Key Insights

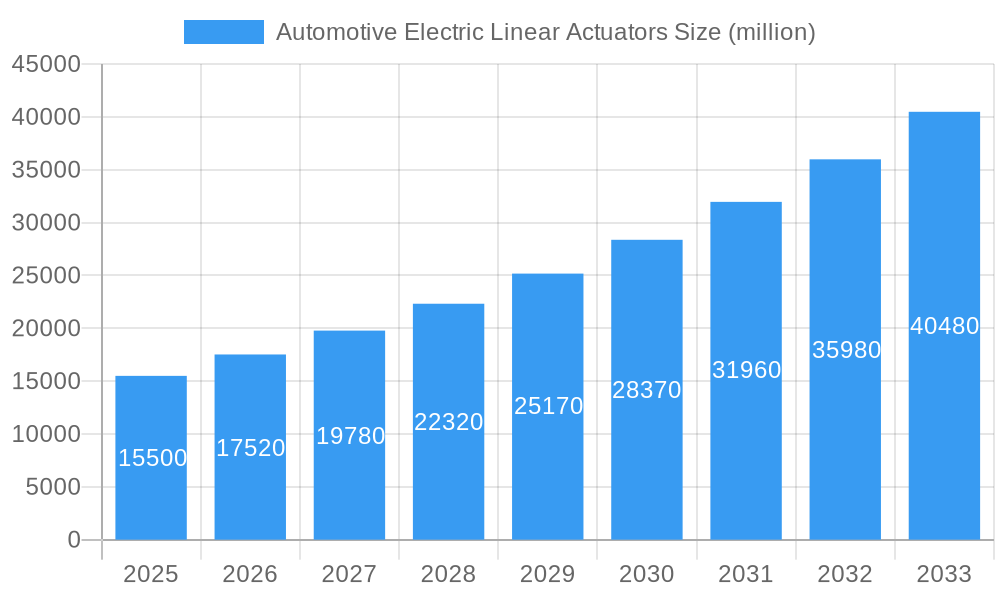

The global Automotive Electric Linear Actuators market is projected to reach USD 67.11 billion by 2025, expanding at a Compound Annual Growth Rate (CAGR) of 6.37%. This growth reflects the increasing integration of advanced actuator technologies across vehicle segments. Key catalysts include the demand for improved fuel efficiency and reduced emissions, driving the adoption of precise electric actuators. The rise in electric and hybrid vehicle production, alongside the development of autonomous driving systems, further fuels market expansion. Additionally, advancements in vehicle safety features, such as sophisticated braking and steering, necessitate reliable electric linear actuators. The Passenger Vehicle segment is expected to lead, driven by consumer demand for comfort and advanced features, while the Commercial Vehicle segment shows significant growth potential due to increased fleet automation.

Automotive Electric Linear Actuators Market Size (In Billion)

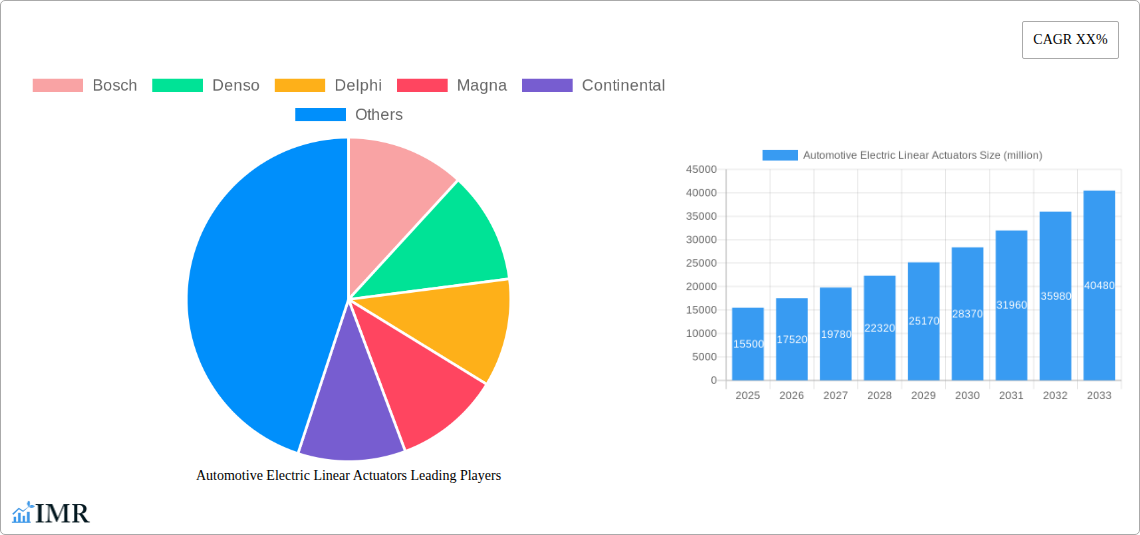

Market dynamics are influenced by trends such as actuator miniaturization and increased power density, enabling more compact and efficient designs. The development of smart actuators with integrated sensors and control electronics is another key trend, facilitating real-time diagnostics and adaptive performance. Challenges include the initial implementation cost compared to traditional systems and the requirement for robust vehicle electrical infrastructure. However, technological advancements and economies of scale are expected to address these cost barriers. The competitive environment features prominent global players such as Bosch, Denso, and Continental, who are actively investing in research and development to innovate and maintain market leadership.

Automotive Electric Linear Actuators Company Market Share

Comprehensive Report: Automotive Electric Linear Actuators Market Dynamics, Trends, and Forecast (2019–2033)

This in-depth report provides a definitive analysis of the global Automotive Electric Linear Actuators market. Spanning from 2019 to 2033, with a base year of 2025, this study offers granular insights into market dynamics, growth trajectories, regional dominance, product innovation, key drivers, emerging opportunities, and the competitive landscape. Our analysis is built upon extensive research, incorporating critical data points for the historical (2019-2024), base (2025), and forecast (2025-2033) periods. We present all quantitative values in million units.

Automotive Electric Linear Actuators Market Dynamics & Structure

The global automotive electric linear actuators market is characterized by a moderately consolidated structure, with key players like Bosch, Denso, Delphi, Magna, Continental, Valeo, Magneti Marelli, Hitachi, Hella, and Mahle holding significant market shares. Technological innovation serves as a primary driver, fueled by the relentless pursuit of enhanced fuel efficiency, reduced emissions, and improved vehicle performance. The increasing integration of advanced driver-assistance systems (ADAS) and the burgeoning electric vehicle (EV) sector are accelerating the adoption of electric linear actuators for a myriad of applications, including advanced braking systems, sophisticated throttle control, and precise fuel injection mechanisms. Regulatory frameworks, particularly stringent emission standards and safety mandates across major automotive hubs like Europe and North America, further propel the demand for these sophisticated components. Competitive product substitutes, while present in some traditional applications, are steadily being outpaced by the superior precision, speed, and energy efficiency offered by electric linear actuators. End-user demographics are shifting towards a greater demand for advanced vehicle features and sustainability, directly influencing actuator development. Merger and acquisition (M&A) trends, though not as prevalent as in some other automotive sectors, are observed as established players seek to consolidate their offerings or acquire specialized technologies to maintain a competitive edge.

- Market Concentration: Moderately consolidated with a few dominant global suppliers.

- Technological Innovation Drivers: Demand for fuel efficiency, emission reduction, ADAS integration, EV proliferation, and enhanced vehicle performance.

- Regulatory Frameworks: Stringent emission standards (e.g., Euro 7, EPA regulations) and safety mandates are key influencers.

- Competitive Product Substitutes: Hydraulic and pneumatic actuators are gradually being replaced in advanced applications.

- End-User Demographics: Growing consumer preference for advanced features, electrification, and eco-friendly vehicles.

- M&A Trends: Strategic acquisitions to enhance technological capabilities and market reach.

Automotive Electric Linear Actuators Growth Trends & Insights

The global Automotive Electric Linear Actuators market is poised for robust growth, driven by escalating demand across both passenger and commercial vehicle segments. The market size is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 7.8% during the forecast period. This expansion is underpinned by several key trends. Firstly, the accelerating shift towards vehicle electrification is a significant catalyst. Electric vehicles (EVs) rely heavily on electric linear actuators for various critical functions, including battery thermal management, power steering, and advanced braking systems, where precision and energy efficiency are paramount. The penetration of EVs is projected to reach 35 million units by 2030, directly translating into increased demand for these components. Secondly, the continuous advancement in automotive technologies, such as ADAS and autonomous driving systems, necessitates the integration of highly precise and responsive actuators for steering, braking, and throttle control. The adoption rate of ADAS features is expected to grow by over 15% annually.

Furthermore, stricter governmental regulations on fuel economy and emissions are compelling original equipment manufacturers (OEMs) to adopt more efficient and precise control systems, where electric linear actuators play a vital role. For instance, the implementation of advanced engine management systems and exhaust gas recirculation (EGR) control, which utilize electric linear actuators, is becoming standard practice. Consumer behavior is also evolving, with an increasing demand for personalized driving experiences, enhanced safety features, and a reduced environmental footprint, all of which are facilitated by sophisticated actuator technologies. The market penetration of electric linear actuators in high-end vehicle models is already substantial, and this trend is progressively filtering down to mid-range and even some entry-level vehicles as costs decrease and production volumes increase.

- Market Size Evolution: Expected to grow significantly, reaching an estimated value of $12.5 billion by 2030.

- Adoption Rates: High adoption in EVs and vehicles equipped with advanced driver-assistance systems.

- Technological Disruptions: Advancements in motor efficiency, control algorithms, and miniaturization of actuators.

- Consumer Behavior Shifts: Growing demand for safety, efficiency, and performance features.

- CAGR: Approximately 7.8% from 2025 to 2033.

- Market Penetration: Increasing penetration in higher vehicle segments and gradual diffusion into mass-market vehicles.

Dominant Regions, Countries, or Segments in Automotive Electric Linear Actuators

The Passenger Vehicle segment is the dominant force driving the growth of the global Automotive Electric Linear Actuators market, accounting for an estimated 72% of the market share in 2025. This dominance is propelled by several interconnected factors. Firstly, the sheer volume of passenger vehicle production globally, exceeding 75 million units annually, provides a massive foundational market. Secondly, the increasing integration of advanced technologies in passenger cars, such as electronic throttle control (ETC), electronic brake-force distribution (EBD), and adaptive cruise control (ACC), directly translates into a higher demand for precise and responsive electric linear actuators. These systems are crucial for enhancing fuel efficiency, improving driving dynamics, and bolstering safety.

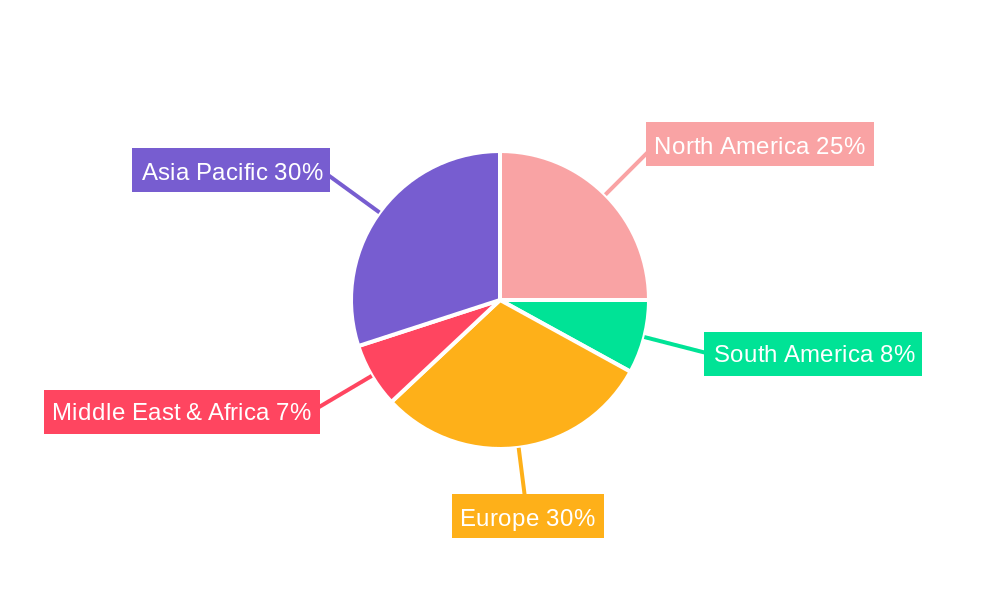

North America, particularly the United States, is a leading region for the adoption of electric linear actuators in passenger vehicles, driven by strong consumer demand for advanced features and a proactive regulatory environment that encourages fuel efficiency improvements. The country's substantial automotive manufacturing base and the presence of major OEMs further contribute to this dominance. The Throttle Actuator sub-segment within passenger vehicles is also a significant contributor to market growth, as it is integral to modern engine management systems for optimizing performance and emissions.

In terms of countries, China stands out as a critical market, not only due to its massive passenger vehicle production and sales but also its rapid adoption of electric vehicles. The Chinese government's strong support for the EV industry, coupled with its ambitious targets for emissions reduction, has spurred significant investment in electric linear actuator technology. The market for electric linear actuators in China is projected to grow at a CAGR of over 9% during the forecast period, outpacing many developed nations. Key drivers in China include government incentives for EV purchases, increasing disposable incomes leading to demand for more feature-rich vehicles, and the localization of production by global automotive suppliers. The country's vast manufacturing capabilities also make it a crucial hub for both production and consumption of these actuators.

- Dominant Segment: Passenger Vehicle (approx. 72% market share in 2025).

- Key Drivers in Passenger Vehicles: High production volumes, integration of ADAS and safety features, demand for fuel efficiency.

- Dominant Sub-Segment: Throttle Actuator (critical for engine performance and emissions control).

- Leading Region: North America (driven by feature demand and regulations).

- Leading Country: China (due to EV growth, government support, and high production volumes).

- Growth Potential in China: Projected CAGR of over 9% during the forecast period.

Automotive Electric Linear Actuators Product Landscape

The product landscape of automotive electric linear actuators is characterized by continuous innovation aimed at improving performance, efficiency, and integration. Key product categories include throttle actuators for precise engine control, fuel injection actuators for optimized fuel delivery, brake actuators for enhanced braking performance and safety systems, and turbo actuators for turbocharger regulation. Emerging product developments focus on miniaturization, increased power density, faster response times, and enhanced durability. For example, advancements in brushless DC motors and sophisticated control algorithms are enabling actuators to achieve higher precision and efficiency. Unique selling propositions often lie in the actuator's ability to integrate seamlessly with vehicle electronics, provide predictive diagnostics, and operate reliably across a wide range of temperature and environmental conditions. The trend towards electromechanical braking systems, where electric linear actuators replace hydraulic components, represents a significant technological leap, offering faster response times and better energy recuperation in EVs.

Key Drivers, Barriers & Challenges in Automotive Electric Linear Actuators

The automotive electric linear actuators market is propelled by several key drivers. The increasing global demand for electric vehicles (EVs) is a primary growth accelerator, as these actuators are integral to many EV systems. Stricter environmental regulations worldwide, mandating lower emissions and improved fuel efficiency, further incentivize the adoption of these precise control mechanisms. Technological advancements in areas like motor efficiency and control electronics are continuously enhancing actuator performance and reducing costs. The growing adoption of Advanced Driver-Assistance Systems (ADAS) and autonomous driving technologies, which require precise actuation for steering, braking, and acceleration, also fuels demand.

Conversely, significant barriers and challenges exist. High initial development and manufacturing costs can be a restraint, particularly for smaller automotive manufacturers or in cost-sensitive markets. The complexity of integration into existing vehicle architectures can also pose challenges, requiring significant engineering effort and compatibility testing. Supply chain disruptions, as witnessed in recent global events, can impact the availability and pricing of critical components, leading to production delays. Intense competition among established players and emerging suppliers can also put pressure on profit margins. Regulatory hurdles related to safety certification and standardization of these complex electromechanical systems can also slow down market penetration.

Emerging Opportunities in Automotive Electric Linear Actuators

Emerging opportunities in the automotive electric linear actuators sector are manifold, driven by evolving automotive trends and consumer preferences. The continued expansion of the electric vehicle (EV) market presents a significant opportunity, particularly in areas such as advanced thermal management systems for batteries and efficient power distribution. The integration of electric linear actuators into sophisticated active aerodynamics systems for improved vehicle efficiency and performance is another burgeoning area. Furthermore, the increasing demand for personalized vehicle experiences is creating opportunities for actuators that enable more dynamic control of various vehicle functions, from seat adjustment to advanced climate control. The development of highly integrated actuator modules that combine multiple functions into a single unit also represents a key innovation pathway, promising reduced complexity and weight. The burgeoning market for retrofitting older vehicles with advanced safety and control features also offers untapped potential.

Growth Accelerators in the Automotive Electric Linear Actuators Industry

Several critical growth accelerators are shaping the long-term trajectory of the automotive electric linear actuators industry. The ongoing paradigm shift towards vehicle electrification remains the most significant catalyst, as electric and hybrid vehicles inherently rely on a greater number of electric actuators compared to their internal combustion engine counterparts. Strategic partnerships and collaborations between actuator manufacturers and major automotive OEMs are crucial for co-developing next-generation technologies and ensuring seamless integration into new vehicle platforms. Furthermore, breakthroughs in material science and manufacturing processes, leading to more cost-effective and higher-performing actuators, will accelerate adoption across a wider range of vehicle segments. The increasing focus on vehicle software and connectivity also opens avenues for actuators that can be controlled and monitored remotely, enabling predictive maintenance and enhanced user experience. Market expansion strategies, targeting emerging automotive markets and niche applications, will also play a vital role in sustained growth.

Key Players Shaping the Automotive Electric Linear Actuators Market

- Bosch

- Denso

- Delphi

- Magna

- Continental

- Valeo

- Magneti Marelli

- Hitachi

- Hella

- Mahle

Notable Milestones in Automotive Electric Linear Actuators Sector

- 2019: Increased adoption of electric throttle control actuators in all new vehicle models in Europe to meet emission standards.

- 2020: Bosch launches a new generation of compact electric brake boosters, enhancing regenerative braking capabilities in EVs.

- 2021: Denso expands its portfolio of electric actuators for automotive thermal management systems to support growing EV demand.

- 2022: Magna invests in advanced actuator technologies for autonomous driving systems.

- 2023: Valeo introduces innovative electric linear actuators for advanced steering systems, improving vehicle agility and safety.

- 2024: Continental showcases its integrated electric actuator solutions for future mobility concepts.

- 2025 (Projected): Widespread integration of electric actuators in advanced battery cooling systems for next-generation EVs.

- 2026 (Projected): Increased adoption of electric actuators in active suspension systems for enhanced ride comfort and handling.

- 2027 (Projected): Emergence of highly intelligent actuators with integrated AI for predictive maintenance and enhanced vehicle diagnostics.

- 2028 (Projected): Significant advancements in electro-mechanical braking systems utilizing high-performance electric linear actuators.

- 2029 (Projected): Growing demand for electric actuators in commercial vehicle applications for emissions control and efficiency.

- 2030 (Projected): Continued innovation in miniaturization and power density of electric linear actuators for diverse automotive applications.

- 2031 (Projected): Increased adoption of electric actuators in advanced driver-assistance systems for enhanced pedestrian and cyclist detection.

- 2032 (Projected): Development of modular actuator systems for easier vehicle assembly and maintenance.

- 2033 (Projected): Electric linear actuators become a standard component across most new vehicle platforms globally.

In-Depth Automotive Electric Linear Actuators Market Outlook

The future outlook for the automotive electric linear actuators market is exceptionally positive, driven by an undeniable confluence of technological advancement, regulatory impetus, and evolving consumer preferences. Growth accelerators such as the sustained surge in electric vehicle adoption, the increasing integration of sophisticated driver-assistance systems, and the continuous push for enhanced fuel efficiency and reduced emissions will continue to propel market expansion. Strategic partnerships between key industry players and automotive manufacturers will be instrumental in driving innovation and ensuring the seamless deployment of advanced actuator technologies. The pursuit of greater miniaturization, improved energy efficiency, and enhanced durability will define the product development landscape. As costs decrease and technological maturity increases, electric linear actuators are poised to become indispensable components across the entire spectrum of automotive applications, from mainstream passenger vehicles to specialized commercial transport, unlocking significant future market potential and strategic opportunities for all stakeholders.

Automotive Electric Linear Actuators Segmentation

-

1. Application

- 1.1. Passenger Vehicle

- 1.2. Commercial Vehicle

-

2. Types

- 2.1. Throttle Actuator

- 2.2. Fuel Injection Actuator

- 2.3. Brake Actuator

- 2.4. Turbo Actuator

- 2.5. Others

Automotive Electric Linear Actuators Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automotive Electric Linear Actuators Regional Market Share

Geographic Coverage of Automotive Electric Linear Actuators

Automotive Electric Linear Actuators REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.37% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Passenger Vehicle

- 5.1.2. Commercial Vehicle

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Throttle Actuator

- 5.2.2. Fuel Injection Actuator

- 5.2.3. Brake Actuator

- 5.2.4. Turbo Actuator

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Automotive Electric Linear Actuators Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Passenger Vehicle

- 6.1.2. Commercial Vehicle

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Throttle Actuator

- 6.2.2. Fuel Injection Actuator

- 6.2.3. Brake Actuator

- 6.2.4. Turbo Actuator

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Automotive Electric Linear Actuators Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Passenger Vehicle

- 7.1.2. Commercial Vehicle

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Throttle Actuator

- 7.2.2. Fuel Injection Actuator

- 7.2.3. Brake Actuator

- 7.2.4. Turbo Actuator

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Automotive Electric Linear Actuators Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Passenger Vehicle

- 8.1.2. Commercial Vehicle

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Throttle Actuator

- 8.2.2. Fuel Injection Actuator

- 8.2.3. Brake Actuator

- 8.2.4. Turbo Actuator

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Automotive Electric Linear Actuators Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Passenger Vehicle

- 9.1.2. Commercial Vehicle

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Throttle Actuator

- 9.2.2. Fuel Injection Actuator

- 9.2.3. Brake Actuator

- 9.2.4. Turbo Actuator

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Automotive Electric Linear Actuators Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Passenger Vehicle

- 10.1.2. Commercial Vehicle

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Throttle Actuator

- 10.2.2. Fuel Injection Actuator

- 10.2.3. Brake Actuator

- 10.2.4. Turbo Actuator

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Automotive Electric Linear Actuators Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Passenger Vehicle

- 11.1.2. Commercial Vehicle

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Throttle Actuator

- 11.2.2. Fuel Injection Actuator

- 11.2.3. Brake Actuator

- 11.2.4. Turbo Actuator

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Bosch

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Denso

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Delphi

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Magna

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Continental

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Valeo

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Magneti Marelli

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Hitachi

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Hella

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Mahle

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Bosch

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Automotive Electric Linear Actuators Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Automotive Electric Linear Actuators Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Automotive Electric Linear Actuators Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Automotive Electric Linear Actuators Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Automotive Electric Linear Actuators Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Automotive Electric Linear Actuators Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Automotive Electric Linear Actuators Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Automotive Electric Linear Actuators Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Automotive Electric Linear Actuators Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Automotive Electric Linear Actuators Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Automotive Electric Linear Actuators Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Automotive Electric Linear Actuators Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Automotive Electric Linear Actuators Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Automotive Electric Linear Actuators Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Automotive Electric Linear Actuators Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Automotive Electric Linear Actuators Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Automotive Electric Linear Actuators Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Automotive Electric Linear Actuators Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Automotive Electric Linear Actuators Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Automotive Electric Linear Actuators Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Automotive Electric Linear Actuators Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Automotive Electric Linear Actuators Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Automotive Electric Linear Actuators Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Automotive Electric Linear Actuators Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Automotive Electric Linear Actuators Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Automotive Electric Linear Actuators Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Automotive Electric Linear Actuators Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Automotive Electric Linear Actuators Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Automotive Electric Linear Actuators Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Automotive Electric Linear Actuators Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Automotive Electric Linear Actuators Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Automotive Electric Linear Actuators Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Automotive Electric Linear Actuators Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Electric Linear Actuators?

The projected CAGR is approximately 6.37%.

2. Which companies are prominent players in the Automotive Electric Linear Actuators?

Key companies in the market include Bosch, Denso, Delphi, Magna, Continental, Valeo, Magneti Marelli, Hitachi, Hella, Mahle.

3. What are the main segments of the Automotive Electric Linear Actuators?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 67.11 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Electric Linear Actuators," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Electric Linear Actuators report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Electric Linear Actuators?

To stay informed about further developments, trends, and reports in the Automotive Electric Linear Actuators, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence