evolving demands of this dynamic sector.

Autogyro Engines Company Market Share

Autogyro Engines Market Report: Dynamics, Trends, and Future Outlook (2019–2033)

This comprehensive report offers an in-depth analysis of the global Autogyro Engines market, projecting significant growth and outlining key trends from 2019 to 2033. Covering market dynamics, growth trajectories, regional dominance, product innovations, and the competitive landscape, this study is essential for stakeholders seeking to understand and capitalize on opportunities within this dynamic sector. With a base year of 2025 and a forecast period extending to 2033, the report provides actionable insights backed by rigorous research and valuable quantitative data.

Autogyro Engines Market Dynamics & Structure

The Autogyro Engines market, while niche, is characterized by a moderate market concentration, with a few key players holding significant sway. Technological innovation remains a primary driver, fueled by the pursuit of enhanced fuel efficiency, reduced emissions, and improved reliability for both civilian and nascent military applications. Regulatory frameworks, particularly concerning aviation safety and emissions standards, play a crucial role in shaping product development and market entry. Competitive product substitutes, such as advancements in drone propulsion systems, present a nuanced challenge, though the unique flight characteristics of autogyros maintain their appeal. End-user demographics are diverse, ranging from private recreational pilots and flight schools to specialized commercial operators and potentially military units exploring unconventional aerial platforms. Mergers and Acquisition (M&A) trends, while not as pronounced as in larger aviation sectors, are observed as companies seek to consolidate expertise and expand their product portfolios.

- Market Concentration: Dominated by a few established engine manufacturers, with potential for new entrants in specialized segments.

- Technological Innovation Drivers: Focus on efficiency, emissions reduction, noise abatement, and integration of advanced avionics.

- Regulatory Frameworks: Strict adherence to aviation safety standards (e.g., FAA, EASA) and evolving environmental regulations.

- Competitive Product Substitutes: Advancements in electric propulsion for unmanned aerial vehicles (UAVs) and light sport aircraft.

- End-User Demographics: Recreational pilots, flight training organizations, aerial surveying companies, and emerging military interest.

- M&A Trends: Potential for consolidation among smaller engine manufacturers or strategic acquisitions by larger aviation component suppliers.

Autogyro Engines Growth Trends & Insights

The Autogyro Engines market is poised for substantial expansion, driven by increasing adoption in Civil Use applications and a growing interest from the Military sector. The market size evolution is projected to see a steady upward trajectory, fueled by the inherent advantages of autogyros, including their relative simplicity, cost-effectiveness for certain operations, and ease of operation compared to traditional helicopters. Adoption rates are expected to rise as pilot training becomes more accessible and the versatility of autogyros for various tasks, from surveillance to personal transportation, becomes more widely recognized. Technological disruptions will primarily center on advancements in engine efficiency, material science for lighter and more durable components, and the integration of digital technologies for enhanced performance monitoring and predictive maintenance. Consumer behavior shifts are anticipated, with a growing segment of aviation enthusiasts and professionals seeking cost-effective, versatile aerial solutions. The CAGR is predicted to be robust, with market penetration gradually increasing within the broader light aviation segment.

The market's expansion is underpinned by a consistent demand for reliable and efficient propulsion systems. In the Civil Use segment, the demand stems from recreational flying, flight training schools looking for cost-effective training platforms, and the growing use of autogyros for aerial photography, surveying, and light cargo transport. The inherent safety features, such as the ability to autorotate in case of engine failure, make them an attractive option for new pilots and those seeking lower operational risks. The Military segment, though currently smaller, represents a significant future growth avenue. Autogyros are being explored for reconnaissance, border patrol, and light attack roles due to their low-altitude maneuverability, stealth capabilities (compared to larger aircraft), and reduced logistical footprint. The lower acquisition and operational costs compared to helicopters also make them appealing for specialized military operations.

The technological evolution of autogyro engines is a key driver. Innovations in 2-Stroke Engines continue to focus on optimizing power-to-weight ratios and improving fuel efficiency, making them suitable for lighter autogyro designs. However, the trend is increasingly leaning towards 4-Stroke Engines, which offer superior fuel economy, lower emissions, and longer service intervals, aligning with environmental regulations and operational cost reduction demands. Manufacturers are investing in advanced materials, electronic fuel injection systems, and improved cooling technologies to enhance engine performance and reliability. The shift towards more sophisticated engine management systems will enable greater precision in fuel delivery and ignition timing, leading to optimized power output and reduced wear.

Consumer behavior is also evolving. The increasing availability of online resources, flight simulators, and accessible training programs is lowering the barrier to entry for aspiring autogyro pilots. This is creating a larger pool of potential buyers, driving demand for reliable and affordable engine options. Furthermore, the growing awareness of the environmental impact of aviation is pushing consumers and operators towards more fuel-efficient and lower-emission engine technologies, which will favor advanced 4-stroke designs. The recreational segment is also seeing a rise in demand for engines that offer a good balance of performance, reliability, and ease of maintenance, catering to pilots who may not have extensive mechanical expertise. The overall market penetration is expected to grow as autogyros carve out a distinct niche within the light aviation sector, offering a compelling alternative to fixed-wing aircraft and helicopters for specific applications.

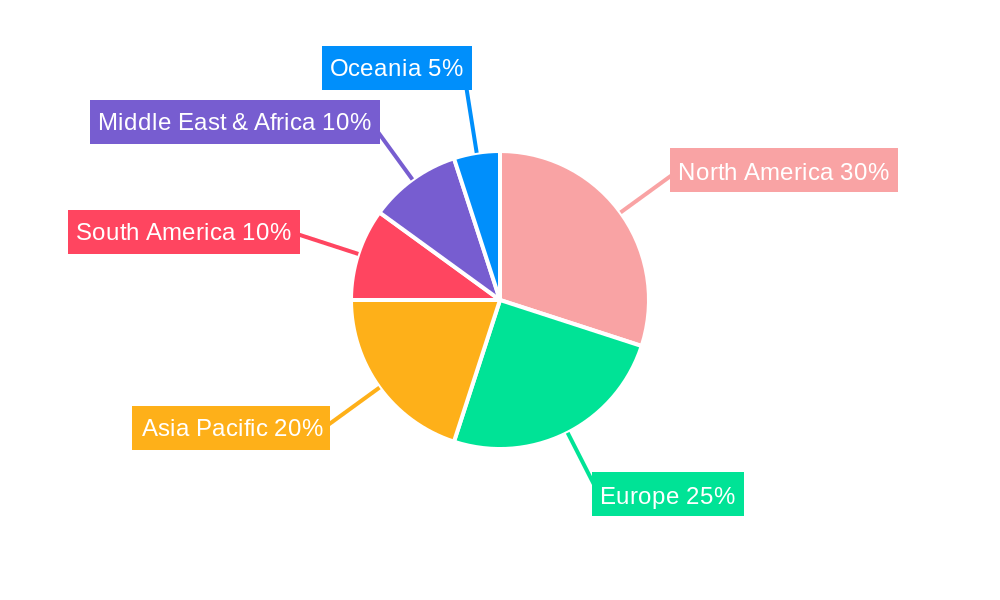

Dominant Regions, Countries, or Segments in Autogyro Engines

The Civil Use application segment is currently the dominant force driving growth in the global Autogyro Engines market. This segment encompasses a broad spectrum of users, from recreational flyers and flight training organizations to commercial operators engaged in aerial surveying, photography, and even light agricultural applications. The inherent safety, relative affordability, and ease of operation of autogyros compared to traditional aircraft make them highly attractive for these purposes. Economic policies in various countries that support light aviation, coupled with the development of robust infrastructure like specialized airfields and training facilities, further bolster the dominance of the Civil Use segment.

North America, particularly the United States, has historically been a leading region for autogyro adoption due to a well-established general aviation culture, favorable regulatory environments for experimental and light aircraft, and a large enthusiast base. This strong foundation in Civil Use applications translates directly into significant demand for autogyro engines. The market share within this region is substantial, driven by a combination of consumer demand for recreational flying and a growing number of commercial entities leveraging autogyros for specialized tasks. The growth potential in North America remains high, with continued investment in product development and market outreach.

In terms of engine types, 4-Stroke Engines are increasingly becoming the segment of choice, gradually surpassing 2-Stroke Engines in market share and growth trajectory. While 2-stroke engines offer a power-to-weight advantage and are simpler in design, the advancements in 4-stroke technology have addressed many of their limitations. Modern 4-stroke autogyro engines offer superior fuel efficiency, lower emissions, quieter operation, and longer service intervals, aligning with evolving environmental regulations and operational cost considerations. This shift towards 4-stroke engines is a significant trend that influences regional market dynamics and manufacturer strategies.

- Dominant Application Segment: Civil Use, driven by recreational flying, training, and niche commercial operations.

- Leading Region: North America, specifically the United States, with its strong general aviation culture.

- Key Drivers in Dominant Region: Favorable regulations, high disposable income, and a large enthusiast base.

- Dominant Engine Type: 4-Stroke Engines, favored for their efficiency, lower emissions, and enhanced reliability.

- Growth Potential: Continued expansion in Civil Use applications, with emerging interest from military sectors.

- Economic Policies: Government support for light aviation, subsidies, and favorable taxation contribute to growth.

- Infrastructure: Development of specialized airfields and pilot training centers enhances market accessibility.

Autogyro Engines Product Landscape

The Autogyro Engines market is characterized by continuous product innovation focused on enhancing performance, reliability, and fuel efficiency. Manufacturers are developing lighter, more compact engines that optimize the power-to-weight ratio essential for autogyro flight characteristics. Advanced materials like composites and high-strength alloys are being integrated to reduce engine weight and improve durability. Unique selling propositions often lie in proprietary combustion technologies, advanced fuel injection systems, and integrated electronic control units (ECUs) for precise engine management. Technological advancements are also geared towards reducing noise pollution and exhaust emissions, making autogyros more environmentally compliant and socially acceptable. Performance metrics such as horsepower, torque, fuel consumption, and service life are key differentiators, with a growing emphasis on long-term operational cost savings and reduced maintenance requirements.

Key Drivers, Barriers & Challenges in Autogyro Engines

The Autogyro Engines market is propelled by several key drivers. Technological advancements in engine design, materials science, and fuel efficiency are making autogyros more accessible and versatile. The growing interest in recreational aviation and the desire for alternative, cost-effective flight solutions are significant market stimulants. Furthermore, the unique operational advantages of autogyros, such as their STOL (Short Take-Off and Landing) capabilities and inherent safety in autorotation, contribute to their appeal. Economic factors, including the pursuit of lower operational costs compared to helicopters, also drive demand.

Key challenges and restraints include the relatively niche market size compared to traditional aircraft engines, which can limit economies of scale in production. Stringent regulatory hurdles for certification and ongoing compliance can increase development costs and time-to-market. Supply chain complexities for specialized components and raw materials can also pose challenges. Intense competition from other light aviation segments and emerging drone technologies presents a continuous pressure. The perception of autogyros as recreational rather than utility aircraft can also be a barrier to broader adoption in commercial and military applications.

Emerging Opportunities in Autogyro Engines

Emerging opportunities in the Autogyro Engines sector are diverse and promising. The increasing demand for sustainable aviation solutions presents a significant opportunity for manufacturers developing electric or hybrid-powered autogyro engines. Expansion into underdeveloped regions with limited traditional aviation infrastructure could see autogyros emerge as a viable mode of transport. The growing use of autogyros for specialized commercial applications, such as precision agriculture, environmental monitoring, and infrastructure inspection, opens up new markets. Furthermore, the evolution of unmanned autogyro systems for cargo delivery and surveillance applications represents a nascent but rapidly growing segment. The development of advanced engine monitoring systems and predictive maintenance solutions also offers opportunities for service-based revenue streams.

Growth Accelerators in the Autogyro Engines Industry

Several catalysts are accelerating growth in the Autogyro Engines industry. Breakthroughs in engine technology, such as the development of lighter, more powerful, and more fuel-efficient engines, are making autogyros more competitive. Strategic partnerships between engine manufacturers and autogyro airframe builders are streamlining product development and market penetration. Market expansion strategies, including increased participation in aviation trade shows, targeted marketing campaigns, and the establishment of robust distributor networks, are vital. The growing recognition of autogyros' unique capabilities by military and government agencies for specific operational needs represents a significant long-term growth driver. Furthermore, advancements in pilot training methodologies and certification processes are democratizing access to autogyro flight.

Key Players Shaping the Autogyro Engines Market

- Lycoming

- Rotax

- Continental Motors

- Jabiru Aircraft

- HKS

- HIRTH ENGINES

Notable Milestones in Autogyro Engines Sector

- 2019: Increased focus on lightweight composite materials in engine manufacturing, leading to improved power-to-weight ratios.

- 2020: Development of advanced electronic fuel injection systems for enhanced fuel efficiency and emissions reduction.

- 2021: Growing interest from military forces in autogyros for reconnaissance and surveillance roles, spurring engine development.

- 2022: Introduction of more stringent noise reduction technologies in new engine models.

- 2023: Advancements in predictive maintenance diagnostics for autogyro engines.

- 2024: Initial exploration and prototyping of hybrid-electric propulsion systems for autogyros.

In-Depth Autogyro Engines Market Outlook

The future of the Autogyro Engines market is exceptionally bright, driven by sustained innovation and expanding applications. Growth accelerators such as advancements in sustainable propulsion technologies, including electric and hybrid powertrains, are poised to redefine the market. Strategic collaborations between engine manufacturers, airframe designers, and technology providers will foster rapid development and market penetration. The increasing demand for autogyros in specialized civilian sectors like precision agriculture and aerial surveying, alongside the latent potential in military applications, provides a strong foundation for long-term growth. As the industry matures, a focus on enhanced pilot training programs and accessible ownership models will further broaden the user base, solidifying the autogyro engine market's trajectory for significant expansion.

Autogyro Engines Segmentation

-

1. Application

- 1.1. Civil Use

- 1.2. Military

-

2. Types

- 2.1. 2-Stroke Engines

- 2.2. 4-Stroke Engines

Autogyro Engines Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Autogyro Engines Regional Market Share

Geographic Coverage of Autogyro Engines

Autogyro Engines REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Civil Use

- 5.1.2. Military

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. 2-Stroke Engines

- 5.2.2. 4-Stroke Engines

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Autogyro Engines Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Civil Use

- 6.1.2. Military

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. 2-Stroke Engines

- 6.2.2. 4-Stroke Engines

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Autogyro Engines Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Civil Use

- 7.1.2. Military

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. 2-Stroke Engines

- 7.2.2. 4-Stroke Engines

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Autogyro Engines Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Civil Use

- 8.1.2. Military

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. 2-Stroke Engines

- 8.2.2. 4-Stroke Engines

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Autogyro Engines Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Civil Use

- 9.1.2. Military

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. 2-Stroke Engines

- 9.2.2. 4-Stroke Engines

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Autogyro Engines Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Civil Use

- 10.1.2. Military

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. 2-Stroke Engines

- 10.2.2. 4-Stroke Engines

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Autogyro Engines Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Civil Use

- 11.1.2. Military

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. 2-Stroke Engines

- 11.2.2. 4-Stroke Engines

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Lycoming

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Rotax

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Continental Motors

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Jabiru Aircraft

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 HKS

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 HIRTH ENGINES

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.1 Lycoming

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Autogyro Engines Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Autogyro Engines Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Autogyro Engines Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Autogyro Engines Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Autogyro Engines Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Autogyro Engines Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Autogyro Engines Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Autogyro Engines Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Autogyro Engines Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Autogyro Engines Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Autogyro Engines Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Autogyro Engines Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Autogyro Engines Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Autogyro Engines Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Autogyro Engines Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Autogyro Engines Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Autogyro Engines Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Autogyro Engines Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Autogyro Engines Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Autogyro Engines Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Autogyro Engines Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Autogyro Engines Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Autogyro Engines Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Autogyro Engines Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Autogyro Engines Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Autogyro Engines Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Autogyro Engines Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Autogyro Engines Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Autogyro Engines Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Autogyro Engines Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Autogyro Engines Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Autogyro Engines Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Autogyro Engines Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Autogyro Engines Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Autogyro Engines Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Autogyro Engines Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Autogyro Engines Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Autogyro Engines Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Autogyro Engines Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Autogyro Engines Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Autogyro Engines Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Autogyro Engines Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Autogyro Engines Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Autogyro Engines Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Autogyro Engines Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Autogyro Engines Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Autogyro Engines Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Autogyro Engines Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Autogyro Engines Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Autogyro Engines Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Autogyro Engines?

The projected CAGR is approximately 8.1%.

2. Which companies are prominent players in the Autogyro Engines?

Key companies in the market include Lycoming, Rotax, Continental Motors, Jabiru Aircraft, HKS, HIRTH ENGINES.

3. What are the main segments of the Autogyro Engines?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Autogyro Engines," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Autogyro Engines report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Autogyro Engines?

To stay informed about further developments, trends, and reports in the Autogyro Engines, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence