Key Insights

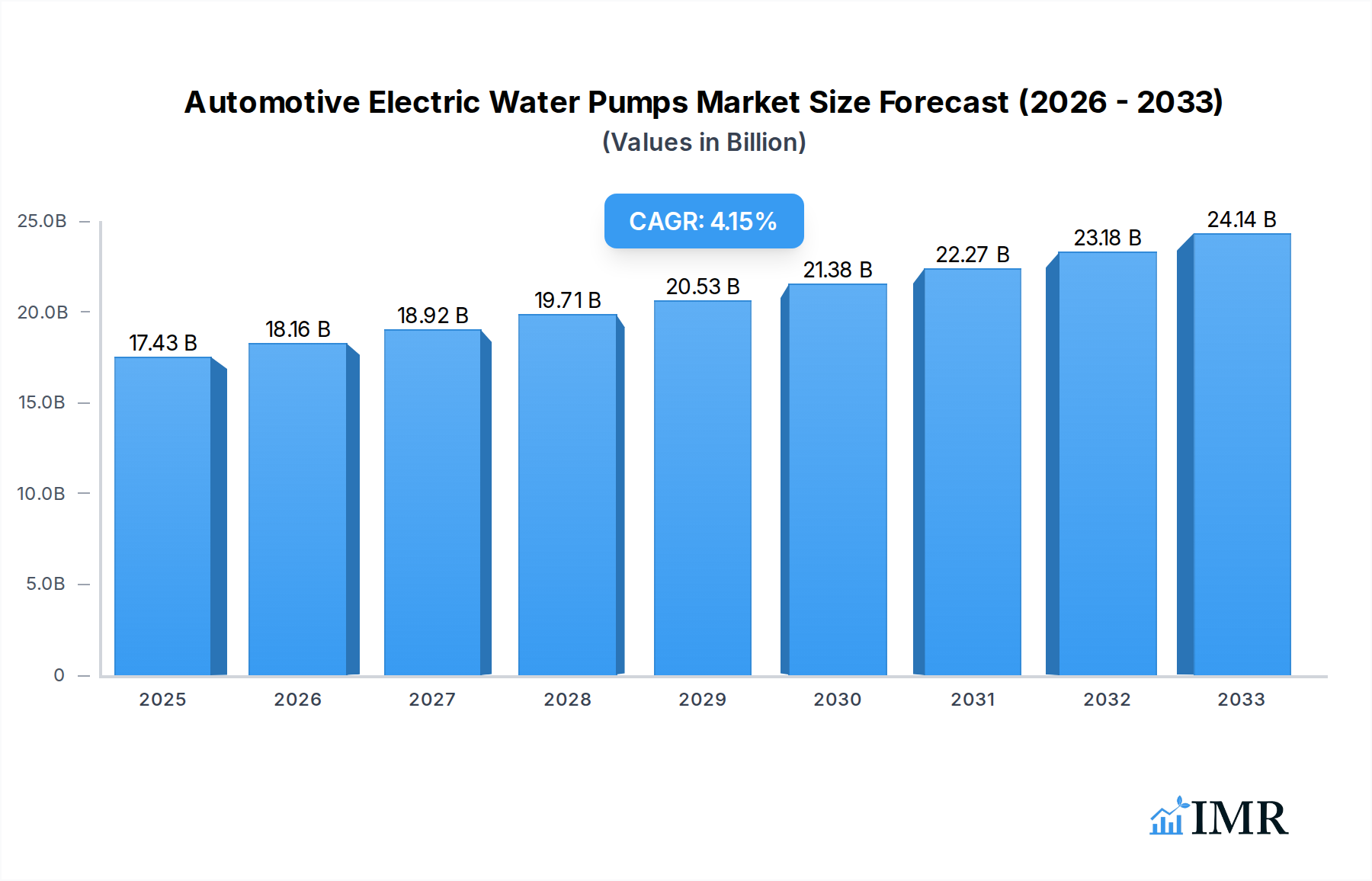

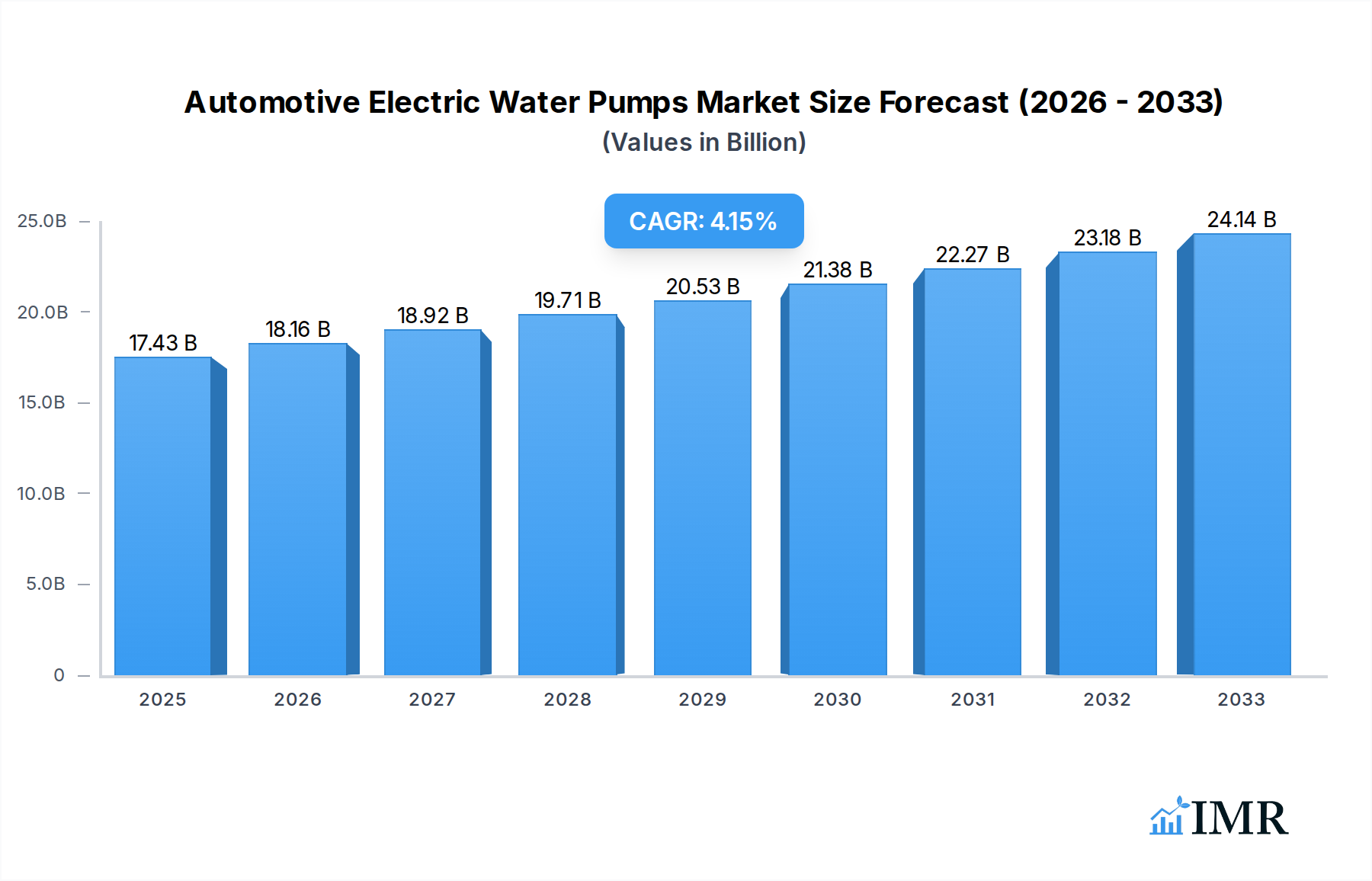

The global Automotive Electric Water Pump market is poised for significant expansion, with an estimated market size of $17.43 billion in 2025, projected to grow at a robust Compound Annual Growth Rate (CAGR) of 4.2% through 2033. This upward trajectory is fueled by several key drivers, most notably the accelerating adoption of electric and hybrid vehicles, which rely heavily on efficient thermal management systems. The increasing demand for advanced engine cooling solutions to meet stringent emission regulations and enhance fuel efficiency further bolsters market growth. Furthermore, the trend towards lighter and more compact vehicle designs necessitates smaller, more adaptable cooling components, favoring the integration of electric water pumps. Technological advancements in motor efficiency, control systems, and material science are also contributing to improved performance and cost-effectiveness, making electric water pumps a more attractive alternative to traditional mechanical pumps.

Automotive Electric Water Pumps Market Size (In Billion)

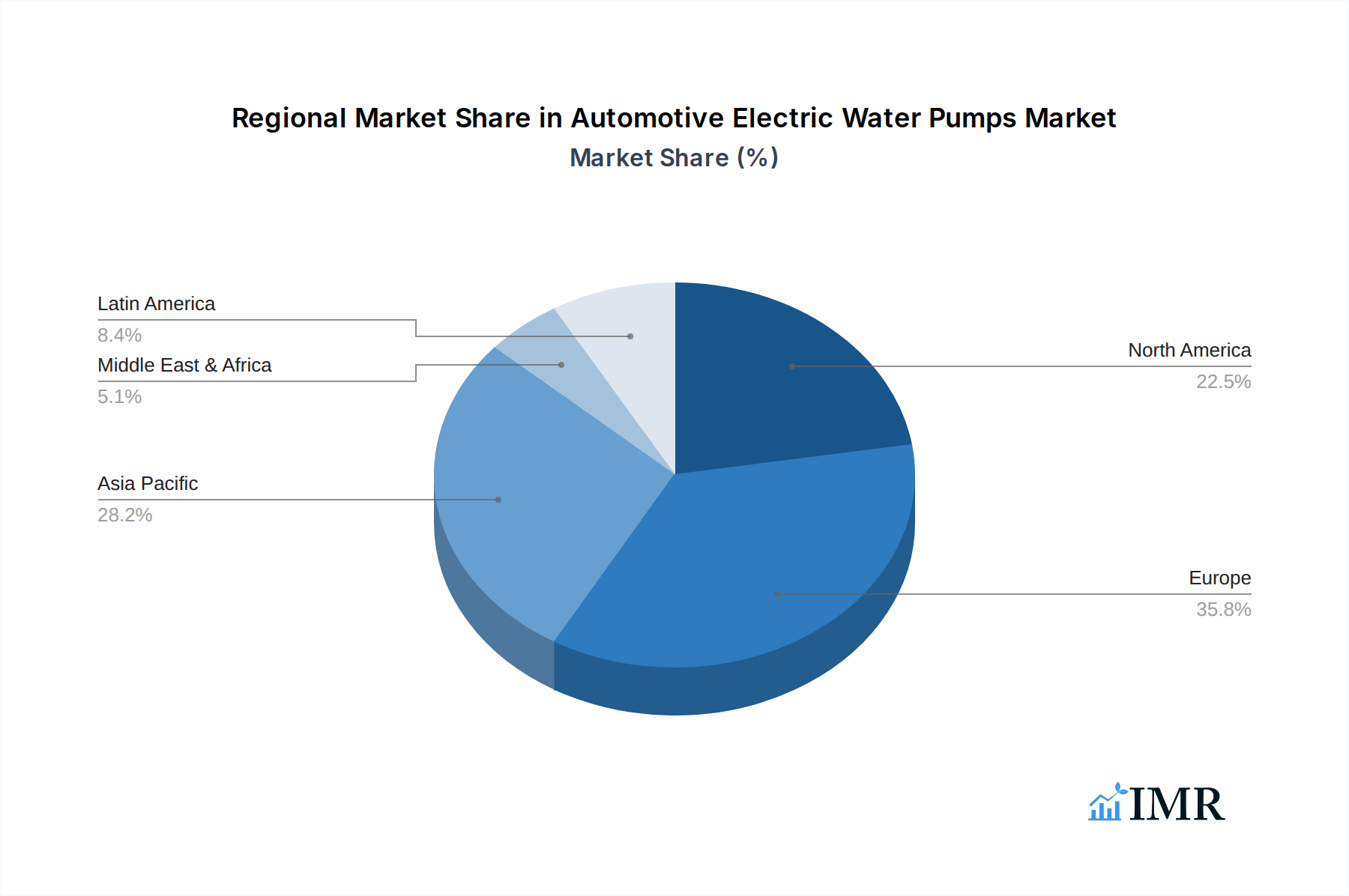

The market's expansion is also influenced by the growing aftermarket demand for reliable and efficient replacement parts, as vehicle parc continues to age. Regions like Europe, with its strong regulatory push towards cleaner mobility and a substantial automotive manufacturing base, represent a critical market segment. Key trends shaping the market include the development of smart water pumps with integrated sensors and predictive maintenance capabilities, as well as the increasing application of electric water pumps in commercial vehicles and heavy-duty applications. While the market enjoys strong growth, it faces certain restraints, including the initial cost of integration for some manufacturers and the need for sophisticated electronic control systems. However, the overwhelming benefits in terms of fuel economy, emissions reduction, and performance optimization are expected to outweigh these challenges, driving sustained market growth. The competitive landscape is characterized by a mix of established automotive component suppliers and specialized electric motor manufacturers, all vying to innovate and capture market share in this dynamic sector.

Automotive Electric Water Pumps Company Market Share

Automotive Electric Water Pumps Market Report: Comprehensive Analysis and Future Outlook (2019–2033)

This in-depth report offers a definitive analysis of the global Automotive Electric Water Pumps market, providing critical insights for stakeholders navigating this rapidly evolving sector. Spanning from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, this study details market dynamics, growth trends, regional dominance, product landscape, key drivers, barriers, emerging opportunities, and growth accelerators. We analyze the intricate relationships within the parent and child markets, offering a holistic view of market structure and competitive forces. High-traffic keywords such as "electric water pump automotive," "EV cooling systems," "thermal management automotive," and "automotive aftermarket pumps" are integrated to maximize search engine visibility. All quantitative data is presented in billions of units.

Automotive Electric Water Pumps Market Dynamics & Structure

The Automotive Electric Water Pumps market exhibits a moderately concentrated structure, with leading players like Robert Bosch GmbH, Continental AG, and Aisin Seiki Co., Ltd. dominating significant market shares, estimated at approximately 25% in 2025. Technological innovation is a primary driver, fueled by the escalating demand for electric vehicles (EVs) and hybrid electric vehicles (HEVs) that necessitate advanced thermal management solutions. Regulatory frameworks, particularly stringent emission standards and the push for fuel efficiency, are indirectly bolstering the adoption of electric water pumps due to their superior efficiency and controllability compared to mechanical counterparts. Competitive product substitutes, primarily traditional mechanical water pumps, are steadily losing ground as manufacturers prioritize lightweighting and optimized cooling for powertrains. End-user demographics are shifting towards a younger, tech-savvy consumer base that values sustainability and advanced automotive features. Mergers and acquisitions (M&A) are a notable trend, with an estimated 5-7 significant deals projected within the forecast period, aimed at consolidating market presence, acquiring specialized technologies, and expanding product portfolios.

- Market Concentration: Moderately concentrated, with top 3 players holding ~25% share in 2025.

- Technological Innovation: Driven by EV/HEV adoption and advanced thermal management needs.

- Regulatory Frameworks: Emission standards and fuel efficiency mandates favor electric solutions.

- Competitive Substitutes: Mechanical water pumps face decline due to performance limitations.

- End-User Demographics: Younger, tech-oriented consumers prioritize efficiency and advanced features.

- M&A Trends: Projected 5-7 significant deals by 2028, focusing on technology acquisition and market expansion.

Automotive Electric Water Pumps Growth Trends & Insights

The global Automotive Electric Water Pumps market is projected for substantial expansion, with its market size estimated to reach approximately $7.20 billion by 2025, and is anticipated to witness a Compound Annual Growth Rate (CAGR) of around 10.5% from 2025 to 2033. This growth is underpinned by a confluence of accelerating factors, primarily the relentless surge in electric vehicle (EV) and hybrid electric vehicle (HEV) production. As the automotive industry pivots towards electrification, the demand for sophisticated thermal management systems, where electric water pumps play a pivotal role, escalates. These pumps are critical for maintaining optimal operating temperatures of batteries, motors, and other critical EV components, thereby enhancing performance, longevity, and overall vehicle efficiency. The adoption rates of electric water pumps are dramatically increasing, moving from niche applications to becoming standard equipment in a majority of new EV and HEV models.

Technological disruptions are reshaping the landscape. Innovations in brushless DC motor technology, advanced sensor integration for precise flow control, and the development of more robust and compact designs are contributing to improved performance and cost-effectiveness. Furthermore, the integration of electric water pumps into integrated thermal management modules is becoming a significant trend, streamlining vehicle architecture and offering synergistic benefits. Consumer behavior is also evolving; there's a growing awareness and demand for vehicles with better energy efficiency and reduced environmental impact. This preference translates into a stronger inclination towards EVs and HEVs, which in turn directly fuels the demand for electric water pumps. The aftermarket segment is also experiencing robust growth, driven by the aging vehicle parc and the need for replacements, especially as older mechanical pumps fail and are replaced with more efficient electric alternatives in a growing number of vehicles. The shift from mechanical to electric water pumps represents a paradigm shift in powertrain cooling, offering unparalleled control and efficiency, which is crucial for meeting the demanding requirements of modern vehicles.

Dominant Regions, Countries, or Segments in Automotive Electric Water Pumps

Asia Pacific, particularly China, is emerging as the dominant region in the Automotive Electric Water Pumps market, propelled by its leadership in global EV production and a robust automotive manufacturing ecosystem. The parent market of the automotive industry in Asia Pacific, estimated to be worth $1.50 trillion in 2025, is seeing its child market for electric water pumps experience unprecedented growth, with a projected market value of $3.10 billion in 2025. This dominance is fueled by a combination of factors including supportive government policies, substantial investments in EV infrastructure, and a rapidly expanding consumer base for electric vehicles. China's "Made in China 2025" initiative and its aggressive targets for electric vehicle adoption have created a fertile ground for electric water pump manufacturers.

Within the Application segment, Battery Thermal Management is driving market growth, estimated to account for approximately 40% of the total market value in 2025. The critical need to maintain optimal battery temperatures for performance, charging speed, and longevity in EVs makes this application paramount. Countries like South Korea and Japan are also significant contributors to regional growth within Asia Pacific, with strong technological prowess in automotive components and a high adoption rate of advanced vehicle technologies.

In the Types segment, Brushless DC (BLDC) Electric Water Pumps are the leading segment, projected to capture around 55% of the market share in 2025. Their superior efficiency, longer lifespan, and precise control capabilities make them indispensable for modern vehicle cooling systems. The supportive economic policies in countries like China, including substantial subsidies for EV manufacturers and buyers, have significantly lowered the barrier to entry for electric vehicles, thus directly boosting the demand for electric water pumps. Furthermore, the robust automotive infrastructure and the presence of major automotive OEMs and Tier-1 suppliers in the region ensure a steady demand and rapid adoption of new technologies. The growth potential within Asia Pacific is immense, driven by both the burgeoning new vehicle market and the increasing demand for replacement parts as the EV fleet matures.

Automotive Electric Water Pumps Product Landscape

The Automotive Electric Water Pump product landscape is characterized by continuous innovation focused on enhanced efficiency, durability, and integration. Leading manufacturers are developing advanced electric water pumps that offer precise, demand-driven cooling, optimizing thermal management for EV batteries, motors, and powertrains. Key product advancements include the use of high-efficiency brushless DC motors, integrated sensors for real-time performance monitoring, and sophisticated control algorithms that enable dynamic flow rate adjustments. These innovations result in significant improvements in vehicle efficiency, reduced emissions, and extended component lifespan. Unique selling propositions revolve around lightweight designs, compact form factors for easier integration, and silent operation. Technological advancements are also geared towards improving sealing technologies to prevent leaks and enhancing resistance to extreme temperatures and vibrations common in automotive environments.

Key Drivers, Barriers & Challenges in Automotive Electric Water Pumps

Key Drivers:

- EV and HEV Production Surge: The rapid increase in electric and hybrid vehicle manufacturing is the primary catalyst, driving demand for sophisticated cooling solutions.

- Stringent Emission Regulations: Global mandates for reduced emissions and improved fuel efficiency necessitate the adoption of more efficient components like electric water pumps.

- Technological Advancements: Innovations in motor technology, sensor integration, and control systems enhance performance and reduce costs, making electric water pumps more competitive.

- Improved Thermal Management: Electric water pumps provide precise control crucial for optimizing battery performance and longevity in EVs, a key consumer concern.

Key Barriers, Challenges & Restraints:

- Higher Initial Cost: Compared to traditional mechanical water pumps, electric variants often have a higher upfront cost, which can be a restraint in price-sensitive markets. The estimated cost difference can be between 20% to 50% in 2025.

- Supply Chain Volatility: Geopolitical factors and raw material availability can impact the cost and supply of critical components for electric water pumps, leading to potential disruptions.

- Integration Complexity: While becoming more streamlined, integrating electric water pumps into existing vehicle architectures can still present engineering challenges for some OEMs.

- Reliability Concerns (Historical): Although rapidly improving, some consumers and repair networks may still hold residual concerns about the long-term reliability of newer electric technologies compared to proven mechanical systems.

Emerging Opportunities in Automotive Electric Water Pumps

Emerging opportunities in the Automotive Electric Water Pumps sector lie in the burgeoning aftermarket for EV components, the development of highly integrated thermal management systems, and expansion into emerging automotive markets with rapidly growing EV adoption. Untapped markets in developing economies are ripe for penetration as EV infrastructure improves and government incentives increase. Innovative applications, such as modular electric water pumps designed for easy replacement and servicing, will cater to the growing EV fleet. Evolving consumer preferences for quieter and more energy-efficient vehicles also present an opportunity for manufacturers to highlight the inherent advantages of electric water pumps. Furthermore, the integration of electric water pumps with advanced predictive maintenance systems for early fault detection and proactive servicing is a significant growth avenue.

Growth Accelerators in the Automotive Electric Water Pumps Industry

The long-term growth of the Automotive Electric Water Pumps industry is significantly accelerated by ongoing breakthroughs in battery technology, leading to higher energy densities and requiring even more sophisticated thermal management. Strategic partnerships between electric water pump manufacturers and battery technology developers are crucial for co-optimizing cooling solutions. The expansion of charging infrastructure globally also indirectly supports EV growth, thereby fueling demand for electric water pumps. Furthermore, advancements in autonomous driving technology, which often involves complex electronic systems that generate significant heat, will necessitate advanced thermal management, further boosting the relevance and demand for electric water pumps. Market expansion strategies focusing on offering a wider range of electric water pump solutions for various vehicle segments, from passenger cars to heavy-duty trucks, will also act as significant growth accelerators.

Key Players Shaping the Automotive Electric Water Pumps Market

- Robert Bosch GmbH

- Continental AG

- Aisin Seiki Co., Ltd.

- Johnson Electric

- Schaeffler AG

- Magna International

- Delphi Technologies

- Denso Corporation

- Rheinmetall Automotive AG

- MAHLE GmbH

- HELLA KGaA Hueck & Co.

- Bühler Motor GmbH

- Gates Corporation

- Webasto

- GMB Corporation

- ACDelco

- Federal-Mogul Holdings Corporation

- Meyle

- AISIN Europe S.A.

- TTI, Inc.

- ZF Friedrichshafen AG

- Nidec Corporation

- NSK Ltd.

- SKF

- NTN Corporation

- Mitsubishi Electric Corporation

- BorgWarner Inc.

- Valeo

- Brose Fahrzeugteile GmbH

- Behr Hella Service GmbH

- FTE Automotive Group

- Wabco Holdings Inc.

- Gentherm Incorporated

- Remy International, Inc.

- IAV Automotive Engineering

- Calsonic Kansei Corporation

- Stant Corporation

- Motorcar Parts of America, Inc.

Notable Milestones in Automotive Electric Water Pumps Sector

- 2021: Robert Bosch GmbH launches its latest generation of highly efficient electric water pumps for heavy-duty vehicles.

- 2022: Continental AG announces a strategic partnership with a major EV manufacturer to supply advanced thermal management modules, including electric water pumps.

- 2022: Aisin Seiki Co., Ltd. expands its production capacity for electric water pumps to meet soaring EV demand in Asia.

- 2023: Johnson Electric introduces a new compact and high-performance electric water pump designed for next-generation EV architectures.

- 2023: Schaeffler AG acquires a significant stake in a thermal management technology startup, enhancing its electric water pump portfolio.

- 2024: Magna International unveils a comprehensive thermal management solution for EVs, featuring integrated electric water pumps.

- 2024: Delphi Technologies showcases its next-generation electric water pump technology with improved diagnostics and control capabilities.

- 2024: Denso Corporation reports record sales for its automotive electric water pumps, driven by OEM demand for EVs.

In-Depth Automotive Electric Water Pumps Market Outlook

The Automotive Electric Water Pumps market is poised for robust and sustained growth, driven by the irreversible shift towards vehicle electrification and the increasing demand for efficient thermal management. The outlook is exceptionally positive, with the market expected to continue its upward trajectory fueled by technological advancements, supportive regulatory environments, and evolving consumer preferences. Growth accelerators such as advancements in battery technology and the expansion of charging infrastructure will further solidify the market's expansion. Strategic opportunities abound for manufacturers to innovate in areas like integrated thermal management systems, aftermarket solutions for the growing EV fleet, and market penetration in emerging economies. The continuous pursuit of performance enhancement, energy efficiency, and sustainability will define the future of this critical automotive component.

Automotive Electric Water Pumps Segmentation

- 1. Application

- 2. Types

Automotive Electric Water Pumps Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Automotive Electric Water Pumps Regional Market Share

Geographic Coverage of Automotive Electric Water Pumps

Automotive Electric Water Pumps REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. IMR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 6. Automotive Electric Water Pumps Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.2. Market Analysis, Insights and Forecast - by Types

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Robert Bosch GmbH

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Continental AG

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Aisin Seiki Co.

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Ltd.

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Johnson Electric

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Schaeffler AG

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Magna International

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Delphi Technologies

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Denso Corporation

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Rheinmetall Automotive AG

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 MAHLE GmbH

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 HELLA KGaA Hueck & Co.

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Bühler Motor GmbH

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.14 Gates Corporation

- 7.1.14.1. Company Overview

- 7.1.14.2. Products

- 7.1.14.3. Company Financials

- 7.1.14.4. SWOT Analysis

- 7.1.15 Webasto

- 7.1.15.1. Company Overview

- 7.1.15.2. Products

- 7.1.15.3. Company Financials

- 7.1.15.4. SWOT Analysis

- 7.1.16 GMB Corporation

- 7.1.16.1. Company Overview

- 7.1.16.2. Products

- 7.1.16.3. Company Financials

- 7.1.16.4. SWOT Analysis

- 7.1.17 ACDelco

- 7.1.17.1. Company Overview

- 7.1.17.2. Products

- 7.1.17.3. Company Financials

- 7.1.17.4. SWOT Analysis

- 7.1.18 Federal-Mogul Holdings Corporation

- 7.1.18.1. Company Overview

- 7.1.18.2. Products

- 7.1.18.3. Company Financials

- 7.1.18.4. SWOT Analysis

- 7.1.19 Meyle

- 7.1.19.1. Company Overview

- 7.1.19.2. Products

- 7.1.19.3. Company Financials

- 7.1.19.4. SWOT Analysis

- 7.1.20 AISIN Europe S.A.

- 7.1.20.1. Company Overview

- 7.1.20.2. Products

- 7.1.20.3. Company Financials

- 7.1.20.4. SWOT Analysis

- 7.1.21 TTI

- 7.1.21.1. Company Overview

- 7.1.21.2. Products

- 7.1.21.3. Company Financials

- 7.1.21.4. SWOT Analysis

- 7.1.22 Inc.

- 7.1.22.1. Company Overview

- 7.1.22.2. Products

- 7.1.22.3. Company Financials

- 7.1.22.4. SWOT Analysis

- 7.1.23 ZF Friedrichshafen AG

- 7.1.23.1. Company Overview

- 7.1.23.2. Products

- 7.1.23.3. Company Financials

- 7.1.23.4. SWOT Analysis

- 7.1.24 Nidec Corporation

- 7.1.24.1. Company Overview

- 7.1.24.2. Products

- 7.1.24.3. Company Financials

- 7.1.24.4. SWOT Analysis

- 7.1.25 NSK Ltd.

- 7.1.25.1. Company Overview

- 7.1.25.2. Products

- 7.1.25.3. Company Financials

- 7.1.25.4. SWOT Analysis

- 7.1.26 SKF

- 7.1.26.1. Company Overview

- 7.1.26.2. Products

- 7.1.26.3. Company Financials

- 7.1.26.4. SWOT Analysis

- 7.1.27 NTN Corporation

- 7.1.27.1. Company Overview

- 7.1.27.2. Products

- 7.1.27.3. Company Financials

- 7.1.27.4. SWOT Analysis

- 7.1.28 Mitsubishi Electric Corporation

- 7.1.28.1. Company Overview

- 7.1.28.2. Products

- 7.1.28.3. Company Financials

- 7.1.28.4. SWOT Analysis

- 7.1.29 BorgWarner Inc.

- 7.1.29.1. Company Overview

- 7.1.29.2. Products

- 7.1.29.3. Company Financials

- 7.1.29.4. SWOT Analysis

- 7.1.30 Valeo

- 7.1.30.1. Company Overview

- 7.1.30.2. Products

- 7.1.30.3. Company Financials

- 7.1.30.4. SWOT Analysis

- 7.1.31 Brose Fahrzeugteile GmbH

- 7.1.31.1. Company Overview

- 7.1.31.2. Products

- 7.1.31.3. Company Financials

- 7.1.31.4. SWOT Analysis

- 7.1.32 Behr Hella Service GmbH

- 7.1.32.1. Company Overview

- 7.1.32.2. Products

- 7.1.32.3. Company Financials

- 7.1.32.4. SWOT Analysis

- 7.1.33 FTE Automotive Group

- 7.1.33.1. Company Overview

- 7.1.33.2. Products

- 7.1.33.3. Company Financials

- 7.1.33.4. SWOT Analysis

- 7.1.34 Wabco Holdings Inc.

- 7.1.34.1. Company Overview

- 7.1.34.2. Products

- 7.1.34.3. Company Financials

- 7.1.34.4. SWOT Analysis

- 7.1.35 Gentherm Incorporated

- 7.1.35.1. Company Overview

- 7.1.35.2. Products

- 7.1.35.3. Company Financials

- 7.1.35.4. SWOT Analysis

- 7.1.36 Remy International

- 7.1.36.1. Company Overview

- 7.1.36.2. Products

- 7.1.36.3. Company Financials

- 7.1.36.4. SWOT Analysis

- 7.1.37 Inc.

- 7.1.37.1. Company Overview

- 7.1.37.2. Products

- 7.1.37.3. Company Financials

- 7.1.37.4. SWOT Analysis

- 7.1.38 IAV Automotive Engineering

- 7.1.38.1. Company Overview

- 7.1.38.2. Products

- 7.1.38.3. Company Financials

- 7.1.38.4. SWOT Analysis

- 7.1.39 Calsonic Kansei Corporation

- 7.1.39.1. Company Overview

- 7.1.39.2. Products

- 7.1.39.3. Company Financials

- 7.1.39.4. SWOT Analysis

- 7.1.40 Stant Corporation

- 7.1.40.1. Company Overview

- 7.1.40.2. Products

- 7.1.40.3. Company Financials

- 7.1.40.4. SWOT Analysis

- 7.1.41 Motorcar Parts of America

- 7.1.41.1. Company Overview

- 7.1.41.2. Products

- 7.1.41.3. Company Financials

- 7.1.41.4. SWOT Analysis

- 7.1.42 Inc.

- 7.1.42.1. Company Overview

- 7.1.42.2. Products

- 7.1.42.3. Company Financials

- 7.1.42.4. SWOT Analysis

- 7.1.1 Robert Bosch GmbH

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Automotive Electric Water Pumps Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: Automotive Electric Water Pumps Share (%) by Company 2025

List of Tables

- Table 1: Automotive Electric Water Pumps Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Automotive Electric Water Pumps Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Automotive Electric Water Pumps Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Automotive Electric Water Pumps Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Automotive Electric Water Pumps Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Automotive Electric Water Pumps Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Automotive Electric Water Pumps Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Germany Automotive Electric Water Pumps Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: France Automotive Electric Water Pumps Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Italy Automotive Electric Water Pumps Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 11: Spain Automotive Electric Water Pumps Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Automotive Electric Water Pumps Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 13: Belgium Automotive Electric Water Pumps Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Sweden Automotive Electric Water Pumps Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Norway Automotive Electric Water Pumps Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Poland Automotive Electric Water Pumps Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 17: Denmark Automotive Electric Water Pumps Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Electric Water Pumps?

The projected CAGR is approximately 4.2%.

2. Which companies are prominent players in the Automotive Electric Water Pumps?

Key companies in the market include Robert Bosch GmbH, Continental AG, Aisin Seiki Co., Ltd., Johnson Electric, Schaeffler AG, Magna International, Delphi Technologies, Denso Corporation, Rheinmetall Automotive AG, MAHLE GmbH, HELLA KGaA Hueck & Co., Bühler Motor GmbH, Gates Corporation, Webasto, GMB Corporation, ACDelco, Federal-Mogul Holdings Corporation, Meyle, AISIN Europe S.A., TTI, Inc., ZF Friedrichshafen AG, Nidec Corporation, NSK Ltd., SKF, NTN Corporation, Mitsubishi Electric Corporation, BorgWarner Inc., Valeo, Brose Fahrzeugteile GmbH, Behr Hella Service GmbH, FTE Automotive Group, Wabco Holdings Inc., Gentherm Incorporated, Remy International, Inc., IAV Automotive Engineering, Calsonic Kansei Corporation, Stant Corporation, Motorcar Parts of America, Inc..

3. What are the main segments of the Automotive Electric Water Pumps?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3900.00, USD 5850.00, and USD 7800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Electric Water Pumps," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Electric Water Pumps report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Electric Water Pumps?

To stay informed about further developments, trends, and reports in the Automotive Electric Water Pumps, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence